|

市場調查報告書

商品編碼

2071382

熱泵市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。Heat Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

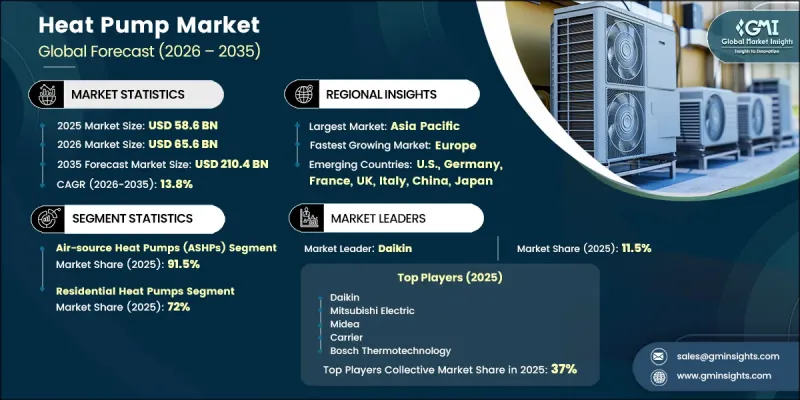

全球熱泵市場預計到 2025 年將達到 586 億美元,到 2035 年將以 13.8% 的複合年成長率成長,達到 2,104 億美元。

市場擴張的驅動力來自日益嚴格的碳排放減排目標、對能源價格和供應穩定性的日益關注,以及熱泵效率的不斷提升。北美、歐洲和亞太地區的各國政府正透過法律規範和節能措施推動建築電氣化,為熱泵的部署創造了有利環境。變頻和變速壓縮機系統的技術進步顯著提升了其在寒冷氣候下的性能,即使在以前被認為不適合部署熱泵的地區也能可靠運作。更嚴格的能源性能標準和建築法規正在加速傳統暖氣系統的更新換代。此外,人們對永續供暖和製冷解決方案的日益關注,以及對住宅、商業和公共建築基礎設施的持續投資,都為市場的長期成長提供了支撐。建築電氣化的趨勢持續惠及整個產業,熱泵作為高效暖通空調控制解決方案,在不同的區域市場中越來越受到青睞。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 586億美元 |

| 預測金額 | 2104億美元 |

| 複合年成長率 | 13.8% |

預計到2025年,空氣源熱泵市佔率將達到91.5%,並在2035年之前維持14.4%的複合年成長率,成為所有產品細分市場中成長最快的領域。空氣源熱泵系統在市場上的強勢地位源於其相比其他技術更低的安裝成本、與現有建築基礎設施的廣泛兼容性以及更簡便的部署要求。無需進行大規模場地準備即可提供高效的供暖和製冷,這一優勢持續推動著空氣源熱泵在住宅和商業應用中的廣泛普及。

預計到2025年,商業用途領域將佔市場佔有率的25.5%,並在2026年至2035年間以13.7%的複合年成長率成長。該領域的需求成長主要受以下因素驅動:企業日益關注營運中的能源效率、永續性目標以及對環境績效指標的遵守。各公司正擴大將熱泵技術與先進的建築能源管理系統和可再生能源設施相結合,以最佳化能源消耗並降低長期營運成本。

預計到2025年,北美熱泵市佔率將達到18.5%,並在2035年之前以8.7%的複合年成長率成長。該地區持續成長的驅動力包括:節能供暖解決方案的日益普及、電氣化舉措的推進以及住宅和商業建築中先進壓縮機技術的廣泛應用。消費者意識的提高、有利的政策框架以及供暖基礎設施的持續現代化,都全部區域市場的永續發展做出了貢獻。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 原物料供應及採購分析

- 供應鏈韌性與風險因素

- 配電網路分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 影響產業的因素

- 成長促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 熱泵成本結構分析

- 價格趨勢分析

- 依產品

- 按地區

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧最佳化生產

- 預測性維護和故障檢測

- 新機會和趨勢

- 投資分析及未來展望

- 永續發展措施與工業4.0的融合

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 主要進展

- 重要合作夥伴關係和合作

- 主要併購活動

- 產品創新和新產品發布

- 市場擴大策略

- 競爭定位矩陣

第5章 市場規模及預測:依產品分類,2022-2035年

- 空氣源

- 地熱

- 水源

第6章 市場規模與預測:依應用領域分類,2022-2035年

- 住宅

- 商業

- 產業

第7章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 奧地利

- 挪威

- 丹麥

- 芬蘭

- 法國

- 德國

- 義大利

- 瑞士

- 西班牙

- 瑞典

- 英國

- 荷蘭

- 亞太地區

- 中國

- 日本

- 澳洲

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 土耳其

- 南非

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

第8章:公司簡介

- Bosch Thermotechnology Corp.

- Carrier

- DAIKIN INDUSTRIES, Ltd.

- Finn Geotherm UK Limited

- FUJITSU GENERAL

- Glen Dimplex Group

- Gree Electric Appliances

- Johnson Controls

- Kensa Heat Pumps

- Lennox

- LG Electronics

- Lochinvar

- Midea

- Mitsubishi Electric Corporation

- NIBE Industrier AB

- OCHSNER

- Panasonic Corporation

- SAMSUNG

- STIEBEL ELTRON GmbH & Co. KG

- Trane

- Vaillant Group

- WOLF GmbH

The Global Heat Pump Market generated USD 58.6 billion in 2025 and is estimated to grow at a CAGR of 13.8% to reach USD 210.4 billion by 2035.

Market expansion is fueled by increasingly stringent carbon reduction targets, rising concerns regarding energy affordability and supply security, and continuous advancements in heat pump efficiency. Governments across North America, Europe, and Asia Pacific are promoting building electrification through regulatory frameworks and energy-efficiency initiatives, creating a favorable environment for heat pump adoption. Technological progress in inverter-based and variable-speed compressor systems has significantly improved performance in colder climates, enabling reliable operation in regions that were previously considered unsuitable for heat pump deployment. Enhanced energy performance standards and stricter building regulations are accelerating replacement cycles for conventional heating systems. In addition, growing awareness of sustainable heating and cooling solutions, combined with ongoing investments in residential, commercial, and institutional infrastructure, is supporting long-term market growth. The industry continues to benefit from the transition toward electrified buildings, making heat pumps an increasingly preferred solution for efficient climate control across diverse geographic markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $58.6 Billion |

| Forecast Value | $210.4 Billion |

| CAGR | 13.8% |

Air-source heat pumps segment held a 91.5% share in 2025 and projected to grow at a CAGR of 14.4% through 2035, the highest growth rate among all product segments. The strong market position of air-source systems is attributed to their lower installation costs compared to alternative technologies, broad compatibility with existing building infrastructure, and simplified deployment requirements. Their ability to deliver efficient heating and cooling without extensive site preparation continues to support widespread adoption across residential and commercial applications.

The commercial applications segment held a 25.5% share in 2025 and is forecast to grow at a CAGR of 13.7% during 2026-2035. Demand within this segment is being driven by increasing focus on operational energy efficiency, sustainability objectives, and compliance with environmental performance targets. Businesses are increasingly integrating heat pump technologies with advanced building energy management systems and renewable energy installations to optimize energy consumption and reduce long-term operating expenses.

North America Heat Pump Market accounted for 18.5% share in 2025 and is expected to grow at a CAGR of 8.7% through 2035. The region continues to benefit from growing adoption of energy-efficient heating solutions, expanding electrification initiatives, and increasing penetration of advanced compressor technologies across residential and commercial buildings. Rising consumer awareness, supportive policy frameworks, and continued modernization of heating infrastructure are contributing to sustained market development throughout the region.

Key participants operating in the global heat pump market include Panasonic Corporation, Samsung, Trane, Carrier, Johnson Controls, LG Electronics, Bosch Thermotechnology Corp., Daikin Industries, Ltd., Mitsubishi Electric Corporation, and Midea. Companies operating in the heat pump market are strengthening their competitive positions through continuous investment in product innovation, energy-efficiency enhancements, and expansion of smart connectivity capabilities. Manufacturers are focusing on developing advanced inverter-driven systems, improving cold-climate performance, and integrating digital monitoring features to enhance user experience and system efficiency. Strategic partnerships with distributors, installers, and construction firms are helping companies expand market reach and improve customer access. Businesses are also increasing investments in regional manufacturing facilities and supply chain optimization to improve delivery capabilities and reduce costs. In addition, market participants are expanding their presence in emerging economies, introducing environmentally friendly refrigerants, and aligning product portfolios with evolving energy-efficiency regulations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Supply chain resilience & risk factors

- 3.1.3 Distribution network analysis

- 3.2 Regulatory landscape

- 3.2.1 North America

- 3.2.2 Europe

- 3.2.3 Asia Pacific

- 3.2.4 Middle East & Africa

- 3.2.5 Latin America

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of heat pumps (Solution Core)

- 3.8 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.8.1 By product (Driven by Primary Research)

- 3.8.2 By region (Driven by Primary Research)

- 3.9 Impact of AI & Generative AI on the market (Solution Core)

- 3.9.1 AI-Driven production optimization (Solution Core)

- 3.9.2 Predictive maintenance & fault detection (Solution Core)

- 3.10 Emerging opportunities & trends

- 3.11 Investment analysis & future prospects

- 3.12 Sustainability initiatives & industry 4.0 integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Key developments

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive positioning matrix

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 Air source

- 5.3 Ground source

- 5.4 Water source

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Austria

- 7.3.2 Norway

- 7.3.3 Denmark

- 7.3.4 Finland

- 7.3.5 France

- 7.3.6 Germany

- 7.3.7 Italy

- 7.3.8 Switzerland

- 7.3.9 Spain

- 7.3.10 Sweden

- 7.3.11 UK

- 7.3.12 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 Australia

- 7.4.4 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 Turkey

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 Bosch Thermotechnology Corp.

- 8.2 Carrier

- 8.3 DAIKIN INDUSTRIES, Ltd.

- 8.4 Finn Geotherm UK Limited

- 8.5 FUJITSU GENERAL

- 8.6 Glen Dimplex Group

- 8.7 Gree Electric Appliances

- 8.8 Johnson Controls

- 8.9 Kensa Heat Pumps

- 8.10 Lennox

- 8.11 LG Electronics

- 8.12 Lochinvar

- 8.13 Midea

- 8.14 Mitsubishi Electric Corporation

- 8.15 NIBE Industrier AB

- 8.16 OCHSNER

- 8.17 Panasonic Corporation

- 8.18 SAMSUNG

- 8.19 STIEBEL ELTRON GmbH & Co. KG

- 8.20 Trane

- 8.21 Vaillant Group

- 8.22 WOLF GmbH

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測

熱泵市場:按類型、技術、容量、安裝方式、應用領域、最終用戶和分銷管道分類-2026-2032年全球市場預測 熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

熱泵式乾衣機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球農作物乾燥熱泵市場報告

2026年全球農作物乾燥熱泵市場報告 熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類

熱泵市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按最終用戶和技術分類 工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業熱泵市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測德國熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)新加坡熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)西班牙熱泵市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)