|

市場調查報告書

商品編碼

1959303

2026 年至 2035 年機能性食品市場中後生元成分的成長要素、產業趨勢和預測。Postbiotic Ingredients in Functional Foods Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

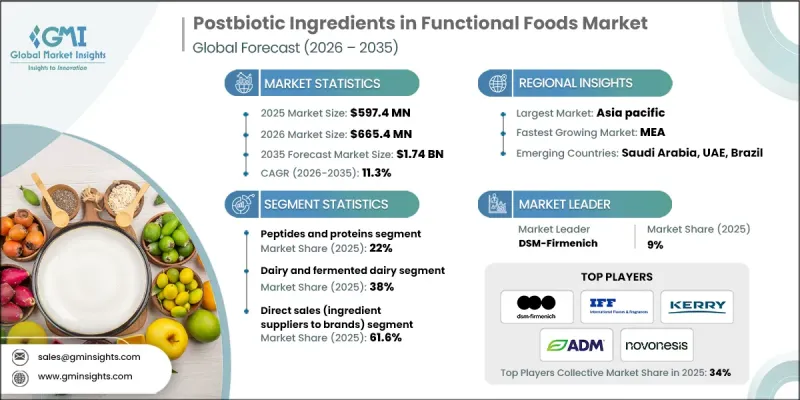

2025 年,全球機能性食品用後生元成分市場價值為 5.974 億美元,預計到 2035 年將以 11.3% 的複合年成長率成長至 17.4 億美元。

這一成長主要得益於消費者對腸道健康和微生物組科學的日益關注,以及對穩定性高、易於配製的功能性成分需求的不斷成長。後生元成分使食品生產商能夠在不製作流程和儲存過程中維持活性菌群所帶來的配方難題的情況下,提供與微生物組相關的益處。因此,越來越多的品牌開始採用後生元作為益生菌的低風險替代品,同時保持其在消化健康和免疫支持方面的強大市場地位。關鍵地區的監管政策細化以及以營養價值和便利性為優先考慮的食品形式的融合,正在加速產品創新。消費者對發酵食品和有益腸道產品的廣泛興趣進一步增強了市場需求,生產商正在開發涵蓋多個品類的微生物組支持配方。耐熱後生元成分的應用正在不斷增加,尤其是在傳統活性菌叢穩定性難以保證的應用中。消費者對消化健康的日益成長且可量化的興趣將繼續支撐市場的長期擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 5.974億美元 |

| 預測金額 | 17.4億美元 |

| 複合年成長率 | 11.3% |

預計到2025年,胜肽和蛋白質細分市場將佔據22%的市場佔有率,並在2035年之前以12.2%的複合年成長率成長。原料供應商正從提供單一成分轉向提供多功能混合物,這些混合物結合了胜肽、酵素、細胞組分、維生素和其他生物活性化合物。這些解決方案以標準化標籤為目標,定位為配料,旨在提供穩定的效力、更佳的風味和更高的生產效率。在商業策略中,跨品類相容性日益重要,這使得這些產品能夠應用於乳製品、飲料和零食配方,同時支持差異化的功能性宣稱,並輔以穩定性檢驗和文件記錄。

預計到2025年,乳製品和發酵乳製品市場佔有率將達到38%,到2035年將以10.9%的複合年成長率成長。該細分市場之所以維持核心地位,是因為其發酵帶來的健康益處以及與消費者既有消費習慣的天然親和性。製造商正在將後生元成分添加到各種乳製品中,以提高配方穩定性,確保產品功能始終如一,同時又不影響消費者的感官體驗。在維持傳統口味的同時,增強消化健康訊息,此優勢持續推動著此品類的市場成長。

預計到2025年,北美機能性食品用後生元成分市場規模將達到1.569億美元,到2035年將達到4.604億美元,主要得益於主流腸道健康機能性食品的強勁創新。美國憑藉其成熟的機能性食品品牌和原料供應商生態系統,正引領區域成長。市場擴張的促進因素包括:膳食補充劑概念在食品飲料行業的跨界應用、消化健康產品零售分銷網路的拓展,以及消費者對便捷攜帶式產品形式的高度認可。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

(註:貿易統計數據僅涵蓋主要國家。)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依原料類型分類,2022-2035年

- 短鏈脂肪酸

- 細胞壁成分

- 胞外多醣

- 酵素

- 胜肽和蛋白質

- 維生素和生物活性物質

- 其他

第6章 市場估價與預測:依食品類型分類,2022-2035年

- 乳製品及發酵乳製品

- 優格

- Kefir

- 發酵乳類飲料

- 起司和發酵乳甜點

- 不含乳製品的飲料

- 功能水

- 果汁和果汁飲料

- 即飲茶和咖啡

- 植物發酵飲料

- 烘焙食品和穀物

- 麵包和麵包卷

- 早餐用麥片穀類和Granola

- 營養棒

- 糖果甜點

- 軟糖和果凍

- 巧克力

- 糖果和潤喉糖

- 嬰幼兒營養食品

- 嬰兒奶粉

- 後續牛奶

- 嬰兒食品

- 醫學和臨床營養

- 其他

第7章 市場估價與預測:依通路分類,2022-2035年

- 直接銷售(從原料供應商到品牌公司)

- 批發商/代理商

- 線上B2B平台

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- IFF(International Flavors &Fragrances)

- DSM-Firmenich

- ADM

- Kerry Group

- BASF

- Evonik

- Novonesis

- DuPont(IFF legacy Danisco)

- Cargill

- Givaudan

The Global Postbiotic Ingredients in Functional Foods Market was valued at USD 597.4 million in 2025 and is estimated to grow at a CAGR of 11.3% to reach USD 1.74 billion by 2035.

Growth is driven by rising consumer awareness of gut health and microbiome science, alongside increasing demand for stable and easy-to-formulate functional ingredients. Postbiotic ingredients offer food manufacturers the ability to deliver microbiome-related benefits without the formulation challenges linked to maintaining live cultures during processing and shelf life. As a result, brands are increasingly turning to postbiotics as a lower-risk alternative to probiotics while maintaining strong positioning around digestive health and immune support. Regulatory clarity in key regions, combined with the convergence of nutrition and convenience-driven food formats, is accelerating product innovation. Broader interest in fermented and gut-friendly products has further strengthened demand, with manufacturers developing microbiome-supportive formulations across multiple categories. Heat-stable postbiotic ingredients are gaining traction, particularly in applications where traditional live cultures face stability limitations. Quantifiable consumer interest in digestive wellness continues to support long-term market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $597.4 Million |

| Forecast Value | $1.74 Billion |

| CAGR | 11.3% |

The peptides and proteins segment accounted for 22% share in 2025 and is expected to grow at a CAGR of 12.2% through 2035. Ingredient suppliers are moving beyond single-component offerings toward multifunctional blends that combine peptides, enzymes, cell fractions, vitamins, and additional bioactive compounds. These solutions are positioned as standardized, label-friendly ingredients that deliver consistent potency, improved flavor profiles, and greater manufacturing efficiency. Commercial strategies increasingly emphasize cross-category compatibility, enabling use across dairy, beverage, and snack formulations while supporting differentiated functional claims backed by stability validation and documentation.

The dairy and fermented dairy applications segment held 38% share in 2025 and is forecast to grow at a CAGR of 10.9% by 2035. This segment remains central due to its natural alignment with fermentation-based health narratives and established consumption habits. Manufacturers are incorporating postbiotic ingredients into a wide range of dairy-based products to enhance formulation stability and ensure consistent functional positioning without compromising sensory expectations. The ability to reinforce digestive health messaging while maintaining traditional taste profiles continues to strengthen adoption within this category.

North America Postbiotic Ingredients in Functional Foods Market accounted for USD 156.9 million in 2025 and is projected to reach USD 460.4 million by 2035, supported by strong innovation in mainstream gut-health functional foods. The United States leads regional growth through a well-developed ecosystem of functional food brands and ingredient suppliers. Market expansion benefits from the crossover of dietary supplement concepts into food and beverage applications, widespread retail availability of digestive wellness products, and high consumer acceptance of convenient, on-the-go functional formats.

Key companies operating in the Global Postbiotic Ingredients in Functional Foods Market include DSM-Firmenich, IFF (International Flavors & Fragrances), ADM, Kerry Group, BASF, Novonesis, Cargill, Givaudan, Evonik, and DuPont (IFF legacy Danisco). Companies in the Postbiotic Ingredients in Functional Foods Market are strengthening their competitive position through targeted research and development, strategic partnerships with food manufacturers, and portfolio diversification. Many players are investing in clinically supported formulations to substantiate claims related to digestive and immune health. Expanding multifunctional ingredient blends enhances cross-category application flexibility and improves formulation efficiency for brand owners. Firms are also prioritizing regulatory alignment and clean-label positioning to meet evolving consumer expectations. Strategic acquisitions and collaborations are enabling companies to broaden their geographic reach and accelerate innovation pipelines.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 ingredient type

- 2.2.3 Food type

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By ingredient type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Short-chain fatty acids

- 5.3 Cell wall components

- 5.4 Exopolysaccharides

- 5.5 Enzymes

- 5.6 Peptides and proteins

- 5.7 Vitamins and bioactives

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Food type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy and fermented dairy

- 6.2.1 Yogurt

- 6.2.2 Kefir

- 6.2.3 Cultured milk drinks

- 6.2.4 Cheese and fermented dairy desserts

- 6.3 Non-dairy beverages

- 6.3.1 Functional water

- 6.3.2 Juices and juice drinks

- 6.3.3 Ready-to-drink tea/coffee

- 6.3.4 Plant-based fermented drinks

- 6.4 Bakery and cereals

- 6.4.1 Bread and buns

- 6.4.2 Breakfast cereals and granola

- 6.4.3 Nutrition bars

- 6.5 Confectionery

- 6.5.1 Gummies and jellies

- 6.5.2 Chocolate

- 6.5.3 Candies and lozenges

- 6.6 Infant and child nutrition

- 6.6.1 Infant formula

- 6.6.2 Follow-on formula

- 6.6.3 Toddler foods

- 6.7 Medical and clinical nutrition

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Distribution channel, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales (ingredient suppliers to brands)

- 7.3 Distributors/agents

- 7.4 Online B2B platforms

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 IFF (International Flavors & Fragrances)

- 9.2 DSM-Firmenich

- 9.3 ADM

- 9.4 Kerry Group

- 9.5 BASF

- 9.6 Evonik

- 9.7 Novonesis

- 9.8 DuPont (IFF legacy Danisco)

- 9.9 Cargill

- 9.10 Givaudan

代謝保健食品市場預測至2034年-按產品類型、功能、原料類型、通路和最終用戶分類的全球分析

代謝保健食品市場預測至2034年-按產品類型、功能、原料類型、通路和最終用戶分類的全球分析 人工智慧設計的機能性食品市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、形式和最終用戶分類

人工智慧設計的機能性食品市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、形式和最終用戶分類 機能性食品益生菌市場規模、佔有率和成長分析:按產品類型、原料類型、劑型、應用、分銷管道、最終用戶和地區分類-2026-2033年產業預測功能性嬰幼兒食品市場預測至2034年-按產品類型、功能、成分類型、包裝類型、價格範圍、最終用戶和地區分類的全球分析代謝保健食品市場預測-全球產品類型、原料類型、健康益處、劑型、消費者群、應用、通路和地區分析-2034年機能性食品市場預測至2034年-全球產品類型、成分類型、性質、成分來源、應用、最終用戶、分銷管道和區域分析

機能性食品益生菌市場規模、佔有率和成長分析:按產品類型、原料類型、劑型、應用、分銷管道、最終用戶和地區分類-2026-2033年產業預測功能性嬰幼兒食品市場預測至2034年-按產品類型、功能、成分類型、包裝類型、價格範圍、最終用戶和地區分類的全球分析代謝保健食品市場預測-全球產品類型、原料類型、健康益處、劑型、消費者群、應用、通路和地區分析-2034年機能性食品市場預測至2034年-全球產品類型、成分類型、性質、成分來源、應用、最終用戶、分銷管道和區域分析 機能性食品市場:按產品類型、原料、應用和地區分類功能性食品和飲料市場預測至2032年:按產品類型、成分、人口統計、產品形式、分銷管道、應用和地區分類的全球分析

機能性食品市場:按產品類型、原料、應用和地區分類功能性食品和飲料市場預測至2032年:按產品類型、成分、人口統計、產品形式、分銷管道、應用和地區分類的全球分析 機能性食品市場規模、佔有率及成長分析(按成分、產品、應用及地區分類)-2026-2033年產業預測

機能性食品市場規模、佔有率及成長分析(按成分、產品、應用及地區分類)-2026-2033年產業預測 腦健康功能性食品飲料市場規模、佔有率及成長分析(依成分、產品、通路及地區分類)-2026-2033年產業預測

腦健康功能性食品飲料市場規模、佔有率及成長分析(依成分、產品、通路及地區分類)-2026-2033年產業預測