|

市場調查報告書

商品編碼

1871206

針對特定年齡層的個人化營養市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Age-Specific Personalized Nutrition Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

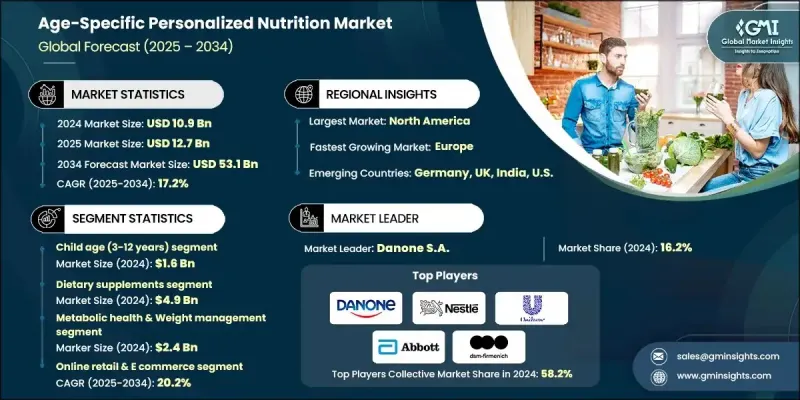

2024 年全球特定年齡層個人化營養市場價值為 109 億美元,預計到 2034 年將以 17.2% 的複合年成長率成長至 531 億美元。

人們越來越意識到飲食、生活方式與長期健康結果之間的聯繫,這推動了各年齡層對個人化營養解決方案的需求。世界衛生組織(WHO)的數據顯示,全球近74%的死亡與非傳染性疾病有關,凸顯了預防性醫療保健措施的緊迫感。消費者擴大採用客製化營養計畫來增強免疫力、提高能量水平並維持整體代謝健康。營養基因組學領域的蓬勃發展和生物技術的進步正在重塑基於年齡和生理特徵的個人化營養方案。美國國立衛生研究院(NIH)資助的遺傳學和微生物組研究正在幫助我們揭示基因如何影響營養代謝和吸收。基因檢測和基於微生物組的評估使個人能夠制定符合自身生物組成的個人化飲食計劃,從而進一步推進精準營養和個人化健康管理的理念。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 109億美元 |

| 預測值 | 531億美元 |

| 複合年成長率 | 17.2% |

美國疾病管制與預防中心(CDC)和世界衛生組織等衛生機構持續強調營養在降低肥胖、糖尿病和心血管疾病風險的重要作用。世界各國政府都在加大對營養教育、更清晰的食品標籤和公共衛生措施的投入,以鼓勵更健康的飲食習慣和生活方式選擇。這些措施正在推動消費者對個人化營養產品和服務的認知度和接受度不斷提高,以滿足他們對針對性健康解決方案的需求。

2024年,代謝健康和體重管理市場規模預計將達24億美元。該市場的成長主要受肥胖率上升、糖尿病病例增加以及生活方式相關的代謝紊亂等因素的推動。消費者正轉向個人化飲食計劃、營養補充劑和數位健康平台,以維持健康的體重水平並改善代謝功能。將人工智慧和穿戴式裝置融入營養監測,可以即時追蹤代謝活動,從而為尋求更佳健康結果的用戶提供更精準、數據驅動且更易於獲取的個人化營養計畫。

2024年,膳食補充劑市場規模預計將達49億美元。消費者對便利高效的營養輸送系統的需求日益成長,推動了該領域的擴張。針對特定年齡層和健康需求(包括免疫、代謝和認知健康)的個人化補充劑正迅速普及。 DNA和微生物組檢測與人工智慧驅動的推薦系統相結合,正在革新補充劑的配方和劑量精準度,確保消費者獲得與其獨特生理需求高度匹配的個人化產品。

預計到2024年,北美地區針對特定年齡層的個人化營養市場將佔據44.6%的佔有率,其中美國在健康和保健方面的消費者支出領先。美國先進的生物技術基礎設施、廣泛的數位健康解決方案以及慢性病的高發生率正在加速個人化營養的普及。消費者越來越傾向於選擇以科學為基礎、技術驅動的健康產品來管理長期健康。此外,美國有利的監管環境以及消費者對實證營養的堅定信心也推動了該市場透過電子商務和傳統零售通路的強勁成長。

塑造年齡特異性個人化營養市場格局的關鍵企業包括:Kerry Group PLC、Herbalife Nutrition Ltd.、Nutrigenomix、Viome Life Sciences、Bioniq、DSM-Firmenich、Unilever PLC、Zeon Lifesciences Ltd.、Abbott、Bright Green Partners、Amway Corporation、Glanbia PLC、Zeon Lifesciences Ltd.、Abbott、Bright Green Partners、Amway Corporation、Glanbia PLC、Nestle SAone 和 PLC SAone SAone SAone。這些市場領導者正在實施一系列策略,以加強其全球影響力。許多企業正大力投資研發,以推動營養基因組學技術的發展,並增強數據驅動的產品客製化能力。與生物技術公司和數位健康新創企業的策略合作,正在擴大獲取基因和微生物組資訊的機會,從而實現更精準的營養規劃。此外,各企業也致力於推出以人工智慧為基礎的平台和訂閱模式,以提高用戶參與度和留存率。拓展產品組合,推出針對特定年齡層的客製化營養補充品和功能性食品,仍是其核心策略之一。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 各年齡層的健康意識日益增強

- 營養基因體學的技術進步

- 更加重視預防性醫療保健

- 產業陷阱與挑戰

- 個人化解決方案成本高昂

- 各區域的監管複雜性

- 市場機遇

- 人工智慧與數位健康平台的整合

- 對預防性醫療保健和長壽產品的需求日益成長

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 年齡層

- 產品類型

- 應用

- 配銷通路

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依年齡層別分類,2021-2034年

- 主要趨勢

- 懷孕前及懷孕年齡

- 嬰兒年齡(0-2歲)

- 兒童年齡(3-12歲)

- 青少年時期(13-18歲)

- 成年年齡(19-64歲)

- 老年人(65歲以上)

第6章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 功能性食品和飲料

- 強化果汁

- 乳製品替代品

- 營養強化零食

- 能量與健康飲料

- 膳食補充劑

- 維生素和礦物質

- 草本及植物萃取物

- 益生菌和益生元

- 胺基酸和蛋白質補充劑

- 代餐產品

- 即飲奶昔

- 營養棒

- 控制卡路里的餐食

- 其他

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 代謝健康與體重管理

- 低熱量代餐

- 脂肪代謝促進劑

- 富含膳食纖維的功能性食品

- 個人化宏量營養素計劃

- 消化系統和腸道健康

- 益生菌和益生元混合物

- 發酵食品

- 酵素補充劑

- 基於微生物組的飲食計劃

- 骨骼和關節健康

- 鈣和維生素D補充劑

- 膠原蛋白飲料

- 葡萄糖胺和軟骨素產品

- 抗發炎營養保健品

- 認知健康

- 益智補品

- 富含 Omega-3 和 DHA 的食品

- 增強大腦功能的飲料

- 草本記憶增強劑

- 免疫健康

- 維生素C和鋅配方

- 抗氧化劑混合物

- 草本免疫力補品

- 針對不同年齡層的免疫支持奶昔

- 心血管健康

- Omega-3脂肪酸補充劑

- 降低膽固醇的營養

- 血壓控制公式

- 抗氧化功能飲料

- 運動與健身營養

- 蛋白粉和蛋白棒

- 胺基酸和支鏈胺基酸配方

- 水合和電解質飲料

- 恢復和耐力補充劑

- 皮膚、頭髮和美容營養

- 膠原蛋白和生物素補充劑

- 抗氧化劑和維生素E混合物

- 水合及提升肌膚彈性

- 抗衰老營養保健品

第8章:市場估算與預測:依配銷通路分類,2021-2034年

- 主要趨勢

- 線上零售與電子商務

- 超市和大型超市

- 藥局和藥局

- 專業營養品店

- 其他

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- Nutrigenomix

- Viome Life Sciences

- Nestle SA

- Danone SA

- Abbott

- DSM-Firmenich

- Unilever PLC

- Herbalife Nutrition Ltd.

- Amway Corporation

- Glanbia PLC

- Bright Green Partners

- Bioniq

- Zeon Lifesciences Ltd

- Kerry Group PLC

The Global Age-Specific Personalized Nutrition Market was valued at USD 10.9 Billion in 2024 and is estimated to grow at a CAGR of 17.2% to reach USD 53.1 Billion by 2034.

The increasing awareness of the connection between diet, lifestyle, and long-term health outcomes is driving demand for tailored nutrition solutions across all age groups. According to the World Health Organization (WHO), nearly 74% of global deaths are linked to non-communicable diseases, underscoring the urgent need for preventive healthcare measures. Consumers are increasingly adopting customized nutrition plans to enhance immunity, improve energy levels, and maintain overall metabolic health. The growing field of nutrigenomics and advancements in biotechnology are reshaping how nutrition is personalized based on age and physiology. Ongoing research funded by the National Institutes of Health (NIH) into genetics and microbiomes is helping uncover how genes affect nutrient metabolism and absorption. The use of genetic testing and microbiome-based assessments enables individuals to create diet plans tailored to their biological composition, further advancing the concept of precision nutrition and personalized health management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.9 Billion |

| Forecast Value | $53.1 Billion |

| CAGR | 17.2% |

Health authorities such as the Centers for Disease Control and Prevention (CDC) and the World Health Organization continue to emphasize the vital role of nutrition in reducing obesity, diabetes, and cardiovascular risks. Governments worldwide are investing in nutrition education, clearer food labeling, and public health initiatives to encourage healthier dietary habits and lifestyle choices. These initiatives are driving greater awareness and adoption of personalized nutrition products and services among consumers seeking targeted wellness solutions.

The metabolic health and weight management segment accounted for USD 2.4 Billion in 2024. This segment's growth is fueled by rising obesity rates, increasing cases of diabetes, and lifestyle-related metabolic disorders. Consumers are turning toward individualized diet plans, nutritional supplements, and digital health platforms to maintain healthy weight levels and improve metabolic function. The integration of artificial intelligence and wearable devices into nutrition monitoring allows for real-time tracking of metabolic activity, resulting in more accurate, data-driven, and accessible personalized nutrition plans for users seeking better health outcomes.

The dietary supplements segment generated USD 4.9 Billion in 2024. The growing consumer demand for easy and effective nutrient delivery systems is boosting this segment's expansion. Personalized supplements targeting specific age groups and health needs, including immune, metabolic, and cognitive health, are witnessing rapid adoption. The use of DNA and microbiome testing combined with AI-driven recommendation systems is revolutionizing supplement formulation and dosage precision, ensuring that consumers receive highly individualized products aligned with their unique biological requirements.

North America Age-Specific Personalized Nutrition Market captured 44.6% share in 2024, with the United States leading in consumer spending on health and wellness. The country's advanced biotechnology infrastructure, widespread use of digital health solutions, and high prevalence of chronic conditions are accelerating the adoption of personalized nutrition. Consumers are increasingly turning to science-backed and technology-enabled health products to manage long-term wellness. The U.S. also benefits from a favorable regulatory environment and strong consumer confidence in evidence-based nutrition, driving robust growth through both e-commerce and traditional retail channels.

Key companies shaping the Age-Specific Personalized Nutrition Market landscape include Kerry Group PLC, Herbalife Nutrition Ltd., Nutrigenomix, Viome Life Sciences, Bioniq, DSM-Firmenich, Unilever PLC, Zeon Lifesciences Ltd., Abbott, Bright Green Partners, Amway Corporation, Glanbia PLC, Nestle S.A., and Danone S.A. Leading companies in the Age-Specific Personalized Nutrition Market are implementing a range of strategies to strengthen their global presence. Many are investing heavily in research and development to advance nutrigenomic technologies and enhance data-driven product customization. Strategic collaborations with biotechnology firms and digital health startups are expanding access to genetic and microbiome insights for more precise nutrition planning. Companies are also focusing on launching AI-based platforms and subscription-based models to improve user engagement and retention. Expanding product portfolios with tailored supplements and functional foods designed for specific age groups remains a core strategy.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Age Group

- 2.2.3 Product Type

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising health consciousness across age groups

- 3.2.1.2 Technological advancements in nutrigenomics

- 3.2.1.3 Increased focus on preventive healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of personalized solutions

- 3.2.2.2 Regulatory complexity across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of ai and digital health platforms

- 3.2.3.2 Growing demand for preventive healthcare and longevity products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Age Group

- 3.7.3 Product Type

- 3.7.4 Application

- 3.7.5 Distribution Channel

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Age Group, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pre-conception & maternal age

- 5.3 Infant age (0-2 years)

- 5.4 Child age (3-12 years)

- 5.5 Teenager age (13-18 years)

- 5.6 Adult age (19-64 years)

- 5.7 Elderly age (65+ years)

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Functional foods & beverages

- 6.2.1 Fortified juices

- 6.2.2 Dairy alternatives

- 6.2.3 Nutrient-enriched snacks

- 6.2.4 Energy & wellness drinks

- 6.3 Dietary supplements

- 6.3.1 Vitamins & minerals

- 6.3.2 Herbal & botanical extracts

- 6.3.3 Probiotics & prebiotics

- 6.3.4 Amino acids & protein supplements

- 6.4 Meal replacement products

- 6.4.1 Ready-to-drink shakes

- 6.4.2 Nutrition bars

- 6.4.3 Calorie-controlled meals

- 6.5 Other

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Metabolic health & Weight management

- 7.2.1 Calorie-controlled meal replacements

- 7.2.2 Fat metabolism enhancers

- 7.2.3 Fiber-rich functional foods

- 7.2.4 Personalized macronutrient plans

- 7.3 Digestive & Gut health

- 7.3.1 Probiotic & Prebiotic blends

- 7.3.2 Fermented foods

- 7.3.3 Enzyme supplements

- 7.3.4 Microbiome-based diet plans

- 7.4 Bone & joint health

- 7.4.1 Calcium & vitamin D supplements

- 7.4.2 Collagen-based drinks

- 7.4.3 Glucosamine & chondroitin products

- 7.4.4 Anti-inflammatory nutraceuticals

- 7.5 Cognitive health

- 7.5.1 Nootropic supplements

- 7.5.2 Omega-3 & DHA Enriched Foods

- 7.5.3 Brain function enhancing drinks

- 7.5.4 Herbal memory boosters

- 7.6 Immune health

- 7.6.1 Vitamin C & Zinc formulations

- 7.6.2 Antioxidant blends

- 7.6.3 Herbal immunity tonics

- 7.6.4 Age-specific immune support shakes

- 7.7 Cardiovascular health

- 7.7.1 Omega-3 fatty acid supplements

- 7.7.2 Cholesterol reduction nutrition

- 7.7.3 Blood pressure control formulas

- 7.7.4 Antioxidant functional beverages

- 7.8 Sports & fitness nutrition

- 7.8.1 Protein powders & bars

- 7.8.2 Amino acid & BCAA Formulas

- 7.8.3 Hydration & electrolyte drinks

- 7.8.4 Recovery & Endurance supplements

- 7.9 Skin, hair & Beauty nutrition

- 7.9.1 Collagen & Biotin supplements

- 7.9.2 Antioxidant & Vitamin E blends

- 7.9.3 Hydration & Skin elasticity boosters

- 7.9.4 Anti-aging nutraceuticals

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Online retail & E-commerce

- 8.3 Supermarkets & hypermarkets

- 8.4 Pharmacies & drugstores

- 8.5 Specialty nutrition stores

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Nutrigenomix

- 10.2 Viome Life Sciences

- 10.3 Nestle S.A.

- 10.4 Danone S.A.

- 10.5 Abbott

- 10.6 DSM-Firmenich

- 10.7 Unilever PLC

- 10.8 Herbalife Nutrition Ltd.

- 10.9 Amway Corporation

- 10.10 Glanbia PLC

- 10.11 Bright Green Partners

- 10.12 Bioniq

- 10.13 Zeon Lifesciences Ltd

- 10.14 Kerry Group PLC

按品種和生命階段分類的寵物專用營養品市場預測(至2034年):全球產品類型、生命階段、品種體型、寵物類型、最終用戶和地區分析

按品種和生命階段分類的寵物專用營養品市場預測(至2034年):全球產品類型、生命階段、品種體型、寵物類型、最終用戶和地區分析 個人化營養市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測智慧營養補充品市場預測(至2034年):全球分析(按產品類型、成分類型、劑型、個人化程度、消費群組、技術整合、應用、最終用戶、分銷管道和地區分類)

個人化營養市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測智慧營養補充品市場預測(至2034年):全球分析(按產品類型、成分類型、劑型、個人化程度、消費群組、技術整合、應用、最終用戶、分銷管道和地區分類) 個人化營養市場規模、佔有率及預測(依產品類型、模式、技術和應用劃分)-全球預測全球個人化營養與健康市場:預測(至2034年)-按產品、通路、技術、應用、最終用戶和地區進行分析個人化營養市場-2026年至2031年預測個人化營養食品飲料市場預測至2032年:全球產品類型、個人化方法、形式、分銷管道、應用、最終用戶和區域分析人工智慧賦能營養配方市場預測至2032年:按技術、應用、最終用戶和地區分類的全球分析

個人化營養市場規模、佔有率及預測(依產品類型、模式、技術和應用劃分)-全球預測全球個人化營養與健康市場:預測(至2034年)-按產品、通路、技術、應用、最終用戶和地區進行分析個人化營養市場-2026年至2031年預測個人化營養食品飲料市場預測至2032年:全球產品類型、個人化方法、形式、分銷管道、應用、最終用戶和區域分析人工智慧賦能營養配方市場預測至2032年:按技術、應用、最終用戶和地區分類的全球分析 個人化營養市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)基於DNA的客製化維生素配方市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

個人化營養市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)基於DNA的客製化維生素配方市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)