|

市場調查報告書

商品編碼

2073251

中國廢棄物衍生可再生氣體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Renewable Gas From Waste - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

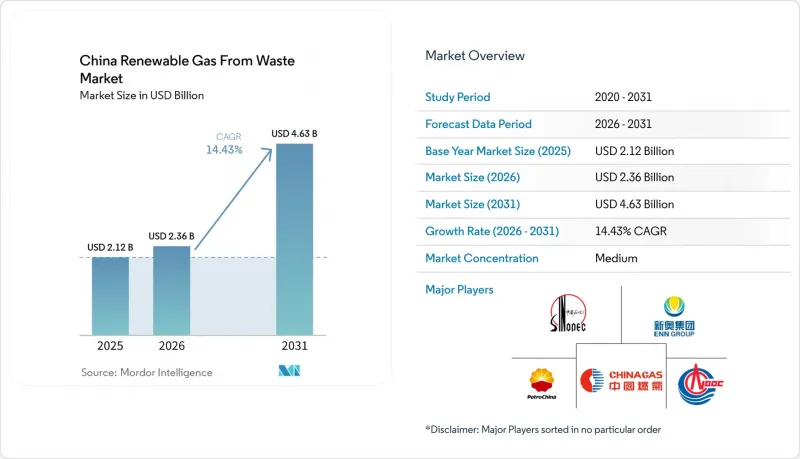

根據 Mordor Intelligence 預測,中國廢棄物衍生可再生氣體市場規模預計將從 2025 年的 21.2 億美元和 2026 年的 23.6 億美元成長到 2031 年的 46.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 14.43%。

本報告依原料(都市固態廢棄物、農業殘渣、食物廢棄物等)、技術(氣化、熱解等)、氣體種類(沼氣、合成氣等)、應用(發電、併網等)及組件(氣體回收、消化器/發酵等)分類。市場預測以美元計價。

中國廢棄物衍生可再生氣體市場的趨勢與洞察

「二氧化碳排放峰」和「碳中和」的目標正在加速對生物天然氣的政策要求。

中國的碳達峰和碳中和議程如今已不僅僅是一項寬泛的政策訊號,它正透過法規、計量體系和專案層面的合規要求,塑造中國的廢棄物衍生可再生氣體市場。國家發展和改革委員會(發改委)發布的《2024年碳達峰和碳中和行動綱領》強化了可再生氣體計畫在企業層級記錄其排放結果所需的計量和檢驗基礎設施。這項轉變意義重大,因為開發商需要擁有更高品質、更有利於資金籌措的報告體系,才能獲得電力公司和產業的收購承諾。這也提高了缺乏檢驗的監測系統和正式報告能力的中小型企業的進入門檻。事實上,中國的廢棄物衍生可再生氣體市場正接近一個關鍵節點,即法律授權、碳核算和基礎設施准入必須無縫銜接,才能實現規模化發展。

加強生物甲烷一體化的能源方法

隨著《中華人民共和國能源法》於2025年1月1日正式實施,生質氣在國家能源體系中獲得了更明確的法律地位。該法鼓勵根據當地實際情況利用生質能能源,並要求能源體系提升其接收和分配可再生能源的能力。這項法律修正案消除了先前城市燃氣供應商用來拒絕生質能甲烷接入輸配網路的模糊地帶。與2025年之前中國廢棄物衍生可再生氣體市場相比,專案開發商現在可以在更強力的製度支持下,協商簽訂長期供應合約。因此,在城市燃氣管網較為完善的省份,天然氣管網供應計畫的商業性軌跡也變得更可預測。

缺乏全國性的生物甲烷生產補貼框架正在削弱該計畫的可行性。

中國廢棄物衍生可再生氣體市場仍缺乏全國性的單位生產補貼,迫使許多項目依賴區域性氣體價格、產品特定銷售和碳排放收入。在發行網路薄弱的地區,開發商無法依賴優質都市區銷售管道,這個問題尤其突出。排放部於2025年12月發布的《豬糞沼氣回收和農業廢棄物集中處理中國碳減排單位調查方法》將有助於補充部分收入結構。然而,這並不能取代直接的生產補貼機制。在缺乏全國性補貼的情況下,雄厚的資金實力仍是主要的競爭優勢,國營企業和大型環保公司比中小開發商更具優勢。因此,即使在資源豐富的地區,專案開發仍然具有選擇性。

細分市場分析

到2025年,農業殘餘物將佔中國廢棄物衍生可再生氣體市場31.50%的市場佔有率,成為該產業最大的原料來源。這一主導地位反映了中國主要農業省份作物產量龐大,秸稈及相關殘餘物供應充足。實際上,這些原料確保了縣級工廠(已建立收集系統)所需的處理能力。此外,農業殘餘物符合更廣泛的農村廢棄物處理和資源化利用目標,這也有利於中國廢棄物衍生可再生氣體市場的發展。

預計到2031年,食物廢棄物將以每年14.32%的速度成長,成為市場上成長最快的原料類別。畜禽糞便、工業有機廢棄物、污水污泥和垃圾掩埋廢棄物分別滿足中國廢棄物衍生可再生氣體市場不同的監管合規和處置需求。畜禽糞便尤其重要,因為在許多地區,畜禽廢棄物的處置已不再是可選項,農業農村部正在全國推廣80%以上的綜合利用率。這一成長反映了都市區強制性分類收集、更清潔原料的供應以及新的碳權(CCER)調查方法,這些都提高了集中式有機廢棄物沼氣加工的盈利。

至2025年,厭氧消化將佔中國廢棄物衍生可再生氣體廢棄物總規模的43.60%,成為農業和市政廢棄物計畫的主導技術平台。其主導地位源於其長期穩定的運作記錄、對現有工廠的熟悉程度以及圍繞畜禽糞便和混合有機原料積累的豐富實施經驗。此外,由於許多現有項目在進行任何精煉工藝之前都以生產未經提純的沼氣為起點,因此該技術仍然至關重要。由此可見,即使新的方法不斷湧現,厭氧消化在中國廢棄物衍生可再生氣體市場中仍發揮基礎性作用。

預計到2031年,氣化技術將以每年15.10%的速度成長,成為預測期內成長最快的技術類別。沼氣氣體純化系統、垃圾掩埋沼氣回收、熱解和監測系統共同支撐著更廣泛、更先進的技術體系。中國光大環境在安徽省蕭縣的首個生質能氣化計畫表明,熱化學轉化技術可以超越中試階段,並將可利用的原料範圍擴大到不適合消化的乾物質。這意義重大,因為中國廢棄物產業需要多種轉化途徑來處理來自城市、農業和工業的各種有機廢棄物,從而生產可再生氣體。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 「二氧化碳排放目標」正在加速生物天然氣領域的政策義務。

- 透過《能源法》促進生物甲烷的引入

- 透過國營企業的進入來檢驗生物甲烷產業的有效性和擴張情況。

- 都市區強制推行食物廢棄物分類,導致集中式原料供應擴大。

- 全國範圍內的碳市場和國有企業的排放揭露正在推動對工業生物甲烷的需求。

- 農業廢棄物管理危機導致政策主導的原料需求成長。

- 市場限制因素

- 缺乏全國性的生物甲烷生產補貼計畫正在削弱該計畫的可行性。

- 原料物流成本高昂,限制了該專案的實施區域。

- 跨部門管理體制的碎片化導致核准延誤。

- 家庭沼氣池的大量棄用正在破壞分散式生產基礎設施。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 透過數位化原料管理和製程最佳化,提高可再生燃氣發電廠的效率。

- 制定有機廢棄物再利用和分類政策,以支持擴大原料供應

- 地緣政治事件對市場的影響

第5章 市場規模與成長預測

- 按原料

- 都市固態廢棄物(MSW)

- 農業殘餘物

- 牲畜糞便

- 工業有機廢棄物

- 污水污泥

- 食物廢棄物

- 其他

- 透過技術

- 厭氧消化

- 垃圾掩埋沼氣回收

- 氣化

- 熱解

- 沼氣氣體純化系統

- 其他

- 依氣體類型

- 沼氣

- 生物甲烷/可再生天然氣(RNG)

- 合成氣

- 透過使用

- 發電

- 熱電聯產(CHP)

- 注入電網

- 運輸燃料

- 工業加熱

- 住宅和商業供暖

- 其他

- 按組件

- 氣體收集系統

- 消化槽和發酵系統

- 氣體處理及淨化設備

- 壓縮機和儲能系統

- 發電設備

- 監控系統

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- PetroChina Company Limited

- China Petroleum & Chemical Corporation(Sinopec Corp.)

- CNOOC Refining and Petrochemical Co., Ltd.

- China Gas Holdings Limited

- ENN Energy Holdings Limited

- Towngas China Company Limited

- China Everbright Environment Group Limited

- Beijing Enterprises Holdings Limited

- China Resources Gas Group Limited

- Shenergy Environment Technology Co., Ltd.

- China Tianying Inc.

- China Conch Venture Holdings Limited

- Shanghai SUS Environment Co., Ltd.

- Grandblue Environment Co., Ltd.

- China Energy Conservation and Environmental Protection Group(CECEP)

- Anhui Province Natural Gas Development Co., Ltd.

- China Three Gorges Corporation

- Shenzhen Gas Corporation Ltd.

- Zheneng Jinjiang Environment Holding Company Limited

- Beijing Capital Eco-Environment Protection Group Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the china renewable gas from waste market size is projected to expand from USD 2.12 billion in 2025 and USD 2.36 billion in 2026 to USD 4.63 billion by 2031, registering a CAGR of 14.43% between 2026 to 2031.

This report is Segmented by Feedstock (Municipal Solid Waste, Agricultural Residues, Food Waste, and More), by Technology (Gasification, Pyrolysis, and More), by Gas Type (Biogas, Syngas, and More), by Application (Electricity Generation, Grid Injection, and More), and by Component (Gas Collection, Digesters & Fermentation, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Renewable Gas From Waste Market Trends and Insights

Dual Carbon Goals Accelerating Bio-Natural Gas Policy Mandates

China's carbon peak and carbon neutrality agenda is now shaping the China renewable gas from waste market through rules, measurement systems, and project-level compliance expectations rather than broad policy signaling alone. The National Development and Reform Commission (NDRC) 2024 action plan on carbon peak and carbon neutrality standards strengthened the measurement and verification base that renewable gas projects need to document emissions outcomes at the enterprise level. That shift matters because developers now need stronger data quality and more bankable reporting before projects can secure offtake confidence from utilities and industries. It also raises entry barriers for smaller firms that lack verified monitoring systems and formal reporting capabilities. In practice, the China renewable gas from waste market is moving closer to sectors where legal recognition, carbon accounting, and access to infrastructure must work together before scale can follow.

Energy Law Strengthening Biomethane Integration

The Energy Law of the People's Republic of China took effect on January 1, 2025, and gave bio-natural gas a clearer statutory position within the national energy system. The law encourages the use of biomass energy according to local conditions and also requires the energy system to improve its ability to accept and allocate renewable energy. That legal change reduces the ambiguity that city gas distributors previously used to resist access to the biomethane grid. Project developers can now negotiate long-term supply arrangements with better institutional backing than the China renewable gas from waste market had before 2025. The result is a more predictable commercial path for grid injection projects in provinces with dense municipal gas networks.

Absence of a National Biomethane Production Subsidy Framework Undermining Viability

The China renewable gas from waste market still lacks a national per-unit production subsidy, leaving many projects dependent on local gas prices, by-product sales, and carbon revenues. This matters most in regions where distribution networks are weaker, and developers cannot rely on premium urban offtake channels. The MEE's December 2025 release of new CCER methodologies for pig farm manure biogas recovery and agricultural waste centralized processing helps part of the revenue stack. Still, it does not replace a direct production support mechanism. Without a national subsidy, stronger balance sheets remain a major competitive advantage, favoring SOEs and large environmental firms over smaller developers. As a result, project deployment remains selective even when the resource base is large.

Other drivers and restraints analyzed in the detailed report include:

- State-Owned Enterprise Entry Validating and Scaling the Biomethane Sector

- Mandatory Urban Food Waste Sorting Expanding Centralized Feedstock Supply

- High Feedstock Logistics Costs Limiting Viable Project Geographies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Agricultural residues accounted for 31.50% of the China renewable gas from waste market share in 2025, making them the largest feedstock base in the sector. Their lead reflects the scale of crop output and the wide availability of straw and related residues across major farming provinces. In practical terms, these streams provide the volume needed for county-level plants where collection systems are already in place. The China renewable gas from waste market also benefits from the fact that agricultural residues align with broader rural waste treatment and resource-use goals.

Food waste is forecast to expand at 14.32% through 2031, making it the fastest-growing feedstock category in the market. Animal manure, industrial organic waste, sewage sludge, and landfill waste serve different compliance and disposal needs within the China renewable gas from waste market. Manure is especially important because livestock waste treatment is no longer optional in many areas, and the Ministry of Agriculture and Rural Affairs has pushed for nationwide comprehensive utilization rates of 80% or more. This growth reflects mandatory urban sorting, cleaner incoming feedstock, and new CCER methodologies that improve the revenue potential of centralized biogas processing from organic waste streams.

Anaerobic digestion accounted for 43.60% of the China renewable gas from waste market size in 2025, making it the leading technology platform across agricultural and urban waste projects. Its dominance stemmed from a long operating history, familiarity with existing plants, and a broad installed base built around manure and mixed organic feedstocks. The technology also remains central because most current projects still begin with raw biogas production before any upgrading step. This gives anaerobic digestion a foundational role in the China renewable gas from waste market, even as newer pathways gain ground.

Gasification is projected to grow at 15.10% through 2031, which makes it the fastest-growing technology category in the forecast period. Biogas upgrading systems, landfill gas recovery, pyrolysis, and monitoring systems all support a broader, increasingly sophisticated technology stack. China Everbright Environment's first biomass gasification project in Xiao County, Anhui, showed that thermochemical conversion can move beyond pilot status and widen the usable feedstock base to drier materials that are less suitable for digestion. That matters because renewable gas from the waste industry in China requires multiple conversion routes to process the full range of municipal, agricultural, and industrial organic waste.

Complete Report Scope:

- By Feedstock

- Municipal Solid Waste (MSW)

- Agricultural Residues

- Animal Manure

- Industrial Organic Waste

- Sewage Sludge

- Food Waste

- Others

- By Technology

- Anaerobic Digestion

- Landfill Gas Recovery

- Gasification

- Pyrolysis

- Biogas Upgrading Systems

- Others

- By Gas Type

- Biogas

- Biomethane / Renewable Natural Gas (RNG)

- Syngas

- By Application

- Electricity Generation

- Combined Heat & Power (CHP)

- Grid Injection

- Transportation Fuel

- Industrial Heating

- Residential & Commercial Heating

- Others

- By Component

- Gas Collection Systems

- Digesters & Fermentation Systems

- Gas Processing & Upgrading Units

- Compressors & Storage Systems

- Power Generation Equipment

- Monitoring & Control Systems

- Others

List of Companies Covered in this Report:

- PetroChina Company Limited

- China Petroleum & Chemical Corporation (Sinopec Corp.)

- CNOOC Refining and Petrochemical Co., Ltd.

- China Gas Holdings Limited

- ENN Energy Holdings Limited

- Towngas China Company Limited

- China Everbright Environment Group Limited

- Beijing Enterprises Holdings Limited

- China Resources Gas Group Limited

- Shenergy Environment Technology Co., Ltd.

- China Tianying Inc.

- China Conch Venture Holdings Limited

- Shanghai SUS Environment Co., Ltd.

- Grandblue Environment Co., Ltd.

- China Energy Conservation and Environmental Protection Group (CECEP)

- Anhui Province Natural Gas Development Co., Ltd.

- China Three Gorges Corporation

- Shenzhen Gas Corporation Ltd.

- Zheneng Jinjiang Environment Holding Company Limited

- Beijing Capital Eco-Environment Protection Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Dual Carbon Goals Accelerating Bio-Natural Gas Policy Mandates

- 4.2.2 Energy Law Strengthening Biomethane Integration

- 4.2.3 State-Owned Enterprise Entry Validating and Scaling the Biomethane Sector

- 4.2.4 Mandatory Urban Food Waste Sorting Expanding Centralized Feedstock Supply

- 4.2.5 National Carbon Market and SOE Emission Disclosure Driving Industrial Biomethane Offtake

- 4.2.6 Agricultural Waste Management Crisis Creating Policy-Driven Feedstock Push

- 4.3 Market Restraints

- 4.3.1 Absence of a National Biomethane Production Subsidy Framework Undermining Viability

- 4.3.2 High Feedstock Logistics Costs Limiting Viable Project Geographies

- 4.3.3 Fragmented Multi-Ministry Regulatory Structure Causing Approval Delays

- 4.3.4 Mass Abandonment of Household Digesters Eroding Distributed Production Base

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Digital Feedstock Management and Process Optimization Improving Renewable Gas Plant Efficiency

- 4.9 Organic Waste Diversion and Segregation Policies Supporting Feedstock Supply Growth

- 4.10 Impact of Geopolitical Events on the Market

5 Market Size & Growth Forecasts

- 5.1 By Feedstock

- 5.1.1 Municipal Solid Waste (MSW)

- 5.1.2 Agricultural Residues

- 5.1.3 Animal Manure

- 5.1.4 Industrial Organic Waste

- 5.1.5 Sewage Sludge

- 5.1.6 Food Waste

- 5.1.7 Others

- 5.2 By Technology

- 5.2.1 Anaerobic Digestion

- 5.2.2 Landfill Gas Recovery

- 5.2.3 Gasification

- 5.2.4 Pyrolysis

- 5.2.5 Biogas Upgrading Systems

- 5.2.6 Others

- 5.3 By Gas Type

- 5.3.1 Biogas

- 5.3.2 Biomethane / Renewable Natural Gas (RNG)

- 5.3.3 Syngas

- 5.4 By Application

- 5.4.1 Electricity Generation

- 5.4.2 Combined Heat & Power (CHP)

- 5.4.3 Grid Injection

- 5.4.4 Transportation Fuel

- 5.4.5 Industrial Heating

- 5.4.6 Residential & Commercial Heating

- 5.4.7 Others

- 5.5 By Component

- 5.5.1 Gas Collection Systems

- 5.5.2 Digesters & Fermentation Systems

- 5.5.3 Gas Processing & Upgrading Units

- 5.5.4 Compressors & Storage Systems

- 5.5.5 Power Generation Equipment

- 5.5.6 Monitoring & Control Systems

- 5.5.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PetroChina Company Limited

- 6.4.2 China Petroleum & Chemical Corporation (Sinopec Corp.)

- 6.4.3 CNOOC Refining and Petrochemical Co., Ltd.

- 6.4.4 China Gas Holdings Limited

- 6.4.5 ENN Energy Holdings Limited

- 6.4.6 Towngas China Company Limited

- 6.4.7 China Everbright Environment Group Limited

- 6.4.8 Beijing Enterprises Holdings Limited

- 6.4.9 China Resources Gas Group Limited

- 6.4.10 Shenergy Environment Technology Co., Ltd.

- 6.4.11 China Tianying Inc.

- 6.4.12 China Conch Venture Holdings Limited

- 6.4.13 Shanghai SUS Environment Co., Ltd.

- 6.4.14 Grandblue Environment Co., Ltd.

- 6.4.15 China Energy Conservation and Environmental Protection Group (CECEP)

- 6.4.16 Anhui Province Natural Gas Development Co., Ltd.

- 6.4.17 China Three Gorges Corporation

- 6.4.18 Shenzhen Gas Corporation Ltd.

- 6.4.19 Zheneng Jinjiang Environment Holding Company Limited

- 6.4.20 Beijing Capital Eco-Environment Protection Group Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

廢棄物衍生可再生氣體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲廢棄物衍生可再生氣體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)美國廢棄物衍生可再生氣體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

廢棄物衍生可再生氣體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲廢棄物衍生可再生氣體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)美國廢棄物衍生可再生氣體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 可再生天然氣市場預測至2034年-按來源、生產流程、分銷方式、應用、最終用戶和地區分類的全球分析認證氣體市場預測-全球按來源、分銷方式、應用、最終用戶和地區分類的分析——2034年

可再生天然氣市場預測至2034年-按來源、生產流程、分銷方式、應用、最終用戶和地區分類的全球分析認證氣體市場預測-全球按來源、分銷方式、應用、最終用戶和地區分類的分析——2034年 天然氣市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、應用、地區和競爭格局分類,2021-2031年

天然氣市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、應用、地區和競爭格局分類,2021-2031年 2026年全球可再生天然氣(RNG)承購保險市場報告歐洲天然氣:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)天然氣市場預測至2034年-按產品類型、類別、來源、通路、應用、最終用戶和地區分類的全球分析

2026年全球可再生天然氣(RNG)承購保險市場報告歐洲天然氣:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)天然氣市場預測至2034年-按產品類型、類別、來源、通路、應用、最終用戶和地區分類的全球分析 全球可再生天然氣市場:按應用、產品類型、生產技術、來源/原料類型和地區分類-市場規模、產業動態、機會分析和預測(2026-2035 年)

全球可再生天然氣市場:按應用、產品類型、生產技術、來源/原料類型和地區分類-市場規模、產業動態、機會分析和預測(2026-2035 年)