|

市場調查報告書

商品編碼

2066704

歐洲天然氣:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Natural Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

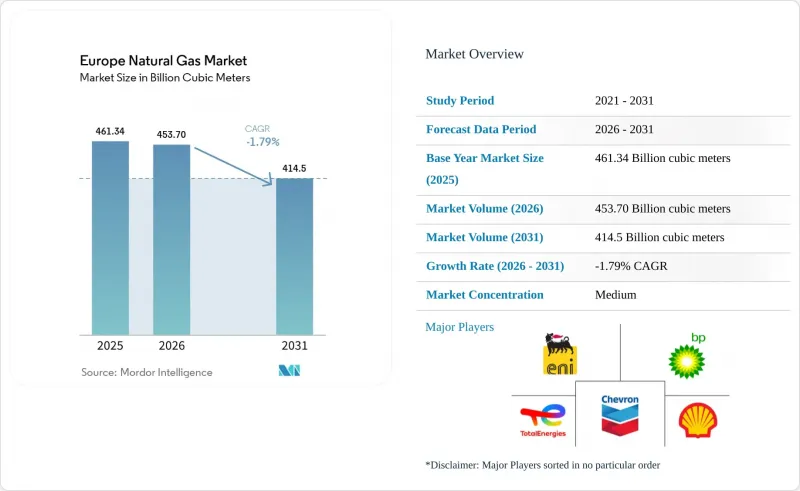

根據 Mordor Intelligence 預測,歐洲天然氣市場規模將從 2025 年的 4,613.4 億立方米和 2026 年的 4,537 億立方米萎縮至 2031 年的 4,145 億立方米,2026 年至 2031 年的年複合成長率(CAGR)為 -1.79%。

本報告按類型(壓縮天然氣、管道天然氣、液化天然氣)、來源(國內陸上生產、國內海上生產、液化天然氣進口)、最終用途行業(化肥生產、城市燃氣供應、運輸、石化原料、其他)和地區(德國、法國、義大利、西班牙、荷蘭、挪威、波蘭和其他歐洲國家)進行分類。

歐洲天然氣市場的趨勢與洞察

電力和區域供熱系統中煤炭向天然氣的轉換

預計到2025年12月,碳排放權價格將上漲至每噸二氧化碳83.79歐元,2030年將達到149歐元,德國和波蘭的市政業者正持續推動老舊燃煤鍋爐向燃氣熱電聯產(CH)系統的轉型。在中等規模的城市,分階段過渡到燃氣系統更為可取,因為區域供熱管網通常缺乏足夠的容量來安裝大規模熱泵。然而,隨著所有權轉移設施(TTF)價格可能超過煤炭轉換的閾值,以及基本負載燃氣經濟效益的下降,轉換機會正在減少。儘管2024年燃氣發電量下降了6%,但能源效率指令規定的短期合規期限仍支持供熱領域的部分轉換。隨著電網升級和可再生能源的普及,預計2029年後區域供熱對天然氣的需求將趨於平穩,這將進一步加劇歐洲天然氣市場的結構性萎縮趨勢,儘管短期需求仍將持續成長。

擴大歐洲液化天然氣再氣化能力

受德國快速引進浮式儲存再氣化裝置(FSRU)以及波蘭和荷蘭FSRU擴建計畫的推動,2022年至2025年間,歐洲的再氣化能力成長了32%,達到每年約2700億立方公尺。光是在德國,威廉港、布倫斯比特爾、盧布明和施塔德四個FSRU計畫在24個月內就運作了448億立方公尺的進口氣化能力。波蘭格但斯克FSRU和什維諾維甚切FSRU計畫的擴建,目前已確保了144億立方公尺的合計供給能力,在華沙產生了可用於區域出口的盈餘。立陶宛克萊佩達碼頭的小規模轉運量明顯增加,2025年記錄的卡車裝載量為1834輛。預計到2030年,隨著擴建工程的推進,處理能力將達到4050億立方公尺。然而,如果需求趨勢保持不變,這將意味著嚴重的過度建設,導致資產所有者擴大尋求長期收購合作夥伴,以降低運轉率風險。

俄烏戰爭後的地緣政治供應鏈中斷

由於制裁和運輸協議到期,供應來源被迫多元化,導致俄羅斯管道天然氣供應量從2021年佔歐盟供應量的約40%急劇下降至2025年的13%。歐盟委員會目前的目標是在2027年底前全面禁止俄羅斯天然氣,這導致需求集中在液化天然氣現貨市場和挪威管道。 2025年,挪威滿足了歐盟31%的需求,但由於產量停滯,未來的成長受到限制。 2025年2月,庫存水準降至40%,低於50%的監管最低標準,導致工業部門價格上漲和供應受限。公共產業仍然不願簽訂價格高昂的20年期液化天然氣契約,導致供應風險溢價長期存在,並阻礙了對新建液化工廠的投資。

細分市場分析

2025年,管道天然氣(PNG)在歐洲天然氣市場仍佔70.7%的市佔率。這反映了數十年來管網建設的成果,使得天然氣價格降至每兆瓦時2-4歐元的低點。然而,隨著與俄羅斯現有合約的到期以及住宅電氣化程度的提高,管道運輸量正在下降,分配給管道天然氣的歐洲天然氣市場規模也在萎縮。液化天然氣(LNG)的交付價格高成本,為每兆瓦時6-8歐元,但預計新型浮式儲存再氣化裝置(FSRU)的投入使用以及靈活的現貨購買方案將推動其在2031年之前以每年3.5%的速度成長。

由於其高度適應性,液化天然氣(LNG)是電力公司平衡波動性可再生能源的首選邊際能源。小規模LNG也支持卡車運輸和船舶加氣,從而促進下游產業的成長。壓縮天然氣(CNG)仍是一個小眾市場,目前只有786座加氣站,主要分佈在義大利、法國和德國。其他驅動技術的存在限制了CNG的成長潛力,預計其總需求將在本十年後半期趨於穩定。總體而言,LNG的擴張在一定程度上緩解了管道運輸的下滑,並減緩了歐洲天然氣市場總需求的下降,但尚未扭轉這一趨勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 發電和區域供熱系統中的煤炭燃料向天然氣燃料轉換

- 擴大歐洲液化天然氣再氣化能力

- 在「適合55歲族群」政策框架下,為天然氣作為過渡燃料提供政策支持

- 波羅的海和北海小規模液化天然氣燃料庫基礎設施擴建

- 透過維修為與氫能相容的管道,降低資產擱淺的風險。

- 市場限制因素

- 俄烏戰爭後的地緣政治供應鏈中斷

- 歐盟2040年脫碳目標將加速電氣化進程。

- 強制分配生物甲烷混合物以減少化石氣體的需求

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 壓縮天然氣(CNG)

- 管道天然氣(PNG)

- 液化天然氣(LNG)

- 按供應來源

- 國內生產-在土地上

- 國內生產 - 離岸生產

- 液化天然氣進口

- 按最終用途行業分類

- 化肥生產

- 城市瓦斯供應

- 運輸

- 石油化學原料

- 其他[工業製造、農業(茶葉種植園)、管道系統積體電路、液化石油氣收縮、海綿鐵和鋼鐵]

- 按地區

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 挪威

- 波蘭

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Shell plc

- BP plc

- TotalEnergies SE

- Equinor ASA

- Eni SpA

- Exxon Mobil Corp.

- Chevron Corp.

- ConocoPhillips

- Engie SA

- EDF SA

- Gazprom PJSC

- OMV AG

- Repsol SA

- PGNiG(PKN Orlen)

- Naturgy Energy Group SA

- VNG AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe natural gas market size is projected to contract from 461.34 Billion cubic meters in 2025 and 453.70 Billion cubic meters in 2026 to 414.5 Billion cubic meters by 2031, registering a CAGR of -1.79% between 2026 to 2031.

This report is Segmented by Type (Compressed Natural Gas, Piped Natural Gas, and Liquefied Natural Gas), Source (Domestic Production - Onshore, Domestic Production - Offshore, and LNG Imports), End-Use Sector (Fertilizer Production, City Gas Distribution, Transportation, Petrochemical Feedstock, and Others), and Geography (Germany, France, Italy, Spain, Netherlands, Norway, Poland, and Rest of Europe).

Europe Natural Gas Market Trends and Insights

Coal-to-Gas Switching in Power & District Heating Fleets

Municipal operators in Germany and Poland continue migrating from aging coal boilers to gas-fired combined heat and power units as carbon-allowance prices climbed to EUR 83.79 per tonne CO2 in December 2025 and are heading toward EUR 149 by 2030. Mid-sized cities favor incremental gas conversions because district-heating grids often lack capacity for large-scale heat pumps. The opportunity window, however, is narrowing as Title Transfer Facility (TTF) prices occasionally exceed coal-switching thresholds, reducing baseload gas economics. While gas-fired electricity output slipped 6% in 2024, near-term compliance deadlines under the Energy Efficiency Directive still support residual switching in heating. As grid upgrades and renewables proliferate, district-heating gas demand is expected to plateau after 2029, reinforcing the European natural gas market's structural decline even as short-term gains persist.

Expansion of European LNG Regasification Capacity

Europe's regasification capacity jumped 32% between 2022 and 2025 to roughly 270 BCM per year, propelled by rapid FSRU deployments in Germany and expansions in Poland and the Netherlands. Germany alone commissioned 44.8 BCM of import capacity across Wilhelmshaven, Brunsbuttel, Lubmin, and Stade within 24 months. Poland's Gdansk FSRU and Swinoujscie upgrade now provide 14.4 BCM combined, giving Warsaw surplus volumes for regional exports. Lithuania's Klaipeda terminal underscores the rise of small-scale reloads, posting 1,834 truck loadings in 2025. Forecast additions could lift capacity to 405 BCM by 2030, implying significant over-build if demand trends hold, so asset owners increasingly seek long-term offtake partners to mitigate utilization risk.

Geopolitical Supply Disruptions After Russia-Ukraine War

Russian pipeline flows plunged from about 40% of EU supply in 2021 to 13% in 2025 as sanctions and the transit-agreement expiry forced diversification. The European Commission now seeks a full Russian-gas ban by the end of 2027, funneling demand to LNG spot markets and Norwegian pipelines. Norway supplied 31% of EU needs in 2025, yet flat output limits future upside. Inventory dipped to 40% in February 2025, below the 50% regulatory minimum, sparking price spikes and industrial curtailments. Utilities remain hesitant to sign 20-year LNG deals at elevated prices, prolonging supply-risk premiums and deterring new liquefaction investments.

Other drivers and restraints analyzed in the detailed report include:

- Policy Support for Gas as a Transition Fuel Under Fit-for-55

- Growth of Small-Scale LNG Bunkering Infrastructure in Baltic & North Seas

- EU 2040 Decarbonization Target Accelerating Electrification

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Piped natural gas retained 70.7% of the Europe natural gas market share in 2025, reflecting decades of network build-out that offers low tariffs of EUR 2-4 per MWh. Pipeline volumes, however, decline as legacy Russian contracts expire and residential electrification widens, shrinking the European natural gas market size allocated to PNG. LNG, although costlier at EUR 6-8 per MWh delivered, is forecast to expand 3.5% annually through 2031 thanks to new FSRUs and flexible spot-purchase options.

LNG's adaptability makes it the favored marginal source for utilities balancing volatile renewables. Small-scale LNG also supports trucking and marine bunkering, reinforcing downstream growth. Compressed natural gas remains niche, with 786 refueling stations mainly in Italy, France, and Germany. Competing drivetrain technologies restrict CNG's headroom, and total demand is set to plateau late in the decade. Overall, LNG's expansion partially cushions pipeline-volume erosion, slowing, but not reversing, the European natural gas market's aggregate decline.

List of Companies Covered in this Report:

- Shell plc

- BP plc

- TotalEnergies SE

- Equinor ASA

- Eni SpA

- Exxon Mobil Corp.

- Chevron Corp.

- ConocoPhillips

- Engie SA

- EDF SA

- Gazprom PJSC

- OMV AG

- Repsol SA

- PGNiG (PKN Orlen)

- Naturgy Energy Group SA

- VNG AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Coal-to-gas switching in power & district-heating fleets

- 4.2.2 Expansion of European LNG regasification capacity

- 4.2.3 Policy support for gas as a transition fuel under Fit-for-55

- 4.2.4 Growth of small-scale LNG bunkering infrastructure in Baltic & North Seas

- 4.2.5 Hydrogen-ready pipeline retrofits lowering stranded-asset risk

- 4.3 Market Restraints

- 4.3.1 Geopolitical supply disruptions after Russia-Ukraine war

- 4.3.2 EU 2040 decarbonisation target accelerating electrification

- 4.3.3 Mandatory biomethane blending quotas reducing fossil-gas demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Compressed Natural Gas (CNG)

- 5.1.2 Piped Natural Gas (PNG)

- 5.1.3 Liquefied Natural Gas (LNG)

- 5.2 By Source

- 5.2.1 Domestic Production - Onshore

- 5.2.2 Domestic Production - Offshore

- 5.2.3 LNG Imports

- 5.3 By End-Use Sector

- 5.3.1 Fertilizer Production

- 5.3.2 City Gas Distribution

- 5.3.3 Transportation

- 5.3.4 Petrochemical Feedstock

- 5.3.5 Others [Industrial Manufacturing, Agriculture (Tea Plantation), IC for Pipeline System, LPG Shrinkage, Sponge Iron/Steel]

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 France

- 5.4.3 Italy

- 5.4.4 Spain

- 5.4.5 Netherlands

- 5.4.6 Norway

- 5.4.7 Poland

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Shell plc

- 6.4.2 BP plc

- 6.4.3 TotalEnergies SE

- 6.4.4 Equinor ASA

- 6.4.5 Eni SpA

- 6.4.6 Exxon Mobil Corp.

- 6.4.7 Chevron Corp.

- 6.4.8 ConocoPhillips

- 6.4.9 Engie SA

- 6.4.10 EDF SA

- 6.4.11 Gazprom PJSC

- 6.4.12 OMV AG

- 6.4.13 Repsol SA

- 6.4.14 PGNiG (PKN Orlen)

- 6.4.15 Naturgy Energy Group SA

- 6.4.16 VNG AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

中國廢棄物衍生可再生氣體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)廢棄物衍生可再生氣體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲廢棄物衍生可再生氣體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)美國廢棄物衍生可再生氣體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中國廢棄物衍生可再生氣體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)廢棄物衍生可再生氣體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲廢棄物衍生可再生氣體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)美國廢棄物衍生可再生氣體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 可再生天然氣市場預測至2034年-按來源、生產流程、分銷方式、應用、最終用戶和地區分類的全球分析認證氣體市場預測-全球按來源、分銷方式、應用、最終用戶和地區分類的分析——2034年

可再生天然氣市場預測至2034年-按來源、生產流程、分銷方式、應用、最終用戶和地區分類的全球分析認證氣體市場預測-全球按來源、分銷方式、應用、最終用戶和地區分類的分析——2034年 天然氣市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、應用、地區和競爭格局分類,2021-2031年

天然氣市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、應用、地區和競爭格局分類,2021-2031年 2026年全球可再生天然氣(RNG)承購保險市場報告天然氣市場預測至2034年-按產品類型、類別、來源、通路、應用、最終用戶和地區分類的全球分析

2026年全球可再生天然氣(RNG)承購保險市場報告天然氣市場預測至2034年-按產品類型、類別、來源、通路、應用、最終用戶和地區分類的全球分析 全球可再生天然氣市場:按應用、產品類型、生產技術、來源/原料類型和地區分類-市場規模、產業動態、機會分析和預測(2026-2035 年)

全球可再生天然氣市場:按應用、產品類型、生產技術、來源/原料類型和地區分類-市場規模、產業動態、機會分析和預測(2026-2035 年)