|

市場調查報告書

商品編碼

2072660

印度獨立顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

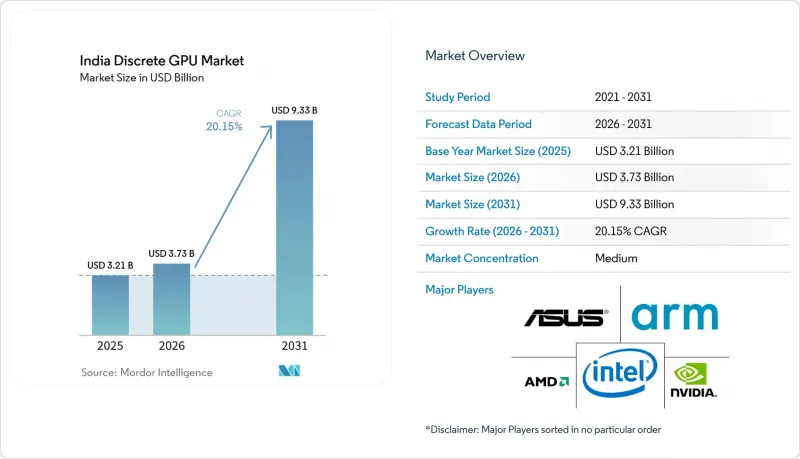

根據 Mordor Intelligence 預測,印度獨立 GPU 市場預計將從 2025 年的 32.1 億美元成長到 2026 年的 37.3 億美元,到 2031 年達到 93.3 億美元,2026 年至 2031 年的複合年成長率預計為 20.15%。

本報告按裝置應用(行動裝置和平板電腦、PC 和工作站、伺服器和資料中心加速器、遊戲主機等)、記憶體類型(基於 GDDR 的 GPU 和基於 HBM 的 GPU)以及效能等級(低成本 GPU、主流 GPU、高效能消費級 GPU 和資料中心/AI 加速器 GPU)進行細分。市場預測以美元 (USD) 為單位。

印度獨立GPU市場的趨勢與洞察

越來越多的AI工作負載需要GPU加速

印度超大規模資料中心營運商正從試點叢集轉向數吉瓦級園區,每個園區都配備功耗在 80 至 150 千瓦之間的 AI 機架。微軟已撥款 175 億美元,Google已撥款 150 億美元用於建造新的區域資料中心,這兩個資料中心都圍繞著高密度 GPU 架構進行了最佳化。政府採購不再是次要因素。 「印度人工智慧計畫」(IndiaAI Mission)已訂購了 38,000 個 GPU,目標是在 2027 年前達到 63,000 個,這進一步加劇了本已緊張的供應鏈壓力。營運商正在爭取多年期的配額以避免現貨市場價格虛高,這實際上加速了需求。因此,一種結構性轉變正在發生,AI 工作負載的成長速度超過了傳統的虛擬化,為印度獨立 GPU 市場的長期成長奠定了基礎。

Z世代與千禧世代中快速成長的PC遊戲文化

2025年第一季筆記型電腦出貨量年增8.1%,其中遊戲筆記型電腦的成長速度超過了消費級筆記型電腦。過去五年,客製化PC製造商實現了三位數的成長,這主要得益於YouTube和JioCinema等平台上面向數百萬觀眾直播的電子競技賽事。高通驍龍8 Elite搭載了1.1GHz三核心Adreno GPU,使其成為首款能夠即時處理虛幻引擎5 Nanite資源的行動晶片。隨著行動和桌面體驗的融合,獨立顯示卡市場正從PC擴展到手持設備。雲端遊戲服務與硬體需求並存,而非蠶食硬體需求,因為對於延遲敏感型遊戲,競爭對手仍然傾向於使用本地渲染。

持續的進口關稅推高了物料清單成本。

HS編碼85439000項下的顯示卡需繳納7.5%的關稅、10%的社會福利稅和18%的綜合商品及服務稅(IGST),導致零售價比到貨成本高出15-20%。到2026年初,如果美元兌印度盧比的外匯從82印度盧比升至85印度盧比,最終價格將再上漲3-4%。超大規模資料中心業者可以透過與原始設備製造商(OEM)直接交易來降低這種影響,但小規模系統整合商缺乏這種議價能力。在本地組裝擴大之前,關稅的不確定性將繼續阻礙普通消費者,從而拖累印度獨立顯示卡市場的複合年成長率(CAGR)。

細分市場分析

到2025年,伺服器和資料中心加速器將佔印度獨立GPU市場佔有率的38.62%,預計到2031年,該細分市場將以20.45%的複合年成長率成長。 Yotta斥資20億美元訂購20,736個Nvidia Blackwell Ultra模組,清楚展現了超大規模超大規模資料中心業者青睞專用AI晶片的趨勢。儘管隨著電子競技和內容創作的蓬勃發展,印度PC和工作站相關的獨立GPU市場規模依然強勁,但其成長速度與機架級部署相比有所放緩。行動裝置利用驍龍8 Elite的Adreno等整合GPU,正在模糊產品類別的界限,但其收入佔有率仍然有限。汽車ADAS和邊緣機器人正在成為新興的細分部署領域,創造了新的垂直市場,並擴大了需求,但在過去十年中,它們的規模尚未超過資料中心。

策略考量顯而易見:僅部署一塊 H100 級主機板即可省去 12 塊消費級 GPU,從而節省機架空間和電力。因此,企業預算正轉向 AI 加速器,即使銷售主要集中在中階產品,收入轉移的趨勢也在加速。儘管印度的獨立 GPU 產業仍在培養發燒友群體,但供應商的藍圖很可能將由超大規模訂單主導。整合商與 AMD 合作設計完整的 AI 架構(例如 TCS 與其 AMD MI455X叢集合作),正在提高承包效能的標準,並取代傳統的 OEM 配置。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- PC遊戲文化在Z世代和千禧世代中蓬勃發展。

- 印度資料中心對需要使用 GPU 加速的 AI 工作負載的需求日益成長。

- 印度政府的「印度製造」等措施正在促進國內GPU製造業的發展。

- 需要即時渲染的OTT影片製作工具的激增

- Web3新創公司,開發鏈上圖形引擎

- 在半都市區的醫院引進配備GPU的機載醫學影像技術

- 市場限制因素

- 持續的進口關稅推高了物料清單(BOM)成本。

- 電力基礎設施不足限制了高階GPU的普及。

- 印度 PCIe Gen 5 供應鏈地點短缺

- 工作站GPU售後服務網路碎片化

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過設備應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

- 按記憶體類型

- 配備 GDDR 記憶體的 GPU

- 配備 HBM 記憶體的 GPU

- 性能等級

- 低成本GPU(100美元以下)

- 主流GPU(100美元 - 400美元)

- 高效能消費級GPU(400美元至1200美元)

- 資料中心/AI加速器GPU(1200美元或以上)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Imagination Technologies Limited

- Arm Ltd.

- MediaTek Inc.

- Huawei Technologies Co., Ltd.(HiSilicon)

- ASUS Tek Computer Inc.

- GIGABYTE Technology Co., Ltd.

- Micro-Star International Co., Ltd.(MSI)

- Colorful Technology Company Limited

- EVGA Corporation

- Sapphire Technology Limited

- Palit Microsystems Ltd.

- Galax Technology Limited

- Leadtek Research Inc.

- Zotac Technology Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the india discrete GPU market size is expected to increase from USD 3.21 billion in 2025 to USD 3.73 billion in 2026 and reach USD 9.33 billion by 2031, growing at a CAGR of 20.15% over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles, and More), Memory Type (GDDR-Based GPUs, and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

India Discrete GPU Market Trends and Insights

Rising AI Workloads Demanding GPU Acceleration

India's hyperscale operators have moved from pilot clusters to multi-gigawatt campuses, each lined with AI racks that swallow 80-150 kilowatts. Microsoft earmarked USD 17.5 billion, and Google pledged USD 15 billion for new regional zones, both optimized around dense GPU fabrics. Government procurement is no longer peripheral; the IndiaAI Mission alone has ordered 38,000 GPUs and targets 63,000 units by 2027, tightening an already strained supply chain. Operators now lock in multi-year allocations to avoid spot-market premiums, effectively pulling forward demand. The upshot is a structural shift where AI workloads overshadow traditional virtualization, anchoring long-run growth for the India discrete GPU market.

Booming PC-Gaming Culture Among Gen-Z and Millennials

Notebook shipments climbed 8.1% year over year in Q1 2025 as gaming laptops outpaced mainstream models. Custom PC builders report triple-digit expansion over five years, driven by esports tournaments that stream to millions on YouTube and JioCinema. Qualcomm's Snapdragon 8 Elite added a three-core Adreno GPU clocked at 1.1 GHz, the first mobile silicon to handle Unreal Engine 5 Nanite assets in real time.This convergence between mobile and desktop experiences expands the addressable base for discrete graphics beyond PCs into handheld devices. Cloud gaming services coexist rather than cannibalize hardware demand because competitive players still prefer local rendering for latency-sensitive titles.

Persistent Import Tariffs Inflating BOM Costs

Graphics boards under HS 85439000 attract 7.5% customs duty, 10% social-welfare cess, and 18% IGST, pushing retail tags 15-20% above landed cost. Currency drift from INR 82 to INR 85 per USD by early 2026 adds another 3-4% to invoices. Hyperscalers mitigate the hit with direct OEM deals, but small system builders lack that leverage. Until local assembly scales, tariff uncertainty will keep mainstream buyers on the fence, shaving points off the India discrete GPU market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Government Initiatives Such as Make-in-India Boosting Local GPU Manufacturing

- Proliferation of OTT Video Creation Tools Needing Real-Time Rendering

- Power Infrastructure Deficits Limiting High-End GPU Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators represented 38.62% of India discrete GPU market share in 2025, and the segment is poised for a 20.45% CAGR through 2031. Yotta's USD 2 billion order for 20,736 Nvidia Blackwell Ultra modules exemplifies hyperscaler preference for purpose-built AI silicon. The India discrete GPU market size tied to PCs and workstations remains robust as esports and content creation flourish, yet growth tails off compared with rack-scale deployments. Mobile devices leverage integrated GPUs like Snapdragon 8 Elite's Adreno, blurring category lines but contributing modest revenue slices. Automotive ADAS and edge robotics emerge as niche adopters, introducing new verticals that broaden demand but will not outrun datacenter volume this decade.

The strategic calculus is clear: deploying one H100-class board offsets the need for a dozen consumer GPUs, saving rack space and power. Consequently, enterprise budgets are tilting toward AI accelerators, accelerating the revenue shift even if unit volumes skew to mid-tier parts. The India discrete GPU industry continues to cultivate enthusiast communities, but hyperscale orders will dominate supplier roadmaps. Integrators that co-design full AI fabrics, as TCS does with AMD MI455X clusters, are raising the bar for turnkey performance and displacing traditional OEM configurations.

Complete Report Scope:

- By Device Application

- Mobile Devices and Tablets

- PCs and Workstations

- Servers and Datacenter Accelerators

- Gaming Consoles and Handhelds

- Automotive / ADAS

- Other Embedded and Edge Devices

- By Memory Type

- GDDR-based GPUs

- HBM-based GPUs

- By Performance Tier

- Low-Cost GPUs (less than 100 USD)

- Mainstream GPUs (100 USD to 400 USD)

- High-Performance Consumer GPUs (400 USD to 1,200 USD)

- Data Center / AI Accelerator GPUs (greater than 1,200 USD)

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Imagination Technologies Limited

- Arm Ltd.

- MediaTek Inc.

- Huawei Technologies Co., Ltd. (HiSilicon)

- ASUS Tek Computer Inc.

- GIGABYTE Technology Co., Ltd.

- Micro-Star International Co., Ltd. (MSI)

- Colorful Technology Company Limited

- EVGA Corporation

- Sapphire Technology Limited

- Palit Microsystems Ltd.

- Galax Technology Limited

- Leadtek Research Inc.

- Zotac Technology Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming PC-gaming culture among Gen-Z and millennials

- 4.2.2 Rising AI workloads demanding GPU acceleration in Indian data centers

- 4.2.3 Government initiatives such as Make-in-India boosting local GPU manufacturing

- 4.2.4 Proliferation of OTT video creation tools needing real-time rendering

- 4.2.5 Under-reported: Web3 start-ups building on-chain graphics engines

- 4.2.6 Under-reported: Adoption of GPU-powered on-device medical imaging in semi-urban hospitals

- 4.3 Market Restraints

- 4.3.1 Persistent import tariffs inflating BOM costs

- 4.3.2 Power infrastructure deficits limiting high-end GPU deployment

- 4.3.3 Under-reported: Scarcity of PCIe Gen 5 supply chain nodes in India

- 4.3.4 Under-reported: Fragmented after-sales service network for workstation-grade GPUs

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-based GPUs

- 5.2.2 HBM-based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (less than 100 USD)

- 5.3.2 Mainstream GPUs (100 USD to 400 USD)

- 5.3.3 High-Performance Consumer GPUs (400 USD to 1,200 USD)

- 5.3.4 Data Center / AI Accelerator GPUs (greater than 1,200 USD)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Apple Inc.

- 6.4.7 Imagination Technologies Limited

- 6.4.8 Arm Ltd.

- 6.4.9 MediaTek Inc.

- 6.4.10 Huawei Technologies Co., Ltd. (HiSilicon)

- 6.4.11 ASUS Tek Computer Inc.

- 6.4.12 GIGABYTE Technology Co., Ltd.

- 6.4.13 Micro-Star International Co., Ltd. (MSI)

- 6.4.14 Colorful Technology Company Limited

- 6.4.15 EVGA Corporation

- 6.4.16 Sapphire Technology Limited

- 6.4.17 Palit Microsystems Ltd.

- 6.4.18 Galax Technology Limited

- 6.4.19 Leadtek Research Inc.

- 6.4.20 Zotac Technology Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment