|

市場調查報告書

商品編碼

2072659

日本獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)Japan Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

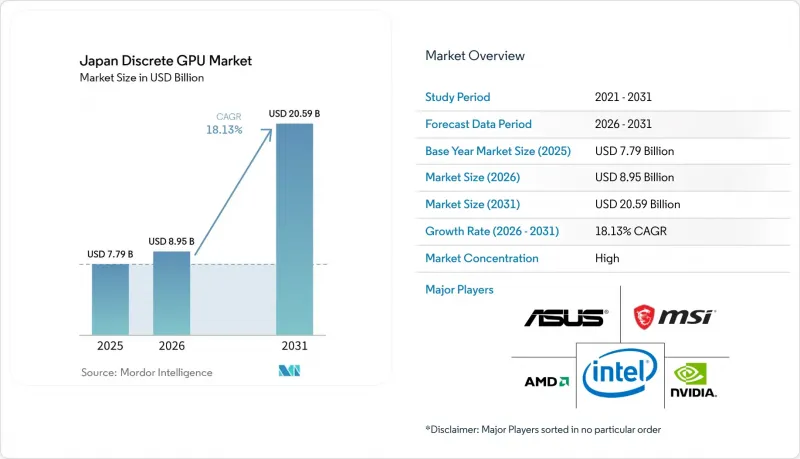

根據 Mordor Intelligence 預測,日本獨立 GPU 市場預計將從 2025 年的 77.9 億美元成長到 2026 年的 89.5 億美元,到 2031 年達到 205.9 億美元,2026 年至 2031 年的複合年預計成長率為 18.13%。

本報告按裝置應用(行動裝置和平板電腦、PC 和工作站、伺服器和資料中心加速器、遊戲主機等)、記憶體類型(基於 GDDR 的 GPU 和基於 HBM 的 GPU)以及效能等級(低成本 GPU、主流 GPU、高效能消費級 GPU 和資料中心/AI 加速器 GPU)進行分類。市場預測以美元 (USD) 為單位。

日本獨立顯示卡市場的趨勢與洞察

人工智慧工作負載的擴展正在推動對高階GPU的需求。

由於資料主權法規限制了高度敏感的訓練語料庫的出口,各公司正在建立基於HBM3E加速器的本地集群,這些加速器能夠處理擁有數兆參數的模型。Softbank Corporation與OpenAI於2026年2月簽署的關於大阪設施的協議,標誌著本地運算中心正逐漸取代離岸雲端服務。理研在其富嶽NEXT系統中採用2140塊Blackwell GPU,進一步凸顯了公共研究機構對尖端半導體技術的重要需求。微軟斥資100億美元擴充Azure的計劃,提升了私部門的影響力,並確保即使消費者需求放緩,訂單也能保持穩定。日本產業技術綜合研究所(AIST)於2026年2月對AMD的MI325X檢驗,加劇了價格競爭,並可能導致每年約12億美元公共支出的重新評估。因此,採購環境發生了變化,穩定的 HBM 供應被認為比逐步提高 teraflops 更重要,這進一步加強了記憶體供應商與 GPU 最終出貨量之間的連結。

汽車ADAS系統中GPU的應用日益廣泛

日本汽車製造商正將獨立GPU整合到其L3級自動駕駛系統中,將推理工作負載從CPU轉移到高吞吐量加速器。豐田的Arene軟體平台計劃在2026年前實現量產車型搭載GPU驅動的感測器融合技術,而本田與NVIDIA合作,計劃在2025年前在其所有電動車產品線中部署獨立GPU。漫長的設計檢驗週期意味著,單一設計方案的採用即可帶來長達十年的大訂單,從而為符合汽車級可靠性和ISO 26262標準的供應商提供穩定的收入來源。日本國土交通省的法規結構將於2025年正式定義功能安全測試要求,這將進一步鞏固那些能夠提供適用於汽車應用的現場故障率證明的供應商的地位。隨著每輛車中電動車零件比例的增加,GPU製造商將擁有更大的影響力,從而能夠直接簽訂供貨契約,繞過傳統的Tier 1仲介業者,提高利潤率。

供應鏈脆弱性與GPU供不應求

2025 年前的 HBM 產能主要分配給了簽訂多年合約的超大規模資料中心業者,迫使日本現貨買家等待 6-9 個月。由於 SK 海力士佔據了 HBM3E 產能的大部分,日本企業被迫在預付貨款以確保產能和承擔專案延期風險之間做出選擇。台積電的 CoWoS 先進封裝產能仍訂單,加劇了對整合邏輯晶片和高頻寬堆疊的基板的競爭。次市場已經出現,二手H100 GPU 的交易價格比標價高出 40%,扭曲了整體擁有成本 (TCO) 的計算。這些因素共同導致中小企業採用 AI 技術的速度放緩,造成需求積壓而短期出貨量下降。

細分市場分析

2025年,隨著企業加速建構生成式人工智慧叢集,伺服器和資料中心加速器在日本獨立GPU市場佔有率中佔比將達到39.58%。由於每個24GPU節點的成本有時超過200萬美元,且每個採購週期對收入的影響翻倍,預計該細分市場將成為日本獨立GPU市場成長最快的領域,複合年成長率將達到18.55%。理研(RIKEN)和產業技術綜合研究所(AIST)等公共機構正在推動多節點採購,從而保證了2031年的基準需求。曾經是銷售量主要驅動力的個人電腦和工作站,如今正面臨著整合顯示卡的市佔率侵蝕,整合顯示卡能夠滿足辦公室工作的生產力需求。獨立擴充卡範圍也日益局限於創新和CAD工作負載,在這些領域,透過CUDA和ROCm進行加速仍然至關重要。

在遊戲主機和掌上型遊戲機領域, SONY的系統晶片(SoC) 策略佔據主導地位,獨立 GPU 的成長潛力有限,因為圖形晶片在製造過程中就已經整合到設備中。汽車高級駕駛輔助系統 (ADAS) 作為新興但具有重要戰略意義的領域,已納入預測範圍。儘管豐田和本田等公司採用該設計已確保了未來十年的銷量,但短期總銷量仍然有限。工廠邊緣設備和保全攝影機開始需要獨立 GPU 來處理視覺工作負載,但這些部署仍處於試點階段,並受到整合預算的限制。總體而言,與資料中心應用相關的日本獨立 GPU 市場規模正在重塑通路經濟格局,其重點已從零售銷售速度轉向企業級支援合約。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧工作負載的增加正在推動對高階GPU的需求。

- 電腦遊戲和電競在日本日益普及

- 雲端遊戲基礎設施的擴展

- 汽車ADAS系統中GPU的應用日益廣泛

- 日本政府對半導體製造業的優惠待遇

- 邊緣人工智慧應用需要獨立GPU,其發展勢頭日益強勁。

- 市場限制因素

- 供應鏈脆弱性與GPU供不應求

- 高功耗阻礙了GPU在資料中心的普及。

- 與主流筆記型電腦整合顯示卡的競爭

- 日本的GPU IP開發受到限制。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按設備和應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

- 按記憶體類型

- 配備 GDDR 記憶體的 GPU

- 配備 HBM 記憶體的 GPU

- 按績效水準

- 低成本GPU(100美元以下)

- 主流GPU(100美元 - 400美元)

- 高效能消費級GPU(400美元至1200美元)

- 資料中心/AI加速器GPU(1200美元或以上)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nvidia Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Gigabyte Technology Co. Ltd.

- Palit Microsystems Ltd.

- Zhejiang Sapphire Technology Co. Ltd.

- Zotac Technology Limited

- Leadtek Research Inc.

- PowerColor Technology Inc.

- EVGA Corporation

- Lenovo Group Limited

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Acer Inc.

- Fujitsu Limited

- Sony Group Corporation

- NEC Corporation

- Panasonic Holdings Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan discrete GPU market size is expected to increase from USD 7.79 billion in 2025 to USD 8.95 billion in 2026 and reach USD 20.59 billion by 2031, growing at a CAGR of 18.13% over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles, and More), Memory Type (GDDR-Based GPUs, and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

Japan Discrete GPU Market Trends and Insights

Growth In AI Workloads Driving High-End GPU Demand

Sovereign-data mandates restrict the export of sensitive training corpora, so enterprises are building on-premises clusters with HBM3E-equipped accelerators that can tackle trillion-parameter models. SoftBank and OpenAI's February 2026 agreement for an Osaka facility exemplifies the pivot toward local compute centers that displace offshore cloud options. RIKEN's selection of 2,140 Blackwell GPUs for the FugakuNEXT system further underscores how public labs have become anchor tenants for bleeding-edge silicon.Microsoft's USD 10 billion Azure expansion adds private-sector heft, ensuring a steady pipeline of orders even if consumer demand cools. Validation of AMD's MI325X by the National Institute of Advanced Industrial Science and Technology in February 2026 introduces price tension that could reallocate roughly USD 1.2 billion in annual public spending. The upshot is a procurement environment where assured HBM supply is more valuable than incremental teraflop gains, tightening the link between memory vendors and final GPU shipments.

Increased Adoption Of GPUs In Automotive ADAS Systems

Japanese automakers are embedding discrete GPUs into level-3 autonomy stacks, shifting inference workloads from CPUs to high-throughput accelerators. Toyota's Arene software platform targets 2026 production vehicles with GPU-assisted sensor fusion, while Honda's 2025 collaboration with NVIDIA extends discrete GPUs across its electric lineup. Long design-validation cycles mean that a single design win can translate into decade-long volume commitments, smoothing revenue profiles for vendors that meet automotive-grade reliability and ISO 26262 standards. The Ministry of Land, Infrastructure, Transport, and Tourism's regulatory framework, which formalized functional-safety testing requirements in 2025, further entrenches vendors that can document field-failure rates compatible with automotive use. As electric-vehicle content per car rises, GPU makers also gain leverage to negotiate direct supply agreements, bypassing traditional tier-1 intermediaries and enhancing margin capture.

Supply Chain Vulnerabilities And GPU Shortages

HBM production through 2025 is fully allocated, largely to hyperscalers that secured multiyear agreements, leaving spot buyers in Japan with six-to-nine-month wait times. Because SK Hynix commands most HBM3E output, Japanese firms must either prepay to lock in slots or risk slipping project timelines. TSMC's CoWoS advanced-packaging capacity remains oversubscribed, intensifying competition for substrates that marry logic dies to high-bandwidth stacks. Secondary markets have emerged in which refurbished H100 GPUs command 40% premiums over list price, distorting total cost of ownership calculations. These factors collectively delay AI rollouts at small and midsize enterprises, trimming near-term shipments even as pent-up demand grows.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives For Semiconductor Manufacturing In Japan

- Rising Popularity Of PC Gaming And eSports In Japan

- High Power Consumption Limiting GPU Deployments In Datacenters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators captured 39.58% of the Japan discrete GPU market share in 2025 as enterprises rushed to establish generative-AI clusters. This slice of the Japan discrete GPU market will rise fastest, advancing at an 18.55% CAGR, because each 24-GPU node can cost upward of USD 2 million, multiplying the revenue impact of every procurement cycle. Public institutions such as RIKEN and the National Institute of Advanced Industrial Science and Technology are anchoring multi-node purchases that guarantee baseline demand through 2031. PCs and workstations, once the volume backbone, now face cannibalization from integrated graphics that meet office-productivity needs, relegating discrete add-in cards to creative and CAD workloads where CUDA or ROCm acceleration remains indispensable.

Gaming consoles and handhelds, dominated by Sony's system-on-chip strategy, offer limited upside for discrete GPUs because graphics silicon is integrated at manufacture. Automotive ADAS enters the forecast as an emerging yet strategic slice: Toyota and Honda design wins lock in volume over 10-year lifecycles, though near-term unit totals are modest. Edge devices in factories and security cameras are beginning to specify discrete GPUs for vision workloads, but these deployments remain pilot-stage and subject to integration budgets. Overall, the Japan discrete GPU market size tied to datacenter use is redefining channel economics, shifting emphasis toward enterprise-grade support contracts and away from retail sell-through velocity.

Complete Report Scope:

- By Device Application

- Mobile Devices and Tablets

- PCs and Workstations

- Servers and Datacenter Accelerators

- Gaming Consoles and Handhelds

- Automotive / ADAS

- Other Embedded and Edge Devices

- By Memory Type

- GDDR-based GPUs

- HBM-based GPUs

- By Performance Tier

- Low-Cost GPUs (less than 100 USD)

- Mainstream GPUs (100 USD to 400 USD)

- High-Performance Consumer GPUs (400 USD to 1,200 USD)

- Data Center / AI Accelerator GPUs (greater than 1,200 USD)

List of Companies Covered in this Report:

- Nvidia Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Gigabyte Technology Co. Ltd.

- Palit Microsystems Ltd.

- Zhejiang Sapphire Technology Co. Ltd.

- Zotac Technology Limited

- Leadtek Research Inc.

- PowerColor Technology Inc.

- EVGA Corporation

- Lenovo Group Limited

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Acer Inc.

- Fujitsu Limited

- Sony Group Corporation

- NEC Corporation

- Panasonic Holdings Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in AI Workloads Driving High-End GPU Demand

- 4.2.2 Rising Popularity of PC Gaming and eSports in Japan

- 4.2.3 Expansion of Cloud Gaming Infrastructure

- 4.2.4 Increased Adoption of GPUs in Automotive ADAS Systems

- 4.2.5 Government Incentives for Semiconductor Manufacturing in Japan

- 4.2.6 Emergence of Edge AI Applications Requiring Discrete GPUs

- 4.3 Market Restraints

- 4.3.1 Supply Chain Vulnerabilities and GPU Shortages

- 4.3.2 High Power Consumption Limiting GPU Deployments in Data Centers

- 4.3.3 Competition from Integrated GPUs in Mainstream Laptops

- 4.3.4 Limited Domestic GPU IP Development in Japan

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-based GPUs

- 5.2.2 HBM-based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (less than 100 USD)

- 5.3.2 Mainstream GPUs (100 USD to 400 USD)

- 5.3.3 High-Performance Consumer GPUs (400 USD to 1,200 USD)

- 5.3.4 Data Center / AI Accelerator GPUs (greater than 1,200 USD)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nvidia Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 ASUSTeK Computer Inc.

- 6.4.5 Micro-Star International Co. Ltd.

- 6.4.6 Gigabyte Technology Co. Ltd.

- 6.4.7 Palit Microsystems Ltd.

- 6.4.8 Zhejiang Sapphire Technology Co. Ltd.

- 6.4.9 Zotac Technology Limited

- 6.4.10 Leadtek Research Inc.

- 6.4.11 PowerColor Technology Inc.

- 6.4.12 EVGA Corporation

- 6.4.13 Lenovo Group Limited

- 6.4.14 Dell Technologies Inc.

- 6.4.15 Hewlett Packard Enterprise Company

- 6.4.16 Acer Inc.

- 6.4.17 Fujitsu Limited

- 6.4.18 Sony Group Corporation

- 6.4.19 NEC Corporation

- 6.4.20 Panasonic Holdings Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment