|

市場調查報告書

商品編碼

2072658

德國獨立顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Germany Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

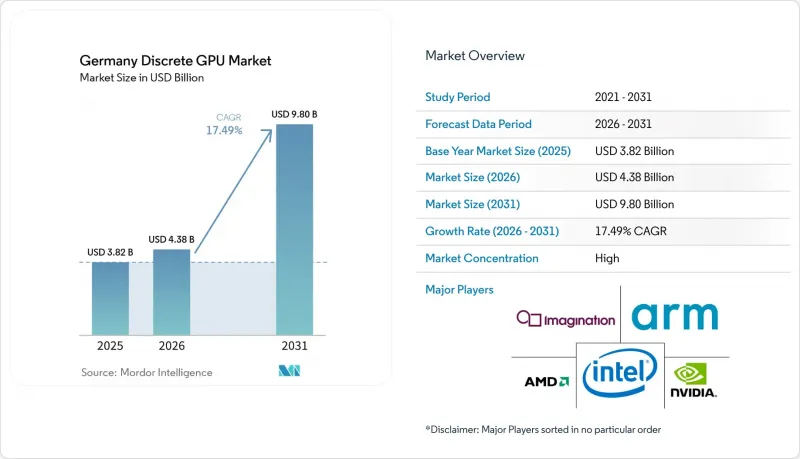

根據 Mordor Intelligence 預測,德國獨立 GPU 市場預計將從 2025 年的 38.2 億美元成長到 2026 年的 43.8 億美元,到 2031 年達到 98 億美元,2026 年至 2031 年的複合年成長率預計為 17.49%。

本報告按裝置應用(行動裝置和平板電腦、PC 和工作站、伺服器和資料中心加速器、遊戲主機等)、記憶體類型(基於 GDDR 的 GPU 和基於 HBM 的 GPU)以及效能等級(低成本 GPU、主流 GPU、高效能消費級 GPU 和資料中心/AI 加速器 GPU)進行細分。市場預測以美元 (USD) 為單位。

德國獨立顯示卡市場的趨勢與洞察

德國資料中心對人工智慧和高效能運算工作負載的需求激增

德國的「主權人工智慧」策略正將GPU供應轉向企業級機架。在德國電信位於慕尼黑的圖赫爾帕克園區,超過1000套DGX B200系統正在運作,每套系統消耗12兆瓦再生能源,並提供近0.5百億億次浮點運算的運算能力。西門子、AgileRobots和Quantum Systems等早期採用者正在本地訓練數位雙胞胎和模擬工作負載,以滿足歐盟的資料居住要求。位於利希、弗萊堡和漢堡的類似GPU叢集使德國新增加速器總數接近4萬台,隨著零售配額的減少,導致供不應求。

德國擁有強大的PC遊戲和電子競技生態系統

2025年,德國遊戲玩家的消費總額達到94億歐元(106億美元),其中硬體支出較去年同期成長12%。儘管如此,主要零售商的獨立顯示卡週銷量卻從約2,800塊驟降至675塊,降幅高達76%。價格彈性仍然很高,NVIDIA產品的平均售價上漲至1,100歐元(1,243美元),AMD產品的平均售價上漲至585歐元(661美元),但銷售仍成長。 2026年,聯邦政府對遊戲工作室的津貼增加至1.25億歐元(1.41億美元),確保了依賴高階顯示卡的本土遊戲的穩定供應。

供應鏈中斷與GPU供不應求

由於台積電CoWoS封裝生產線產能不足,以及SK海力士、美光和三星的HBM3E顯存供應緊張,德國零售庫存已跌至歷史新低。 RTX 5090的市價超過4000美元,是廠商建議零售價的兩倍,就連AMD的中階顯示卡也出現了長達數週的缺貨情況。政府主導的自主雲端推廣進一步加劇了供應短缺,通訊業者紛紛下單,導致消費者管道被邊緣化。

細分市場分析

到2025年,伺服器和資料中心加速器將佔德國獨立顯示卡市場收入的40.73%,反映了自主人工智慧叢集的快速普及。預計到2031年,該細分市場將以17.75%的複合年成長率成長,並將繼續成為德國獨立顯示卡市場成長的基石。消費級PC和專業工作站共同構成了第二大支柱,但隨著供應轉向企業級機架,它們的銷售量正在急劇下降。遊戲主機和掌上型遊戲機仍然是一個小眾市場,因為它們捆綁的是客製化APU而非獨立顯示卡,而輕薄筆記型電腦中的整合式顯示卡進一步削弱了入門級市場的需求。

德國伺服器用獨立GPU市場預計將持續擴張,德國電信、Google和施瓦茲集團計畫在2027年前完工的設施中總合超過3萬塊加速器。汽車邊緣伺服器運行數位雙胞胎,以及需要本地推理處理的工業4.0閘道器,是推動獨立GPU長尾應用的主要動力。同時,在行動裝置和平板電腦領域,整合GPU的ARM架構SoC佔據主導地位,這拖慢了獨立GPU的搭載率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 德國資料中心對人工智慧和高效能運算工作負載的需求激增

- 德國擁有強大的PC遊戲和電子競技生態系統

- 專業視覺化領域擴大採用GPU加速工作站。

- 能源效率法規正在推動GPU節點向最先進的方向升級。

- 德國IPCEI微電子計畫下的半導體投資聯邦補貼

- 一個需要嵌入式獨立GPU的工業4.0邊緣運算示範專案。

- 市場限制因素

- 供應鏈中斷與GPU供不應求

- 高性能GPU的初始成本很高

- 歐盟嚴格的環境法規正在增加整個生命週期的合規成本。

- 入門級市場中與整合GPU的競爭

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按設備和應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

- 按記憶體類型

- 配備 GDDR 記憶體的 GPU

- 配備 HBM 記憶體的 GPU

- 按績效水準

- 低成本GPU(100美元以下)

- 主流GPU(100美元 - 400美元)

- 高效能消費級GPU(400美元至1200美元)

- 資料中心/AI加速器GPU(超過1200美元)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Imagination Technologies Limited

- ARM Limited

- QUALCOMM Incorporated

- Samsung Electronics Co., Ltd.

- Apple Inc.

- HUAWEI Technologies Co., Ltd.

- MediaTek Inc.

- VIA Technologies Inc.

- Zhaoxin Semiconductor Co., Ltd.

- Tachyum sro

- Graphcore Limited

- Tenstorrent, Inc.

- SiPearl SAS

- SAPPHIRE Technology Limited

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- Gigabyte Technology Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany discrete GPU market size is expected to increase from USD 3.82 billion in 2025 to USD 4.38 billion in 2026 and reach USD 9.80 billion by 2031, growing at a CAGR of 17.49% over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles, and More), Memory Type (GDDR-Based GPUs, and HBM-Based GPUs), and Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

Germany Discrete GPU Market Trends and Insights

Surging Demand for AI and HPC Workloads in German Data Centers

Germany's sovereign-AI strategy has tilted GPU supply toward enterprise racks. Deutsche Telekom's Tucherpark campus in Munich operates more than 1,000 DGX B200 systems, each drawing 12 MW of renewable power and delivering almost half an exaflop of compute. Early adopters, including Siemens, Agile Robots, and Quantum Systems, train digital twins and simulation workloads locally to comply with EU data-residency rules. Similar GPU clusters at Julich, Freiburg, and Hamburg bring the national total to nearly 40,000 new accelerators, prompting consumer shortages as retail allocations shrink.

Robust PC Gaming and Esports Ecosystem in Germany

German gamers spent EUR 9.4 billion (USD 10.6 billion) in 2025, with hardware outlays up 12% year on year. Despite the enthusiasm, weekly discrete GPU sales at top retailers slid from roughly 2,800 cards to 675, evidencing a 76% unit collapse. Price elasticity remains high: average selling prices rose to EUR 1,100 (USD 1,243) for NVIDIA and EUR 585 (USD 661) for AMD, yet revenue still advanced.Federal grants for game studios climbed to EUR 125 million (USD 141 million) in 2026, ensuring a steady pipeline of domestic titles that rely on high-end graphics.

Supply Chain Disruptions and GPU Shortages

TSMC's limited CoWoS packaging lines and tight HBM3E supply from SK Hynix, Micron, and Samsung have pushed German retail inventories to historic lows. Street prices for an RTX 5090 exceed USD 4,000, double the launch MSRP, and even AMD's mid-range cards face multi-week backorders. The government's sovereign-cloud push intensifies the squeeze as operators lock in bulk orders, sidelining consumer channels.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of GPU-Accelerated Workstations for Professional Visualization

- Energy-Efficiency Mandates Driving Upgrades to Advanced GPU Nodes

- High Up-Front Cost of High-Performance GPUs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators contributed 40.73% of 2025 revenue to the Germany discrete GPU market share, reflecting the rapid installation of sovereign-AI clusters. The segment is projected to post a 17.75% CAGR to 2031, ensuring it remains the linchpin of Germany discrete GPU market growth. Consumer PCs and professional workstations together form the second pillar, yet their volumes have fallen sharply as supply diverts toward enterprise racks. Gaming consoles and handhelds remain niche because they bundle custom APUs rather than discrete cards, while integrated GPUs in thin-and-light notebooks further erode entry-level demand.

Germany discrete GPU market size for servers will continue to swell as Deutsche Telekom, Google, and Schwarz Group collectively add another 30,000-plus accelerators in sites scheduled for completion by 2027. Automotive edge servers running digital twins, along with Industry 4.0 gateways that need local inferencing, strengthen long-tail adoption. Conversely, mobile and tablet categories lean on ARM-based SoCs with embedded GPUs, undercutting discrete attach rates.

Complete Report Scope:

- By Device Application

- Mobile Devices and Tablets

- PCs and Workstations

- Servers and Datacenter Accelerators

- Gaming Consoles and Handhelds

- Automotive / ADAS

- Other Embedded and Edge Devices

- By Memory Type

- GDDR-based GPUs

- HBM-based GPUs

- By Performance Tier

- Low-Cost GPUs (less than 100 USD)

- Mainstream GPUs (100 USD to 400 USD)

- High-Performance Consumer GPUs (400 USD to 1,200 USD)

- Data Center / AI Accelerator GPUs (greater than 1,200 USD)

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Imagination Technologies Limited

- ARM Limited

- QUALCOMM Incorporated

- Samsung Electronics Co., Ltd.

- Apple Inc.

- HUAWEI Technologies Co., Ltd.

- MediaTek Inc.

- VIA Technologies Inc.

- Zhaoxin Semiconductor Co., Ltd.

- Tachyum s.r.o.

- Graphcore Limited

- Tenstorrent, Inc.

- SiPearl SAS

- SAPPHIRE Technology Limited

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- Gigabyte Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for AI and HPC Workloads in German Data Centers

- 4.2.2 Robust PC Gaming and Esports Ecosystem in Germany

- 4.2.3 Growing Adoption of GPU-Accelerated Workstations for Professional Visualization

- 4.2.4 Energy-Efficiency Mandates Driving Upgrades to Advanced GPU Nodes

- 4.2.5 Federal Subsidies for Semiconductor Investment Under Germany's IPCEI Microelectronics Program

- 4.2.6 Industry 4.0 Edge Computing Pilots Requiring Embedded Discrete GPUs

- 4.3 Market Restraints

- 4.3.1 Supply Chain Disruptions and GPU Shortages

- 4.3.2 High Up-Front Cost of High-Performance GPUs

- 4.3.3 Stringent EU Environmental Regulations Increasing Lifecycle Compliance Costs

- 4.3.4 Competition from Integrated GPUs in Entry-Level Segments

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-based GPUs

- 5.2.2 HBM-based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (less than 100 USD)

- 5.3.2 Mainstream GPUs (100 USD to 400 USD)

- 5.3.3 High-Performance Consumer GPUs (400 USD to 1,200 USD)

- 5.3.4 Data Center / AI Accelerator GPUs (greater than 1,200 USD)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Imagination Technologies Limited

- 6.4.5 ARM Limited

- 6.4.6 QUALCOMM Incorporated

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 Apple Inc.

- 6.4.9 HUAWEI Technologies Co., Ltd.

- 6.4.10 MediaTek Inc.

- 6.4.11 VIA Technologies Inc.

- 6.4.12 Zhaoxin Semiconductor Co., Ltd.

- 6.4.13 Tachyum s.r.o.

- 6.4.14 Graphcore Limited

- 6.4.15 Tenstorrent, Inc.

- 6.4.16 SiPearl SAS

- 6.4.17 SAPPHIRE Technology Limited

- 6.4.18 ASUSTeK Computer Inc.

- 6.4.19 Micro-Star International Co., Ltd.

- 6.4.20 Gigabyte Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment