|

市場調查報告書

商品編碼

2065433

亞太地區獨立顯示卡市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)Asia-Pacific Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

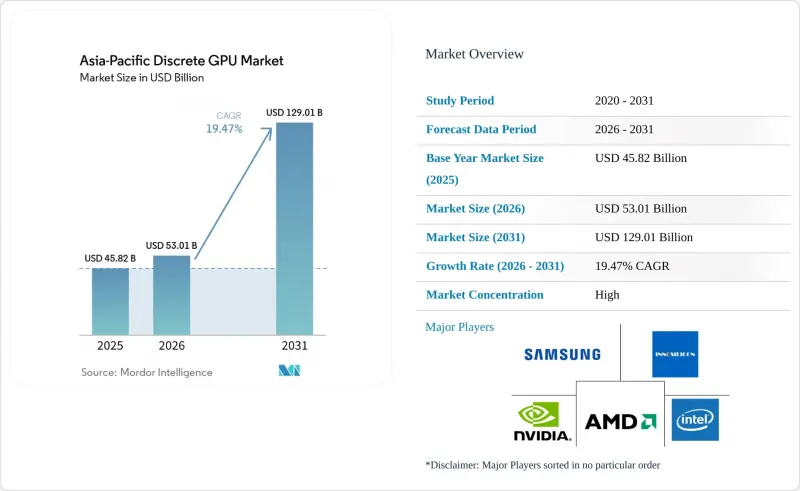

根據 Mordor Intelligence 預測,亞太地區獨立 GPU 市場規模預計將從 2025 年的 458.2 億美元成長到 2026 年的 530.1 億美元,然後在 2031 年達到 1,290.1 億美元,2026 年至 2031 年的複合年成長率為 19.99%。

本報告按裝置應用(行動裝置和平板電腦、PC 和工作站、伺服器和資料中心加速器等)、記憶體類型(基於 GDDR 的 GPU 和基於 HBM 的 GPU)、效能等級(低成本 GPU、主流 GPU、高效能消費級 GPU 等)以及國家/地區(中國、日本、韓國等)進行細分。市場預測以美元 (USD) 為單位。

亞太地區獨立GPU市場的趨勢與洞察

人工智慧訓練和推理工作負載呈指數級成長

到2025年,大規模語言模型中的參數數量將超過1兆,計算密度將遠遠超過整合顯示卡的運算能力。 2026年3月,Meta公司訂購了6吉瓦的AMD Instinct MI455X顯示卡,而Oracle公司則為其雲端環境訂購了5萬台MI450設備。印度已累計12.4億美元,計劃在2025年前部署1萬個GPU,並力爭在其「主權運算」計畫下,於2027年前達到10萬個。日本和韓國正在建造百萬兆級叢集,累計均約40億美元,將人工智慧基礎設施轉變為戰略資產。這些部署正在縮短更新周期,加速資本投資,並增加對採用HBM3E記憶體和先進封裝技術的頂級加速器的需求。

亞太地區超大規模資料中心快速擴張

AWS正在澳洲投資200億澳元(130億美元)用於企業發展;微軟已獲得29億美元資金以確保在日本的資料中心容量;Google承諾投資30億美元在馬哈拉斯特拉邦建設一座設施,該設施將於2027年提供200兆瓦的電力。新加坡的「資料中心優先框架2025」也分配了200兆瓦的電力,但強制要求可再生能源佔比達到50%,且PUE值低於1.3,這實際上要求部署液冷GPU機架,這將使資本支出增加15-20%。騰訊雲端和阿里雲目前正在為NVIDIA A100執行個體推出靈活的收費模式,獨立GPU的購買力正從企業轉向超大規模資料中心業者。這些投資推動了H100和MI300X顯示卡的集中採購,維持了亞太地區獨立GPU市場的需求,同時也加劇了CoWoS產能的供應鏈壓力。

先進製程節點供應鏈持續波動

到2026年底,台積電的CoWoS生產線在月晶圓加工量方面取得了突破性進展。然而,對於新進業者而言,情況依然嚴峻,NVIDIA佔據了大部分產能,AMD緊隨其後。到2025年中期,H100的前置作業時間將達到52週,迫使客戶提前18-24個月預訂,限制了預算柔軟性。 H100對中國的出口上限為每月4800片,導致買家轉向灰色市場,價格比標價高出60%,或選擇性能較低且需要授權的A800衍生產品。由於SK海力士將其80%的HBM3E產能分配給NVIDIA,HBM供應依然緊張,促使NVIDIA在2026年3月宣布了一項130億美元的擴張計劃,但預計這種情況要到2028年或更晚才會有所緩解。這些瓶頸導致部署延遲和成本超支,給亞太地區的獨立GPU市場帶來了沉重負擔。

細分市場分析

到2025年,伺服器和資料中心加速器將佔銷售額的40.10%,凸顯了基於超大規模資料中心業者中心和自主雲端建構的AI訓練叢集的關鍵作用。隨著企業將推理處理從公共雲端遷移到成本最佳化的本地機架,亞太地區的獨立GPU市場預計到2031年將以19.73%的複合年成長率成長。 NVIDIA H100和AMD MI300X顯示卡的單價約為3萬美元,佔據了新增部署容量的很大一部分,儘管其銷量落後於消費級顯示卡。工作站GPU對於使用CUDA和ROCm管線的內容創作者仍然至關重要,而受任天堂預計在2026年底發布新主機的推動,遊戲主機的需求保持穩定。汽車產業的應用仍處於早期階段,但比亞迪等中國電動車製造商正在評估用於身臨其境型座艙顯示器的獨立模組。邊緣運算和工業設備正在悄然成長,因為它們將低功耗電路板與 CPU 無法處理的機器視覺工作負載相結合。

由於整合顯示卡在不增加任何組件成本的情況下,效能已達到獨立顯示卡的80-90%,主流PC和筆記型電腦的需求正面臨利潤率壓力。然而,在Adobe Premiere和Blender渲染等專業視覺化環境中,獨立顯示卡仍然是首選。混合架構遊戲手持終端機推動了銷售成長,而由於資料中心持續短缺,剩餘的消費級顯示卡正被學術研究叢集所採用。儘管出貨配置正向加速器傾斜,但由於消費級顯示卡的高價格彈性和資料中心顯示卡的低價彈性,此細分市場整體保持穩定。在資料主權政策和法規日益嚴格的背景下,區域系統整合商正將700瓦顯卡、水冷系統和可再生能源採購合約打包成交承包機架,這正在推動長期成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 亞太地區獨立GPU市場

- 人工智慧訓練和推理工作負載呈指數級成長。

- AAA級PC和行動遊戲的日益普及

- 中國和印度都制定了國家層級的GPU國產化計畫。

- 亞太地區超大規模資料中心快速擴張

- 將獨立GPU整合到下一代擴增實境(AR)眼鏡中

- 來自區域雲端提供者的捆綁式「GPU即服務」服務

- 市場限制因素

- 先進製程節點供應鏈持續波動

- 整合GPU的入門級設備之間的競爭日益激烈。

- 不同地區能源成本的上漲正在影響資料中心 GPU 的總擁有成本 (TCO)。

- 高密度城市資料中心冷卻基礎設施的局限性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按設備和應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

- 按記憶體類型

- 配備 GDDR 記憶體的 GPU

- 配備 HBM 記憶體的 GPU

- 按績效水準

- 低成本GPU(100美元以下)

- 主流GPU(100-400美元)

- 高效能消費級GPU(400美元至1200美元)

- 資料中心/AI加速器GPU(超過1200美元)

- 國家

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- ASUSTeK Computer Inc.

- Gigabyte Technology Co., Ltd.

- Micro-Star International Co., Ltd.

- Colorful Technology Company Limited

- Leadtek Research Inc.

- Sapphire Technology Limited

- Palit Microsystems Ltd.

- Innosilicon Technology(Shanghai)Co., Ltd.

- Biren Technology Co., Ltd.

- Moore Threads Intelligent Technology(Beijing)Co., Ltd.

- Shanghai Tianshu Zhixin Semiconductor Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific discrete GPU market size is expected to grow from USD 45.82 billion in 2025 to USD 53.01 billion in 2026 and is forecast to reach USD 129.01 billion by 2031 at a 19.47% CAGR over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, and More), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and More), and Country (China, Japan, South Korea, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Discrete GPU Market Trends and Insights

Exponential Growth in AI Training and Inference Workloads

Parameter counts on large language models crossed the 1-trillion threshold in 2025, pushing compute density well beyond integrated-graphics capabilities. Meta contracted 6 gigawatts of AMD Instinct MI455X capacity in March 2026, while Oracle ordered 50,000 MI450 devices for its cloud estate. India earmarked USD 1.24 billion for 10,000 GPUs in 2025 and aims to reach 100,000 units by 2027 under its sovereign-compute agenda. Japan and South Korea have each budgeted roughly USD 4 billion to stand up exascale clusters, turning AI infrastructure into a strategic asset. These deployments shorten replacement cycles, front-load capital expenditure, and lift demand for top-tier accelerators featuring HBM3E memory and advanced packaging.

Rapid Expansion of Hyperscale Data Centers Across Asia-Pacific

AWS committed AUD 20 billion (USD 13 billion) to its Australian footprint, Microsoft reserved USD 2.9 billion for Japanese capacity, and Google pledged USD 3 billion for a Maharashtra facility delivering 200 megawatts by 2027. Singapore's 2025 DataCenter-First Framework allocated 200 megawatts but mandates 50% renewable power and a sub-1.3 PUE, effectively requiring liquid-cooled GPU racks that add 15-20% to capex. Tencent Cloud and Alibaba Cloud now package NVIDIA A100 instances with elastic billing, shifting discrete GPU purchases from enterprises to hyperscalers. These investments underpin a dense procurement cycle for H100 and MI300X boards, sustain demand in the Asia-Pacific discrete GPU market, and intensify supply-chain pressure on CoWoS capacity.

Ongoing Supply Chain Volatility for Advanced Process Nodes

By late 2026, TSMC's CoWoS line achieved a milestone of processing wafers monthly. However, NVIDIA secured a dominant share of that output, with AMD trailing, creating a tight squeeze for potential new entrants. H100 lead times stretched to 52 weeks in mid-2025, forcing customers into 18-24-month preorder windows that erode budgeting flexibility. Export-control ceilings of 4,800 H100 units per month for China diverted buyers to gray-market boards priced up to 60% above list or to lower-performance A800 variants requiring licenses. HBM supply remains tight as SK Hynix allocates 80% of HBM3E volume to NVIDIA, prompting a USD 13 billion expansion plan announced in March 2026, but relief arrives only after 2028. These bottlenecks weigh on the Asia-Pacific discrete GPU market by delaying deployments and inflating costs.

Other drivers and restraints analyzed in the detailed report include:

- National Initiatives for Domestic GPU Manufacturing in China and India

- Rising Popularity of AAA PC and Mobile Gaming Titles

- Intensifying Price Competition from Integrated GPUs in Entry-Level Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators generated 40.10% of 2025 revenue, underscoring the outsized role of AI training clusters built by hyperscalers and sovereign clouds. The Asia-Pacific discrete GPU market is projected to expand at a 19.73% CAGR through 2031 as enterprises repatriate inference from public clouds to cost-optimized on-premises racks. NVIDIA H100 and AMD MI300X boards, priced near USD 30,000 per unit, dominate new capacity even though unit volumes trail those of consumer cards. Workstation GPUs remain important for creators using CUDA and ROCm pipelines, while console demand stays stable on the back of Nintendo's expected late-2026 launch. Automotive adoption is nascent, yet Chinese EV makers such as BYD evaluate discrete modules for immersive cabin displays. Edge-industrial devices are a quiet growth pocket, pairing low-power boards with machine-vision workloads that CPUs cannot service.

Mainstream PC and notebook demand faces margin compression as integrated GPUs reach 80-90% of discrete performance at zero incremental bill-of-materials cost. Nevertheless, professional visualization rigs still prefer discrete cards for Adobe Premiere and Blender rendering. Gaming handhelds with hybrid architectures spur incremental volume, while research clusters in academia adopt surplus consumer cards when datacenter stockouts persist. The segment's blend of price-elastic consumer sales and inelastic datacenter buys helps stabilize overall revenue, even as shipment mix shifts toward accelerators. As policy mandates tighten data sovereignty, regional system integrators bundle turnkey racks with 700-watt GPUs, liquid cooling, and renewable-energy sourcing agreements, reinforcing long-run growth.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- ASUSTeK Computer Inc.

- Gigabyte Technology Co., Ltd.

- Micro-Star International Co., Ltd.

- Colorful Technology Company Limited

- Leadtek Research Inc.

- Sapphire Technology Limited

- Palit Microsystems Ltd.

- Innosilicon Technology (Shanghai) Co., Ltd.

- Biren Technology Co., Ltd.

- Moore Threads Intelligent Technology (Beijing) Co., Ltd.

- Shanghai Tianshu Zhixin Semiconductor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Asia Pacific Discrete GPU Market

- 4.2.2 Exponential Growth in AI Training and Inference Workloads

- 4.2.3 Rising Popularity of AAA PC and Mobile Gaming Titles

- 4.2.4 National Initiatives for Domestic GPU Manufacturing in China and India

- 4.2.5 Rapid Expansion of Hyperscale Data Centers Across Asia-Pacific

- 4.2.6 Integration of Discrete GPUs into Next-Gen Augmented Reality Glasses

- 4.2.7 Bundled GPU-as-a-Service Offerings by Regional Cloud Providers

- 4.3 Market Restraints

- 4.3.1 Ongoing Supply Chain Volatility for Advanced Process Nodes

- 4.3.2 Intensifying Price Competition from Integrated GPUs in Entry-Level Devices

- 4.3.3 Escalating Regional Energy Tariffs Hitting Datacenter GPU TCO

- 4.3.4 Cooling Infrastructure Limits in Dense Urban Datacenters

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-based GPUs

- 5.2.2 HBM-based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (Less than USD 100)

- 5.3.2 Mainstream GPUs (USD 100-USD 400)

- 5.3.3 High-Performance Consumer GPUs (USD 400-USD 1,200)

- 5.3.4 Data Center / AI Accelerator GPUs (Greater than USD 1,200)

- 5.4 By Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 South Korea

- 5.4.4 India

- 5.4.5 Southeast Asia

- 5.4.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 ASUSTeK Computer Inc.

- 6.4.7 Gigabyte Technology Co., Ltd.

- 6.4.8 Micro-Star International Co., Ltd.

- 6.4.9 Colorful Technology Company Limited

- 6.4.10 Leadtek Research Inc.

- 6.4.11 Sapphire Technology Limited

- 6.4.12 Palit Microsystems Ltd.

- 6.4.13 Innosilicon Technology (Shanghai) Co., Ltd.

- 6.4.14 Biren Technology Co., Ltd.

- 6.4.15 Moore Threads Intelligent Technology (Beijing) Co., Ltd.

- 6.4.16 Shanghai Tianshu Zhixin Semiconductor Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment