|

市場調查報告書

商品編碼

2072657

中國獨立顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)China Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

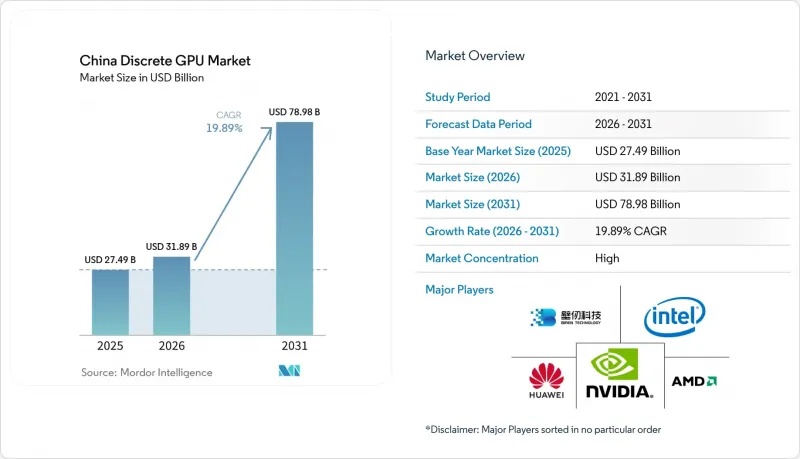

根據 Mordor Intelligence 預測,中國獨立 GPU 市場規模將從 2025 年的 274.9 億美元和 2026 年的 318.9 億美元成長到 2031 年的 789.8 億美元,2026 年至 2031 年的年複合成長率(CAGR)%為 19.89%。

本報告按裝置應用(行動裝置和平板電腦、PC 和工作站、伺服器和資料中心加速器、遊戲主機等)、記憶體類型(基於 GDDR 的 GPU 和基於 HBM 的 GPU)以及效能等級(低成本 GPU、主流 GPU、高效能消費級 GPU 和資料中心/AI 加速器 GPU)進行分類。市場預測以美元 (USD) 為單位。

中國獨立顯示卡市場的趨勢與洞察

中國超大規模資料中心對人工智慧訓練和推理工作負載的需求激增

超大規模資料中心營運商已將GPU採購列為首要資本投資重點。阿里雲計畫在2025會計年度投資530億美元,在國內伺服器機房部署超過10萬塊加速器。同年,位元組跳動投入230億美元訓練其豆寶平台模型,該模型需要約5萬塊H100級晶片。騰訊將其人工智慧相關資本投資加倍,並為其混元模型部署了新的GPU叢集。百度Ernie 4.0平台已運作,搭載約2萬塊獨立GPU,效能可與OpenAI媲美。這些部署均基於多年期供貨協議,該協議促進了與本地供應商的晶片和軟體聯合設計,從而緩解需求週期性波動並降低出口管制風險。

政府獎勵促進國內半導體自給自足和GPU創新

中國「國家積體電路產業投資基金三期」決定在2024年投入3,440億元(約470億美元),明確將GPU研發列為戰略重點領域。同年,國務院指示到2027年,政府和國營企業IT採購總量的一半必須採用國產半導體,無疑對國產圖形處理器產生了強勁的需求。上海將於2025年提供GPU新創企業20億元人民幣(約2.8億美元)的直接津貼,深圳和武漢也已效法此模式。工信部設定了2030年半導體自給率達到80%的目標,進一步將財政資源與藍圖的里程碑目標相符。人才引進措施已吸引3,500多名海外工程師回國,擴大了國內先進GPU架構所需的人才儲備。

美國出口限制阻礙了尖端GPU IP和HBM記憶體的取得。

2025年1月,美國出口管制條例修正案對銷往中國的GPU引入了性能上限,限制了其雙向傳輸速度和浮點運算吞吐量(DOC.GOV)。作為回應,NVIDIA推出了H20、L20和L2系列GPU。雖然這些GPU的訓練吞吐量比H100低約三分之一,但它們在2025年仍佔資料中心GPU銷售額的15%。由於漫長的授權流程,AMD的MI308GPU的廣泛上市時間被推遲到2025年第三季。美國要求SK海力士和美光減少HBM3顯存的出口,進一步加劇了供應壓力,導致對華配額減少了約40%。國內企業正在試行基於GDDR6X顯存的晶片佈局作為臨時措施,但這些替代方案會增加功耗和散熱成本。

細分市場分析

預計到2025年,中國獨立顯示卡市場中,伺服器和資料中心加速器將佔總收入的39.17%,凸顯了市場結構從純粹的消費級顯示卡向伺服器和資料中心顯示卡的轉變。阿里雲、騰訊、位元組跳動和百度等公司提前多年預訂了產能,推動了這個細分市場的發展,它們合計將其人工智慧加速器的產量擴大到30萬顆以上。這種採購模式有利於那些能夠提供具競爭力的性價比、同時滿足合規要求並確保季度穩定需求的廠商。專業視覺化和工作站顯示卡雖然與資料中心晶片有所不同,但它們在創新工作流程中創造的收入,預計到2025年將佔總收入的12%左右,因為內容工作室正在影片編輯和建築渲染等領域採用生成式人工智慧技術。

遊戲PC和工作站市場出貨量依然龐大,但由於平均售價趨於平穩,營收成長正在放緩。網咖和家庭發燒友持續更換PC,這得益於售價低於400美元的低成本國產GPU,這些GPU能夠提供電競等級的影格速率。車載GPU市場雖然起步較小,但正經歷快速成長。隨著理想汽車、蔚來汽車和小鵬汽車等公司將集中式運算單元推向主流市場,預計到2027年,其年出貨量將超過200萬台。涵蓋工業視覺和零售分析的邊緣設備仍在發展中,但憑藉數據本地化政策的推動,該領域前景廣闊。資料本地化政策抑制了雲端卸載,增加了對本地推理的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中國超大規模資料中心對人工智慧訓練和推理工作負載的需求激增

- 中國PC遊戲和電競生態系統的持續成長

- 政府激勵措施促進國內半導體自給自足和GPU創新。

- 汽車ADAS與自動駕駛平台中獨立GPU的快速普及

- 國內雲端 GPUaaS 供應商對中小企業 AI 工作負載的需求不斷成長。

- 翻新GPU出口的擴大正在推動國內升級週期和價格的正常化。

- 市場限制因素

- 美國出口限制阻礙了尖端GPU IP和HBM記憶體的取得。

- 全球半導體供應鏈面臨的壓力正在推高零件成本。

- 中國二級資料中心冷卻和電力基礎設施面臨的限制因素

- 替代 CUDA 的軟體生態系統碎片化阻礙了 GPU 在日本的廣泛應用。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按設備和應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

- 按記憶體類型

- 配備 GDDR 記憶體的 GPU

- 配備 HBM 記憶體的 GPU

- 按績效水準

- 低成本GPU(100美元以下)

- 主流GPU(100美元 - 400美元)

- 高效能消費級GPU(400美元至1200美元)

- 資料中心/AI加速器GPU(超過1200美元)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Huawei Technologies Co. Ltd.(HiSilicon)

- Biren Technology

- Moore Threads Intelligent Technology Co. Ltd.

- Jingjia Microelectronics Co. Ltd.

- Cambricon Technologies Corp. Ltd.

- Zhaoxin Semiconductor Corp. Ltd.

- Hygon Information Technology Co. Ltd.

- Innosilicon Technology Ltd.

- Tianshu Zhixin Semiconductor Co. Ltd.

- VeriSilicon Holdings Co. Ltd.

- Colorful Technology Co. Ltd.

- Galaxy Microsystems Ltd.

- Micro-Star International Co. Ltd.

- ASUSTeK Computer Inc.

- Lenovo Group Ltd.

- Inspur Electronic Information Industry Co. Ltd.

- Giga-Byte Technology Co. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the china discrete GPU market size is projected to expand from USD 27.49 billion in 2025 and USD 31.89 billion in 2026 to USD 78.98 billion by 2031, registering a CAGR of 19.89% between 2026 and 2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles, and More), Memory Type (GDDR-Based GPUs, and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

China Discrete GPU Market Trends and Insights

Surging Demand for AI Training and Inference Workloads in Chinese Hyperscale Datacenters

Hyperscale operators have moved GPU procurement to the top of capital-expenditure priorities. Alibaba Cloud spent USD 53 billion in fiscal 2025 and deployed more than 100,000 accelerators across domestic server halls. ByteDance earmarked USD 23 billion the same year to train its Doubao foundation model, an effort that required roughly 50,000 H100-class chips. Tencent doubled AI-related capex, rolling out new GPU clusters for its Hunyuan model. Baidu's Ernie 4.0 stack came online with about 20,000 discrete GPUs that delivered OpenAI-comparable performance. These deployments follow multi-year supply contracts that dampen demand cyclicality and encourage joint silicon-software co-design with local vendors to mitigate export-control risks.

Government Incentives for Domestic Semiconductor Self-Reliance and GPU Innovation

China's National Integrated Circuit Industry Investment Fund Phase III committed CNY 344 billion (USD 47 billion) in 2024, explicitly listing GPU development as a strategic domain. A State Council directive from the same year mandates that half of all government and state-owned enterprise IT procurement source domestic semiconductors by 2027, creating guaranteed demand for homegrown graphics processors.Shanghai offered CNY 2 billion (USD 280 million) in direct grants to GPU startups during 2025, a model replicated by Shenzhen and Wuhan municipalities. The Ministry of Industry and Information Technology sets an 80% semiconductor self-sufficiency goal by 2030, further aligning fiscal resources with road-map milestones. Talent incentives have attracted more than 3,500 engineers back from overseas positions, enlarging the domestic skills pool required for advanced GPU architecture.

U.S. Export Controls Limiting Access to Cutting-Edge GPU IP and HBM Memory

Revisions to United States export rules in January 2025 introduced performance ceilings that restrict bidirectional transfer rates and floating-point throughput for GPUs bound for China DOC.GOV. NVIDIA responded with H20, L20 and L2 variants that deliver about one-third less training throughput than the H100, yet still consumed 15% of 2025 datacenter revenue. AMD's MI308 navigated a protracted licensing process that delayed broad availability until the third quarter of 2025. Supply pressure intensified after the United States urged SK Hynix and Micron to scale back HBM3 exports, reducing allocations to Chinese buyers by roughly 40%. Domestic firms are experimenting with GDDR6X-based chiplet layouts as stop-gaps, but these alternatives incur higher power draw and cooling overhead.

Other drivers and restraints analyzed in the detailed report include:

- Continuous Growth of PC Gaming and Esports Ecosystem in China

- Rapid Adoption of Discrete GPUs in Automotive ADAS and Autonomous-Driving Platforms

- Fragmentation of CUDA-Alternative Software Ecosystems Hindering Domestic GPU Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators accounted for 39.17% of 2025 revenue in the China discrete GPU market, underscoring the structural shift away from purely consumer graphics boards. The segment benefits from multi-year capacity reservations by Alibaba Cloud, Tencent, ByteDance, and Baidu, each scaling fleets that now exceed a combined 300,000 AI accelerators. This procurement discipline stabilizes quarterly demand and supports vendors that can satisfy compliance rules while offering competitive price-performance ratios. Professional visualization and workstation cards trail datacenter silicon but still monetize creative workflows, capturing roughly 12% of the 2025 total as content studios embrace generative AI in video editing and architectural rendering.

The gaming PC and workstation category remains large by volume, yet its revenue share is slowing as average selling prices plateau. Gaming cafes and home enthusiasts continue to refresh rigs, helped by lower-tier domestic GPUs that deliver esports-class frame rates at sub-USD 400 price points. Automotive GPUs, though starting from a smaller base, are on a steep climb. Annual shipments are projected to top 2 million units by 2027 as Li Auto, NIO, and XPeng push centralized compute boxes into mainstream trims. Edge devices covering industrial vision and retail analytics form a nascent but promising slice, favored by data-localization policies that discourage cloud offloading and thus raise on-premises inference demand.

Complete Report Scope:

- By Device Application

- Mobile Devices and Tablets

- PCs and Workstations

- Servers and Datacenter Accelerators

- Gaming Consoles and Handhelds

- Automotive / ADAS

- Other Embedded and Edge Devices

- By Memory Type

- GDDR-Based GPUs

- HBM-Based GPUs

- By Performance Tier

- Low-Cost GPUs (less than 100 USD)

- Mainstream GPUs (100 USD to 400 USD)

- High-Performance Consumer GPUs (400 USD to 1,200 USD)

- Data Center / AI Accelerator GPUs (greater than 1,200 USD)

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Huawei Technologies Co. Ltd. (HiSilicon)

- Biren Technology

- Moore Threads Intelligent Technology Co. Ltd.

- Jingjia Microelectronics Co. Ltd.

- Cambricon Technologies Corp. Ltd.

- Zhaoxin Semiconductor Corp. Ltd.

- Hygon Information Technology Co. Ltd.

- Innosilicon Technology Ltd.

- Tianshu Zhixin Semiconductor Co. Ltd.

- VeriSilicon Holdings Co. Ltd.

- Colorful Technology Co. Ltd.

- Galaxy Microsystems Ltd.

- Micro-Star International Co. Ltd.

- ASUSTeK Computer Inc.

- Lenovo Group Ltd.

- Inspur Electronic Information Industry Co. Ltd.

- Giga-Byte Technology Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for AI Training and Inference Workloads in Chinese Hyperscale Datacenters

- 4.2.2 Continuous Growth of PC Gaming and Esports Ecosystem in China

- 4.2.3 Government Incentives for Domestic Semiconductor Self-Reliance and GPU Innovation

- 4.2.4 Rapid Adoption of Discrete GPUs in Automotive ADAS and Autonomous Driving Platforms

- 4.2.5 Rising Demand from Domestic Cloud-Based GPUaaS Providers Targeting SME AI Workloads

- 4.2.6 Expansion of Refurbished GPU Exports Creating Domestic Upgrade Cycle and Price Normalization

- 4.3 Market Restraints

- 4.3.1 U.S. Export Controls Limiting Access to Cutting-Edge GPU IP and HBM Memory

- 4.3.2 Global Semiconductor Supply-Chain Constraints Raising Bill-of-Materials Costs

- 4.3.3 Cooling and Power Infrastructure Limitations in Tier-2 Chinese Datacenters

- 4.3.4 Fragmentation of CUDA-Alternative Software Ecosystems Hindering Domestic GPU Adoption

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-Based GPUs

- 5.2.2 HBM-Based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (less than 100 USD)

- 5.3.2 Mainstream GPUs (100 USD to 400 USD)

- 5.3.3 High-Performance Consumer GPUs (400 USD to 1,200 USD)

- 5.3.4 Data Center / AI Accelerator GPUs (greater than 1,200 USD)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Huawei Technologies Co. Ltd. (HiSilicon)

- 6.4.5 Biren Technology

- 6.4.6 Moore Threads Intelligent Technology Co. Ltd.

- 6.4.7 Jingjia Microelectronics Co. Ltd.

- 6.4.8 Cambricon Technologies Corp. Ltd.

- 6.4.9 Zhaoxin Semiconductor Corp. Ltd.

- 6.4.10 Hygon Information Technology Co. Ltd.

- 6.4.11 Innosilicon Technology Ltd.

- 6.4.12 Tianshu Zhixin Semiconductor Co. Ltd.

- 6.4.13 VeriSilicon Holdings Co. Ltd.

- 6.4.14 Colorful Technology Co. Ltd.

- 6.4.15 Galaxy Microsystems Ltd.

- 6.4.16 Micro-Star International Co. Ltd.

- 6.4.17 ASUSTeK Computer Inc.

- 6.4.18 Lenovo Group Ltd.

- 6.4.19 Inspur Electronic Information Industry Co. Ltd.

- 6.4.20 Giga-Byte Technology Co. Ltd.

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment