|

市場調查報告書

商品編碼

2072453

馬來西亞太陽能:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Malaysia Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

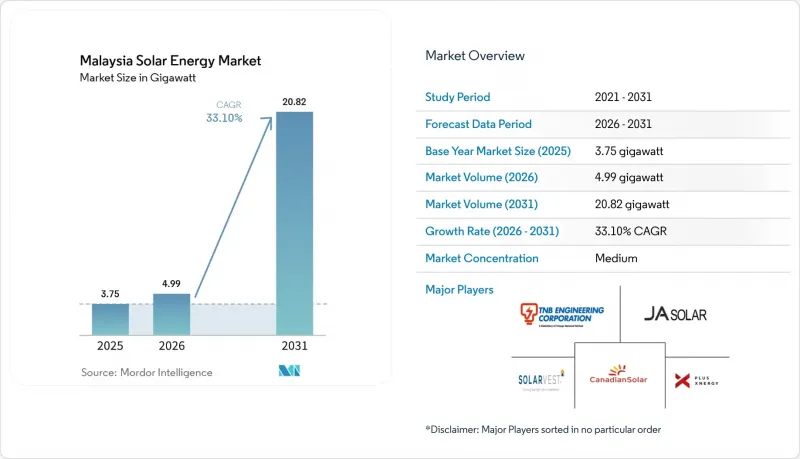

根據 Mordor Intelligence 預測,馬來西亞太陽能市場將從 2025 年的 3.75 吉瓦成長到 2026 年的 4.99 吉瓦,然後從 2026 年到 2031 年以 33.1% 的複合年成長率成長,到 2031 年達到 20.82 吉瓦。

本報告按技術(光伏和聚光型太陽光電)、併網類型(併網和離網)以及最終用戶(公用事業、商業/工業和住宅)進行細分。市場規模和預測以裝置容量(GW)為單位。

馬來西亞太陽能市場趨勢與洞察

政府主導的大型集散戶競標的擴大正在推動市場加速發展。

馬來西亞持續擴大其大型太陽能系統(LSS)計劃,提供透明的容量儲備和定價結構,從而增強專案的資金籌措潛力。 LSS5計劃於2024年以平均每千瓦時0.1699馬幣的價格鎖定了2吉瓦的裝機容量。 LSS PETRA 5+計畫的目標是在2025年再部署2吉瓦,在維持成本競爭力的同時,規範儲能需求。可預測的進度安排使開發商能夠儘早鎖定供電契約,降低物流風險,並滿足嚴格的併網里程碑要求。這項政策降低了監管的不確定性,展現了政府的長期承諾,吸引了國內外對馬來西亞太陽能市場的直接投資。

光學模組價格的下降正在加速專案的經濟可行性。

由於全球供應過剩,2024年組件價格下降了近20%,使得馬來西亞電力公司站點的平準化電成本(LCOE)低於每千瓦時0.20馬幣成為可能。組件價格的下降縮短了屋頂採用者的投資回收期,從而擴大了馬來西亞太陽能市場的基本客群。然而,美國對馬來西亞產品徵收的反傾銷稅降低了製造工廠的運轉率,帶來了採購時機風險,開發商需要透過供應商多元化來規避這些風險。儘管如此,硬體成本的下降抵消了價格波動的影響,使新計畫更具競爭力。

半島電網擁塞限制了電網連接能力。

輸電能力未能跟上太陽能發電的快速發展步伐。馬來西亞國家能源公司(Tenaga Nacional Belhad)計劃在2030年投入103億馬幣用於電網現代化改造,但其部署速度仍無法滿足短期併網需求。太陽能發電高峰期恰逢白天工業活動淡季,加劇了回流限制,導致電力輸出削減。開發商正擴大在負載中心附近安裝儲能設施和叢集以緩解瓶頸,但及時升級電網對於支援馬來西亞太陽能市場的發展和減輕系統整體負擔至關重要。

細分市場分析

到2025年,光伏發電將佔馬來西亞太陽能市場佔有率的100%,鞏固其作為唯一商業性部署技術的地位。馬來西亞每日每平方公尺4.5-5.5千瓦時(kWh/m²)的充足太陽輻射,使得光伏發電的產能利用率能夠將平準化電力成本(LCOE)控制在市電平價以下。預計到2031年,馬來西亞光伏市場將以33.1%的複合年成長率成長,這反映了其成熟的性能、強大的本地組裝網路和高效的授權流程。同時,由於直射太陽輻射量未達到經濟閾值,且高資本密集度抑制了投資興趣,聚光型太陽光電(CSP)計畫尚未進入規劃階段。

晶科能源和隆基的現場組件組裝縮短了運輸前置作業時間,並對沖了外匯波動風險,從而提高了開發商的成本確定性。位於Sejingkat的60兆瓦/80兆瓦時電池儲能專案展示了太陽能發電與儲能混合模式在頻率調節方面的有效性,進一步提升了該專案獲得銀行融資的合格。能源委員會的併網法規要求符合IEC標準並具備先進的逆變器功能,從而提高了質量,並確保太陽能發電裝置安全併入馬來西亞太陽能市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府擴大LSS競標範圍

- 降低太陽能發電組件的成本

- 企業購電協議 (PPA) 和 RE100 的需求增加

- 資料中心電力需求激增(柔佛和雪蘭莪)

- 引進虛擬淨計量政策

- 推廣利用水庫進行浮體式太陽能發電

- 市場限制因素

- 半島地區電網擁塞

- 中小企業屋頂太陽能發電工程資金籌措成本高。

- 土地利用與農業有衝突

- 光伏組件進口和供應的波動性

- 供應鏈分析

- 監理展望

- 技術展望

- 波特五力模型

- PESTLE分析

第5章 市場規模與成長預測

- 透過技術

- 太陽能發電(PV)

- 聚光型太陽熱能發電(CSP)

- 按網格類型

- 併網

- 離網

- 最終用戶

- 公用事業規模

- 商業和工業(C&I)

- 住宅

- 按成分(定性分析)

- 太陽能模組/面板

- 逆變器(組串式、集中式、微型)

- 安裝和追蹤系統

- 系統周邊設備和電氣設備

- 儲能和混合整合

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- First Solar Inc.

- Canadian Solar Inc.

- Plus Xnergy Holding Sdn Bhd

- TNB Engineering Corporation Sdn Bhd

- Solarvest Holdings Berhad

- JA Solar Technology Co. Ltd.

- SunPower Corporation

- Hasilwan(M)Sdn Bhd

- TS Solartech Sdn Bhd

- Ditrolic Energy

- Cypark Resources Berhad

- Samaiden Group Berhad

- Gading Kencana Sdn Bhd

- Engie Services Malaysia

- Huawei Technologies Malaysia Sdn Bhd

- JinkoSolar Holding Co Ltd.

- LONGi Green Energy Technology Co Ltd.

- Hanwha Q CELLS

- Sunview Group Berhad

- Risen Energy Co Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the malaysia solar energy market size is expected to grow from 3.75 gigawatt in 2025 to 4.99 gigawatt in 2026 and is forecast to reach 20.82 gigawatt by 2031 at 33.1% CAGR over 2026-2031.

This report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), and End-User (Utility-Scale, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Malaysia Solar Energy Market Trends and Insights

Government LSS Auction Expansions Drive Market Acceleration

Malaysia continues to enlarge the LSS program, providing transparent capacity pipelines and price discovery that underpin project bankability. LSS5 was awarded 2 GW in 2024 at an average tariff of RM0.1699 per kWh. LSS PETRA 5 + aims for another 2 GW in 2025, maintaining competitive pressure on cost while standardizing storage requirements. Predictable scheduling enables developers to secure supply contracts early, mitigate logistics risk, and meet stringent grid-code milestones. The policy lowers regulatory uncertainty and signals long-term commitment that attracts both domestic and foreign direct investment into the Malaysia solar energy market.

Declining PV Module Costs Accelerate Project Economics

A global supply glut led to a nearly 20% decline in module prices in 2024, enabling sub-RM 0.20 per kWh levelized costs at Malaysian utility sites. Cheaper panels shorten payback periods for rooftop adopters, thereby broadening the Malaysian solar energy market's customer base. However, U.S. anti-dumping duties on Malaysian exports disrupt manufacturing utilization, creating procurement timing risk that developers must hedge through diversified sourcing strategies. Lower hardware outlays nevertheless outweigh the volatility, reinforcing the competitiveness of new projects.

Grid Congestion in Peninsular Grid Constrains Integration Capacity

Transmission capacity has not kept pace with the rapid expansion of solar energy. Tenaga Nasional Berhad has earmarked RM 10.3 billion until 2030 for grid modernization, yet the roll-out lags behind near-term connection requests. Peak PV output coincides with mid-day industrial lulls, aggravating reverse-flow constraints that prompt curtailment. Developers increasingly add storage or clusters near load centers to mitigate bottlenecks, but systemic relief hinges on timely transmission upgrades that sustain the growth of the Malaysian solar energy market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Corporate PPA and RE100 Demand Transforms Procurement Patterns

- Data Center Power Demand Spike Creates Industrial Anchor Load

- High Financing Cost for Rooftop SME Projects Limits Market Penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar PV held 100.00% of Malaysia's solar energy market share in 2025, underscoring its entrenched position as the only commercially deployed technology. Robust irradiation of 4.5-5.5 kWh/ m2 /m2/day permits capacity factors that keep levelized costs below grid parity. The Malaysia solar energy market size for PV is projected to climb at a 33.1% CAGR through 2031, reflecting proven performance, abundant local assembly, and streamlined permitting. No concentrated solar power (CSP) ventures entered planning because direct normal irradiance falls short of economic thresholds, and higher capital intensity dampens appetite.

Local module assembly by JinkoSolar and LONGi reduces shipping lead times and hedges currency fluctuation, improving cost certainty for developers. Bankability gains further traction from the Sejingkat 60 MW / 80 MWh battery project, which validates hybrid PV-storage for frequency regulation. Energy Commission grid codes mandate IEC compliance and advanced inverter functionality, elevating quality while ensuring PV assets integrate safely into the Malaysia solar energy market.

Complete Report Scope:

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

List of Companies Covered in this Report:

- First Solar Inc.

- Canadian Solar Inc.

- Plus Xnergy Holding Sdn Bhd

- TNB Engineering Corporation Sdn Bhd

- Solarvest Holdings Berhad

- JA Solar Technology Co. Ltd.

- SunPower Corporation

- Hasilwan (M) Sdn Bhd

- TS Solartech Sdn Bhd

- Ditrolic Energy

- Cypark Resources Berhad

- Samaiden Group Berhad

- Gading Kencana Sdn Bhd

- Engie Services Malaysia

- Huawei Technologies Malaysia Sdn Bhd

- JinkoSolar Holding Co Ltd.

- LONGi Green Energy Technology Co Ltd.

- Hanwha Q CELLS

- Sunview Group Berhad

- Risen Energy Co Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government LSS auction expansions

- 4.2.2 Declining PV module costs

- 4.2.3 Rising corporate-PPA/RE100 demand

- 4.2.4 Data-centre power demand spike (Johor & Selangor)

- 4.2.5 Virtual NEM policy roll-out

- 4.2.6 Reservoir-based floating-solar push

- 4.3 Market Restraints

- 4.3.1 Grid congestion in Peninsular grid

- 4.3.2 High financing cost for rooftop SME projects

- 4.3.3 Land-use conflicts with agriculture

- 4.3.4 Import-supply volatility for PV modules

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 By Grid Type

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By End-User

- 5.3.1 Utility-Scale

- 5.3.2 Commercial and Industrial (C&I)

- 5.3.3 Residential

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Solar Modules/Panels

- 5.4.2 Inverters (String, Central, Micro)

- 5.4.3 Mounting and Tracking Systems

- 5.4.4 Balance-of-System and Electricals

- 5.4.5 Energy Storage and Hybrid Integration

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 First Solar Inc.

- 6.4.2 Canadian Solar Inc.

- 6.4.3 Plus Xnergy Holding Sdn Bhd

- 6.4.4 TNB Engineering Corporation Sdn Bhd

- 6.4.5 Solarvest Holdings Berhad

- 6.4.6 JA Solar Technology Co. Ltd.

- 6.4.7 SunPower Corporation

- 6.4.8 Hasilwan (M) Sdn Bhd

- 6.4.9 TS Solartech Sdn Bhd

- 6.4.10 Ditrolic Energy

- 6.4.11 Cypark Resources Berhad

- 6.4.12 Samaiden Group Berhad

- 6.4.13 Gading Kencana Sdn Bhd

- 6.4.14 Engie Services Malaysia

- 6.4.15 Huawei Technologies Malaysia Sdn Bhd

- 6.4.16 JinkoSolar Holding Co Ltd.

- 6.4.17 LONGi Green Energy Technology Co Ltd.

- 6.4.18 Hanwha Q CELLS

- 6.4.19 Sunview Group Berhad

- 6.4.20 Risen Energy Co Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

美國太陽能:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

美國太陽能:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 太陽能市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、太陽能組件、應用、最終用途、地區和競爭格局分類,2021-2031年

太陽能市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、太陽能組件、應用、最終用途、地區和競爭格局分類,2021-2031年 太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測

太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測 太陽能發電系統市場:2026-2032年全球市場預測(依產品、系統規模、安裝類型及應用分類)

太陽能發電系統市場:2026-2032年全球市場預測(依產品、系統規模、安裝類型及應用分類) 2026年全球太陽能市場報告

2026年全球太陽能市場報告 太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙太陽能:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南太陽能市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙太陽能:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)越南太陽能市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)