|

市場調查報告書

商品編碼

1940736

東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Southeast Asia Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

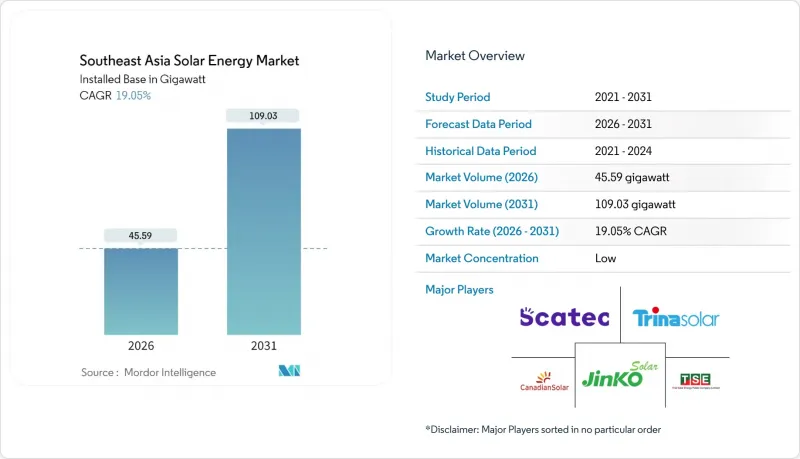

預計東南亞太陽能市場將從 2025 年的 38.29 吉瓦成長到 2026 年的 45.59 吉瓦,到 2031 年達到 109.03 吉瓦,2026 年至 2031 年的複合年成長率為 19.05%。

組件價格下降、碳中和力度加大以及零售電價與電網電價差距縮小,正推動越南、印尼、泰國、菲律賓、馬來西亞、新加坡和汶萊等國的投資熱潮。國家競標項目定價為每千瓦時0.04-0.05美元,正在取代新建燃煤發電廠,而企業可再生能源購電協議(PPA)則提前滿足了工商業(C&I)需求。儘管併網挑戰依然嚴峻,但將太陽能與儲能結合的混合型太陽能電站有助於降低棄電風險、創造新的輔助業務收益收入並提高計劃融資可行性。由於對中國組件徵收反傾銷稅以及高日照地區土地使用糾紛日益增多,供應鏈兩極化限制了短期利潤率,但也為浮體式太陽能和農光互補創造了新的機會。

東南亞太陽能市場趨勢與展望

加速實現國家可再生能源目標和碳中和承諾

修訂後的電力計畫提高了2024年的區域太陽能目標,其依據不再是氣候外交,而是能源安全的經濟效益。越南修訂後的第八版電力發展計畫(PDP VIII)提出,公用事業規模的發電裝置容量將達到30吉瓦。印尼將2030年的目標加倍,達到9.2吉瓦,泰國承諾到2030年將其再生能源比例提高到30%。液化天然氣進口成本的上漲(2024年平均價格為14-16美元/百萬英熱單位)推動太陽能成為成本最低的能源之一。菲律賓在其綠色能源競標項目中以有史以來最低的單價授予了3.5吉瓦的契約,這表明透明競標比上網電價補貼(FIT)更具資金籌措優勢。新加坡承諾2035年進口4吉瓦的可再生能源,促成了超過20億新元的跨境輸電投資。

單晶PERC和TOPCon光學模組成本快速下降

隨著多晶矽價格跌破每公斤6美元,到2024年,拓普康(TOPCon)組件的價格將降至每瓦0.12-0.15美元,進一步拉大其與傳統PERC組件的性能差距。其優異的溫度係數可使熱帶氣候下的年發電量提高4-6%,並將越南的平準化電力成本(LCOE)降低至每千瓦時0.038-0.042美元。即使計入環境監管成本,這項成本也遠低於新建燃煤發電廠。印尼145兆瓦的Sirata浮體式計劃採用雙面拓普康組件,由於水面反照率效應,發電量提高了12-15%。緬甸和柬埔寨正在興起二手PERC組件的次市場,降低了離網電氣化的進入門檻。

高光照區域的土地利用競爭

在越南寧順省和平順省,農業用地競爭激烈,導致年租金超過每公頃2,000美元,內部報酬率下降了1.2個百分點。泰國已將1.8萬公頃軍事用地排除在2024年太陽能發電計畫之外,以優先保障糧食安全。在印度尼西亞,面積超過10公頃的太陽能發電廠,其環境評估核准時間將延長約一年。水庫浮體式太陽能發電和農光互補系統(將農作物與太陽能結合)正在成為新興的解決方案,但它們的初始投資成本較高,約為18%至22%。

細分市場分析

2025年,東南亞太陽能市場將以太陽能裝置容量為主。聚光太陽熱能發電(CSP)在商業性不可行,因為直接太陽輻射量很少超過每平方公尺1500千瓦時。 TOPCon和異質接面技術將轉換效率提升至24-25%,使系統總成本降低每瓦0.08-0.12美元,預計2031年將維持19.12%的年複合成長率(CAGR)。東南亞太陽能市場受益於中國供應鏈的規模優勢。隆基、天合光能和晶科能源等公司將到岸成本控制在比全球平均低15-20%的水平,使越南公共產業計劃能夠以每千瓦時0.042-0.048美元的競標中標。儘管異質結組件的價格溢價高達 25-30%,但在新加坡和馬來西亞,異質結組件仍佔高階屋頂光伏需求的 8%,這表明在空間受限的地區,人們更願意為千瓦級密度支付更高的價格。

薄膜碲化鎘技術僅佔市場佔有率的2%,但其卓越的高溫效率已在菲律賓150兆瓦的卡拉塔甘(Calatagan )計劃中得到證實。鈣鈦礦-矽串聯電池已在新加坡太陽能研究院完成實驗室測試,並進入現場測試階段。如果濕度穩定性方面取得技術突破,該技術可望在2027年進入商業試點階段。在此之前,晶體矽預計將繼續主導東南亞太陽能市場,隨著傳統PERC技術的逐步淘汰,預計到2031年,高階雙面TOPCon電池的出貨量將佔總出貨量的70%以上。

東南亞太陽能市場報告按技術(太陽能和聚光型太陽熱能發電)、併網類型(併網和離網)、終端用戶(大型電站、商業/工業、住宅)和地區(越南、印尼、菲律賓、泰國、馬來西亞、新加坡和東南亞其他地區)進行細分。市場規模和預測以裝置容量(吉瓦)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加速實現國家可再生能源目標和碳中和承諾

- 單晶PERC和TOPCon光學模組成本快速下降

- 商業和工業用戶的市電平價屋頂太陽能

- 東協區域電力貿易試點計畫(寮國-泰國-馬來西亞-新加坡走廊)

- 綠氫能出口雄心推動了大型太陽能計劃的推進

- 市場限制

- 高光照區域的土地利用競爭

- 區域城市脆弱的電力分配基礎設施

- 越南和馬來西亞提高模組級進口關稅(有貿易救濟措施風險)

- 菲律賓和越南與颶風相關的資產風險溢價上升

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過技術

- 太陽能(光伏)

- 聚光太陽能發電(CSP)

- 按電網連接類型

- 併網

- 離網

- 最終用戶

- 實用規模

- 商業和工業(C&I)

- 住宅

- 按成分(定性分析)

- 太陽能模組/面板

- 逆變器(組串式、集中式、微型)

- 安裝和追蹤系統

- 系統周邊設備和電氣設備

- 儲能和混合整合

- 按地區

- 越南

- 印尼

- 菲律賓

- 泰國

- 馬來西亞

- 新加坡

- 其他東南亞國家

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、夥伴關係、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- Canadian Solar Inc.

- JinkoSolar Holding Co. Ltd.

- Trina Solar Co. Ltd.

- LONGi Green Energy Technology Co. Ltd.

- Vena Energy Pte Ltd.

- Scatec ASA

- Thai Solar Energy PCL

- Blue Solar Co. Ltd.

- Sunseap Group Pte Ltd.

- AC Energy Corp.

- Sembcorp Industries Ltd.

- Cleantech Solar Energy Pte Ltd.

- First Solar Inc.

- Hanwha Q CELLS GmbH

- TotalEnergies Renewables Asia

- ENGIE South-East Asia

- Neoen SA

- Adaro Power

- PT Platinum Energy

- Solarie Energy

第7章 市場機會與未來展望

The Southeast Asia Solar Energy Market is expected to grow from 38.29 gigawatt in 2025 to 45.59 gigawatt in 2026 and is forecast to reach 109.03 gigawatt by 2031 at 19.05% CAGR over 2026-2031.

Falling module prices, rising carbon-neutral pledges, and widening retail-grid parity are reinforcing investment momentum across Vietnam, Indonesia, Thailand, the Philippines, Malaysia, Singapore, and Brunei. National auction programs priced between USD 0.04 and 0.05 per kWh have displaced new coal builds, while corporate renewable power purchase agreements (PPAs) are pulling commercial and industrial (C&I) demand forward. Grid integration remains a significant challenge, yet hybrid solar-plus-storage plants are mitigating curtailment risk, unlocking new ancillary service revenues, and enhancing project bankability. Heightened supply-chain bifurcation, triggered by anti-dumping duties on Chinese modules, and rising land-use conflicts in high-irradiance provinces are tempering near-term margins but are also spawning opportunities in floating solar and agrivoltaics.

Southeast Asia Solar Energy Market Trends and Insights

Accelerated National Renewable-Energy Targets and Carbon-Neutral Pledges

Revised power plans elevated regional solar targets in 2024 and are now anchored in energy-security economics rather than climate diplomacy. Vietnam's updated PDP VIII calls for 30 GW of utility-scale capacity. Indonesia has doubled its 2030 goal to 9.2 GW, and Thailand has lifted its renewable electricity commitment to 30% by 2030. Higher import costs for liquefied natural gas, averaging USD 14-16 per MMBtu in 2024, pushed solar to the top of least-cost supply stacks. The Philippines awarded 3.5 GW of contracts at record-low tariffs under its Green Energy Auction Program, signalling that transparent auctions can outcompete feed-in tariffs in capital attraction. Singapore's pledge to import 4 GW of renewables by 2035 has mobilized more than SGD 2 billion of cross-border transmission investment.

Rapid Cost Decline of Mono-PERC and TOPCon PV Modules

TOPCon module prices fell to USD 0.12-0.15 per W in 2024 as polysilicon costs slipped below USD 6 per kg, widening the performance gap with legacy PERC. Superior temperature coefficients deliver 4-6% higher annual yields in tropical heat, driving Vietnamese levelized costs down to USD 0.038-0.042 per kWh, well below new coal plants once environmental compliance is priced in. Indonesia's 145 MW Cirata floating project used bifacial TOPCon panels to capture 12-15% extra generation from water-surface albedo. Secondary markets for retired PERC modules are emerging across Myanmar and Cambodia, lowering entry barriers for off-grid electrification.

Land-Availability Conflicts in High-Irradiance Zones

Competition for farmland is elevating lease prices above USD 2,000 per hectare annually in Vietnam's Ninh Thuan and Binh Thuan provinces, eroding internal rates of return by up to 1.2 percentage points. Thailand withdrew 18,000 hectares of military land from solar allocation in 2024 to prioritize food security. Indonesia's environmental checks add almost one year to permitting for arrays larger than 10 hectares. Floating solar on reservoirs and agrivoltaic crop-sharing schemes are emerging workarounds, albeit at 18-22% capital-cost premiums.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Parity Rooftop PV for Commercial and Industrial Users

- ASEAN Cross-Border Power-Trade Pilot

- Weak Distribution-Grid Infrastructure in Secondary Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Photovoltaic installations captured the entire Southeast Asia solar energy market in 2025, making concentrated solar power commercially unviable due to direct normal irradiance seldom exceeding 1,500 kWh per m2. TOPCon and heterojunction lines are pushing conversion efficiency to 24-25%, decreasing balance-of-system costs by USD 0.08-0.12 per W and sustaining a 19.12% CAGR forecast through 2031. The Southeast Asia solar energy market benefits from the scale of the Chinese supply chain: LONGi, Trina Solar, and JinkoSolar delivered landed costs 15-20% below global averages, enabling utility projects in Vietnam to clear auctions at USD 0.042-0.048 per kWh. Heterojunction modules carved out an 8% slice of premium rooftop demand in Singapore and Malaysia despite 25-30% price premiums, underscoring the willingness to pay for kW-density in space-constrained zones.

Thin-film cadmium-telluride technology gained only 2% share but posted better high-temperature yield in the Philippines' 150 MW Calatagan project. Perovskite-silicon tandem cells are transitioning from lab to field trials at Singapore's Solar Energy Research Institute and could enter commercial pilots by 2027, pending breakthroughs in humidity stability. Until then, crystalline silicon will continue to dominate the Southeast Asia solar energy market, with premium bifacial TOPCon projected to command more than 70% of shipments by 2031 as legacy PERC technologies retire.

The Southeast Asia Solar Energy Market Report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), End-User (Utility-Scale, Commercial and Industrial, and Residential), and Geography (Vietnam, Indonesia, Philippines, Thailand, Malaysia, Singapore, and Rest of Southeast Asia). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW)

List of Companies Covered in this Report:

- Canadian Solar Inc.

- JinkoSolar Holding Co. Ltd.

- Trina Solar Co. Ltd.

- LONGi Green Energy Technology Co. Ltd.

- Vena Energy Pte Ltd.

- Scatec ASA

- Thai Solar Energy PCL

- Blue Solar Co. Ltd.

- Sunseap Group Pte Ltd.

- AC Energy Corp.

- Sembcorp Industries Ltd.

- Cleantech Solar Energy Pte Ltd.

- First Solar Inc.

- Hanwha Q CELLS GmbH

- TotalEnergies Renewables Asia

- ENGIE South-East Asia

- Neoen SA

- Adaro Power

- PT Platinum Energy

- Solarie Energy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated national RE targets & carbon-neutral pledges

- 4.2.2 Rapid cost decline of mono-PERC and TOPCon PV modules

- 4.2.3 Grid-parity rooftop PV for C&I users

- 4.2.4 ASEAN cross-border power-trade pilot (Lao-Thai-Malaysian-Singapore corridor)

- 4.2.5 Green-hydrogen export ambitions driving utility-scale solar pipelines

- 4.3 Market Restraints

- 4.3.1 Land-availability conflicts in high-irradiance zones

- 4.3.2 Weak distribution-grid infrastructure in secondary cities

- 4.3.3 Rising module-level import tariffs in Vietnam & Malaysia (trade-remedy risk)

- 4.3.4 Heightened cyclone-related asset-risk premiums in Philippines & Vietnam

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 By Grid Type

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By End-User

- 5.3.1 Utility-Scale

- 5.3.2 Commercial and Industrial (C&I)

- 5.3.3 Residential

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Solar Modules/Panels

- 5.4.2 Inverters (String, Central, Micro)

- 5.4.3 Mounting and Tracking Systems

- 5.4.4 Balance-of-System and Electricals

- 5.4.5 Energy Storage and Hybrid Integration

- 5.5 By Geography

- 5.5.1 Vietnam

- 5.5.2 Indonesia

- 5.5.3 Philippines

- 5.5.4 Thailand

- 5.5.5 Malaysia

- 5.5.6 Singapore

- 5.5.7 Rest of South East Asia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Canadian Solar Inc.

- 6.4.2 JinkoSolar Holding Co. Ltd.

- 6.4.3 Trina Solar Co. Ltd.

- 6.4.4 LONGi Green Energy Technology Co. Ltd.

- 6.4.5 Vena Energy Pte Ltd.

- 6.4.6 Scatec ASA

- 6.4.7 Thai Solar Energy PCL

- 6.4.8 Blue Solar Co. Ltd.

- 6.4.9 Sunseap Group Pte Ltd.

- 6.4.10 AC Energy Corp.

- 6.4.11 Sembcorp Industries Ltd.

- 6.4.12 Cleantech Solar Energy Pte Ltd.

- 6.4.13 First Solar Inc.

- 6.4.14 Hanwha Q CELLS GmbH

- 6.4.15 TotalEnergies Renewables Asia

- 6.4.16 ENGIE South-East Asia

- 6.4.17 Neoen SA

- 6.4.18 Adaro Power

- 6.4.19 PT Platinum Energy

- 6.4.20 Solarie Energy

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

太陽能市場

太陽能市場 太陽能發電系統市場:2026-2032年全球市場預測(以交付方式、組件、系統類型、安裝方式、系統規模及最終用途分類)

太陽能發電系統市場:2026-2032年全球市場預測(以交付方式、組件、系統類型、安裝方式、系統規模及最終用途分類) 馬來西亞太陽能:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)美國太陽能:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

馬來西亞太陽能:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)美國太陽能:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 太陽能市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、太陽能組件、應用、最終用途、地區和競爭格局分類,2021-2031年

太陽能市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、太陽能組件、應用、最終用途、地區和競爭格局分類,2021-2031年 太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測

太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測 太陽能發電設備:全球市場、技術、終端用戶與競爭格局

太陽能發電設備:全球市場、技術、終端用戶與競爭格局 2026年全球太陽能市場報告

2026年全球太陽能市場報告 太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)