|

市場調查報告書

商品編碼

1939057

越南太陽能市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Vietnam Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

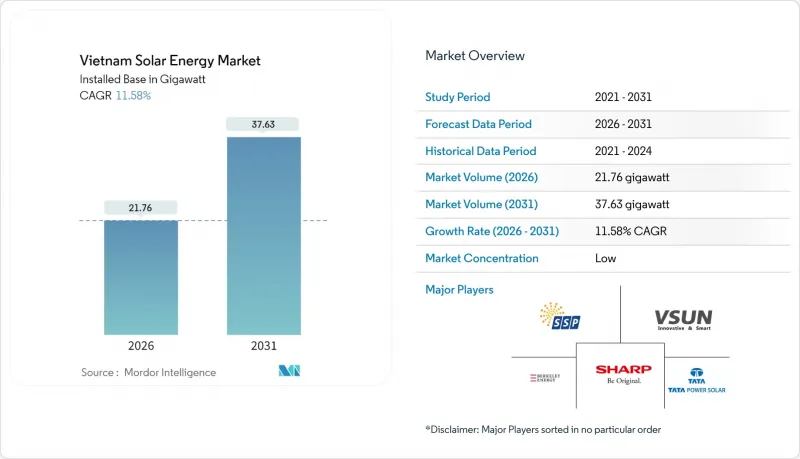

越南太陽能市場在 2025 年的價值為 19.5 吉瓦,預計到 2031 年將達到 37.63 吉瓦,高於 2026 年的 21.76 吉瓦。

預計在預測期(2026-2031 年)內,複合年成長率將達到 11.58%。

這一上升趨勢反映了2020年上網電價補貼(FIT)制度結束後推行的政策改革、第八個電力發展規劃(PDP8)的擴展以及組件成本的持續下降。浮體式太陽能的競標、直接購電協議(DPPA)的引入以及資料中心對全天候清潔能源的需求正在推動成長,而電網發展和上網電價補貼政策的不確定性則限制了近期的運作風險。 2020年至2024年,組件資本支出下降了36%,高輻照度地區大型電站的平準化度電成本(LCOE)已降至每千瓦時0.04美元以下。此外,優惠的氣候融資管道進一步鼓勵了私部門的投資。儘管南部地區電網堵塞,大型計劃實施也面臨瓶頸,但在太陽能與儲能混合利用的強制性政策以及企業購電協議(PPA)承諾的推動下,預計到2030年,該國的太陽能市場仍將保持兩位數的成長。

越南太陽能市場趨勢與展望

第八個電力發展計畫(PDP8)已將太陽能發電目標修訂為2030年達到34吉瓦。

2025年4月發布的第768號決議修訂了第八版電力發展計畫(PDP8),將2030年太陽能發電裝置容量上限提高至46.5-73.4吉瓦。這要求安裝永續兩小時的電池儲能設施。開發商目前正在安裝鋰離子電池系統,每千瓦時成本為200-250美元,這意味著一座100兆瓦的電站需要額外投資4000萬至5000萬美元,從而可以利用晚間高峰時段比白天高出30-40%的電價。雖然寧順省和平順省已簡化了超過儲能容量上限計劃的核准程序,但北部省份由於電網基礎設施薄弱而導致核准延誤。越南電力公司估計,需要150億美元的新電網投資才能滿足PDP8的能源需求,但指出平均每年的投資額僅12億美元,可能與該計畫的下限相符。然而,該政策鞏固了越南太陽能市場的長期前景,並為省級土地競標和私營部門資金籌措結構提供了指南。

企業購電協議及綠色貸款交易推動工商業需求

80/2024號法令允許每月用電量超過20萬千瓦時的消費者簽訂購電協議(DPPA)。短短六個月內,總計1.77吉瓦的24個計劃被列入等候核准。紡織、電子和食品加工企業為了對沖價格風險並獲得ESG認證,傾向於選擇虛擬購電協議,因為這種協議可以幫助它們避免每公里50萬至200萬美元的專用線路建設成本。世界銀行承諾在2024年投入5億美元用於可再生能源併網,亞洲開發銀行則在2023年至2024年間撥款17億美元用於屋頂太陽能和微電網建設。預計到2027年,谷歌和微軟等超大規模資料中心業者將簽署約300兆瓦的專用太陽能契約,以實現其全天候無碳運營的目標。雖然 20 萬千瓦時的閾值限制了中小企業的進入,但這項法規將加速越南太陽能市場的商業性轉型。

越南南部電網擁塞和發電量減少

寧順省和平順省的太陽能發電量已超過當地需求,導致500千伏幹線接近其熱負載極限運作,迫使越南電力集團(EVN)在2020年削減高達60%的過剩發電量。在旱季高峰期,平均削減率高達15%至25%,嚴重影響計劃盈利。一項計畫投資150億美元的高壓直流輸電擴建工程要到2027年才能全面運作,新增容量將面臨電網監管風險。目前,貸款機構要求購買削減保險,導致債務利差增加50至75個基點。雖然強制性10%的電池儲能有助於平衡電力供應,但無法抵消持續數天的電力過剩,這成為越南太陽能市場發展的一大限制因素。

細分市場分析

到2025年,太陽能系統將以19.5吉瓦的裝置容量佔據主導地位,並因資本投資持續下降,在2031年之前保持11.58%的複合年成長率。由於缺乏動態效率所需的直接太陽輻射,聚光型太陽熱能發電在越南仍不具備商業性可行性。寧順省的公用事業規模地面安裝系統採用單軸追蹤器,發電量提高了12%至18%,而都市區屋頂安裝則利用組件級電力電子設備來最大限度地減少陰影遮蔽造成的損失。水力發電廠的浮體式太陽能發電系統拓展了安裝地點的選擇範圍,並可利用現有電網。 TOPCon和異質結組件的快速普及(預計2024年將佔出貨量的35%)將有助於降低系統總成本。另一方面,聚光太陽能發電(CSP)資本密集度很高,成本在每千瓦3000美元至4000美元之間,而普通太陽能發電的成本僅為每千瓦550美元至650美元,而且聚光太陽能發電還會受到濕度造成的光學損耗,因此,到2031年之前,其前景黯淡。這鞏固了普通太陽能發電在越南太陽能市場的主導地位。

隨著開發人員部署雙面組件和直流耦合電池,並搭配混合逆變器,技術創新正在加速發展,往返效率可達92-94%。在50MW以上的電站中,串列型逆變器正在取代集中式逆變器,提高了系統的韌性,並支援容量的逐步擴展。儲能強制性要求正在改變採購模式:一套45MW/90MWh的儲能系統與一座450MW的太陽能電站相結合,透過尖峰時段的電價邊際收益克服了投資壁壘,為越南太陽能市場的混合化發展鋪平了道路。

越南太陽能市場報告按技術(太陽能和聚光型太陽熱能發電)、併網類型(併網和離網)以及最終用戶(大型公用事業公司、商業/工業用戶和住宅)進行細分。市場規模和預測以裝置容量(吉瓦)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 補貼上網電價(FIT)及屋頂淨計量

- 第八個電力發展計畫(PDP8)將太陽能發電目標擴大到2030年達到34吉瓦。

- 購電協議 (PPA) 和綠色貸款交易的增加將推動工商業需求。

- 一級光學模組資本支出下降(2020-2024年:-36%)

- 可再生運作採購,資料中心建設迅速成長。

- 地方政府土地權競標傾向在灌溉水庫中建造浮體式太陽能發電設施。

- 市場限制

- 越南南部電網擁塞和發電量減少

- 不明確的FIT減免與價格上限制度

- 自2026年起,國內一級EPC(工程、採購、施工)承包能力將出現短缺

- 投資者擔憂大型商業和工業系統屋頂結構的強度。

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 透過技術

- 太陽能發電(PV)

- 聚光型太陽熱能發電(CSP)

- 按網格類型

- 併網

- 離網

- 最終用戶

- 公用事業規模

- 商業和工業(C&I)

- 住宅

- 按成分(定性分析)

- 光學模組/面板

- 逆變器(組串式、集中式、微型)

- 安裝和追蹤系統

- 系統周邊設備和電氣設備

- 儲能和混合整合

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、夥伴關係、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- Song Giang Solar Power JSC

- Vietnam Sunergy JSC

- Sharp Energy Solutions Corp.

- Tata Power Solar Systems Ltd

- Shire Oak International Ltd

- B.Grimm Power PCL

- VU Phong Energy Group JSC

- Longi Green Energy Technology Co. Ltd

- Trina Solar Co. Ltd

- Berkeley Energy C&I Solutions

- Trung Nam Group

- BIM Group(AC Renewables)

- Bamboo Capital-CME Solar

- Xuan Cau Holdings

- T&T Group

- SkyX Solar

- First Solar Inc.

- JA Solar Technology Co. Ltd

- Canadian Solar Inc.

- Sunseap(EDP Renewables)

第7章 市場機會與未來展望

The Vietnam Solar Energy Market was valued at 19.5 gigawatt in 2025 and estimated to grow from 21.76 gigawatt in 2026 to reach 37.63 gigawatt by 2031, at a CAGR of 11.58% during the forecast period (2026-2031).

The upward curve reflects policy recalibration following the 2020 feed-in tariff (FIT) sunset, the expansion of Power Development Plan VIII (PDP8), and ongoing module-cost deflation. Competitive land auctions for floating arrays, the rollout of direct power-purchase agreements (DPPAs), and data-center procurement for 24X7 clean power underpin demand momentum, while transmission build-outs and FIT uncertainty temper near-term commissioning risk. Module capex fell 36% between 2020 and 2024, compressing utility-scale levelized costs below USD 0.04 per kWh in high-insolation provinces, and concessional climate-finance pipelines are amplifying the private sector's appetite. Despite grid congestion in the south and execution bottlenecks for large projects, hybrid solar-plus-storage mandates and corporate offtake commitments position the Vietnam solar energy market for double-digit growth through 2030.

Vietnam Solar Energy Market Trends and Insights

Power Development Plan VIII Upsizing Solar Target to 34 GW by 2030

Decision 768, issued in April 2025, reset the PDP8, raising the 2030 solar ceiling to 46.5-73.4 GW and mandating battery energy storage equal to at least 10% of the nameplate capacity with a 2-hour duration. Developers now finance lithium-ion arrays costing USD 200-250 per kWh, adding USD 40-50 million to a 100 MW plant, yet unlocking evening-peak tariffs 30-40% above midday rates. Ninh Thuan and Binh Thuan have streamlined permits for projects exceeding the storage threshold, whereas northern provinces lag due to weaker grid infrastructure. Electricity Vietnam estimates that USD 15 billion in new transmission is required to absorb PDP8 volumes, but the annual spend averages only USD 1.2 billion, implying that deployment will likely track the plan's lower bound. The policy nonetheless anchors long-term visibility for the Vietnam solar energy market, guiding provincial land auctions and private-sector financing structures.

Corporate PPAs & Green-Loan Pipelines Accelerating C&I Demand

Decree 80/2024 unlocked DPPAs for consumers topping 200,000 kWh per month, and within six months, 24 projects totaling 1.77 GW entered the approval queue. Textile, electronics, and food processors are chasing tariff hedges and ESG credentials, favoring virtual PPAs that avoid private-line build costs of USD 0.5-2 million per kilometer. The World Bank committed USD 500 million in 2024 for renewable integration, while the Asian Development Bank disbursed USD 1.7 billion during 2023-24 for rooftop solar and microgrids. Hyperscalers such as Google and Microsoft expect to contract close to 300 MW of dedicated solar by 2027 to meet 24X7 carbon-free goals. Although the 200,000 kWh threshold limits SME participation, the decree accelerates the commercial pivot within the Vietnam solar energy market.

Grid Congestion & Curtailment in Southern Vietnam

Solar output in Ninh Thuan and Binh Thuan already exceeds local demand, and the 500 kV backbone operates near thermal limits, forcing Electricity Vietnam to curtail up to 60% of excess generation in 2020. Curtailment averages 15-25% during dry-season peaks, undermining project returns. The planned HVDC reinforcement, worth USD 15 billion, will not be fully online until 2027, leaving new capacity exposed to dispatch risk. Lenders now insist on curtailment insurance, adding 50-75 basis-point spreads to debt. Mandatory 10% battery storage helps time-shift energy but cannot offset multi-day oversupply events, keeping this restraint a prominent drag on the Vietnam solar energy market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Data-Center Build-Outs with 24X7 Renewables Procurement

- Declining Capex of Tier-1 PV Modules (-36% 2020-24)

- Uncertain FIT Step-Down & Price-Cap Regime

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar photovoltaic systems controlled the entire 19.5 GW base in 2025, and continued capex declines support an 11.58% CAGR to 2031. Concentrated solar power remains commercially unviable in Vietnam because the country lacks the direct-normal irradiance required for thermodynamic efficiency. Utility-scale ground mounts in Ninh Thuan utilize single-axis trackers to achieve 12-18% yield gains, whereas urban rooftops rely on module-level power electronics to minimize shading losses. Floating PV on hydropower reservoirs broadens the siting palette and leverages existing transmission. The rapid uptake of TOPCon and heterojunction modules, already accounting for 35% of 2024 shipments, reduces balance-of-system costs. CSP's higher capital intensity of USD 3,000-4,000 per kW, compared to USD 550-650 for PV, together with humidity-driven optical losses, negates its prospects through 2031, cementing photovoltaic primacy in the Vietnam solar energy market.

Innovation accelerates as developers deploy bifacial modules and DC-coupled batteries via hybrid inverters that yield round-trip efficiencies of 92-94%. String-inverter architectures are replacing central units in plants exceeding 50 MW, enhancing fault tolerance and facilitating incremental capacity additions. Battery mandates reshape procurement: 45 MW/90 MWh stacks paired with 450 MW solar farms now clear investment hurdles under peak-tariff spreads, signaling a hybridized roadmap for Vietnam's solar energy market.

The Vietnam Solar Energy Market Report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), and End-User (Utility-Scale, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- Song Giang Solar Power JSC

- Vietnam Sunergy JSC

- Sharp Energy Solutions Corp.

- Tata Power Solar Systems Ltd

- Shire Oak International Ltd

- B.Grimm Power PCL

- VU Phong Energy Group JSC

- Longi Green Energy Technology Co. Ltd

- Trina Solar Co. Ltd

- Berkeley Energy C&I Solutions

- Trung Nam Group

- BIM Group (AC Renewables)

- Bamboo Capital - CME Solar

- Xuan Cau Holdings

- T&T Group

- SkyX Solar

- First Solar Inc.

- JA Solar Technology Co. Ltd

- Canadian Solar Inc.

- Sunseap (EDP Renewables)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidised feed-in-tariffs (FiTs) & rooftop net-metering schemes

- 4.2.2 Power Development Plan VIII (PDP8) upsizing solar target to 34 GW by 2030

- 4.2.3 Corporate PPAs & Green-loan pipelines accelerating C&I demand

- 4.2.4 Declining capex of Tier-1 PV modules (-36 % 2020-24)

- 4.2.5 Surge in data-centre build-outs with 24 X 7 renewables procurement

- 4.2.6 Provincial land-use auctions favouring floating PV on irrigation reservoirs

- 4.3 Market Restraints

- 4.3.1 Grid congestion & curtailment in Southern Vietnam

- 4.3.2 Uncertain FIT step-down & price-cap regime

- 4.3.3 Shortage of local tier-1 EPC capacity post-2026

- 4.3.4 Investor scepticism over roof structural integrity for large C&I systems

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 By Grid Type

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By End-User

- 5.3.1 Utility-Scale

- 5.3.2 Commercial and Industrial (C&I)

- 5.3.3 Residential

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Solar Modules/Panels

- 5.4.2 Inverters (String, Central, Micro)

- 5.4.3 Mounting and Tracking Systems

- 5.4.4 Balance-of-System and Electricals

- 5.4.5 Energy Storage and Hybrid Integration

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Song Giang Solar Power JSC

- 6.4.2 Vietnam Sunergy JSC

- 6.4.3 Sharp Energy Solutions Corp.

- 6.4.4 Tata Power Solar Systems Ltd

- 6.4.5 Shire Oak International Ltd

- 6.4.6 B.Grimm Power PCL

- 6.4.7 VU Phong Energy Group JSC

- 6.4.8 Longi Green Energy Technology Co. Ltd

- 6.4.9 Trina Solar Co. Ltd

- 6.4.10 Berkeley Energy C&I Solutions

- 6.4.11 Trung Nam Group

- 6.4.12 BIM Group (AC Renewables)

- 6.4.13 Bamboo Capital - CME Solar

- 6.4.14 Xuan Cau Holdings

- 6.4.15 T&T Group

- 6.4.16 SkyX Solar

- 6.4.17 First Solar Inc.

- 6.4.18 JA Solar Technology Co. Ltd

- 6.4.19 Canadian Solar Inc.

- 6.4.20 Sunseap (EDP Renewables)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

太陽能市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、太陽能組件、應用、最終用途、地區和競爭格局分類,2021-2031年

太陽能市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、太陽能組件、應用、最終用途、地區和競爭格局分類,2021-2031年 太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測

太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測 太陽能發電系統市場:2026-2032年全球市場預測(依產品、系統規模、安裝類型及應用分類)

太陽能發電系統市場:2026-2032年全球市場預測(依產品、系統規模、安裝類型及應用分類) 2026年全球太陽能市場報告

2026年全球太陽能市場報告 太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類

太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類 東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙太陽能:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)太陽能解決方案市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭格局分類,2021-2031年)日本太陽能市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙太陽能:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)太陽能解決方案市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭格局分類,2021-2031年)日本太陽能市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)