|

市場調查報告書

商品編碼

1937436

西班牙太陽能:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Spain Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

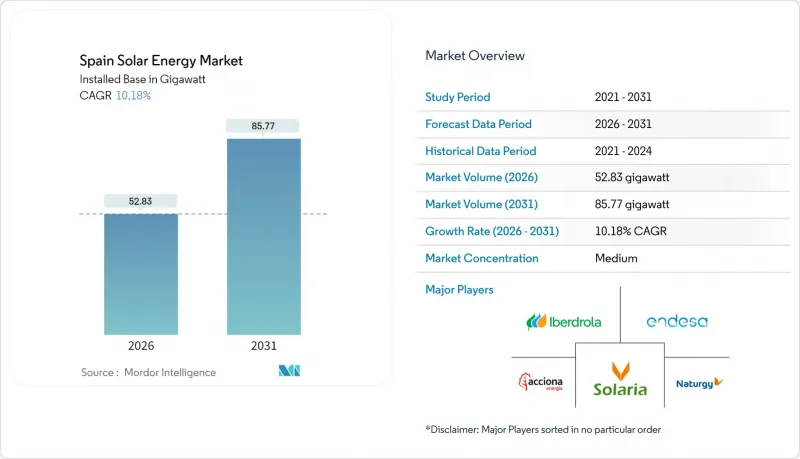

2025 年西班牙太陽能市場價值為 47.95 吉瓦,預計到 2031 年將達到 85.77 吉瓦,高於 2026 年的 52.83 吉瓦。

預計在預測期(2026-2031 年)內,複合年成長率將達到 10.18%。

西班牙太陽能發電裝置容量的快速擴張已使其佔全國發電量的21%,遠高於歐盟平均。這使西班牙有望實現修訂後的國家能源與氣候計畫中設定的76吉瓦太陽能目標。組件價格的下降、符合歐盟「Fit for 55」指令的更快捷的核准流程,以及企業對購電協議(PPA)的強勁需求,正在推動西班牙整體太陽能市場的成長。由於限電和價格競爭導致收入下降,混合式太陽能-儲能系統正在興起,尤其是在太陽能資源豐富的地區。儘管國際開發商正在加速發展,例如道達爾能源的塞維利亞叢集(263兆瓦)和Plenitude的Renopur計劃(330兆瓦),但電網堵塞和Natura 2000土地使用限制正在限制近期項目的部署。

西班牙太陽能市場趨勢與分析

大型光學模組成本下降

由於全球供應過剩,組件價格持續下降,使得卡斯蒂利亞-拉曼恰和埃斯特雷馬杜拉即使在土地品質較差的情況下也能實現具有競爭力的平準化能源成本 (LCOE)。雙面太陽能板與單軸追蹤器的組合,使得容量係數超過 25%,從而擴大了大型地面光電站的經濟潛力。道達爾能源等國際公用事業公司報告稱,與 2023 年相比,資本支出 (CAPEX) 可節省高達 15%。成本持平使得節省下來的資金可以重新用於周邊設備升級和能源管理軟體,從而促進與電池儲能的混合應用。當地工程公司報告稱,系統設計正顯著轉向 1500VDC,這可以減少電纜損耗和人工投入。因此,西班牙的太陽能市場正在不斷擴大,即使在傳統經濟低度開發地區也是如此。

歐盟「適合55歲人士」和「REPowerEU」合規期限

具有法律約束力的2030年脫碳目標為開發商提供了監管確定性,並加快了競標和資金籌措速度。西班牙核准2024年新增22,326兆瓦太陽能發電項目,並在2025年第一季新增3,019兆瓦。監管一致性也延伸至儲能領域,家用電池可獲得容量收益,並改善分散式資產的現金流量。地方政府也回應國家政策,安達盧西亞政府正加速推進2025年1.4吉瓦計劃的併網進程。明確的政策時間表最大限度地降低了市場價格風險,並鼓勵外國直接投資進入西班牙太陽能市場。

土地利用與 Natura 2000 保護區衝突

西班牙約30%的土地面積被劃為保護區,所有超過5公頃的計劃都必須進行全面的環境影響評估。光是穆爾西亞一地就計畫在2030年安裝3萬公頃的太陽能發電設施,其中60%位於曾經的耕地上,這些土地正面臨來自農業合作社的強烈反對。開發商擴大將目光投向廢棄礦場等棕地地,這使得每兆瓦的修復成本增加了5萬至10萬歐元。在衝突較少的土地上集中開發,使得本已受電網脆弱性限制的地區電力容量更加集中,從而加劇了限電風險。

細分市場分析

截至2025年,太陽能將佔西班牙太陽能市場的94.45%,到2031年將以10.45%的複合年成長率成長。同時,西班牙國家太陽能委員會(PNIEC)將聚光型太陽熱能發電發電(CSP)的目標裝置容量下調至4.8吉瓦。預計到2024年,鋰離子電池的成本將低於140美元/千瓦時,並且能夠以熔鹽系統一半的成本提供2-4小時的儲能,因此開發商正優先考慮太陽能-儲能混合系統。這將使西班牙太陽能市場在2025年至2030年間新增超過31吉瓦的裝置容量。

聚光型太陽熱能發電發電(CSP)仍能以每兆瓦時20-50歐元的價格提供工業製程熱,比價格波動較大的天然氣更經濟。西班牙目前擁有2.3吉瓦的運作電站。然而,2024年尚無新的公用事業規模聚光太陽能發電計劃完成融資。隨著公用事業公司將資金重新分配給採用n型電池的雙面太陽能發電(其發電量可提高10-15%),預計聚光太陽能發電的佔有率將進一步下降。

太陽能市場報告按技術(太陽能和聚光型太陽熱能發電)、併網類型(併網和離網)以及最終用戶(大型企業、商業/工業和住宅)進行細分。市場規模和預測以裝置容量(吉瓦)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 公用事業規模光學模組成本下降

- 歐盟「Fit for 55」和「REPowerEU」合規期限

- IBEX-35 指數成分股公司之間的公司間購電協議 (PPA) 數量迅速成長

- 利用併網電池混合動力系統提高計劃內部報酬率

- 乾旱地區(安達盧西亞、卡斯蒂利亞-拉曼查)農業太陽能(Agri-PV)激勵措施

- 自給自足型合作社(autoconsumo colectivo)的激增

- 人工智慧最佳化的發電規劃可提高商家的收入。

- 市場限制

- 土地利用與 Natura 2000 保護區衝突

- 在陽光照射強烈的地區,逆變器飽和可能導致輸出功率下降。

- 日前合約池中不穩定的蠶食折扣

- 雙軸追蹤器獲得地方政府批准所需時間較長。

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 透過技術

- 太陽能(光伏)

- 聚光型太陽熱能發電(CSP)

- 按網格類型

- 併網

- 離網

- 最終用戶

- 公用事業規模

- 商業和工業(C&I)

- 住宅

- 按成分(定性分析)

- 光學模組/面板

- 逆變器(組串式、集中式、微型)

- 安裝和追蹤系統

- 系統周邊設備和電氣設備

- 儲能和混合整合

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、聯盟、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- Iberdrola SA

- Acciona Energia

- Endesa(Enel Group)

- Solaria Energia y Medio Ambiente SA

- Repsol SA

- Engie Espana

- Naturgy Renovables

- Gransolar Group

- Soltec Power Holdings

- Cobra IS(ACS Group)

- RIC Energy

- Forestalia Renovables

- Prodiel

- Powertis(SPIC)

- Q-Energy

- X-Elio

- Opdenergy

- TotalEnergies Renewables Espana

- Sonnedix

- Fit Energy

第7章 市場機會與未來展望

The Spain Solar Energy Market was valued at 47.95 gigawatt in 2025 and estimated to grow from 52.83 gigawatt in 2026 to reach 85.77 gigawatt by 2031, at a CAGR of 10.18% during the forecast period (2026-2031).

Rapid capacity growth already lifts solar to 21% of national electricity generation, well ahead of the European Union average, and places the country on a clear trajectory to meet its 76 GW solar PV target under the revised National Energy and Climate Plan. Declining module prices, accelerated permitting aligned with EU Fit-for-55 mandates, and strong corporate PPA appetite underpin momentum across the Spain solar energy market. Hybrid solar-and-storage configurations, especially in high-irradiance provinces, are emerging as a hedge against curtailment and price cannibalization. International developers are deepening commitments, as illustrated by TotalEnergies' 263 MW Sevilla cluster and Plenitude's 330 MW Renopool project, while grid congestion and Natura-2000 land constraints temper short-term volumes.

Spain Solar Energy Market Trends and Insights

Declining cost of utility-scale PV modules

Module prices continue to fall due to global oversupply, allowing projects in Castilla-La Mancha and Extremadura to reach competitive levelized costs even on lower-grade land. Bifacial panels paired with single-axis trackers now achieve capacity factors above 25%, widening the economic envelope for large ground-mounted plants. International utilities such as TotalEnergies cite capex savings of up to 15% compared with 2023 figures. Cost parity encourages hybridization with battery storage because freed capital can be reallocated to balance-of-system upgrades and energy management software. Local engineering firms report a notable shift toward 1,500 VDC system designs that cut cable losses and labor inputs. The net effect is an enlarged Spain solar energy market pipeline in regions previously on the economic margin.

EU Fit-for-55 & REPowerEU Compliance Deadlines

Binding 2030 decarbonization targets give developers regulatory certainty, accelerating auction participation and bankability. Spain authorized 22,326 MW of PV construction in 2024 and cleared an additional 3,019 MW in Q1 2025. Regulatory alignment extends to storage: behind-the-meter batteries now qualify for capacity revenues, improving cash flows for distributed assets. Regional authorities echo the national stance; the Junta de Andalucia fast-tracked grid interconnection for 1.4 GW of projects in 2025. Clear policy timelines minimize merchant-price risk, drawing foreign direct investment into the Spain solar energy market.

Land-Use Conflicts with Natura-2000 Conservation Areas

Protected zones cover about 30% of Spain and trigger full environmental impact studies for any project footprint larger than 5 hectares. Murcia alone plans 30,000 ha of PV by 2030, yet 60% lies on former cropland that faces organized opposition from farm cooperatives. Developers increasingly target brownfield sites such as disused mines, adding EUR 50,000-100,000/MW in remediation costs. Concentration in low-conflict land funnels capacity into regions already constrained by weak transmission, thereby amplifying curtailment risk.

Other drivers and restraints analyzed in the detailed report include:

- Corporate PPA Boom Among IBEX-35 Firms

- Grid-Connected Battery Hybrids Enhancing Project IRR

- Curtailment Risk from Inverter Saturation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar photovoltaic commanded 94.45% of the Spain solar energy market in 2025 and is expanding at a 10.45% CAGR to 2031, whereas CSP's PNIEC target has fallen to 4.8 GW. Lithium-ion batteries cost below USD 140/kWh in 2024 and enable two-to-four-hour storage at half the cost of molten-salt systems, so developers prioritise PV-plus-battery hybrids. Spain's solar energy market size for photovoltaic additions will therefore increase by more than 31 GW between 2025 and 2030.

CSP still offers industrial process heat at EUR 20-50/MWh, cheaper than volatile natural gas prices, and Spain hosts 2.3 GW of operating plants. Yet no new utility-scale CSP projects reached financial close in 2024. As utilities redeploy capital into bifacial PV with n-type cells that lift yield by 10-15%, CSP's share will shrink further.

The Solar Energy Market Report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), and End-User (Utility-Scale, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- Iberdrola SA

- Acciona Energia

- Endesa (Enel Group)

- Solaria Energia y Medio Ambiente SA

- Repsol SA

- Engie Espana

- Naturgy Renovables

- Gransolar Group

- Soltec Power Holdings

- Cobra IS (ACS Group)

- RIC Energy

- Forestalia Renovables

- Prodiel

- Powertis (SPIC)

- Q-Energy

- X-Elio

- Opdenergy

- TotalEnergies Renewables Espana

- Sonnedix

- Fit Energy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining cost of utility-scale PV modules

- 4.2.2 EU Fit-for-55 & REPowerEU compliance deadlines

- 4.2.3 Corporate PPA boom among IBEX-35 firms

- 4.2.4 Grid-connected battery hybrids enhancing project IRR

- 4.2.5 Agri-PV incentives in drought-stricken regions (Andalucia, Castilla-La Mancha)

- 4.2.6 Surge in self-consumption cooperatives (autoconsumo colectivo)

- 4.2.7 AI-optimised dispatch lifting merchant revenue capture

- 4.3 Market Restraints

- 4.3.1 Land-use conflicts with Natura-2000 conservation areas

- 4.3.2 Curtailment risk from inverter saturation in high-irradiance provinces

- 4.3.3 Volatile cannibalisation discounts in day-ahead pool

- 4.3.4 Lengthy municipal permitting for 2-axis trackers

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 By Grid Type

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By End-User

- 5.3.1 Utility-Scale

- 5.3.2 Commercial and Industrial (C&I)

- 5.3.3 Residential

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Solar Modules/Panels

- 5.4.2 Inverters (String, Central, Micro)

- 5.4.3 Mounting and Tracking Systems

- 5.4.4 Balance-of-System and Electricals

- 5.4.5 Energy Storage and Hybrid Integration

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Iberdrola SA

- 6.4.2 Acciona Energia

- 6.4.3 Endesa (Enel Group)

- 6.4.4 Solaria Energia y Medio Ambiente SA

- 6.4.5 Repsol SA

- 6.4.6 Engie Espana

- 6.4.7 Naturgy Renovables

- 6.4.8 Gransolar Group

- 6.4.9 Soltec Power Holdings

- 6.4.10 Cobra IS (ACS Group)

- 6.4.11 RIC Energy

- 6.4.12 Forestalia Renovables

- 6.4.13 Prodiel

- 6.4.14 Powertis (SPIC)

- 6.4.15 Q-Energy

- 6.4.16 X-Elio

- 6.4.17 Opdenergy

- 6.4.18 TotalEnergies Renewables Espana

- 6.4.19 Sonnedix

- 6.4.20 Fit Energy

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

太陽能市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、太陽能組件、應用、最終用途、地區和競爭格局分類,2021-2031年

太陽能市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、太陽能組件、應用、最終用途、地區和競爭格局分類,2021-2031年 太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測

太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測 太陽能發電系統市場:2026-2032年全球市場預測(依產品、系統規模、安裝類型及應用分類)

太陽能發電系統市場:2026-2032年全球市場預測(依產品、系統規模、安裝類型及應用分類) 2026年全球太陽能市場報告

2026年全球太陽能市場報告 太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類

太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類 東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南太陽能市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)太陽能解決方案市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭格局分類,2021-2031年)日本太陽能市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南太陽能市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)太陽能解決方案市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭格局分類,2021-2031年)日本太陽能市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)