|

市場調查報告書

商品編碼

1938987

泰國太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Thailand Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

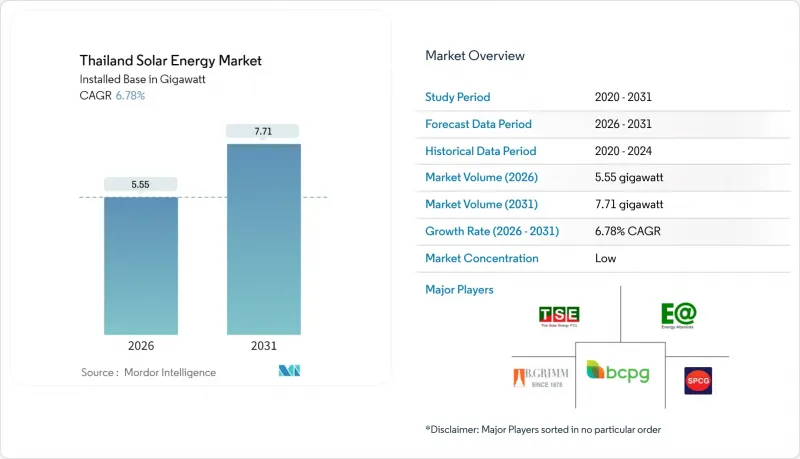

預計泰國太陽能發電市場將從 2025 年的 5.20 吉瓦成長到 2026 年的 5.55 吉瓦,到 2031 年達到 7.71 吉瓦,2026 年至 2031 年的複合年成長率為 6.78%。

儘管電網基礎設施存在瓶頸,但持續的價格壓力、可再生能源政策目標以及不斷下降的太陽能發電成本預計將推動泰國太陽能市場穩步成長。一項於2024年核准的2000兆瓦直接購電試點項目,為資料中心和大型製造商開闢了新的採購途徑,並縮短了獨立發電商(IPP)的銷售週期。組件價格在2024年降至每瓦0.10至0.12美元,將商業投資回收期縮短至5至7年,並提高了所有客戶群體的融資可行性。計畫在九個水庫上建造的浮體式太陽能混合計劃將新增2.7吉瓦的裝置容量,同時避免了地面安裝工程面臨的土地徵用障礙。太陽能租賃模式和1兆瓦以下系統的簡化許可程序,正在推動曼谷及其周邊省份住宅安裝的蓬勃發展,預示著光纖接入的普及程度正在不斷提高。

泰國太陽能市場趨勢與洞察

零售電價上漲與電價波動

儘管2024年零售電價維持在每千瓦時4.15-4.18泰銖不變,但泰國發電局(EGA)報告累計虧損約980億泰銖,並表示到2025年底電價可能上漲8-12%。東部經濟走廊的製造商正轉向屋頂光電發電,以對沖天然氣價格波動風險,典型的1兆瓦安裝工程可在不到7年的時間內回收成本。根據能源政策與規劃辦公室的數據,燃氣發電廠仍為泰國電網提供約60%的電力,其電價與液化天然氣現貨進口價格掛鉤。面臨歐盟碳邊境調節課稅的商業買家正在加速採購光伏發電系統,以確保其出口利潤。這種不斷成長的需求正在推動泰國太陽能市場的新發展勢頭,無論是自裝系統還是第三方資金籌措系統。

雙面和拓普康太陽能組件成本快速下降

2024年,雙面組件的平均價格降至每瓦0.10-0.12美元,拓普康電池的效率達24-25%,但成本略有上升。開發商透過談判達成多年供應協議,將組件價格鎖定至2027年,以穩定平準化能源成本。較低的資本密集度使得小規模屋頂光電系統即使在淨計費模式下也能在五年內收回成本。中國工廠的產能過剩導致產品流向東南亞,進一步壓低了當地價格。 2024年,美國對泰國組裝的光伏組件徵收反傾銷稅,重塑了出口路線,但國內產能過剩為當地計劃提供了廣泛的價格優惠。

併網核准時間過長以及輸出限制的風險

開發商表示,取得併網許可需要6到18個月的時間,因為電力公司必須進行電壓穩定性研究和變電站容量評估。超過10兆瓦的計劃還需要進行環境影響評估並獲得國家能源政策委員會的核准,這將延長施工前期並增加擁有成本。 2024年,太陽能滲透率超過日間需求18%的配電線路經歷了長達50小時的限電。如果沒有即時定價和強制儲能,過剩發電量可能導致強制停電,從而侵蝕計劃收益。這些障礙使預期成長率下降了近一個百分點。

細分市場分析

預計到2025年,太陽能光電系統將佔泰國裝置容量的100%,並在2031年之前以每年6.72%的速度成長。泰國太陽能市場規模(光電技術)預計2025年達到5.20吉瓦,到2031年達到7.71吉瓦。由於聚光型太陽熱能發電在泰國潮濕的氣候條件下經濟效益不佳,預計光伏發電將繼續佔據較大的市場佔有率。雙面組件能夠捕捉反射輻射,正迅速成為浮體式太陽能光電專案競標的標準配置。烏汶叻差那加計畫(Ubon Ratana 計劃)的發電量比單面組件陣列高出5-8%。效率高達24-25%的拓普康(TOPCon)電池在土地資源有限、價格溢價合理的大型競標中,正逐漸取代PERC組件。

成本的持續下降正在擴大光伏發電和聚光型太陽熱能發電之間的經濟差距,後者需要充足的直射太陽輻射,而季風季節很難達到這種水平。能源部2024年的上網電價補貼計畫將聚光太陽能熱發電排除在外,實際上鎖定了太陽能產業的壟斷地位。國際能源總署(IEA)的數據預測,到2027年,光電模組價格將進一步下降15-20%,這將使光電發電成為泰國唯一具有商業性可行性的太陽能技術。

泰國太陽能市場報告按技術(光伏和聚光型太陽熱能發電)、併網類型(併網和離網)以及最終用戶(大型發電、商業/工業和住宅)進行細分。市場規模和預測以裝置容量(吉瓦)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 零售電價上漲與電價波動

- 雙面和拓普康太陽能組件成本快速下降

- 直接購電協議試點計畫為工商業需求打開了大門

- 政府推廣2.7吉瓦浮體式太陽能混合發電項目

- 透過農地和太陽能發電相結合的計畫來降低土地徵用風險

- 出口導向企業對綠色可再生能源證書(REC)的需求不斷成長

- 市場限制

- 冗長的併網核准程序和發電量削減的風險

- 曼谷和東部經濟走廊的輸電線路飽和

- 美國和歐盟市場對泰國製造的模組提高進口關稅

- 國內儲能系統用鋰離子電池生產的限制

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 透過技術

- 光伏(PV)

- 聚光型太陽熱能發電(CSP)

- 按網格類型

- 併網

- 離網

- 最終用戶

- 公用事業規模

- 商業和工業(C&I)

- 住宅

- 按成分(定性分析)

- 光學模組/面板

- 逆變器(組串式、集中式、微型)

- 安裝和追蹤系統

- 系統周邊設備和電氣設備

- 儲能和混合整合

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、夥伴關係、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- SPCG PLC

- BCPG PLC

- Thai Solar Energy PLC

- B.Grimm Power PLC

- Energy Absolute PLC

- Solartron PLC

- Delta Electronics(Thailand)PLC

- Huawei Technologies Co. Ltd.

- Sungrow Power Supply Co. Ltd.

- JinkoSolar Holding Co. Ltd.

- Trina Solar Co. Ltd.

- LONGi Green Energy Co. Ltd.

- Canadian Solar Inc.

- First Solar Inc.

- Risen Energy Co. Ltd.

- Seraphim Solar Group

- Sharp Energy Solutions Corp.

- Hitachi Energy Thailand

- Black & Veatch Holding Co.

- Marubeni Corp.

第7章 市場機會與未來展望

The Thailand Solar Energy Market is expected to grow from 5.20 gigawatt in 2025 to 5.55 gigawatt in 2026 and is forecast to reach 7.71 gigawatt by 2031 at 6.78% CAGR over 2026-2031.

Continued tariff pressure, renewable energy policy targets, and declining photovoltaic costs position the Thai solar energy market for steady growth, despite grid infrastructure bottlenecks. A 2,000 MW direct power purchase pilot, approved in 2024, is opening an alternative procurement pathway for data centers and large manufacturers, which shortens sales cycles for independent power producers. Module prices that fell to USD 0.10-0.12 per watt in 2024 trimmed commercial payback periods to five to seven years, enhancing bankability across all customer classes. Floating-solar hybrid projects planned for nine hydroelectric reservoirs will add 2.7 GW of incremental capacity, circumventing land-acquisition hurdles that limit the use of ground-mounted sites. Solar leasing models and simplified licensing for systems below 1 MW are driving a residential installation boom in Bangkok and peri-urban provinces, signaling broader democratization of solar access.

Thailand Solar Energy Market Trends and Insights

Rising Retail-Grid Tariffs and Electricity-Price Volatility

Retail tariffs remained at THB 4.15-4.18 per kWh in 2024; however, the Electricity Generating Authority of Thailand reported cumulative losses of nearly THB 98 billion, suggesting an 8-12% tariff hike by late 2025 is likely. Manufacturers in the Eastern Economic Corridor now view rooftop solar as a hedge against gas price swings, as a typical 1 MW installation pays for itself within seven years. Data from the Energy Policy and Planning Office show that gas-fired units still supply about 60% of the grid's electricity, linking tariffs to spot LNG imports. Commercial buyers facing European Union carbon-border fees have accelerated solar procurement to protect export margins. The resulting demand is giving the Thai solar energy market fresh momentum across both on-site and third-party financed systems.

Rapid Cost Decline of Bifacial and TOPCon PV Modules

Average bifacial module prices declined to USD 0.10-0.12 per watt in 2024, while TOPCon cells achieved 24-25% efficiencies at only marginally higher costs. Developers now negotiate multi-year supply contracts, locking in component prices to 2027 and stabilizing levelized energy costs. Lower capital intensity has enabled smaller rooftops to achieve five-year paybacks even under net-billing. Oversupply in Chinese factories diverted products to Southeast Asia, further pushing down local prices. Although United States antidumping tariffs on Thai-assembled panels reshuffled export channels in 2024, domestic oversupply created broader price relief for local projects.

Long-Cycle Grid-Connection Approvals and Curtailment Risks

Developers report approval times of six to eighteen months because utilities must conduct voltage-stability studies and substation-capacity reviews before granting interconnection. Projects larger than 10 MW also require environmental impact assessments and National Energy Policy Council sign-offs, which extend pre-construction periods and increase holding costs. In 2024, curtailment events totaled up to fifty hours in feeders where solar penetration exceeded 18% of daytime demand. Absent real-time pricing or mandatory storage, over-generation causes forced shutdowns that undermine project revenue. These obstacles shave nearly one percentage point off forecast growth.

Other drivers and restraints analyzed in the detailed report include:

- Direct PPA Pilot Opening Commercial and Industrial Demand

- Government Push for 2.7 GW Floating-Solar Hybrids

- Saturated Feeders in Bangkok and Eastern Economic Corridor

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Photovoltaic systems accounted for 100.00% of the installed capacity in 2025 and are expected to expand at a 6.72% growth rate through 2031. The Thailand solar energy market size for photovoltaic technology reached 5.20 GW in 2025 and is expected to reach 7.71 GW by 2031, maintaining a significant share, as concentrated solar power remains economically impractical under Thailand's humid climate. Bifacial modules that capture reflected irradiance are quickly becoming standard in floating-solar tenders, with the Ubolratana project registering 5-8% higher output than monofacial arrays. TOPCon cells, which offer 24-25% conversion efficiency, are overtaking PERC modules in utility-scale bids where land constraints justify premium pricing.

Continuous cost declines widen the economic gap between photovoltaic and concentrated solar power, which needs direct-normal-irradiance levels rarely achieved in the monsoon season. The Ministry of Energy's 2024 feed-in-tariff schedule excludes concentrated solar power, effectively cementing photovoltaics' monopoly. Looking forward, International Energy Agency data project module prices dropping another 15-20% by 2027, ensuring photovoltaic technologies remain the only commercially viable solar option in Thailand.

The Thailand Solar Energy Market Report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), and End-User (Utility-Scale, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- SPCG PLC

- BCPG PLC

- Thai Solar Energy PLC

- B.Grimm Power PLC

- Energy Absolute PLC

- Solartron PLC

- Delta Electronics (Thailand) PLC

- Huawei Technologies Co. Ltd.

- Sungrow Power Supply Co. Ltd.

- JinkoSolar Holding Co. Ltd.

- Trina Solar Co. Ltd.

- LONGi Green Energy Co. Ltd.

- Canadian Solar Inc.

- First Solar Inc.

- Risen Energy Co. Ltd.

- Seraphim Solar Group

- Sharp Energy Solutions Corp.

- Hitachi Energy Thailand

- Black & Veatch Holding Co.

- Marubeni Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising retail-grid tariffs & electricity-price volatility

- 4.2.2 Rapid cost decline of bifacial & TOPCon PV modules

- 4.2.3 Direct-PPA pilot opening C&I demand flood-gates

- 4.2.4 Government push for 2.7 GW floating-solar hybrids

- 4.2.5 Agro-PV programs easing land-acquisition risks

- 4.2.6 Growing demand for green RECs from export-oriented firms

- 4.3 Market Restraints

- 4.3.1 Long-cycle grid-connection approvals & curtailment risks

- 4.3.2 Saturated feeders in Bangkok & Eastern Economic Corridor

- 4.3.3 Rising import tariffs on Thai modules in US/EU markets

- 4.3.4 Limited domestic Li-ion cell production for BESS

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 By Grid Type

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By End-User

- 5.3.1 Utility-Scale

- 5.3.2 Commercial and Industrial (C&I)

- 5.3.3 Residential

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Solar Modules/Panels

- 5.4.2 Inverters (String, Central, Micro)

- 5.4.3 Mounting and Tracking Systems

- 5.4.4 Balance-of-System and Electricals

- 5.4.5 Energy Storage and Hybrid Integration

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 SPCG PLC

- 6.4.2 BCPG PLC

- 6.4.3 Thai Solar Energy PLC

- 6.4.4 B.Grimm Power PLC

- 6.4.5 Energy Absolute PLC

- 6.4.6 Solartron PLC

- 6.4.7 Delta Electronics (Thailand) PLC

- 6.4.8 Huawei Technologies Co. Ltd.

- 6.4.9 Sungrow Power Supply Co. Ltd.

- 6.4.10 JinkoSolar Holding Co. Ltd.

- 6.4.11 Trina Solar Co. Ltd.

- 6.4.12 LONGi Green Energy Co. Ltd.

- 6.4.13 Canadian Solar Inc.

- 6.4.14 First Solar Inc.

- 6.4.15 Risen Energy Co. Ltd.

- 6.4.16 Seraphim Solar Group

- 6.4.17 Sharp Energy Solutions Corp.

- 6.4.18 Hitachi Energy Thailand

- 6.4.19 Black & Veatch Holding Co.

- 6.4.20 Marubeni Corp.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

太陽能市場

太陽能市場 太陽能發電系統市場:2026-2032年全球市場預測(以交付方式、組件、系統類型、安裝方式、系統規模及最終用途分類)

太陽能發電系統市場:2026-2032年全球市場預測(以交付方式、組件、系統類型、安裝方式、系統規模及最終用途分類) 馬來西亞太陽能:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)美國太陽能:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

馬來西亞太陽能:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)美國太陽能:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 太陽能市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、太陽能組件、應用、最終用途、地區和競爭格局分類,2021-2031年

太陽能市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、太陽能組件、應用、最終用途、地區和競爭格局分類,2021-2031年 太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測

太陽能市場規模、佔有率和成長分析:按產品/組件、技術、安裝類型、併網類型、最終用途、電源和地區分類-2026-2033年產業預測 太陽能發電設備:全球市場、技術、終端用戶與競爭格局

太陽能發電設備:全球市場、技術、終端用戶與競爭格局 2026年全球太陽能市場報告

2026年全球太陽能市場報告 太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

太陽能發電系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、安裝類型、最終用戶、功能及設備分類東南亞太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)