|

市場調查報告書

商品編碼

2066473

LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)LED Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

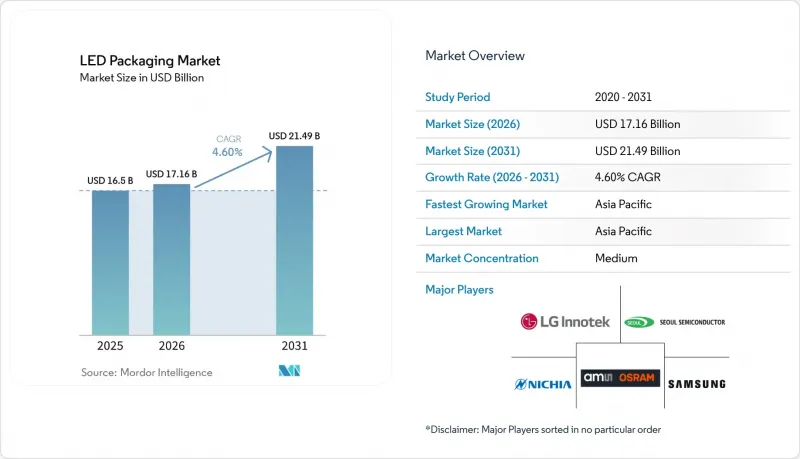

根據 Mordor Intelligence 預測, LED構裝市場規模將從 2025 年的 165 億美元和 2026 年的 171.6 億美元成長到 2031 年的 214.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.60%。

本報告按封裝架構(板載晶片、玻璃封裝等)、功率等級(中功率(0.5–1 W)、高功率(1–3 W 等))、發光類型(可見光LED構裝、紅外線LED構裝等)、材料化學(基板、封裝等)、應用(通用照明等)和地區進行細分。市場預測以美元計價。

全球LED構裝市場趨勢與洞察

IT產品中Mini-LED背光技術的應用正在快速成長。

在輕薄筆記型電腦、高色彩顯示器和高對比度平板電腦需求不斷成長的推動下,mini-LED背光技術已迅速成為主流生產技術。儘管平均售價較低,但由於直下式面板每塊所需的晶片數量是傳統側光系統的5到10倍,因此總消耗量仍在增加。 CSP封裝具有亞毫米級間距、低Z軸高度和精確波長分檔等特點,如今已成為高階顯示器品牌的標準配備。透過實現千兆像素級光學檢測自動化並交付預分檔陣列來最大化價值的封裝製造商蓬勃發展,而依賴手動貼片平台的傳統SMD供應商則難以與之競爭。

汽車產業正在加速向自我調整矩陣式LED頭燈過渡。

汽車原始設備製造商 (OEM) 正優先採用矩陣式和像素式照明技術,以提高駕駛者的視野,同時避免眩光。奧迪的 25,600 像素頭燈原型標誌著車輛中發光元件數量的顯著增加,這推動了對高功率CSP 和覆晶封裝的需求,這些封裝能夠承受 -40 度C至 +150 度C的溫度循環,並符合 AEC-Q102 標準。雖然在歐洲,由於 123 號法規的實施,這些技術的應用速度最快,並為當地供應商帶來了早期收益,但美國仍在等待國家公路交通安全管理局 (NHTSA) 對眩光容忍度的最終決定。擁有汽車級品管系統的供應商正在確保設計方案被採納,並獲得多年生產合約。

圍繞覆晶設計的曠日持久的專利訴訟的成本。

億光半導體、日亞化學工業株式會社、首爾半導體和Lumileds等公司持續提起跨國專利侵權訴訟,平均每起案件的訴訟成本高達500萬美元。關於利潤損失和合理許可費的賠償爭議加劇了不確定性,迫使規模較小的參與企業必須預留累計而非投資研發。現有公司之間的交叉授權構成了一道壁壘,阻礙了新進入者的步伐,並延緩了現有專利組合的商業化。

細分市場分析

到2025年,表面黏著型元件將佔據LED構裝市場43.45%的佔有率,這一主導地位建立在數十年來自動化組裝基礎設施發展的基礎之上。晶片級封裝(CSP)方案無需導線架和封裝材料,厚度可減少至0.5毫米以下,同時提高了光提取效率。受mini-LED背光和穿戴式裝置對超薄模組的需求推動,CSP的銷售額正以5.11%的複合年成長率成長。汽車和工業領域的買家仍在使用板載晶片(COB)和覆晶封裝,以確保更優異的散熱性能,但訴訟成本阻礙了快速轉型。整合式模組裝置透過整合驅動IC和發光陣列降低了組件成本,因此受到優先考慮簡化供應鏈的照明設備OEM廠商的青睞。

SMD供應商憑藉高速貼片加工能力和廣泛的插座相容性維持市場佔有率。然而,由於中國產能過剩導致的價格下降正在擠壓利潤空間,加速了高可靠性細分市場的轉型。在這些市場中,CSP和覆晶封裝在批量生產方面兼具性能和成本優勢。傳統的通孔和雙列直插式封裝正逐漸從戶外顯示器和專業維修應用中消失。

受通用照明維修需求的推動,中功率(0.5–1 W)封裝預計到2025年將佔LED構裝市場規模的37.67%。高功率(1–3 W)裝置正以4.98%的複合年成長率成長,這反映了自適應矩陣式頭燈和工廠機器視覺照明燈具等應用對獨立發光元件和高速開關的需求,這些應用的亮度均超過100流明。功率超過3 W的超高高功率裝置正在滲透到體育場館、園藝和工業車間,但隨著結到外殼的熱目標低於2 度C/W,材料正轉向銅基板、類鑽石界面層,甚至微通道冷卻器。

功耗為0.5瓦的指示器正日益商品化,導致價格大幅下降。汽車產業對指示器有著嚴格的要求,例如AEC-Q102認證和承受3000次熱循環的能力,這與消費品產業截然不同。這種差異要求製造商改進和最佳化其生產流程,以滿足不同功率等級的特定需求。因此,這種做法導致資金被分配到不同的可靠性標準上,以確保符合各個市場的多樣化要求。

區域分析

到2025年,亞太地區將佔據68.55%的LED構裝市場佔有率,這主要得益於中國廣東和江蘇兩省垂直整合的叢集,這些集群實現了外延生長和最終模組組裝在同一地點完成。京東方華燦投資超過20億元人民幣(約2.8億美元),千兆光電投資2.1557億元人民幣(約2.8億美元),展現了規模經濟效應,降低了晶片成本,同時也加劇了區域內的競爭。日本正專注於高效率紫外線LED封裝與汽車封裝,利用日亞化學工業株式會社的280奈米生產線,並透過亞琛汽車研發中心與歐洲OEM廠商建立合作關係。韓國三星電子和LG Innotek正在投資6,000億韓元(約4.5億美元)建造覆晶球柵陣列(BGA)生產線,目標市場為高階顯示器和汽車模組。在東南亞,隨著企業分散地域風險,投資 8,388 萬美元的馬來西亞澳陽順泉工廠已開始營運。

在北美,監管主導的維修和專業應用備受關注。加拿大將於2026年1月禁用汞燈,全國正迅速向LED燈過渡;同時,美國也已最終確定了自我調整遠光燈的相關法規。國內封裝業者正專注於汽車、UV-C紫外線消毒和工業可靠性等細分市場。歐洲嚴格的生態設計法規以及自我調整頭燈的早期獲批,推動了對高功率、汽車認證封裝產品的強勁需求。德國作為汽車零件的採購中心發揮著至關重要的作用,當地的一級照明製造商與日本和韓國的晶片供應商合作開發模組。

儘管南美洲、中東和非洲的市場總合規模不大,但需求會根據具體情況而激增。在巴西,建設業的復甦帶動了通用照明產品的銷售成長;而在石油資源豐富的海灣國家,大型企劃正在採用高流明照明組件。在南非,礦區和工業區強制要求使用防護等級為IP65的耐候型組件;在埃及,電力供應有限的農村地區則更傾向於使用低功率太陽能路燈。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- IT產品中Mini-LED背光技術的應用正在快速成長。

- 汽車產業正在加速向自我調整矩陣式LED頭燈過渡。

- 政府禁止使用含汞照明產品

- 中國先進CSP生產線晶圓廠產能快速擴張

- 設備內建光學生物識別感測器正在推動對紅外線LED的需求。

- 新興的園藝固體UV-B照明系統

- 市場限制因素

- 由於覆晶設計領域專利叢林造成的持續訴訟成本。

- 高顯色指數紅色磷光體供應短缺

- 功率超過 3 瓦的高功率應用面臨溫度控管的挑戰。

- 低功耗SMD封裝產能過剩導致價格下降

- 產業價值鏈分析

- 技術分析

- 監理情勢

- 宏觀經濟因素的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按包裝類型

- 表面黏著型元件(SMD)

- 板載晶片(COB)

- 晶片級封裝(CSP)

- 覆晶LED構裝

- 雙列直插封裝(DIP/通孔)

- 整合模組裝置(IMD)

- 機上眼鏡(GOB)

- Mini-LED顯示器封裝

- 按電力等級

- 低功耗(小於0.5瓦)

- 中功率(0.5–1 瓦)

- 高功率(1-3瓦)

- 高功率(3瓦或以上)

- 按排放類型

- 可見光LED構裝

- 紅外線LED構裝

- 紫外線LED構裝

- 材料化學

- 基材

- 封裝

- 黏接/晶片貼裝

- 磷光體/塗層

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 家用電子產品

- 工業和專業應用

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 東南亞

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Samsung Electronics Co. Ltd.

- Seoul Semiconductor Co. Ltd.

- CreeLED Inc.

- Ams-Osram AG

- Lumileds Holding BV

- Everlight Electronics Co. Ltd.

- LG Innotek Co. Ltd.

- NationStar Optoelectronics Co. Ltd.

- Lextar Electronics Corp.

- Epistar Corporation

- Dominant Opto Technologies Sdn Bhd

- Toyoda Gosei Co. Ltd.

- Lite-On Technology Corporation

- Hongli Zhihui Group Co. Ltd.

- MLS Co. Ltd.

- Refond Optoelectronics Co. Ltd.

- Bridgelux Inc.

- San'an Optoelectronics Co. Ltd.

- Everlight Americas Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the lED packaging market size is projected to expand from USD 16.50 billion in 2025 and USD 17.16 billion in 2026 to USD 21.49 billion by 2031, registering a CAGR of 4.60% between 2026 and 2031.

This report is Segmented by Packaging Architecture (Chip-On-Board, Glass-On-Board, and More), Power Class (Mid Power (0. 5 - 1 W), High Power (1 - 3 W), and More), Emission Type (Visible LED Packages, Infrared LED Packages, and More), Material Chemistry (Substrates, Encapsulation, and More), Application (General Lighting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global LED Packaging Market Trends and Insights

Surging Adoption of Mini-LED Backlights in IT Products

Demand for thinner laptops, vivid monitors, and high-contrast tablets has vaulted mini-LED backlighting into mainstream production. Each direct-lit panel requires five to ten times as many dies as its edge-lit predecessors, increasing total unit consumption even as average selling prices decline. CSP packages offer sub-millimeter pitch, low z-height, and tight wavelength binning, which premium display brands now specify as baseline. Packaging houses that automate optical inspection at gigapixel throughput and ship pre-binned arrays capture the most value, while legacy SMD suppliers reliant on manual pick-and-place platforms struggle to compete.

Accelerated Automotive Shift to Adaptive Matrix LED Headlamps

Automotive original equipment manufacturers (OEMs) have prioritized matrix and pixel lighting to improve driver visibility without glare. Audi's 25,600-pixel headlamp prototype exemplifies the jump in on-board emitter count, pushing high-power CSP and flip-chip packages that withstand -40 °C to +150 °C cycles and meet AEC-Q102. Europe advances fastest under Regulation 123, giving regional suppliers early revenue, while the United States awaits final glare thresholds from the National Highway Traffic Safety Administration. Suppliers with automotive-grade quality systems win design-ins and lock multi-year production contracts.

Persistent Patent-Thicket Litigation Costs for Flip-Chip Designs

Everlight, Nichia, Seoul Semiconductor, and Lumileds continue to file cross-border infringement suits, averaging USD 5 million in legal spend per case. Damages debates over lost profits versus reasonable royalties elevate uncertainty and force smaller entrants to allocate reserves rather than fund research and development. Cross-licensing among incumbents creates barriers that slow new entrants and extend monetization for established portfolios.

Other drivers and restraints analyzed in the detailed report include:

- Government Bans on Mercury-Based Lighting Products

- Rapid Fab Capacity Build-Out in China for Advanced CSP Lines

- Supply Tightness of High-CRI Red Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount device formats commanded 43.45% of the LED packaging market share in 2025, a lead built on decades of automated assembly infrastructure. CSP alternatives eliminate lead frames and mold compounds, shrinking profiles below 0.5 mm and boosting optical extraction. CSP sales climb on a 5.11% CAGR, pushed by mini-LED backlighting and wearable devices that demand thin modules. Automotive and industrial buyers retain chip-on-board and flip-chip arrangements for superior thermal paths, yet litigation costs temper rapid migration. Integrated-module devices combine driver integrated circuits with the emitter array, reducing the bill of materials and appealing to luminaire OEMs that favor supply-chain simplification.

SMD suppliers defend their share through high-speed pick-and-place throughput and pervasive socket compatibility. Nonetheless, price erosion from surplus Chinese capacity compresses margins, accelerating the shift toward high-reliability niches where CSP and flip-chip packages provide both performance and cost headroom at volume. Legacy through-hole and dual-in-line formats fade in outside indicator and specialty retrofits.

Mid-power 0.5-1 W packages captured 37.67% of the LED packaging market size in 2025, buoyed by general lighting retrofits. High-power 1-3 W devices expand at a 4.98% CAGR, reflecting adaptive matrix headlamps and factory machine-vision luminaires that each need individual emitters exceeding 100 lumens with rapid switching. Ultra-high-power units above 3 W penetrate stadium, horticulture, and industrial bays but carry junction-to-case thermal targets under 2 °C/W, steering materials toward copper substrates, diamond-like interface layers, or even microchannel coolers.

Indicators with a power consumption of 0.5 W are increasingly subject to commoditization and substantial price reductions. The automotive sector, characterized by its stringent requirements such as AEC-Q102 certification and the ability to withstand 3,000 thermal cycles, distinctly separates itself from consumer-grade product lines. This differentiation necessitates that manufacturers refine and optimize their production processes to cater to the specific demands of each power category. Consequently, this approach results in the allocation of capital to distinct reliability standards, ensuring compliance with the varying requirements of these markets.

Geography Analysis

Asia-Pacific retained 68.55% of the LED packaging market share in 2025, led by China's vertically integrated clusters in Guangdong and Jiangsu, which collocate epitaxy with final module assembly. Investments topping RMB 2 billion (USD 280 million) at BOE Huacan and RMB 215.57 million (USD 30 million) at Qianzhao Optoelectronics illustrate scale economies that lower per-die costs while intensifying regional price competition. Japan focuses on high-efficiency UV and automotive packages, leveraging Nichia's 280 nm line and its alliance with European OEMs through the Aachen Automotive Innovation Center. South Korea's Samsung Electronics and LG Innotek channel 600 billion won (USD 450 million) into flip-chip ball-grid-array lines that target premium displays and vehicle modules. Southeast Asia welcomes Malaysia's USD 83.88 million Aoyang Shunchang plant as firms diversify geographic risk.

North America emphasizes regulatory-driven retrofits and specialty applications. The January 2026 Canadian mercury lamp ban compels rapid LED conversions countrywide, while the United States finalizes adaptive driving beam regulations. Domestic packaging houses focus on automotive, UV-C sterilization, and industrial reliability niches. Europe's stringent Ecodesign rules and early adaptive headlamp approvals are driving steady demand for high-power, automotive-qualified packages. Germany anchors automotive sourcing, with local Tier-1 lighting firms co-developing modules with Japanese and Korean die suppliers.

South America, the Middle East, and Africa collectively represent modest shares but deliver situational spikes. Brazil's construction rebound lifts general lighting unit sales, while oil-rich Gulf states deploy high-lumen packages in mega-projects. South Africa mandates ruggedized IP65 modules for mining and industrial zones, while Egypt prefers low-power solar streetlights for grid-constrained rural districts.

- Nichia Corporation

- Samsung Electronics Co. Ltd.

- Seoul Semiconductor Co. Ltd.

- CreeLED Inc.

- Ams-Osram AG

- Lumileds Holding B.V.

- Everlight Electronics Co. Ltd.

- LG Innotek Co. Ltd.

- NationStar Optoelectronics Co. Ltd.

- Lextar Electronics Corp.

- Epistar Corporation

- Dominant Opto Technologies Sdn Bhd

- Toyoda Gosei Co. Ltd.

- Lite-On Technology Corporation

- Hongli Zhihui Group Co. Ltd.

- MLS Co. Ltd.

- Refond Optoelectronics Co. Ltd.

- Bridgelux Inc.

- San'an Optoelectronics Co. Ltd.

- Everlight Americas Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Mini-LED Backlights in IT Products

- 4.2.2 Accelerated Automotive Shift to Adaptive Matrix LED Headlamps

- 4.2.3 Government Bans on Mercury-Based Lighting Products

- 4.2.4 Rapid Fab Capacity Build-Out in China for Advanced CSP Lines

- 4.2.5 On-Device Opto-Biometric Sensors Driving IR LED Demand

- 4.2.6 Emerging Horticulture Solid-State UV-B Illumination Systems

- 4.3 Market Restraints

- 4.3.1 Persistent Patent-Thicket Litigation Costs for Flip-Chip Designs

- 4.3.2 Supply Tightness of High-CRI Red Phosphors

- 4.3.3 Thermal-Management Challenges Above 3 W Ultra-High-Power Class

- 4.3.4 Price Erosion from Over-Capacity in Low-Power SMD Packaging

- 4.4 Industry Value-Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Architecture

- 5.1.1 Surface Mount Device (SMD)

- 5.1.2 Chip-on-Board (COB)

- 5.1.3 Chip Scale Package (CSP)

- 5.1.4 Flip-Chip LED Packages

- 5.1.5 Dual In-Line Package (DIP / Through-Hole)

- 5.1.6 Integrated Module Device (IMD)

- 5.1.7 Glass-on-Board (GOB)

- 5.1.8 Mini-LED Display Packaging

- 5.2 By Power Class

- 5.2.1 Low Power (Below 0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (1-3 W)

- 5.2.4 Ultra-High Power (Above 3 W)

- 5.3 By Emission Type

- 5.3.1 Visible LED Packages

- 5.3.2 Infrared LED Packages

- 5.3.3 Ultraviolet LED Packages

- 5.4 By Material Chemistry

- 5.4.1 Substrates

- 5.4.2 Encapsulation

- 5.4.3 Bonding / Die-Attach

- 5.4.4 Phosphors / Coatings

- 5.5 By Application

- 5.5.1 General Lighting

- 5.5.2 Automotive Lighting

- 5.5.3 Display and Backlighting

- 5.5.4 Consumer Electronics

- 5.5.5 Industrial and Specialty

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Southeast Asia

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co. Ltd.

- 6.4.3 Seoul Semiconductor Co. Ltd.

- 6.4.4 CreeLED Inc.

- 6.4.5 Ams-Osram AG

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 Everlight Electronics Co. Ltd.

- 6.4.8 LG Innotek Co. Ltd.

- 6.4.9 NationStar Optoelectronics Co. Ltd.

- 6.4.10 Lextar Electronics Corp.

- 6.4.11 Epistar Corporation

- 6.4.12 Dominant Opto Technologies Sdn Bhd

- 6.4.13 Toyoda Gosei Co. Ltd.

- 6.4.14 Lite-On Technology Corporation

- 6.4.15 Hongli Zhihui Group Co. Ltd.

- 6.4.16 MLS Co. Ltd.

- 6.4.17 Refond Optoelectronics Co. Ltd.

- 6.4.18 Bridgelux Inc.

- 6.4.19 San'an Optoelectronics Co. Ltd.

- 6.4.20 Everlight Americas Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

LED構裝市場規模、佔有率和趨勢分析報告:按材料、封裝類型、應用、地區和細分市場分類(2026-2033年)

LED構裝市場規模、佔有率和趨勢分析報告:按材料、封裝類型、應用、地區和細分市場分類(2026-2033年) LED構裝設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中國LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

LED構裝設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中國LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 晶片級封裝LED市場:依LED類型、應用和最終用途分類-2026-2032年全球市場預測LED構裝市場:依封裝類型、基板材料、晶片類型和應用分類-全球預測,2026-2032年LED導線架市場按產品、材質、電鍍類型、導線架類型和最終用戶分類 - 全球預測 2026-2032

晶片級封裝LED市場:依LED類型、應用和最終用途分類-2026-2032年全球市場預測LED構裝市場:依封裝類型、基板材料、晶片類型和應用分類-全球預測,2026-2032年LED導線架市場按產品、材質、電鍍類型、導線架類型和最終用戶分類 - 全球預測 2026-2032 LED構裝市場規模、佔有率及成長分析(按應用、技術、最終用途及地區分類)-2026-2033年產業預測

LED構裝市場規模、佔有率及成長分析(按應用、技術、最終用途及地區分類)-2026-2033年產業預測