|

市場調查報告書

商品編碼

2063944

中國LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)China LED Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

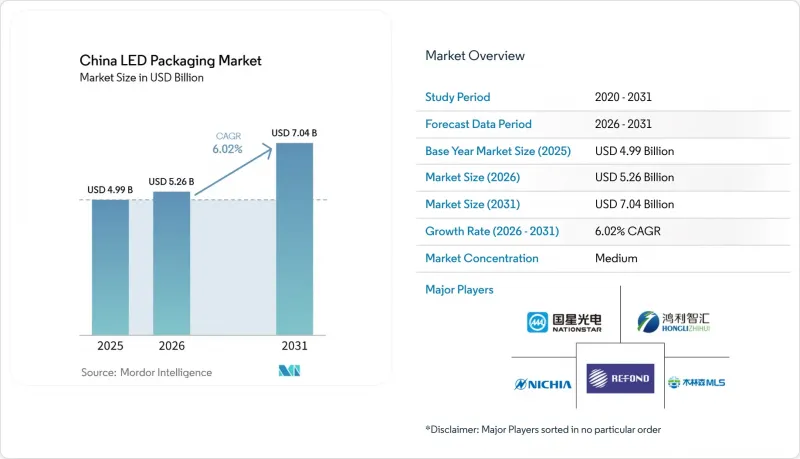

根據 Mordor Intelligence 預測,中國LED構裝市場規模預計到 2025 年將達到 49.9 億美元,到 2026 年將達到 52.6 億美元,到 2031 年將達到 70.4 億美元,2026 年至 2031 年的複合年成長率為 6.02%。

本報告按封裝架構(板載晶片(COB) 及其他)、功率等級(中功率(0.5–1W)、高功率(1–3W) 及其他)、發光類型(可見光LED構裝、紅外線 (IR) LED構裝及其他)、材料化學(封裝材料及其他)、應用領域進行通用照明、汽車照明及其他)和地區進行通用照明、汽車照明及其他)和地區進行通用照明、汽車照明。市場預測以美元 (USD) 為單位。

中國LED構裝市場趨勢與洞察

政府主導的智慧城市LED維修

市政採購專案正以整合調光、感測器和遠距離診斷功能的連網LED照明燈具取代傳統路燈。天津濱海新區於2024年完成的7.9萬套維修項目,充分展現了中高功率板載晶片(COB)模組的卓越性能,使其能耗降低了40%。競標文件中對GB 7000.1-2024安全標準和國內採購比例的要求日益嚴格,導致能夠證明其產品與國家物聯網標準互通性的中國封裝製造商獲得合約。隨著智慧路燈控制器收集遙測數據,擁有強大分析平台的供應商可以獲得持續的業務收益。這種以結果為基本契約,進一步鞏固了那些擁有內部驅動電子元件和現場故障診斷能力的垂直整合型參與企業的優勢。

加速採用迷你/微型LED背光

預計到2025年,中國mini-LED電視的出貨量將超過800萬台,到2026年,隨著100吋面板零售價降至1萬元人民幣(約1,385美元)以下,出貨量可望突破1,000萬台。海信116吋RGB mini-LED電視等旗艦機型透過將單面板晶片數量增加三倍,實現了97%的BT.2020色域覆蓋率和10000尼特的峰值亮度,顯著提升了對晶片級封裝(CSP)的需求。小於微米的嚴格封裝公差和超過99.9%的良率目標提高了市場進入門檻,並促使京東方、華星光電以及國內封裝廠商之間建立長期供應合作關係。韓國和日本的競爭對手目前面臨著規格相當的產品50%的價格競爭差距,迫使他們加快RGB微型LED藍圖。

中功率產品產能過剩導致價格下降

2026年3月,主要封裝廠商宣布的價格上漲幅度在3%至25%之間,但這一漲幅在浙江省迅速受阻。該地區低價位生產線的缺陷率仍維持在15%左右,設備運轉率低於85%的損益平衡點。儘管2024年整個產業的銷售額成長了8.9%,但利潤成長僅限於專注於汽車和mini-LED領域的公司,凸顯了大宗商品價格的脆弱性。 2025年上半年,MLS和NationStar的銷售額出現下滑,而利基參與企業Refond和Jufei則實現了兩位數的成長,證實了中功率產品存在結構性供應過剩。在透過工廠關閉或需求成長解決供應過剩問題之前,利潤率壓力將持續存在,從而阻礙對SMD生產線的新投資。

細分市場分析

隨著電視製造商從白色背光轉向對晶片密度和貼裝精度要求更高的RGB mini-LED光源,晶片級封裝預計到2031年將以6.78%的複合年成長率成長。即使到了2025年,表面黏著型元件(SMD)仍佔據中國LED構裝市場42.78%的佔有率。這得歸功於數十年的自動化技術將缺陷率降低到2%以下,以及1萬片起訂的單價降至0.10美元以下。

雖然量產的 2835、3030 和 5050 尺寸封裝仍然是住宅照明的必需品,但無需焊線的覆晶裝置正逐漸成為需要卓越散熱性能的大電流汽車模組的主流選擇。天門正在建造中的玻璃基板量產線目標是實現 99.995% 的轉移良率,預計達到這一水準將有助於實現低成本的微型 LED 穿戴式裝置和汽車顯示器。

2025年,額定功率為0.5-1W的中功率LED佔總銷量的35.49%。然而,由於持續的供應過剩,這些LED的毛利率僅為個位數。同時,額定功率為1-3W的高功率LED的複合年成長率(CAGR)為6.94%。這項快速成長主要得益於自我調整遠光燈和工業高棚照明燈具的應用,這兩種應用均能減少照明燈具的數量並減輕維修工作。

功率輸出為0.5W或以下的指示燈級發光元件在穿戴式裝置和標示市場中佔據主導地位。然而,這些領域極低的利潤率極大地限制了再投資和進一步發展的機會。同時,在高階市場,功率超過3W的銅基板發光元件主要應用於園藝植物生長照明和體育場泛光燈。在這些應用中,為了獲得更高的流明密度和更長的L70壽命,廠商願意支付30%至50%的溢價。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府主導的智慧城市LED照明維修

- 加速採用迷你/微型LED背光

- 汽車LED在新能源汽車中的廣泛應用

- 出口型電子製造服務商對SMD封裝的需求

- 中國主要LED公司實現垂直整合

- 傳質玻璃基板封裝技術突破

- 市場限制因素

- 由於中功率LED供應過剩,價格下降

- 對進口高性能磷光體的依賴

- 叢集人事費用上升

- 回收和電子廢棄物合規成本

- 產業價值鏈分析

- 技術分析

- 監理情勢

- 宏觀經濟因素的影響

- 波特五力分析

第5章 市場規模與成長預測

- 透過包裝架構

- 表面黏著型元件(SMD)

- 板載晶片(COB)

- 晶片級封裝(CSP)

- 覆晶LED構裝

- 雙列直插式封裝(DIP/通孔)

- 其他封裝結構(IMD、GOB、Mini-LED 顯示器封裝)

- 按輸出類別

- 低功率(0.5W 或更低)

- 中功率(0.5-1瓦)

- 高功率(1-3瓦)

- 高功率(3瓦或以上)

- 按發光類型

- 可見光LED構裝

- 紅外線(IR) LED構裝

- 紫外線 (UV) LED構裝

- 材料化學

- 基材

- 封裝

- 黏接/晶片貼裝

- 磷光體/塗層

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 家用電子產品

- 工業和特殊應用

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- MLS Co. Ltd.

- NationStar Optoelectronics Co. Ltd.

- Hongli Zhihui Group Co. Ltd.

- Refond Optoelectronics Co. Ltd.

- Jufei Optoelectronics Co. Ltd.

- San'an Optoelectronics Co. Ltd.

- Nichia Corporation

- ams OSRAM AG

- Samsung Electronics Co. Ltd.(Samsung LED)

- Seoul Semiconductor Co. Ltd.

- Lumileds Holding BV

- Everlight Electronics Co. Ltd.

- Bridgelux Inc.

- Citizen Electronics Co. Ltd.

- Cree LED

- Epistar Corporation

- Foshan NationStar Optoelectronics

- Lite-On Technology Corporation

- TongYiFang Optoelectronics

- Ledteen Lighting Co. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the china lED packaging market size is projected to be USD 4.99 billion in 2025, USD 5.26 billion in 2026, and reach USD 7.04 billion by 2031, growing at a CAGR of 6.02% from 2026 to 2031.

This report is Segmented by Packaging Architecture (Chip-On-Board (COB), and More), Power Class (Mid Power (0. 5-1 W), High Power (1-3 W), and More), Emission Type (Visible LED Packages, Infrared (IR) LED Packages, and More), Material Chemistry (Encapsulation, and More), Application (General Lighting, Automotive Lighting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

China LED Packaging Market Trends and Insights

Government-Backed Smart-City LED Retrofits

Municipal procurement programs are replacing legacy streetlights with networked LED luminaires that integrate dimming, sensors, and remote diagnostics. Projects such as the 79 000-unit retrofit completed in Tianjin's Binhai New Area in 2024 cut energy use by 40%, proving the case for mid- to high-power chip-on-board modules. Tender documents increasingly require compliance with GB 7000.1-2024 safety rules and domestic-content thresholds, directing contract awards to Chinese packagers that can certify interoperability with national IoT standards. Because smart-streetlight controllers collect telemetry, suppliers with robust analytics platforms gain recurring service revenue. This shift toward performance-based contracts strengthens the grip of vertically integrated players that maintain in-house driver electronics and field-failure diagnostics.

Accelerating Mini/Micro-LED Backlighting Adoption

China shipped more than 8 million mini-LED televisions in 2025, and volumes are forecast to top 10 million units in 2026 as retail prices for 100-inch panels fall below CNY 10 000 (USD 1 385). Flagship sets such as Hisense's 116-inch RGB mini-LED achieve 97% BT.2020 coverage and 10 000-nit peaks by tripling die counts per panel, massively expanding demand for chip-scale packages. Placement tolerances tighter than 50 µm and yield targets above 99.9% elevate the barrier to entry, prompting long-term supply tie-ups between BOE, China Star Optoelectronics, and domestic packagers. Korean and Japanese competitors now face a 50% price disadvantage on comparable specifications, spurring them to accelerate their own RGB micro-LED roadmaps.

Price Erosion from Excess Mid-Power Capacity

March 2026 list-price hikes of 3%-25% announced by leading packagers were quickly undercut in Zhejiang, where defect rates in budget lines still hover near 15% and equipment utilization lags the 85% break-even threshold. Combined industry revenue grew 8.9% in 2024, yet profit expansion was confined to firms with automotive or mini-LED focus, highlighting the fragility of commodity pricing. Revenue at MLS and NationStar declined in the first half of 2025, even as niche players Refond and Jufei posted double-digit growth, confirming the structural oversupply in mid-power formats. Until plant closures or demand growth absorb this overhang, margin compression will persist, discouraging fresh investment in SMD lines.

Other drivers and restraints analyzed in the detailed report include:

- Automotive LED Penetration in NEVs

- Export-Oriented EMS Demand for SMD Packages

- Dependence on Imported High-Performance Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chip-scale packages are projected to expand at a 6.78% CAGR through 2031 as television makers move from white backlights to RGB mini-LED engines that need higher die density and tighter placement tolerances. Surface-mount device formats still held 42.78% of the China LED packaging market share in 2025, as decades of automation have driven defect rates below 2% and pushed unit pricing to under USD 0.10 for 10 000-piece orders.

High-volume 2835, 3030, and 5050 footprints remain indispensable in residential lamps, yet flip-chip devices without wire bonds now dominate high-current automotive modules that need superior heat dissipation. Glass-substrate mass-transfer lines under construction in Tianmen aim for 99.995% transfer yields, a threshold that could unlock cost-effective micro-LED wearables and automotive displays.

In 2025, mid-power LEDs, rated between 0.5-1 W, accounted for 35.49% of total revenue. However, due to a persistent oversupply, these LEDs are grappling with single-digit gross margins. On the other hand, high-power packages, rated between 1-3 W, are witnessing a growth rate of 6.94% CAGR. This surge is largely attributed to their adoption in adaptive driving-beam headlights and industrial high-bay luminaires, both of which are known to reduce fixture counts and maintenance labor.

Indicator-class emitters with power levels below 0.5 W play a dominant role in the wearables and signage markets. However, the extremely narrow profit margins in these segments significantly constrain opportunities for reinvestment and further development. At the top end, copper-substrate emitters above 3 W now target horticultural grow lights and stadium floodlamps that absorb the 30%-50% price premium in exchange for higher lumen density and long L70 life.

List of Companies Covered in this Report:

- MLS Co. Ltd.

- NationStar Optoelectronics Co. Ltd.

- Hongli Zhihui Group Co. Ltd.

- Refond Optoelectronics Co. Ltd.

- Jufei Optoelectronics Co. Ltd.

- San'an Optoelectronics Co. Ltd.

- Nichia Corporation

- ams OSRAM AG

- Samsung Electronics Co. Ltd. (Samsung LED)

- Seoul Semiconductor Co. Ltd.

- Lumileds Holding B.V.

- Everlight Electronics Co. Ltd.

- Bridgelux Inc.

- Citizen Electronics Co. Ltd.

- Cree LED

- Epistar Corporation

- Foshan NationStar Optoelectronics

- Lite-On Technology Corporation

- TongYiFang Optoelectronics

- Ledteen Lighting Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-Backed Smart-City LED Retrofits

- 4.2.2 Accelerating Mini / Micro-LED Backlighting Adoption

- 4.2.3 Automotive LED Penetration in NEVs

- 4.2.4 Export-Oriented EMS Demand for SMD Packages

- 4.2.5 Vertical Integration by Chinese LED Champions

- 4.2.6 Mass-Transfer Glass Substrate Packaging Breakthroughs

- 4.3 Market Restraints

- 4.3.1 Price Erosion from Excess Mid-Power Capacity

- 4.3.2 Dependence on Imported High-Performance Phosphors

- 4.3.3 Labor-Cost Inflation in Coastal Clusters

- 4.3.4 Recycling And E-Waste Compliance Costs

- 4.4 Industry Value-Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Architecture

- 5.1.1 Surface Mount Device (SMD)

- 5.1.2 Chip-on-Board (COB)

- 5.1.3 Chip Scale Package (CSP)

- 5.1.4 Flip-Chip LED Packages

- 5.1.5 Dual In-line Package (DIP / Through-hole)

- 5.1.6 Other Packaging Architectures (IMD, GOB, Mini-LED Display Packaging)

- 5.2 By Power Class

- 5.2.1 Low Power (Below 0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (1-3 W)

- 5.2.4 Ultra-High Power (Above 3 W)

- 5.3 By Emission Type

- 5.3.1 Visible LED Packages

- 5.3.2 Infrared (IR) LED Packages

- 5.3.3 Ultraviolet (UV) LED Packages

- 5.4 By Material Chemistry

- 5.4.1 Substrates

- 5.4.2 Encapsulation

- 5.4.3 Bonding / Die-Attach

- 5.4.4 Phosphors / Coatings

- 5.5 By Application

- 5.5.1 General Lighting

- 5.5.2 Automotive Lighting

- 5.5.3 Display And Backlighting

- 5.5.4 Consumer Electronics

- 5.5.5 Industrial and Specialty

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share, Products and Services, Recent Developments)

- 6.4.1 MLS Co. Ltd.

- 6.4.2 NationStar Optoelectronics Co. Ltd.

- 6.4.3 Hongli Zhihui Group Co. Ltd.

- 6.4.4 Refond Optoelectronics Co. Ltd.

- 6.4.5 Jufei Optoelectronics Co. Ltd.

- 6.4.6 San'an Optoelectronics Co. Ltd.

- 6.4.7 Nichia Corporation

- 6.4.8 ams OSRAM AG

- 6.4.9 Samsung Electronics Co. Ltd. (Samsung LED)

- 6.4.10 Seoul Semiconductor Co. Ltd.

- 6.4.11 Lumileds Holding B.V.

- 6.4.12 Everlight Electronics Co. Ltd.

- 6.4.13 Bridgelux Inc.

- 6.4.14 Citizen Electronics Co. Ltd.

- 6.4.15 Cree LED

- 6.4.16 Epistar Corporation

- 6.4.17 Foshan NationStar Optoelectronics

- 6.4.18 Lite-On Technology Corporation

- 6.4.19 TongYiFang Optoelectronics

- 6.4.20 Ledteen Lighting Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

LED構裝市場規模、佔有率和趨勢分析報告:按材料、封裝類型、應用、地區和細分市場分類(2026-2033年)

LED構裝市場規模、佔有率和趨勢分析報告:按材料、封裝類型、應用、地區和細分市場分類(2026-2033年) LED構裝設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

LED構裝設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 晶片級封裝LED市場:依LED類型、應用和最終用途分類-2026-2032年全球市場預測LED構裝市場:依封裝類型、基板材料、晶片類型和應用分類-全球預測,2026-2032年LED導線架市場按產品、材質、電鍍類型、導線架類型和最終用戶分類 - 全球預測 2026-2032

晶片級封裝LED市場:依LED類型、應用和最終用途分類-2026-2032年全球市場預測LED構裝市場:依封裝類型、基板材料、晶片類型和應用分類-全球預測,2026-2032年LED導線架市場按產品、材質、電鍍類型、導線架類型和最終用戶分類 - 全球預測 2026-2032 LED構裝市場規模、佔有率及成長分析(按應用、技術、最終用途及地區分類)-2026-2033年產業預測

LED構裝市場規模、佔有率及成長分析(按應用、技術、最終用途及地區分類)-2026-2033年產業預測