|

市場調查報告書

商品編碼

2066434

亞太地區LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia Pacific LED Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

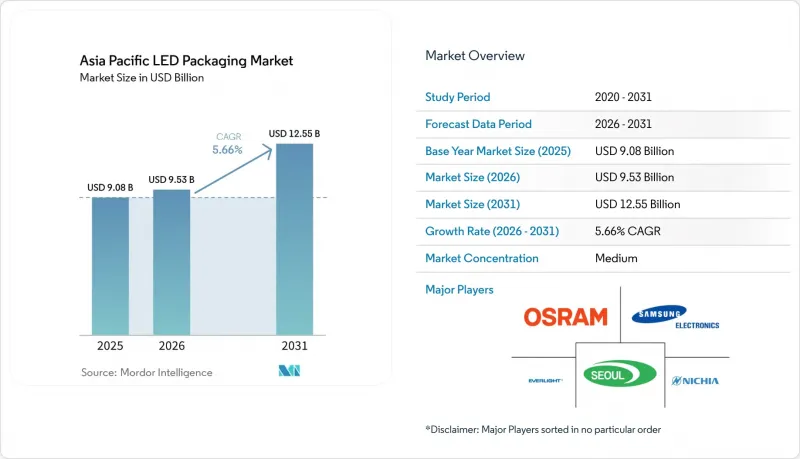

根據 Mordor Intelligence 預測,亞太地區LED構裝市場規模預計將從 2025 年的 90.8 億美元成長到 2026 年的 95.3 億美元,然後在 2031 年達到 125.5 億美元,2026 年至 2031 年的複合年成長率為 5.66%。

本報告按封裝類型(表面黏著型元件、板載晶片等)、功率等級(低功耗等)、發光類型(可見光LED構裝等)、材料化學(基板、封裝、鍵結和晶片貼裝等)、應用(通用照明、汽車照明等)和地區進行細分。市場預測以美元計價。

亞太地區LED構裝市場趨勢及洞察

Mini-LED 和 Micro-LED 背光燈的快速普及

由於中國的能源效率補貼計畫優先扶持符合L1級能源效率標準的電視,電視製造商加快了Mini LED在區域出貨量中的滲透,預計到2026年,Mini LED的出貨量將佔比達到約10%。三星發表了六款Micro RGB電視,這些電視無需彩色濾光片,並已獲得BT.2020色域認證,推動了晶片級整合化的發展。從小米到寶馬,各大汽車製造商都在致力於採用亮度超過4000尼特的Mini LED駕駛座顯示螢幕,這帶動了對能夠承受高結溫的高亮度封裝的需求。這種轉變促進了板載晶片(COB)和玻璃基板模組的發展,促使面板製造商將封裝製程內部化,並迫使獨立供應商專注於高良率、大批量封裝設備的研發。預計到2026年,Micro LED的銷售額將加倍,達到1.054億美元;近眼AR設備的出貨量預計到2030年將達到2,100萬台,這將為封裝技術的持續創新奠定基礎。

政府的能源效率法規鼓勵LED的廣泛應用。

中國於2026年3月頒布的新標準擴大了適用範圍,將射燈、高棚燈和待機功率限制為0.5瓦的智慧產品納入其中,提高了商業建築的光通量效率標準。在日本,為實現脫碳目標,已強制要求在2030年實現全國高速公路100%使用LED照明。印度的「生產連結獎勵計畫計畫」旨在透過投資1,0478千羅爾(約12.6億美元)用於在地化生產,將國內增值率提高到75-80%。亞洲和歐洲之間不同的測試標準要求出口商對產品進行雙重認證,這推動了板載晶片封裝(COB)的需求。

對先進包裝設備進行大量初始資本投資

C Sun公司已投資14.8億新台幣(約4,690萬美元)在台中新建工廠,引進人工智慧驅動的先進封裝工具。這凸顯了實現±1µm精度Micro LED定位所需的巨額初始投資。無錫諾沃的泰國分公司正透過Mini LED背光燈的自動化生產為當地客戶提供支持,但即使是代工組裝也需要專有的機器人技術,而許多中小企業難以資金籌措。 NationStar計劃投資9.701億元人民幣(約1.164億美元)用於六個Mini和Micro LED項目,但預計7-8年的投資回收期阻礙了後後進企業進入市場。這些經濟因素意味著新增產能將集中在能夠將資本投資分攤到多條產品線上的大型企業集團和合資企業手中。

細分市場分析

2025年,表面黏著型元件(SMD)封裝在亞太地區LED構裝市場總規模中佔比43.74%,並持續在通用照明燈具和側入式顯示器領域保持主導地位。晶片級封裝(CSP)的銷售額預計到2031年將以6.28%的複合年成長率成長,這主要得益於覆晶設計,該設計無需陶瓷基板,可降低材料清單並減少熱阻。中國面板製造商擴大採用板載晶片(COB)Mini LED燈條用於75英寸及以上尺寸的電視,這壓縮了供應鏈,並擠壓了獨立封裝製造商的利潤空間。日本和韓國的汽車零件供應商傾向於採用覆晶式封裝,以簡化自動化光學檢測並支援LED單元電流檢測,這是AEC認證頭燈的強制性要求。

CSP成本的持續下降歸功於晶圓級高產能和更少的組裝步驟,但在戶外標誌領域,硫化物暴露和高濕度環境下的可靠性仍然是令人擔憂的問題。 SMD製造商正透過改進環氧樹脂封裝材料和引入二次光學元件來應對這些問題,但價格差異仍然存在。目前,亞太地區的LED構裝產業正呈現日益兩極化的趨勢。Delta地區、江蘇省和台灣地區大規模運作通用SMD生產線,而與驅動後端工藝配套的CSP生產線則專注於對性能要求極高的領域。隨著顯示器和汽車行業封裝業務的日益內部化,缺乏先進傳質技術或覆晶專業知識的供應商正面臨著市場佔有率的萎縮。

至2025年,中功率(0.5-1瓦)裝置將佔亞太地區LED構裝市佔率的39.38%。高功率LED(1瓦以上)裝置的成長速度較快,年複合成長率達6.21%,主要得益於自我調整遠光燈對高流明密度的需求。雖然散熱過孔最佳化技術已使一些中功率LED產品得以進入室內高棚燈這一細分市場,但汽車行業規範仍要求採用能夠承受-40 度C至125 度C溫度循環的陶瓷或金屬基板。

功率超過 3 瓦的高功率陣列主要面向體育場館和溫室等需要盡可能減少照明燈具數量的場所。原始設備製造商 (OEM) 正在考慮採用單一高功率發送器還是叢集中功率組件。叢集可以降低熱量集中,但會增加驅動通道的數量和光學對準的複雜性。能夠提供全功率範圍產品的供應商可以滿足這些架構選擇,並確保無論 OEM 選擇何種設計方案,都能維持穩定的銷售量。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- Mini-LED 和 Micro-LED 背光燈的快速普及

- 政府對節能的強制規定正在推動LED的普及。

- 由於規模經濟效應, LED構裝的平均售價(ASP)正在下降。

- 汽車LED在頭燈和ADAS(先進駕駛輔助系統)的應用率不斷提高。

- 中國和印度先進包裝生產線在地化獎勵

- 推出用於客製化園藝照明的覆晶CSP

- 市場限制因素

- 先進包裝設備的初始資本投資成本高

- 高功率封裝中的溫度控管挑戰

- 由於稀土元素供應瓶頸,磷光體供應受到限制。

- 專利到期導致的價格壓力

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 按包裝類型

- 表面黏著型元件(SMD)

- 板載晶片(COB)

- 晶片級封裝(CSP)

- 覆晶LED構裝

- 雙列直插封裝(DIP/通孔)

- 其他包裝形式

- 按電力等級

- 低功率(小於0.5瓦)

- 中功率(0.5–1 瓦)

- 高功率(1-3瓦)

- 高功率(3瓦或以上)

- 按發光類型

- 可見光LED構裝

- 紅外線LED構裝

- 紫外線LED構裝

- 材料化學

- 基材

- 封裝

- 黏接/晶片貼裝

- 磷光體/塗層

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 家用電子產品

- 工業和專業應用

- 按地區

- 中國

- 日本

- 印度

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Samsung Electronics Co., Ltd.(Samsung LED)

- Osram GmbH(OSRAM Opto Semiconductors)

- Seoul Semiconductor Co., Ltd.

- Everlight Electronics Co., Ltd.

- Cree LED, Inc.

- LG Innotek Co., Ltd.

- Lumileds Holding BV

- Guangzhou Nationstar Optoelectronics Co., Ltd.

- Shenzhen Hongli Zhihui Group Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Epistar Corporation

- Toyoda Gosei Co., Ltd.

- Lextar Electronics Corp.

- Dominant Opto Technologies Sdn. Bhd.

- Opto Tech Corporation

- Refond Optoelectronics Co., Ltd.

- MLS Co., Ltd.(Forest Lighting)

- Advanced Optoelectronic Technology, Inc.

- Bridgelux, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia pacific lED packaging market size is expected to grow from USD 9.08 billion in 2025 to USD 9.53 billion in 2026 and is forecast to reach USD 12.55 billion by 2031 at a 5.66% CAGR over 2026-2031.

This report is Segmented by Packaging Architecture (Surface Mount Device, Chip-On-Board, and More), Power Class (Low Power, and More), Emission Type (Visible LED Packages, and More), Material Chemistry (Substrates, Encapsulation, Bonding and Die-Attach, and More), Application (General Lighting, Automotive Lighting, and More), and Geography. The Market Forecasts are Provided in USD.

Asia Pacific LED Packaging Market Trends and Insights

Rapid Adoption of Mini-LED and Micro-LED Backlighting

Television makers accelerated Mini LED penetration to roughly 10% of regional shipments in 2026, as energy-efficiency subsidies in China reward Level-1-compliant sets. Samsung introduced six Micro RGB TV sizes that eliminate color filters and deliver full BT.2020 gamut certification, reinforcing the move toward chip-level integration. Automakers from Xiaomi to BMW are committed to Mini LED cockpit displays that exceed 4,000 nits, expanding demand for high-brightness packages that manage elevated junction temperatures. The shift favors chip-on-board and glass-substrate modules, prompting panel makers to internalize packaging and forcing independent vendors to specialize in high-yield mass-transfer equipment. Micro LED revenue doubled to USD 105.4 million in 2026, and near-eye AR shipments are projected at 21 million units by 2030, setting the stage for sustained packaging innovation.

Government Energy-Efficiency Mandates Boosting LED Uptake

China's March 2026 standard widened coverage to spotlight, high-bay luminaires, and smart products with a 0.5-watt standby limit, tightening efficacy baselines across commercial construction. Japan mandated 100 % LED road lighting on national highways by 2030 to meet decarbonization goals. India's Production-Linked Incentive scheme unlocked INR 10 478 crore (USD 1.26 billion) for localization, aiming to lift domestic value addition to 75-80%. Divergent testing protocols between Asia and Europe compel exporters to dual-qualify products, spurring demand for chip-on-board packages that surpass 150 lumens-per-watt.

High Initial CapEx for Advanced Packaging Equipment

C Sun invested NT 1.48 billion (USD 46.9 million) in a new Taichung site for AI-driven advanced packaging tools, underlining the steep outlay required for +-1 µm Micro LED placement accuracy. Wuxi NOVO's Thailand branch supports regional customers with Mini LED backlight automation, yet even contract assembly now demands proprietary robotics that many small companies cannot finance. NationStar plans CNY 970.1 million (USD 116.4 million) in six Mini and Micro LED projects, with payback periods of 7 to 8 years, discouraging late entrants. These economics channel new capacity toward large conglomerates or joint ventures that can amortize tooling over multiple product lines.

Other drivers and restraints analyzed in the detailed report include:

- Declining ASP of LED Packages Through Economies of Scale

- Rising Automotive LED Penetration in Headlamps and ADAS

- Thermal Management Challenges in High-Power Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface Mount Device packages accounted for 43.74% of the Asia Pacific LED packaging market size in 2025, sustaining dominance in general illumination fixtures and edge-lit displays. Chip Scale Package revenue is advancing at a 6.28% CAGR through 2031 as flip-chip designs eliminate ceramic submounts, trim the bill of materials, and reduce thermal resistance. Panel makers in China increasingly deploy chip-on-board Mini LED bars in 75-inch-plus televisions, compressing the supply chain and shifting profit pools away from independent packagers. Japanese and Korean automotive suppliers favor flip-chip layouts that simplify automated optical inspection and support per-LED current sensing, a prerequisite for AEC-qualified headlamps.

Continued CSP cost erosion stems from high wafer-level throughput and fewer assembly steps, yet reliability under sulfur exposure and high humidity remains a concern for outdoor signage. SMD producers are responding with epoxy-mold-compound upgrades and secondary optics, but price gaps persist. The Asia Pacific LED packaging industry now observes a dual-track model: commodity SMD lines run at hyperscale in the Pearl River Delta, whereas CSP lines co-located with driver back-end flow in Jiangsu and Taiwan focus on performance-critical segments. Suppliers lacking advanced mass-transfer or flip-chip expertise face shrinking addressable markets as display and automotive verticals internalize packaging.

Mid-power parts ranging from 0.5-1 W captured 39.38% of Asia Pacific LED packaging market share in 2025. High-power components above 1 W are growing faster at 6.21% CAGR as adaptive-beam headlamps demand robust lumen density. Thermal-via optimization allows select mid-power footprints to encroach on indoor high-bay niches; however, automotive specifications still require ceramic or metal-core substrates that withstand -40 °C to 125 °C cycles.

Ultra-high-power arrays above 3 W address sports arenas and horticulture greenhouses where fixture count must be minimized. OEMs weigh single high-power emitters against clustered mid-power assemblies: clusters lower thermal hotspots but increase driver channel count and optical alignment complexity. Suppliers that span the full power spectrum hedge against these architecture choices and lock in volume regardless of OEM design selection.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd. (Samsung LED)

- Osram GmbH (OSRAM Opto Semiconductors)

- Seoul Semiconductor Co., Ltd.

- Everlight Electronics Co., Ltd.

- Cree LED, Inc.

- LG Innotek Co., Ltd.

- Lumileds Holding B.V.

- Guangzhou Nationstar Optoelectronics Co., Ltd.

- Shenzhen Hongli Zhihui Group Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Epistar Corporation

- Toyoda Gosei Co., Ltd.

- Lextar Electronics Corp.

- Dominant Opto Technologies Sdn. Bhd.

- Opto Tech Corporation

- Refond Optoelectronics Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

- Advanced Optoelectronic Technology, Inc.

- Bridgelux, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Mini-LED and Micro-LED Backlighting

- 4.2.2 Government Energy-Efficiency Mandates Boosting LED Uptake

- 4.2.3 Declining ASP of LED Packages Through Economies of Scale

- 4.2.4 Rising Automotive LED Penetration in Headlamps and ADAS

- 4.2.5 Localization Incentives for Advanced Packaging Lines in China and India

- 4.2.6 Emergence of Flip-Chip CSP for Horticulture Lighting Customisation

- 4.3 Market Restraints

- 4.3.1 High Initial CapEx for Advanced Packaging Equipment

- 4.3.2 Thermal Management Challenges in High-Power Packages

- 4.3.3 Phosphor Supply Constraints from Rare-Earth Bottlenecks

- 4.3.4 Patent Expiry Cliff Creating Pricing Pressures

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Architecture

- 5.1.1 Surface Mount Device (SMD)

- 5.1.2 Chip-on-Board (COB)

- 5.1.3 Chip Scale Package (CSP)

- 5.1.4 Flip-Chip LED Packages

- 5.1.5 Dual In-line Package (DIP / Through-hole)

- 5.1.6 Others, Packaging Architecture

- 5.2 By Power Class

- 5.2.1 Low Power (Less than 0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (1-3 W)

- 5.2.4 Ultra-High Power (More than 3 W)

- 5.3 By Emission Type

- 5.3.1 Visible LED Packages

- 5.3.2 Infrared LED Packages

- 5.3.3 Ultraviolet LED Packages

- 5.4 By Material Chemistry

- 5.4.1 Substrates

- 5.4.2 Encapsulation

- 5.4.3 Bonding / Die-Attach

- 5.4.4 Phosphors / Coatings

- 5.5 By Application

- 5.5.1 General Lighting

- 5.5.2 Automotive Lighting

- 5.5.3 Display and Backlighting

- 5.5.4 Consumer Electronics

- 5.5.5 Industrial and Specialty

- 5.6 By Geography

- 5.6.1 China

- 5.6.2 Japan

- 5.6.3 India

- 5.6.4 Southeast Asia

- 5.6.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd. (Samsung LED)

- 6.4.3 Osram GmbH (OSRAM Opto Semiconductors)

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Everlight Electronics Co., Ltd.

- 6.4.6 Cree LED, Inc.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Lumileds Holding B.V.

- 6.4.9 Guangzhou Nationstar Optoelectronics Co., Ltd.

- 6.4.10 Shenzhen Hongli Zhihui Group Co., Ltd.

- 6.4.11 Sanan Optoelectronics Co., Ltd.

- 6.4.12 Epistar Corporation

- 6.4.13 Toyoda Gosei Co., Ltd.

- 6.4.14 Lextar Electronics Corp.

- 6.4.15 Dominant Opto Technologies Sdn. Bhd.

- 6.4.16 Opto Tech Corporation

- 6.4.17 Refond Optoelectronics Co., Ltd.

- 6.4.18 MLS Co., Ltd. (Forest Lighting)

- 6.4.19 Advanced Optoelectronic Technology, Inc.

- 6.4.20 Bridgelux, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

LED構裝市場規模、佔有率和趨勢分析報告:按材料、封裝類型、應用、地區和細分市場分類(2026-2033年)

LED構裝市場規模、佔有率和趨勢分析報告:按材料、封裝類型、應用、地區和細分市場分類(2026-2033年) LED構裝設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中國LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

LED構裝設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中國LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 晶片級封裝LED市場:依LED類型、應用和最終用途分類-2026-2032年全球市場預測LED構裝市場:依封裝類型、基板材料、晶片類型和應用分類-全球預測,2026-2032年LED導線架市場按產品、材質、電鍍類型、導線架類型和最終用戶分類 - 全球預測 2026-2032

晶片級封裝LED市場:依LED類型、應用和最終用途分類-2026-2032年全球市場預測LED構裝市場:依封裝類型、基板材料、晶片類型和應用分類-全球預測,2026-2032年LED導線架市場按產品、材質、電鍍類型、導線架類型和最終用戶分類 - 全球預測 2026-2032 LED構裝市場規模、佔有率及成長分析(按應用、技術、最終用途及地區分類)-2026-2033年產業預測

LED構裝市場規模、佔有率及成長分析(按應用、技術、最終用途及地區分類)-2026-2033年產業預測