|

市場調查報告書

商品編碼

2063945

LED構裝設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)LED Packaging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

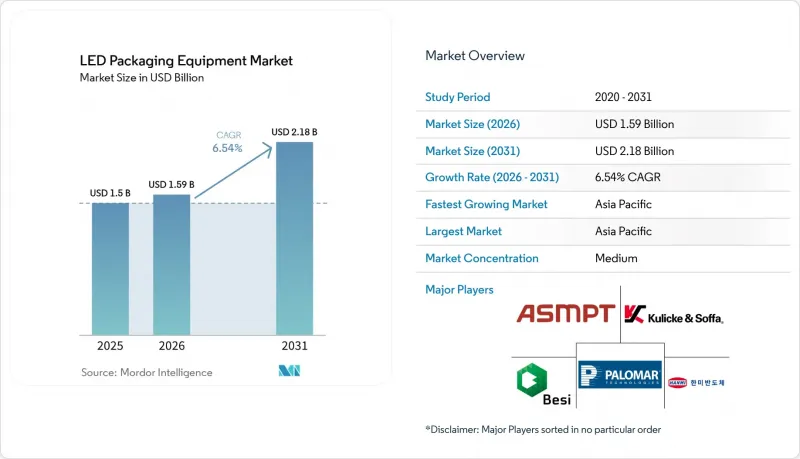

根據 Mordor Intelligence 預測, LED構裝設備市場預計將從 2025 年的 15 億美元成長到 2026 年的 15.9 億美元,到 2031 年達到 21.8 億美元,2026 年至 2031 年的複合年成長率為 6.54%。

本報告按設備類型(晶片鍵合設備、焊線設備、封裝設備等)、封裝類型(SMD LED構裝、COB封裝、CSP LED構裝)、LED應用(通用照明、顯示器、汽車照明、家用電子電器)和地區(北美、歐洲等)進行細分。市場預測以美元(USD)計價。

全球LED構裝設備市場趨勢與洞察

微型LED和迷你LED產能快速擴張

各細分領域的領導者正在擴大使用數萬顆迷你LED的全陣列局部調光面板的生產規模,這需要傳輸晶片且精度不低於±10微米的設備。 ASMPT的Vortex II晶片鍵合機在2mil x 4mil的晶片上實現了99.999%的發光良率,提高了先進顯示器的性能標準。 Kulicke和Soffa的LUMINEX雷射系統將分類和重新排列整合到單一單元中,擴展了整個DirectView RGB和背光工作流程的應用前景。 Besi預測,在光電和LED技術普及的推動下,到2026年,晶片貼裝市場規模將加倍,達到16億美元。這些升級將使每條生產線的資本成本增加高達40%,為政府支持的一級面板製造商帶來規模經濟效益。小規模的晶圓廠正努力維持產能,這可能會加速產業整合。

汽車主動式轉向頭燈的廣泛應用

汽車製造商正轉向矩陣式LED系統,可提供無眩光遠光燈和600公尺的照明距離,這使得封裝公差在Z軸方向上的高度限制達到±35微米。歐司朗的OSLON Compact PL系列採用絕緣導熱焊盤,需要高精度的拾取和放置製程以及可控的導熱界面材料。像素化發光體需要亞像素級的精確定位,因此供應商正在整合高解析度視覺系統和自動恢復迴路來補償放置誤差。 AEC-Q102認證可能需要長達24個月的時間,雖然檢驗過程漫長,但擁有汽車行業認證製程配方的供應商具有優勢。隨著歐洲放鬆管制措施擴展到北美和亞洲,自我調整模組預計將成為中階車型的標準配置,這將帶動晶片鍵合機和偵測工具訂單的成長。

對受美國出口管制約束的線焊設備進行貿易合規性審計。

2024年12月,美國工業與安全局(BIS)在其受監管物品清單中新增了24類設備,擴大了「外國直接產品(FDP)」規則的適用範圍,將國外製造但包含美國製造積體電路的設備也納入其中。封裝供應商目前面臨60至90天的交貨延遲,因為他們需要等待許可證才能拿到。應用材料公司支付了2.52億美元的和解金,這一案例清楚地表明了錯誤分類造成的經濟損失。一些供應商正在考慮重新設計運動控制板以去除美國製造的組件,但工程成本高昂,而且性能可能會受到影響。不受這些限制影響的中國設備製造商看到了搶佔市場佔有率的機會,尤其是在那些努力滿足北京「50%在地採購」要求的晶圓廠(半導體製造廠)。

細分市場分析

預計到2025年,晶片鍵合機將佔LED封裝設備市場銷售額的35.68%,凸顯其在LED構裝設備市場的核心地位。引線鍵合機仍然很重要,但由於覆晶和CSP設計的興起,以及互連方式轉向凸塊下連接,其市場佔有率正在下降。在製程中,晶片放置後會進行封裝膠,使用紫外線或熱固化矽膠或環氧樹脂保護鍵結。自動化封裝系統將這三個製程以及線上檢測整合到承包單元中,從而縮短了週期時間。這些生產線為早期採用者提供了明顯的整體擁有成本(TCO)優勢,因為它們可以將產量提高20-30%,並將人事費用降低約15-20%。 ASMPT的「線上連接系統」將其Vortex II鍵合機與前端和後端工作站同步,顯著提高了生產效率。雖然自動化平台的成本是獨立設備的2到3倍,但當運轉率超過80%時,投資回收期就會縮短。亞洲中小型廠商目前正將晶片貼裝、點膠和視覺模組等設備打包銷售,以吸引價格敏感型買家。因此,預計到預測期結束時,自動化生產線將在LED構裝設備市場佔據更大的佔有率。

自動化程度的激增符合「工業4.0」的要求,後者要求資料可追溯性、預測性維護和遠距離診斷。歐洲客戶依賴翻新設備來降低資本支出 (CAPEX),而北美晶圓廠則傾向於使用全新的、完全互聯的設備,以符合與政府獎勵相關的可追溯性法規。由於這兩個地區都面臨技術工人短缺的問題,自校準焊接機和自動編程AOI降低了技術門檻。預計這種轉型不會同步進行,二級組裝仍在運作半自動化工作單元,而一級顯示器和汽車零件供應商則擴大轉向全自動化工廠。能夠提供模組化升級的供應商可以滿足這兩種需求,並緩解與經濟週期相關的收入波動。

區域分析

預計亞太地區將佔據主導地位,到2025年將佔LED構裝設備市場68.71%的佔有率,並預計到2031年將維持7.17%的複合年成長率。中國50%的國產設備配額制度正在加速從Naura和JT Automation等公司在地採購,除非進口商建立合資企業,否則將被邊緣化。日本的「Rapidus」計畫提供535億日圓(約3.55億美元)的補貼,旨在重新運作先進封裝技術,並為精密工具供應商帶來新的基本客群。韓國韓美半導體利用在地化服務超越了新川智行在美光科技的地位,這表明設備運轉率和接近性優勢比傳統老牌企業更具吸引力。

預計到2025年,北美和歐洲合計約佔全球銷售額的四分之一。該地區的LED構裝設備市場受到嚴格的出口合規要求和勞動力短缺的雙重限制。美國商務部工業安全局(BIS)的法規導致包括美國製造的積體電路在內的產品出貨延遲,迫使一些供應商重新設計基板以降低「美國化」程度。另一方面,《晶片與科學法案》正在推動國內先進封裝生產線的津貼,部分抵銷了合規負擔。在歐洲,人們對經過認證的翻新設備越來越感興趣,TOWA的翻新項目可提供40%至60%的價格折扣,但由於缺乏全部區域的品質保證標誌,資金籌措存在不確定性。

預計到2025年,南美洲和中東及非洲地區的銷售額將佔總銷售額的不到7%。這些地區的業務主要集中在組裝進口LED晶片組裝成成品燈具和標誌模組。儘管政府的電氣化計劃可能會引入承包生產線,但現場技術人員短缺和備件物流問題阻礙了大規模自動化。隨著通訊業者主導的智慧城市示範計畫的推進,可能會出現對中型AOI(自動光學偵測)生產線的局部需求,但這種需求仍然很小,不太可能影響全球供應商的藍圖。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 產業供應鏈分析

- 監理情勢

- 科技趨勢

- 宏觀經濟因素的影響

- 市場促進因素

- 迷你LED和微型LED產能快速擴張

- 汽車自我調整頭燈的廣泛應用

- 透過線上AOI/AXI整合提高生產線良率

- 低溫燒結銀晶片黏接膏的需求

- 亞太地區政府對國內包裝生產線的補貼

- 在歐洲建立設備翻新市場

- 市場限制因素

- 關於美國出口管制線焊機的貿易合規性審計

- 高功率發電線路中的熱失控風險

- 10µm以下覆晶鍵合技術熟練工人短缺

- 二線顯示器製造商凍結資本投資

- 波特五力分析

第5章 市場規模與成長預測

- 依設備類型

- 晶片黏合設備

- 焊線設備

- 封裝裝置

- 自動包裝系統

- 按包裝類型

- SMD LED構裝

- COB 包

- CSP LED構裝

- 透過LED應用

- 一般照明

- 展示

- 汽車照明

- 家用電子產品

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 東南亞

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ASM Pacific Technology Ltd.

- Kulicke and Soffa Industries Inc.

- BE Semiconductor Industries NV

- Hanmi Semiconductor Co., Ltd.

- Palomar Technologies Inc.

- Shinkawa Ltd.

- Toray Engineering Co., Ltd.

- Suneast Equipment Co., Ltd.

- Besi APAC Pte. Ltd.

- ASMPT Suzhou Co., Ltd.

- F&K Delvotec Bondtechnik GmbH

- Towa Corporation

- Nordson Corporation

- DIAS Automation(Suzhou)Co., Ltd.

- Hitachi High-Tech Corporation

- Nitto Denko Corporation

- Shenzhen JT Automation Equipment Co., Ltd.

- Tronstol Technology Co., Ltd.

- Datacon Technology GmbH

- Revasum Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the lED packaging equipment market size is expected to increase from USD 1.50 billion in 2025 to USD 1.59 billion in 2026 and reach USD 2.18 billion by 2031, growing at a CAGR of 6.54% over 2026-2031.

This report is Segmented by Equipment Type (Die Bonding Equipment, Wire Bonding Equipment, Encapsulation Equipment, and More), Package Type (SMD LED Packaging, COB Packaging, and CSP LED Packaging), LED Application (General Lighting, Displays, Automotive Lighting, and Consumer Electronics), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global LED Packaging Equipment Market Trends and Insights

Rapid Mini-LED and Micro-LED Capacity Ramp-Up

Segment leaders are scaling full-array local-dimming panels that use tens of thousands of mini-LEDs, forcing equipment to deliver mass-transfer speed without compromising +-10 micrometer accuracy. ASMPT's Vortex II die bonder hits 99.999% light-up yield for 2 mil X 4 mil dies, raising the performance bar for advanced display deployment. Kulicke and Soffa's LUMINEX laser system couples sorting and re-pitching in one tool, widening addressable opportunities across direct-view RGB and backlighting workflows. Besi projects its die-attach addressable market to double to USD 1.6 billion by 2026 on the back of photonics and LED adoption. These upgrades lift capital per line by as much as 40%, creating scale advantages for tier-1 panel makers with access to state support. Smaller fabs struggle to match throughput, potentially accelerating industry consolidation.

Rising Adoption of Automotive Adaptive Headlamps

Automakers are migrating to matrix LED systems that enable glare-free high beams and 600-meter reach, pushing packaging tolerances toward +-35 micrometers in z-height. ams OSRAM's OSLON Compact PL families come with isolated thermal pads that demand precision pick-and-place and controlled thermal-interface materials. Pixelated emitters require sub-pixel placement, so equipment vendors are embedding high-resolution vision systems and auto-recovery loops for misplacement correction. Qualification under AEC-Q102 can last 24 months, elongating the validation pipeline and favoring suppliers with automotive-certified process recipes. As regulatory green lights spread from Europe to North America and Asia, adaptive modules are set to become standard on mid-range trims, stimulating higher unit orders for die bonders and inspection tools.

Trade-Compliance Audits on US Export-Controlled Wire-Bonders

The U.S. Bureau of Industry and Security added 24 tool categories to its controlled list in December 2024 and extended Foreign Direct Product rules to foreign-made gear containing U.S. ICs. Packaging suppliers now face 60-90 day shipment delays while licenses clear, and Applied Materials' USD 252 million settlement illustrates the monetary downside of mis-classification. Some vendors contemplate redesigning motion-control boards to rid U.S. content, but engineering costs are steep and performance may slip. Chinese toolmakers free of these constraints are finding an opening to capture share, particularly among fabs racing to meet Beijing's 50% local-equipment threshold.

Other drivers and restraints analyzed in the detailed report include:

- Line Yield Gains Via Inline AOI/AXI Integration

- Demand for Low-Temperature Sintered Silver Die-Attach Pastes

- Thermal Run-Away Risks in High-Power CSP Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Die bonders accounted for 35.68% of 2025 revenue, underscoring their central role in the LED packaging equipment market. Wire bonders remain relevant, yet flip-chip and CSP designs erode their volume share as interconnects shift under-bump. Encapsulation dispensers follow die placement in the process flow, coupling silicone or epoxy resins with UV or thermal curing to protect the junction. Automated packaging systems combine all three steps, plus inline inspection, into turnkey cells that shorten takt time. These lines command 20-30% higher throughput and cut labor by roughly 15-20%, giving early adopters a measurable cost-of-ownership edge. ASMPT's In-Line Linker System synchronizes its Vortex II bonder with upstream and downstream stations, proving the productivity jump. Although automated platforms cost two to three times more than standalone tools, payback compresses when capacity utilization tops 80%. Smaller Asian vendors are now bundling die bond, dispense, and vision modules to court price-sensitive buyers. Consequently, automated lines are projected to capture a larger share of the LED packaging equipment market by the end of the forecast period.

The surge in automation dovetails with Industry 4.0 mandates for data traceability, predictive maintenance and remote diagnostics. European customers lean on refurbished equipment to temper capex, but North American fabs often favor new, fully connected gear to comply with traceability rules tied to government incentives. As both regions wrestle with technician shortages, self-calibrating bonders and auto-programming AOI lessen the skills hurdle. The transition is unlikely to be uniform, tier-2 assemblers may still run semi-automated workcells, whereas tier-1 display and automotive suppliers gravitate toward lights-out factories. Vendors able to offer modular upgrades can cater to both profiles, cushioning revenue volatility across business cycles.

Geography Analysis

Asia-Pacific dominated with 68.71% of LED packaging equipment market size in 2025 and is on track to register a 7.17% CAGR through 2031. China's 50% domestic-equipment quota accelerates local procurement from Naura and JT Automation, marginalizing importers unless they form joint ventures. Japan's JPY 53.5 billion (USD 355 million) subsidy inside the Rapidus scheme aligns with its push to reboot advanced packaging, presenting a fresh customer base for precision tool vendors. South Korea's Hanmi Semiconductor leveraged localized service to dethrone Shinkawa at Micron, highlighting how equipment uptime and proximity override legacy incumbency.

North America and Europe together accounted for roughly one-quarter of 2025 revenue. The LED packaging equipment market here is shaped by strict export compliance and a labor crunch. The U.S. BIS rulebook slows shipments containing U.S. ICs, prompting some vendors to redesign control boards for de-Americanization. On the upside, the CHIPS and Science Act channels grants toward domestic advanced-packaging lines, partially offsetting compliance drag. Europe shows rising interest in certified refurbished gear; TOWA's program offers 40-60% price relief but operates without a region-wide quality seal, creating financing uncertainty.

South America, the Middle East and Africa contributed less than 7% of 2025 turnover. Activity centers on assembling imported LED dice into finished lamps or signage modules. Government electrification plans occasionally seed turnkey lines, yet shortage of field engineers and spare-parts logistics hampers large-scale automation. As telco-backed smart-city pilots progress, pockets of demand may emerge for mid-range AOI-equipped lines, but volumes remain too modest to sway global supplier roadmaps.

- ASM Pacific Technology Ltd.

- Kulicke and Soffa Industries Inc.

- BE Semiconductor Industries N.V.

- Hanmi Semiconductor Co., Ltd.

- Palomar Technologies Inc.

- Shinkawa Ltd.

- Toray Engineering Co., Ltd.

- Suneast Equipment Co., Ltd.

- Besi APAC Pte. Ltd.

- ASMPT Suzhou Co., Ltd.

- F&K Delvotec Bondtechnik GmbH

- Towa Corporation

- Nordson Corporation

- DIAS Automation (Suzhou) Co., Ltd.

- Hitachi High-Tech Corporation

- Nitto Denko Corporation

- Shenzhen JT Automation Equipment Co., Ltd.

- Tronstol Technology Co., Ltd.

- Datacon Technology GmbH

- Revasum Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Supply-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technology Outlook

- 4.5 Impact of Macroeconomic Factors

- 4.6 Market Drivers

- 4.6.1 Rapid Mini-LED and Micro-LED Capacity Ramp-Up

- 4.6.2 Rising Adoption of Automotive Adaptive Headlamps

- 4.6.3 Line Yield Gains Via Inline AOI/AXI Integration

- 4.6.4 Demand for Low-Temperature Sintered Silver Die-Attach Pastes

- 4.6.5 Government Subsidies for Domestic Packaging Lines in Asia-Pacific

- 4.6.6 Equipment Refurbishment Market Formalisation in Europe

- 4.7 Market Restraints

- 4.7.1 Trade-Compliance Audits on US Export-Controlled Wire-Bonders

- 4.7.2 Thermal Run-Away Risks in High-Power CSP Lines

- 4.7.3 Skilled Operator Shortage for Sub-10 µm Flip-Chip Bonding

- 4.7.4 CAPEX Freezes at Tier-2 Display Makers

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Die Bonding Equipment

- 5.1.2 Wire Bonding Equipment

- 5.1.3 Encapsulation Equipment

- 5.1.4 Automated Packaging Systems

- 5.2 By Package Type

- 5.2.1 SMD LED Packaging

- 5.2.2 COB Packaging

- 5.2.3 CSP LED Packaging

- 5.3 By LED Application

- 5.3.1 General Lighting

- 5.3.2 Displays

- 5.3.3 Automotive Lighting

- 5.3.4 Consumer Electronics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 Southeast Asia

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASM Pacific Technology Ltd.

- 6.4.2 Kulicke and Soffa Industries Inc.

- 6.4.3 BE Semiconductor Industries N.V.

- 6.4.4 Hanmi Semiconductor Co., Ltd.

- 6.4.5 Palomar Technologies Inc.

- 6.4.6 Shinkawa Ltd.

- 6.4.7 Toray Engineering Co., Ltd.

- 6.4.8 Suneast Equipment Co., Ltd.

- 6.4.9 Besi APAC Pte. Ltd.

- 6.4.10 ASMPT Suzhou Co., Ltd.

- 6.4.11 F&K Delvotec Bondtechnik GmbH

- 6.4.12 Towa Corporation

- 6.4.13 Nordson Corporation

- 6.4.14 DIAS Automation (Suzhou) Co., Ltd.

- 6.4.15 Hitachi High-Tech Corporation

- 6.4.16 Nitto Denko Corporation

- 6.4.17 Shenzhen JT Automation Equipment Co., Ltd.

- 6.4.18 Tronstol Technology Co., Ltd.

- 6.4.19 Datacon Technology GmbH

- 6.4.20 Revasum Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

LED構裝市場規模、佔有率和趨勢分析報告:按材料、封裝類型、應用、地區和細分市場分類(2026-2033年)

LED構裝市場規模、佔有率和趨勢分析報告:按材料、封裝類型、應用、地區和細分市場分類(2026-2033年) LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中國LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中國LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)北美LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 晶片級封裝LED市場:依LED類型、應用和最終用途分類-2026-2032年全球市場預測LED構裝市場:依封裝類型、基板材料、晶片類型和應用分類-全球預測,2026-2032年LED導線架市場按產品、材質、電鍍類型、導線架類型和最終用戶分類 - 全球預測 2026-2032

晶片級封裝LED市場:依LED類型、應用和最終用途分類-2026-2032年全球市場預測LED構裝市場:依封裝類型、基板材料、晶片類型和應用分類-全球預測,2026-2032年LED導線架市場按產品、材質、電鍍類型、導線架類型和最終用戶分類 - 全球預測 2026-2032 LED構裝市場規模、佔有率及成長分析(按應用、技術、最終用途及地區分類)-2026-2033年產業預測

LED構裝市場規模、佔有率及成長分析(按應用、技術、最終用途及地區分類)-2026-2033年產業預測