|

市場調查報告書

商品編碼

2066384

北美LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)North America LED Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

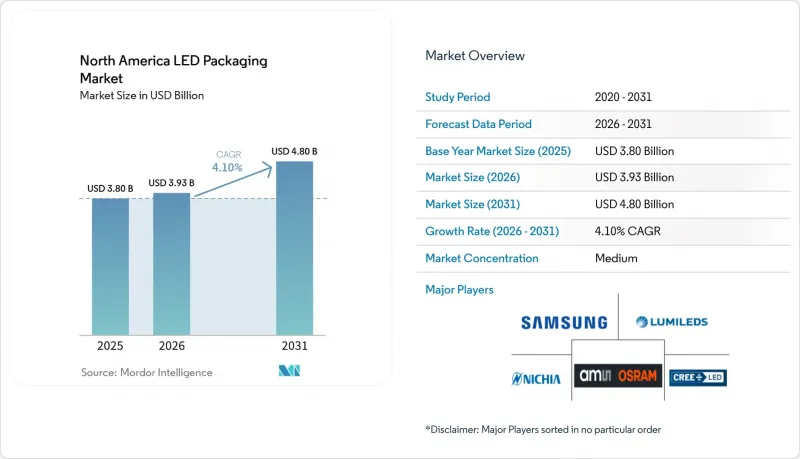

根據 Mordor Intelligence 預測,北美LED構裝市場規模將從 2025 年的 38 億美元和 2026 年的 39.3 億美元成長到 2031 年的 48 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.10%。

本報告按封裝類型(SMD、COB、CSP、覆晶、DIP 等)、功率等級(低、中、高、超高)、發光類型(可見光、紅外線、紫外線)、材料化學(基板、封裝材料、封裝、磷光體)、應用領域(通用照明、汽車、顯示器等)和國家/地區進行細分。市場預測以美元(USD)為單位。

北美LED構裝市場趨勢與洞察

迷你LED背光燈需求激增

在2026年1月舉行的消費性電子展(CES)上,電視和顯示器品牌宣布將推出超過2,000萬台mini-LED背光顯示器。這凸顯了高密度LED矩陣的快速普及,這種矩陣可在每個顯示器的面板內實現超過1萬個局部調光區域。由於mini-LED採用間距小於0.5毫米、尺寸僅100-200微米的微型晶片,北美封裝製造商正在升級其設備,採用精度低於10微米的貼片系統,從而實現高吞吐量的鍵合。據Bridgelux稱,隨著顯示整合製造商向晶片級設計轉型,其CSP2727系列產品目前約佔北美CSP出貨量的30%。將於2025年1月生效的能源之星9.0法規將對65吋以上螢幕的開啟功耗提出更嚴格的要求。然而,由於迷你LED能夠將未使用區域的亮度降低99%以上,製造商可以在不犧牲峰值亮度的情況下保持合規性。這種架構轉變也有利於板載晶片(COB)模組,使其無需導線架,封裝高度可降低至1毫米以下,並改善散熱性能。隨著元件數量的快速成長,後端光學校準正成為瓶頸,因此,能夠在60秒內完成整個背光面板測試的自動化光度測試站越來越受到關注。

汽車頭燈向矩陣式LED過渡

2022年,自適應遠光燈系統( 自我調整 Driving Beam System)獲得美國監管機構FMVSS 108標準的批准,這促使汽車製造商迅速加快矩陣式頭燈的普及。特斯拉在其2025款Model Y車型中採用了矩陣式頭燈,而Rivian則在2024年8月透過OTA空中升級為其R1T和R1S卡車啟用了該功能。 ams OSRAM在2026年國際消費電子展(CES)上發布的EVIYOS 3.0晶片擁有25,600個獨立可控像素,能夠生成高解析度的“光毯”,根據交通狀況自動調節並將導航指示投射到路面上。這些模組需要採用能夠承受125 度C以上結溫的覆晶封裝,以及能夠在-40 度C至+105 度C的溫度範圍內保持±200K色溫的光學塗層。將於2024年發布的ISO 26262功能安全標準強制要求採用冗餘晶片架構和即時故障檢測,將使組件成本增加高達20%,但能確保故障無損運作。隨著加拿大和墨西哥監管協調工作的推進,一級照明供應商正將組裝轉移到北美,以最大限度地降低物流成本和外匯風險。

價格下跌給毛利率帶來了壓力。

2025年,通用中功率SMD LED的平均售價較去年同期下降8-12%。這主要是由於亞洲代工組裝運轉率超過90%,導致市場供過於求。北美廠商的毛利率因此下降了200-300個基點,迫使它們整合製造地並加速折舊免稅額老舊的貼片設備。雖然向CSP和覆晶設計的轉變將降低導線架和塑膠封裝的成本,但每台售價高達200萬至300萬美元的新型晶片貼裝機對於許多區域性專業廠商來說仍然難以承受。業內傳聞稱,未來18個月內可能會出現一波新的併購和資產出售浪潮,尤其是在那些缺乏專有磷光體或光學塗層以維持高溢價的公司中。

細分市場分析

表面黏著型元件預計在2025年佔總銷售額的44.28%,能夠無縫融入現有貼片組裝線的龐大部署系統。然而,晶片級封裝(CSP)預計將以4.68%的複合年成長率(CAGR)超越所有競爭產品,直至2031年。北美CSP LED構裝市場正受益於其30-40%的低熱阻優勢,這使得戶外照明製造商無需依賴主動散熱即可提高驅動電流。事實上,洛杉磯和多倫多的路燈設計師報告稱,透過改用CSP基板(可減少反射器深度),其照明燈具的重量最多可減輕15%。無需焊線的覆晶形式在汽車頭燈領域也越來越受歡迎,該領域需要1000 cd/mm²的亮度以及微秒調光。同時,隨著自動化表面黏著技術線的普及,傳統雙列直插式 (DIL) 和通孔封裝的出貨佔有率已縮減至少於 3%。

第二代CSP進一步整合了暫態電壓抑制二極體和封裝整合熱敏電阻器,為OEM廠商提供即時健康數據,用於預測性維護。此功能支援「照明即服務」合約的趨勢,照明供應商可保證多年流明輸出。覆晶製造商透過將光波導層壓在焊料凸塊上,簡化了自適應驅動光束像素的組裝,這對於追求最高安全等級的汽車製造商至關重要。同時,板載晶片(COB)供應商憑藉其在鋁基基板均勻分佈100W熱量而不形成熱點的能力,繼續主導著園藝和體育場館照明市場,儘管均熱板混合產品正逐漸蠶食這一細分市場。

功率介於 0.5 瓦至 1 瓦的中功率LED 預計在 2025 年將佔總銷量的 39.18%,並且仍然是改裝燈泡和獎杯中實現「能源之星」每美元流明目標的最經濟有效的方式。功率介於 1 瓦至 3 瓦的高功率LED 預計將以 4.99% 的複合年成長率成長,這主要得益於矩陣式頭燈陣列對高通量、高分檔晶片的需求。在北美LED構裝市場,隨著電動車 (EV) 平台將更多電力預算分配給照明,與傳統內燃機汽車相比,高功率裝置的佔有率預計將會上升。在穿戴式裝置和儀表板圖示等對電池續航時間優先於亮度的應用領域,低功率指示組件仍有需求。同時,功率超過 3 瓦的超高高功率封裝正被引入體育場館泛光照明和園藝種植架等領域。

熱設計成敗是決定成敗的關鍵因素。高功率晶片需要使用均熱板基板或燒結銅基板來維持結溫低於 110 度C ,但這些材料會使材料清單成本增加 20-30%。如果模組在 30,000 小時的實際運作週期內超過 L70,則未能解決散熱問題的供應商將面臨保固索賠的風險。一級供應商越來越要求在採購過程中提交熱電阻報告,這項變更不利於通用型中功率產品線的發展,但卻有助於提高高度專業化的高功率供應商的客戶留存率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

- 市場促進因素

- Mini-LED背光燈需求激增

- 汽車頭燈向矩陣式LED過渡

- 美國《晶片與整合產品法案》(CHIPS Act) 對國內LED供應鏈的優惠待遇

- CSP技術在高流明戶外照明燈具中的快速普及

- 將UV-C LED整合到HVAC系統中以控制病原體

- 微型LED在AR/VR穿戴裝置的新應用

- 市場限制因素

- 價格下跌給毛利率帶來了壓力。

- 3. W 封裝以外的溫度控管挑戰。

- 亞太地區對合約包裝的依賴

- 稀土元素磷光體的供應風險

第5章 市場規模與成長預測

- 按包裝類型

- 表面黏著型元件(SMD)

- 板載晶片(COB)

- 晶片級封裝(CSP)

- 覆晶LED構裝

- 雙列直插封裝(DIP/通孔)

- 其他,包結構

- 按電力等級

- 低功率(小於0.5瓦)

- 中功率(0.5–1 瓦)

- 高功率(1-3瓦)

- 高功率(3瓦或以上)

- 按發光類型

- 可見光LED構裝

- 紅外線LED構裝

- 紫外線LED構裝

- 材料化學

- 基材

- 封裝

- 黏接/晶片貼裝

- 磷光體/塗層

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 家用電子產品

- 工業和專業應用

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Cree LED, Inc.

- Samsung Electronics Co., Ltd.

- ams-OSRAM AG

- Lumileds Holding BV

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Lextar Electronics Corp.

- Everlight Electronics Co., Ltd.

- Dominant Opto Technologies Sdn Bhd

- Stanley Electric Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Lite-On Technology Corporation

- NationStar Optoelectronics Co., Ltd.

- Rohinni LLC

- Brightek Optoelectronic Co., Ltd.

- Loyal Group(Refond)

- Genesis Photonics Inc.

- Lumens Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america lED packaging market size is projected to expand from USD 3.80 billion in 2025 and USD 3.93 billion in 2026 to USD 4.80 billion by 2031, registering a CAGR of 4.10% between 2026 to 2031.

This report is Segmented by Packaging Architecture (SMD, COB, CSP, Flip-Chip, DIP, and More), Power Class (Low, Mid, High, and Ultra-High), Emission Type (Visible, Infrared, and Ultraviolet), Material Chemistry (Substrates, Encapsulation, Bonding, and Phosphors), Application (General Lighting, Automotive, Display, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America LED Packaging Market Trends and Insights

Surge In Mini-LED Backlighting Demand

Television and monitor brands unveiled more than 20 million mini-LED backlit units at the January 2026 Consumer Electronics Show, underscoring rapid adoption of dense LED matrices that deliver in-panel local dimming exceeding 10,000 zones per display. Mini-LEDs use dies as small as 100-200 µm placed on pitches below 0.5 mm, so North American packagers are re-tooling with sub-10 µm-accuracy pick-and-place systems capable of high-throughput bonding. Bridgelux reported its CSP2727 family now accounts for roughly 30% of the company's continental CSP shipments as display integrators migrate to chip-scale designs. Energy Star 9.0 limits, effective January 2025, tightened on-mode power for screens larger than 65 inches, and mini-LED's ability to dim unused zones by more than 99% helps manufacturers stay compliant without lowering peak brightness. The architectural shift also favors chip-on-board (COB) modules that eliminate lead frames, reduce package height under 1 mm, and improve thermal spreading. As component counts balloon, backend optical calibration emerges as a bottleneck, spurring interest in automated photometric testing stations that can process entire backlight panels in under 60 seconds.

Automotive Headlamp Shift To Matrix LED

Adaptive-driving-beam systems gained U.S. regulatory clearance under FMVSS 108 in 2022, and original equipment manufacturers quickly accelerated matrix headlamp rollouts. Tesla integrated matrix headlights into the 2025 Model Y, and Rivian activated the feature via over-the-air update in August 2024 for its R1T and R1S trucks. ams OSRAM's EVIYOS 3.0 chip, launched at CES 2026, packs 25,600 individually addressable pixels to create high-resolution light carpets that adapt to traffic and project navigation prompts onto pavement. These modules require flip-chip packages rated for junction temperatures above 125 °C, as well as optical coatings that hold color temperature within +-200 K from -40 °C to +105 °C. ISO 26262 functional-safety rules published in 2024 force redundant die architectures and real-time fault detection, adding up to 20% in bill-of-material cost but ensuring fail-silent behavior. As regulations harmonize across Canada and Mexico, tier-one lighting suppliers are localizing assembly in North America to minimize logistics overhead and currency-exchange exposure.

Price Erosion Pressuring Gross Margins

Average selling prices for commodity mid-power SMD LEDs fell 8-12% year-over-year in 2025 as Asian contract assemblers ran at utilization rates above 90% and flooded the market with excess output. North American players saw gross margins compress by 200-300 basis points, forcing manufacturing consolidation and accelerated depreciation of legacy pick-and-place assets. Migrating to CSP and flip-chip designs partially offsets the squeeze because lead-frame and plastic encapsulation costs disappear, but new die-attach tools priced at USD 2-3 million each are beyond reach for many regional specialists. Industry chatter suggests a new wave of mergers and asset sales is likely over the next 18 months, especially among firms lacking proprietary phosphors or optical coatings that can defend premium ASPs.

Other drivers and restraints analyzed in the detailed report include:

- U.S. CHIPS Act Incentives For Domestic LED Supply Chain

- Rapid Adoption Of CSP In High-Lumen Outdoor Fixtures

- Thermal-Management Challenges Beyond 3 W Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount devices held 44.28% of 2025 revenue because they drop seamlessly into the vast installed base of pick-and-place assembly lines, yet chip-scale packages are forecast to outpace all rivals at a 4.68% CAGR through 2031. The North America LED Packaging market size for CSPs benefits from a 30-40% lower thermal resistance that lets outdoor fixture makers push drive currents without resorting to active cooling. In practice, streetscape engineers in Los Angeles and Toronto report fixture weight declines of up to 15% after switching to CSP boards that shrink reflector depth. Wire-bond-free flip-chip formats are also ascending in automotive headlamps where designers need 1,000 cd/mm2 intensity and microsecond dimming. Meanwhile, legacy dual-in-line and through-hole packages have retreated to fewer than 3% of shipments as automated surface-mount lines become universal.

Second-generation CSPs further integrate transient-voltage suppression diodes and on-package thermistors, giving OEMs real-time health data for predictive maintenance. This functionality supports the trend toward lighting-as-a-service contracts in which fixture vendors guarantee lumen output over multi-year periods. Flip-chip makers are layering optical waveguides atop solder bumps to simplify assembly of adaptive-driving-beam pixels, a feature essential for automakers chasing top safety ratings. Chip-on-board suppliers, meanwhile, continue to dominate horticultural and stadium lighting thanks to their ability to spread 100 W across aluminum substrates without hotspot formation, though vapor-chamber hybrids are beginning to nibble at that niche.

Mid-power LEDs between 0.5 W and 1 W controlled 39.18% of 2025 revenue as they remain the cheapest path to meet Energy Star lumen-per-dollar targets in retrofit bulbs and troffers. The high-power 1-3 W class is projected to chart a 4.99% CAGR, fueled by matrix headlamp arrays that need tightly binned, high-flux dies. The North America LED Packaging market share for high-power devices is set to climb as electric-vehicle platforms allocate larger electrical budgets to lighting than their internal-combustion predecessors. Low-power indicator parts hang on in wearables and dashboard icons where battery life trumps intensity, whereas ultra-high-power packages above 3 W are entering stadium floodlights and horticulture grow racks.

Thermal budgets separate winners from laggards. High-power dies demand vapor-chamber substrates or sintered copper bases to maintain junctions below 110 °C, yet those materials add 20-30% to BOM. Vendors that cannot solve heat extraction risk warranty claims when real-world duty cycles push modules past L70 in under 30,000 h. Tier-ones increasingly mandate thermal-impedance reports during sourcing, a shift that disadvantages commoditized mid-power lines but enhances the stickiness of specialized high-power suppliers.

List of Companies Covered in this Report:

- Nichia Corporation

- Cree LED, Inc.

- Samsung Electronics Co., Ltd.

- ams-OSRAM AG

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Lextar Electronics Corp.

- Everlight Electronics Co., Ltd.

- Dominant Opto Technologies Sdn Bhd

- Stanley Electric Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Lite-On Technology Corporation

- NationStar Optoelectronics Co., Ltd.

- Rohinni LLC

- Brightek Optoelectronic Co., Ltd.

- Loyal Group (Refond)

- Genesis Photonics Inc.

- Lumens Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Impact of Macroeconomic Factors

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Market Drivers

- 4.7.1 Surge in Mini-LED Backlighting Demand

- 4.7.2 Automotive Headlamp Shift to Matrix LED

- 4.7.3 U.S. CHIPS Act Incentives for Domestic LED Supply Chain

- 4.7.4 Rapid Adoption of CSP in High-Lumen Outdoor Fixtures

- 4.7.5 Integration of UV-C LEDs in HVAC for Pathogen Control

- 4.7.6 Emerging Micro-LED Use in AR/VR Wearables

- 4.8 Market Restraints

- 4.8.1 Price Erosion Pressuring Gross Margins

- 4.8.2 Thermal-Management Challenges Beyond 3 W Packages

- 4.8.3 Dependence on Asia-Pacific Contract Packaging

- 4.8.4 Supply Risk of Rare-Earth Phosphors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Architecture

- 5.1.1 Surface Mount Device (SMD)

- 5.1.2 Chip-on-Board (COB)

- 5.1.3 Chip Scale Package (CSP)

- 5.1.4 Flip-Chip LED Packages

- 5.1.5 Dual In-line Package (DIP / Through-hole)

- 5.1.6 Others, Packaging Architecture

- 5.2 By Power Class

- 5.2.1 Low Power (Less Than 0.5 W)

- 5.2.2 Mid Power (0.5 to 1 W)

- 5.2.3 High Power (1 to 3 W)

- 5.2.4 Ultra-High Power (More Than 3 W)

- 5.3 By Emission Type

- 5.3.1 Visible LED Packages

- 5.3.2 Infrared LED Packages

- 5.3.3 Ultraviolet LED Packages

- 5.4 By Material Chemistry

- 5.4.1 Substrates

- 5.4.2 Encapsulation

- 5.4.3 Bonding / Die-Attach

- 5.4.4 Phosphors / Coatings

- 5.5 By Application

- 5.5.1 General Lighting

- 5.5.2 Automotive Lighting

- 5.5.3 Display and Backlighting

- 5.5.4 Consumer Electronics

- 5.5.5 Industrial and Specialty

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Cree LED, Inc.

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 ams-OSRAM AG

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Seoul Semiconductor Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Epistar Corporation

- 6.4.9 Lextar Electronics Corp.

- 6.4.10 Everlight Electronics Co., Ltd.

- 6.4.11 Dominant Opto Technologies Sdn Bhd

- 6.4.12 Stanley Electric Co., Ltd.

- 6.4.13 Toyoda Gosei Co., Ltd.

- 6.4.14 Lite-On Technology Corporation

- 6.4.15 NationStar Optoelectronics Co., Ltd.

- 6.4.16 Rohinni LLC

- 6.4.17 Brightek Optoelectronic Co., Ltd.

- 6.4.18 Loyal Group (Refond)

- 6.4.19 Genesis Photonics Inc.

- 6.4.20 Lumens Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

LED構裝市場規模、佔有率和趨勢分析報告:按材料、封裝類型、應用、地區和細分市場分類(2026-2033年)

LED構裝市場規模、佔有率和趨勢分析報告:按材料、封裝類型、應用、地區和細分市場分類(2026-2033年) LED構裝設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中國LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

LED構裝設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中國LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 晶片級封裝LED市場:依LED類型、應用和最終用途分類-2026-2032年全球市場預測LED構裝市場:依封裝類型、基板材料、晶片類型和應用分類-全球預測,2026-2032年LED導線架市場按產品、材質、電鍍類型、導線架類型和最終用戶分類 - 全球預測 2026-2032

晶片級封裝LED市場:依LED類型、應用和最終用途分類-2026-2032年全球市場預測LED構裝市場:依封裝類型、基板材料、晶片類型和應用分類-全球預測,2026-2032年LED導線架市場按產品、材質、電鍍類型、導線架類型和最終用戶分類 - 全球預測 2026-2032 LED構裝市場規模、佔有率及成長分析(按應用、技術、最終用途及地區分類)-2026-2033年產業預測

LED構裝市場規模、佔有率及成長分析(按應用、技術、最終用途及地區分類)-2026-2033年產業預測