|

市場調查報告書

商品編碼

2065585

歐洲遊戲GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Europe Gaming GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

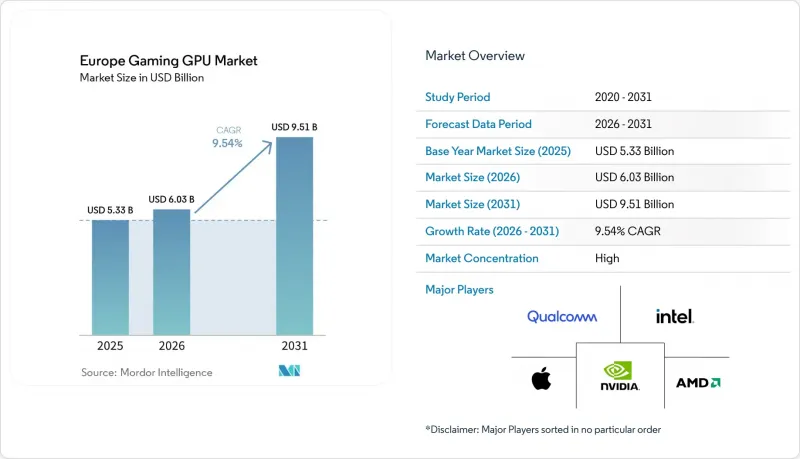

根據 Mordor Intelligence 預測,歐洲遊戲 GPU 市場規模預計將在 2025 年達到 53.3 億美元,2026 年達到 60.3 億美元,到 2031 年達到 95.1 億美元,2026 年至 2031 年的複合年成長率為 9.54%。

本報告按GPU類型(獨立GPU和整合GPU)、裝置類型(遊戲桌上型電腦、遊戲筆記型電腦、智慧型手機和平板電腦(行動遊戲))、最終用戶類型(休閒玩家、發燒友和專業玩家)、記憶體類型(GDDR6、GDDR6X、傳統顯存、統一記憶體)以及國家進行細分。市場預測以美元計價。

歐洲遊戲GPU市場的趨勢與洞察

電子競技和競技電腦遊戲的參與者人數不斷成長。

歐洲大規模的玩家群體支撐著對競技遊戲的強勁需求,並持續推動高效能硬體的消費。根據歐洲電子遊戲協會 (Video Games Europe) 和歐洲遊戲開發者聯盟 (European Games Developers Federation) 的數據顯示,到 2024 年,6 至 64 歲的歐洲人群中將有 54% 的人會玩電子遊戲,這全部區域提供了廣泛的目標硬體市場。這種廣泛的參與度正在促使遊戲模式從休閒娛樂轉向更注重性能的專業競技,刷新率、響應速度和影像穩定性等因素的重要性日益凸顯。預計到 2025 年,德國遊戲硬體及配件市場將成長 12%,達到 34 億歐元(約 37.1 億美元)。這表明,即使在遊戲成本高昂的環境下,玩家仍然願意在遊戲設備上投入資金。遊戲 PC 配件市場成長 13%,達到 13.7 億歐元(約 14.9 億美元),顯示該地區最重要的硬體市場之一對遊戲組件的需求仍然強勁。這意味著歐洲遊戲 GPU 市場的發展動力仍然來自於對效能的持續升級,而不是一次性購買。

對即時射線追蹤和人工智慧影像放大技術的需求

在歐洲遊戲GPU市場,AI超採樣不再是可選的高級功能,而是標準的購買因素。 NVIDIA表示,隨GeForce RTX 5000系列顯示卡推出的DLSS 4技術,到2026年5月將支援超過980款遊戲和應用程式。 AMD也在2025年2月發表Radeon RX 9000系列顯示卡與RDNA 4架構時,將AI輔助渲染定位為核心功能,並搭載了FSR 4技術。 NVIDIA進一步指出,GeForce RTX 50系列顯示卡的「多幀生成」功能,在支援的工作負載下,可將有效幀輸出提升至8倍。這些技術正促使更多消費者尋求能夠在長時間內保持高畫質設定的顯示卡,而不僅僅是滿足基本的1080p性能要求。這種轉變提高了歐洲遊戲GPU市場廠商必須達到的最低規格標準。

遊戲顯示卡和系統的初始成本很高。

在目前的升級週期中,對於歐洲遊戲顯示卡市場的許多買家來說,前期投入成本仍然是一筆不小的負擔。 AMD計劃在2025年推出售價549美元的Radeon RX 9070和售價599美元的RX 9070 XT,而英特爾則計劃在2024年底推出售價249美元的Arc B580。即使不考慮稅費、合作夥伴佣金和系統整體成本,這些價格也使得當前一代硬體對於普通家庭來說遠非衝動消費之選。這種價格壓力正在縮小那些購買擁有更大顯存容量和射線追蹤性能的高階產品的活躍用戶群體,即便這些產品的長期性能價值顯而易見。一些用戶也選擇延長現有系統的使用壽命或訂閱串流遊戲服務,而不是直接升級。因此,發燒友的購買速度仍高於一般用戶,使得市場支出比銷售更強勁。

細分市場分析

預計到2025年,獨立顯示卡將佔據歐洲遊戲GPU市場74.44%的佔有率,並在2031年之前以9.90%的複合年成長率持續成長。專用顯示卡硬體仍然扮演著核心角色,因為遊戲效能仍然依賴持續的運算能力、更大的散熱空間以及對高要求視覺工作負載的直接支援。 NVIDIA的DLSS 4技術被應用於超過980款遊戲和應用程式,這充分證明了為何功能豐富的獨立顯示卡仍然擁有最佳性能。 AMD在2025年推出的Radeon RX 9000系列顯示卡進一步鞏固了其市場地位,該系列顯示卡採用RDNA 4架構、配備16GB GDDR6顯存,並支援FSR 4技術,可滿足當前世代遊戲的需求。從實際角度來看,歐洲遊戲GPU市場的最大佔有率仍然由專為遊戲設計的顯示卡佔據,而非那些用於整個系統的共用顯示卡。

整合式顯示卡仍佔據剩餘市場佔有率的主導地位,在休閒遊戲、輕薄裝置和雲端遊戲網路基地台發揮重要作用。英特爾推出Arc B系列顯示卡表明,該公司有意繼續在成本績效的圖形領域保持市場佔有率,儘管目前最強勁的遊戲需求仍集中在獨立顯示卡領域。 NVIDIA和德國電信的雲端服務也降低了輕度遊戲場景對高效能本地顯示卡的需求,從而維持了整合式顯示卡和混合顯示卡配置在低階市場的有效性。然而,在歐洲遊戲顯示卡產業,獨立顯示卡(其高階遊戲功能發展最為迅速)仍佔據著大部分營收和產品研發的重點。

2025年,遊戲桌上型電腦將佔據歐洲遊戲GPU市場44.31%的佔有率,其中塔式桌上型電腦仍是最大的裝置類別。其主導地位源自於其高度的升級柔軟性、卓越的散熱性能以及無需更換整個系統即可單獨更換顯示卡的特性。在發燒友主導的市場中,桌上型電腦仍然是進行GPU逐步升級而非徹底更換硬體的最佳選擇。 2025年德國遊戲硬體及配件市場的成長也印證了這一趨勢,因為德國作為該地區最重要的遊戲硬體市場之一,其組件支出仍然強勁。因此,儘管其他設備類型有所擴張,歐洲遊戲GPU市場仍與桌上型電腦組件的需求緊密相關。

預計到2031年,遊戲筆記型電腦的複合年成長率將達到10.12%,成為歐洲遊戲GPU市場成長最快的裝置類型。華碩在2026年發表了面向北歐市場的Zephyrus G14和G16系統,搭載最高RTX 5080和RTX 5090筆記型電腦GPU,凸顯了這一趨勢。此外,NVIDIA對GeForce NOW的Blackwell架構升級,使得即使在本地GPU效能有限的裝置上也能實現高解析度串流媒體播放,從而提升了可攜式系統的吸引力。同時,智慧型手機和平板電腦也作為第三種途徑進入市場,5G雲端遊戲服務讓行動用戶無需改變設備外形規格。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 電子競技和競技電腦遊戲的參與者人數不斷成長。

- 對即時射線追蹤和人工智慧影像放大技術的需求

- 遊戲筆記型電腦和可攜式高效能PC的廣泛普及。

- 手機遊戲的獲利模式正朝著畫面品質更高的遊戲方向發展。

- 5G獨立組網雲端遊戲套餐正在擴大高階GPU的應用程式。

- 16 GB 顯存的預期讓我重新考慮是否要升級。

- 市場限制因素

- 遊戲顯示卡和系統的初始成本很高。

- 由於部署基礎設施成熟,更換週期得以延長。

- GDDR6 和 GDDR6X 的供應緊張推高了中階GPU 的價格。

- 歐盟能源和待機功耗合規壓力對高TDP硬體造成影響

- 產業價值鏈分析

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按GPU類型

- 獨立顯示卡

- 整合顯示卡

- 依設備類型

- 遊戲桌上型電腦

- 遊戲筆記型電腦

- 智慧型手機和平板電腦(手機遊戲)

- 最終用戶

- 休閒玩家

- 業餘玩家和職業玩家

- 按記憶體類型

- GDDR6

- GDDR6X

- 傳統圖形內存

- 統一記憶體

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Incorporated

- Apple Inc.

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- GIGA-BYTE Technology Co., Ltd.

- Acer Inc.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- Razer Inc.

- SAPPHIRE Technology Limited

- ASRock Inc.

- ZOTAC Technology Limited

- Palit Microsystems Ltd.

- TUL Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe gaming GPU market size is projected to be USD 5.33 billion in 2025, USD 6.03 billion in 2026, and reach USD 9.51 billion by 2031, growing at a CAGR of 9.54% from 2026 to 2031.

This report is Segmented by GPU Type (Discrete GPUs, and Integrated GPUs), Device Type (Gaming Desktops, Gaming Laptops, and Smartphones and Tablets (Mobile Gaming)), End-User Type (Casual Gamers, and Enthusiast and Professional Gamers), Memory Type (GDDR6, GDDR6X, Legacy Graphics Memory, and Unified Memory), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe Gaming GPU Market Trends and Insights

Rising Esports And Competitive PC Gaming Participation

Competitive gaming demand in Europe rests on a very large player base that continues to feed more performance-focused hardware purchases over time. Video Games Europe and the European Games Developer Federation stated that 54% of Europeans aged 6-64 played video games in 2024, which kept the addressable hardware base broad across the region. That broad participation supports a steady funnel from casual play into organized and performance-led gaming, where refresh rate, responsiveness, and visual stability matter more. Germany's games hardware and accessories segment grew 12% in 2025 to EUR 3.40 billion (USD 3.71 billion), showing that players were still willing to spend on gaming equipment even in a higher-cost environment. Gaming PC accessories rose 13% to EUR 1.37 billion (USD 1.49 billion), which points to healthy component demand in one of the region's most important hardware markets. This keeps the Europe gaming GPU market tied to repeated performance-led upgrades rather than to a single purchase cycle.

Demand for Real-Time Ray Tracing and AI-Upscaling

AI-upscaling is now a standard purchase factor in the Europe gaming GPU market rather than an optional premium feature. NVIDIA said DLSS 4, introduced with the GeForce RTX 5000 generation, had reached more than 980 games and applications by May 2026. AMD also positioned AI-assisted rendering as a core feature when it launched the Radeon RX 9000 series and RDNA 4 architecture with FSR 4 in February 2025.NVIDIA further stated that Multi Frame Generation on GeForce RTX 50 Series hardware can increase effective frame output by up to 8x in supported workloads. These technologies are pushing more buyers to look beyond basic 1080p performance and target cards that can sustain higher visual settings over a longer ownership period. That change is lifting the baseline specification that vendors must meet across the Europe gaming GPU market.

High Upfront Cost of Gaming GPUs and Systems

The current upgrade cycle still carries a high upfront cost burden for many buyers in the Europe gaming GPU market. AMD launched the Radeon RX 9070 at USD 549 and the RX 9070 XT at USD 599 in 2025, while Intel positioned the Arc B580 at USD 249 in late 2024. Even before taxes, partner premiums, and the cost of a full system are added, those levels keep current-generation hardware far from impulse-purchase territory for mainstream households. That pressure narrows the active buyer base for higher-VRAM and higher-ray-tracing tiers, even when long-term performance value is clear. It also pushes some users toward longer retention of existing systems or toward streamed gaming services instead of direct replacement. The result is a market where spending remains healthier than unit turnover because enthusiasts continue to buy sooner than mass-market users.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Gaming Laptops and Portable High-Performance PCs

- Mobile Gaming Monetization Moving Toward Higher-Fidelity Titles

- Mature Installed Base Lengthening Replacement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs commanded a 74.44% share of the Europe gaming GPU market in 2025 and are projected to expand at a 9.90% CAGR through 2031. Dedicated graphics hardware remains central because gaming performance still depends on sustained compute, stronger thermal headroom, and direct support for advanced visual workloads. NVIDIA's DLSS 4 footprint across more than 980 games and applications shows why feature-rich discrete cards continue to hold the strongest performance position. AMD reinforced that position in 2025 when it launched the Radeon RX 9000 series with RDNA 4, 16 GB GDDR6 configurations, and FSR 4 support for current-generation gaming. In practical terms, the largest slice of the Europe gaming GPU market continues to sit with cards designed for direct gaming load rather than for shared system use.

Integrated GPUs account for the remaining segment share and remain more relevant for casual play, thin devices, and cloud gaming access points. Intel's Arc B-series launch showed that the company still wants a role in value-oriented graphics, even though the strongest gaming demand remains concentrated in discrete categories. Cloud services from NVIDIA and Deutsche Telekom also reduce the need for a powerful local GPU in lighter gaming scenarios, which helps integrated and hybrid setups stay viable at the lower end. Even so, the Europe gaming GPU industry still draws most of its revenue and product attention from discrete silicon because premium gaming features are advancing fastest there.

Gaming desktops held 44.31% share of the Europe gaming GPU market size in 2025, which kept towers as the largest device category. Their lead reflects stronger upgrade flexibility, better cooling, and the ability to replace a graphics card without changing the full system. In enthusiast-led markets, desktops remain the clearest route to stepwise GPU upgrades rather than full hardware replacement. Germany's 2025 growth in gaming hardware and accessories supports that pattern because component spending remained active in one of the region's most important gaming hardware markets. That keeps the Europe gaming GPU market closely linked to desktop component demand, even as other device types expand.

Gaming laptops are projected to grow at a 10.12% CAGR through 2031, making them the fastest-growing device type in the Europe gaming GPU market. ASUS highlighted this shift in 2026 with Zephyrus G14 and G16 systems that carried up to RTX 5080 Laptop GPU and RTX 5090 Laptop GPU options in Nordic markets. NVIDIA's GeForce NOW Blackwell upgrade also increased the appeal of portable systems by enabling high-resolution streaming on devices that do not carry the same local GPU headroom. Smartphones and tablets add a third route because 5G cloud gaming services expose mobile users to premium GPU rendering without changing the device form factor.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Incorporated

- Apple Inc.

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- GIGA-BYTE Technology Co., Ltd.

- Acer Inc.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- Razer Inc.

- SAPPHIRE Technology Limited

- ASRock Inc.

- ZOTAC Technology Limited

- Palit Microsystems Ltd.

- TUL Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Rising Esports and Competitive PC Gaming Participation

- 4.3.2 Demand for Real-Time Ray Tracing and AI-Upscaling

- 4.3.3 Rising Adoption of Gaming Laptops and Portable High-Performance PCs

- 4.3.4 Mobile Gaming Monetization Moving Toward Higher-Fidelity Titles

- 4.3.5 5G Standalone Cloud Gaming Bundles Expanding Premium GPU Exposure

- 4.3.6 16 GB VRAM Expectations Reshaping Upgrade Decisions

- 4.4 Market Restraints

- 4.4.1 High Upfront Cost of Gaming GPUs and Systems

- 4.4.2 Mature Installed Base Lengthening Replacement Cycles

- 4.4.3 GDDR6 and GDDR6X Supply Tightness Inflating Midrange GPU Prices

- 4.4.4 EU Energy and Standby Compliance Pressure on High-TDP Hardware

- 4.5 Industry Value Chain Analysis

- 4.6 Supply Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By GPU Type

- 5.1.1 Discrete GPUs

- 5.1.2 Integrated GPUs

- 5.2 By Device Type

- 5.2.1 Gaming Desktops

- 5.2.2 Gaming Laptops

- 5.2.3 Smartphones and Tablets (Mobile Gaming)

- 5.3 By End-User Type

- 5.3.1 Casual Gamers

- 5.3.2 Enthusiast and Professional Gamers

- 5.4 By Memory Type

- 5.4.1 GDDR6

- 5.4.2 GDDR6X

- 5.4.3 Legacy Graphics Memory

- 5.4.4 Unified Memory

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Incorporated

- 6.4.5 Apple Inc.

- 6.4.6 MediaTek Inc.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 ASUSTeK Computer Inc.

- 6.4.9 Micro-Star International Co., Ltd.

- 6.4.10 GIGA-BYTE Technology Co., Ltd.

- 6.4.11 Acer Inc.

- 6.4.12 Dell Technologies Inc.

- 6.4.13 HP Inc.

- 6.4.14 Lenovo Group Limited

- 6.4.15 Razer Inc.

- 6.4.16 SAPPHIRE Technology Limited

- 6.4.17 ASRock Inc.

- 6.4.18 ZOTAC Technology Limited

- 6.4.19 Palit Microsystems Ltd.

- 6.4.20 TUL Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment