|

市場調查報告書

商品編碼

2065567

ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Enterprise Resource Planning Integration Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

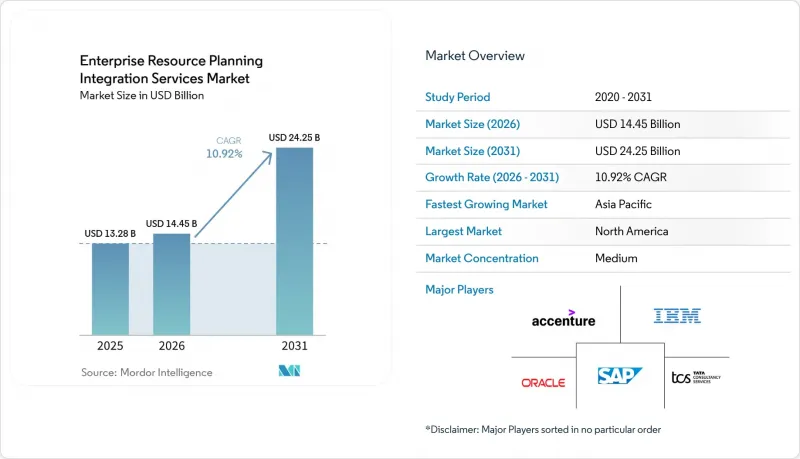

根據 Mordor Intelligence 預測,ERP 整合服務市場規模預計將在 2025 年達到 132.8 億美元,2026 年達到 144.5 億美元,到 2031 年達到 242.5 億美元,2026 年至 2031 年的複合年成長率為 10.92%。

本報告按服務類型(應用整合、資料整合、流程整合及其他服務)、部署模式(本地部署、雲端部署和混合部署)、企業規模(中小企業和大型企業)、產業(製造業、銀行、金融服務和保險業、零售和電子商務、醫療保健、IT和電信等)以及地區進行細分。市場預測以美元計價。

全球ERP整合服務市場趨勢與洞察

基於雲端的ERP系統的快速普及

雲端ERP的普及正將焦點從單體中間件轉向跨多個超大規模資料中心業者中心和私有資料中心的分散式整合架構。截至2026年2月,SAP Integration Suite已連接250萬個系統,其中85%連接的是非SAP應用程式。這顯示開放API閘道器的趨勢已成定局。由於微軟Azure保證SAP私有版本99.95%的服務級別,對本地高可用性叢集的需求進一步降低。根據Odoo預測,2025年83%的新ERP部署將採用雲端混合環境,反映出向訂閱經濟模式的廣泛轉變。 IBM的「RISE with SAP on Power Virtual Server」透過整合儲存、網路和備份,將遷移時間縮短了15-25%,從而縮短了第三方整合商銷售客製化連接器的時間。隨著生產工作負載遷移到公共雲端,ERP 整合服務市場正在向打包適配器、策略驅動的路由和低程式碼編配發展,以加快價值實現速度。

異質系統之間即時資料同步的需求

使用夜間批次的 ETL 流程無法滿足動態定價、即時庫存分配或即時結算的需求。到 2025 年, Oracle將摩根大通的跨境結算系統整合到 Oracle 雲端 ERP 中,消除了 160 個國家長達 24 小時的匹配延遲。從 SAP 到 Snowflake 的變更資料擷取(CDC) 串流將分析延遲從數小時縮短到數秒。一家每天處理 200 GB 感測器資料的製造商現在僅透過仲介將異常事件傳輸到其雲端 ERP,代理商可在不到一秒的時間內處理這些事件。由於即時結算方案已在 80 多個國家/地區運行,因此符合 ISO 20022 標準已成為供應商的必備條件。隨著企業重新設計其架構以適應串流數據,這些趨勢正推動 ERP 整合服務市場保持穩定成長。

客製化傳統ERP系統的複雜性。

約有 21,000 個 SAP ECC 系統(佔實施基數的 61%)尚未完成遷移,主流支援將於 2027 年 12 月終止。自訂 ABAP 程式碼和未記錄的附加元件會消耗高達一半的遷移預算,隨著截止日期的臨近,諮詢費用預計還會上漲。到 2025 年,只有 30% 的企業能夠完全運作SAP S/4HANA Cloud,而且大部分整合工作預計將在兩年內集中完成。由於待處理案例積壓不斷增加,ERP 整合服務業面臨執行風險和潛在的專案延期。

細分市場分析

到2025年,應用整合將佔總收入的34.20%,反映出ERP、CRM、供應鏈和HCM套件之間複雜連接器網路的建立。然而,隨著事件驅動架構取代夜間ETL,以及嵌入式財務用例需要受控的外部API,API管理預計將在2026年至2031年間實現15.40%的複合年成長率,成為管治堆疊中成長率最高的領域。在ERP整合服務市場,對整合REST、SOAP、EDIFACT和GraphQL多重通訊協定閘道器的需求正在加速成長,這些閘道器能夠在單一策略層下實現一致的身份驗證和速率控制。供應商現在能夠自動產生OpenAPI合約、管理版本沿襲,並透過訂閱收費實現高價值端點的貨幣化。

資料整合服務仍然是分析工作負載的核心,可將 CDC 資料流即時傳輸到 Snowflake 和 BigQuery。流程整合顧問公司利用低程式碼編排器和 RPA 技術,無需人工干預即可整合從訂單到付款的端到端工作流程。 B2B EDI 整合主要由航太和消費品行業的需求驅動,在這些行業中,ANSI X12 和 EDIFACT 仍然是合約的基礎標準。雲端整合仲介服務透過將連接器維護和安全修補程式外包給服務供應商,使企業 IT 部門擺脫了維護任務。隨著容器化微服務的日益普及,到 2031 年,API 管理將在 ERP 整合服務市場中佔據更大的佔有率。

到2025年,雲端採用將基礎設施、授權和原生整合結合的超大規模資料中心業者服務包將貢獻57.50%的收入。 IBM的「基於Power Virtual Server的SAP RISE」透過整合中間件層,將基礎設施成本降低了30%。然而,由於歐洲和亞洲的數據居住要求禁止某些記錄跨境傳輸,混合雲配置的複合年成長率高達14.00%,在所有採用方案中位居榜首。 GDPR第48條禁止未經授權的跨境資料傳輸,鼓勵跨國公司將主資料保留在本地,同時將分析資料傳送到雲端。

因此,混合拓撲結構需要安全的訊息匯流排、跨區域複製以及租戶感知加密。 IBM X-Force 的一項研究表明,到 2025 年,將有 1,600 萬台裝置感染竊取資訊的惡意軟體,而 MuleSoft Anypoint 和 Microsoft Entra Connect 經常被用作攻擊入口。調查顯示,僅有 62% 的 SAP雲端用戶遵循了建議的安全性增強措施,導致設定檔中仍保留明文金鑰。因此,整合平台必須整合符合 ISO 27001 SOC 2 II 型要求的金鑰管理和稽核日誌功能。由於主權和延遲方面的限制,與混合拓撲結構相關的 ERP 整合服務的市場佔有率預計將持續成長。

區域分析

預計到2025年,北美將佔全球收入的42.30%,這主要得益於美國和加拿大成熟的ERP環境,以及隨著新的SaaS模組的引入,持續的整合需求。人工智慧輔助工作負載,例如微軟支援語音查詢的Jupyter Notebook Copilot,正在加速受管治API的普及,並縮短用戶培訓週期。更嚴格的HIPAA處罰促使醫療保健IT預算持續投資於安全整合架構,從而緩解遷移後的速度放緩。因此,北美將繼續為ERP整合服務市場的成長做出重大貢獻。

預計到2031年,亞太地區的複合年成長率將達到14.90%,在所有地區中成長最高。預計2027年至2029年間,中國、印度、日本和韓國向SAP S/4HANA的遷移將最為集中,這與SAP ECC主流支援的終止時間相吻合。使用IBM/SAP的Power Virtual Server進行遷移,可將所需時間縮短高達25%。中國的《資料安全法》強制要求對敏感記錄進行本地複製,這將加速混合整合代理的普及。因此,隨著最後期限的臨近,與亞太地區相關的ERP整合服務的市場佔有率預計將大幅成長。

在歐洲,企業已在既有的客製化需求和GDPR合規性之間取得了平衡。第48條的跨境限制正在推動SAP Sovereign Cloud等主權雲端服務的普及。南美、中東和非洲的規模雖然仍然較小,但未來潛力巨大。巴西和沙烏地阿拉伯在政府數位化方面處於主導,而墨西哥加入美墨加協定(USMCA)正在加速跨境供應鏈整合,這需要即時ERP連接器。這種地理分散化意味著全球ERP整合服務市場正在發揮緩衝作用,抵禦區域衝擊。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基於雲端的ERP系統的快速普及

- 異質系統之間即時資料同步的需求

- API優先型數位轉型策略的興起

- iPaaS平台在中小企業中越來越受歡迎。

- 低程式碼/無程式碼整合工具的興起

- 合規要求推動受監管產業的數據整合

- 市場限制因素

- 客製化傳統ERP系統的複雜性

- 大規模整合專案總擁有成本高

- 混合環境中的資料安全管治問題

- 熟練的整合專家短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 應用整合

- 資料整合

- 過程整合

- API管理

- B2B/EDI整合

- 雲端整合經紀

- 其他

- 部署模式

- 現場

- 雲

- 混合

- 按公司規模

- 小型企業

- 大公司

- 按行業

- 製造業

- BFSI

- 零售與電子商務

- 衛生保健

- IT/通訊

- 政府/公共部門

- 能源公用事業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- IBM Corporation

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infosys Limited

- Capgemini SE

- Tata Consultancy Services Limited

- Deloitte Touche Tohmatsu Limited

- Cognizant Technology Solutions Corporation

- Wipro Limited

- HCL Technologies Limited

- MuleSoft LLC

- Boomi LP

- Celigo Inc.

- Jitterbit Inc.

- SnapLogic Inc.

- Workato Inc.

- Software AG

- Seeburger AG

- Infor Inc.

- Epicor Software Corporation

- IFS AB

第7章 市場機會與未來展望

According to Mordor Intelligence, the eRP integration services market size is projected to be USD 13.28 billion in 2025, USD 14.45 billion in 2026, and reach USD 24.25 billion by 2031, growing at a CAGR of 10.92% from 2026 to 2031.

This report is Segmented by Service Type (Application Integration, Data Integration, Process Integration, and Other Services), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (SMEs and Large Enterprises), Industry Vertical (Manufacturing, BFSI, Retail and Ecommerce, Healthcare, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Resource Planning Integration Services Market Trends and Insights

Rapid Adoption of Cloud-Based ERP Systems

Cloud ERP deployments are displacing monolithic middleware with distributed integration fabrics that span multiple hyperscalers and private data centers. SAP Integration Suite connected 2.5 million systems as of February 2026, and 85% of those links involved non-SAP applications, signaling a decisive move toward open API gateways. Microsoft Azure's 99.95% service-level commitment for SAP private editions further reduces the perceived need for on-premises high-availability clusters. Odoo reported that cloud and hybrid setups formed 83% of new ERP deployments in 2025, mirroring the broader pivot to subscription economics. IBM's RISE with SAP on Power Virtual Server shaved 15%-25% off migration timelines by bundling storage, networking, and backup, thereby tightening the window for third-party integrators to sell custom connectors. As more production workloads move to the public cloud, the ERP integration services market is evolving toward pre-packaged adapters, policy-driven routing, and low-code orchestration to shorten time-to-value.

Need for Real-Time Data Synchronization Across Heterogeneous Systems

Overnight batch ETL cannot support dynamic pricing, real-time inventory allocation, or instant payments. Oracle embedded J. P. Morgan's cross-border rails into Oracle Cloud ERP in 2025, eliminating 24-hour reconciliation delays for 160 countries. SAP-to-Snowflake Change Data Capture streams cut analytical latency from hours to seconds. Manufacturers processing 200 GB of sensor data daily now route only anomaly events to cloud ERP via sub-second brokers. More than 80 countries already operate instant-payment schemes, and ISO 20022 compliance is now table-stakes for integration vendors. These developments keep the ERP integration services market on a steady growth path as enterprises re-architect for streaming data.

Complexity of Legacy ERP Customizations

Roughly 21,000 SAP ECC installations, 61% of the installed base, remain unmigrated, with mainstream support ending in December 2027. Custom ABAP code and undocumented bolt-ons devour up to half of migration budgets, and consulting rates are set to rise as the deadline nears. Only 30% of organizations were fully live on SAP S/4HANA Cloud in 2025, indicating that the bulk of integration workloads will compress into a two-year window. As backlogs swell, the ERP integration services industry faces execution risk and potential project delays.

Other drivers and restraints analyzed in the detailed report include:

- Increasing API-First Digital Transformation Strategies

- Growing Popularity of iPaaS Platforms Among SMEs

- High Total Cost of Ownership for Large Integration Projects

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Application integration accounted for 34.20% of 2025 revenue, reflecting the entrenched web of connectors that tie ERP to CRM, supply chain, and HCM suites. Yet API management is projected to log a 15.40% CAGR over 2026-2031, the fastest within the service stack, as event-driven architectures supersede nightly ETL and embedded-finance use cases call for governed external APIs. The ERP integration services market registers accelerating demand for multi-protocol gateways that wrap REST, SOAP, EDIFACT, and GraphQL under a single policy layer, ensuring consistent authentication and rate controls. Vendors now auto-generate OpenAPI contracts, maintain version lineage, and monetize high-value endpoints through subscription billing.

Data-integration services remain core for analytical workloads, streaming CDC feeds into Snowflake and BigQuery in real time. Process-integration consultancies lean on low-code orchestrators and robotic process automation to knit end-to-end workstreams such as order-to-cash without swivel-chair tasks. B2B and EDI integration still rides demand from aerospace and consumer goods, where ANSI X12 and EDIFACT remain contractual bedrock. Cloud integration brokerage outsources connector maintenance and security patching to providers, freeing enterprise IT from upkeep. As containerized microservices proliferate, API management will command a larger share of the ERP integration services market size through 2031.

Cloud deployments accounted for 57.50% of 2025 revenue, driven by hyperscaler bundles that combine infrastructure, licenses, and native integration. IBM's RISE with SAP on Power Virtual Server posted 30% infrastructure savings by collapsing middleware layers. Yet hybrid configurations are expanding at a 14.00% CAGR, the highest among deployment options, as European and Asian data-residency mandates block certain records from leaving national borders. GDPR Article 48 forbids unsanctioned cross-border transfers, encouraging multinationals to keep master data on-premises while sending analytics to the cloud.

Hybrid topologies, therefore, require secure message buses, dual-region replication, and tenant-aware encryption. IBM X-Force cataloged 16 million devices infected by infostealer malware in 2025, with MuleSoft Anypoint and Microsoft Entra Connect often serving as breach entry points. Only 62% of surveyed SAP cloud users adhere to recommended security hardening, leaving plaintext keys in configs. Integration platforms must therefore bundle secrets management and audit logging that meet ISO 27001 and SOC 2 Type II requirements. Sovereignty and latency constraints ensure that the ERP integration services market share tied to hybrid topologies will continue to rise.

Geography Analysis

North America accounted for 42.30% of 2025 revenue, driven by mature ERP footprints in the United States and Canada that require ongoing integration as new SaaS modules roll in. AI-assisted workloads, such as Microsoft's Jupyter Notebook Copilot for voice queries, accelerate the adoption of governed APIs, shortening user-training cycles. Tougher HIPAA penalties keep healthcare IT budgets flowing toward secure integration fabrics, cushioning any post-migration slowdown. Hence, North America remains a robust contributor to the ERP integration services market size.

Asia-Pacific is projected to post a 14.90% CAGR through 2031, the fastest regional rate. Deferred SAP S/4HANA migrations in China, India, Japan, and South Korea will compress into 2027-2029 as SAP ECC leaves mainstream support. IBM and SAP's Power Virtual Server migrations reduce timelines by up to 25%. China's Data Security Law forces local replication of sensitive records, promoting hybrid integration proxies. Consequently, the ERP integration services market share tied to Asia-Pacific will surge as deadlines loom.

Europe balances entrenched customizations with GDPR fidelity. Article 48's cross-border restrictions promote sovereign-cloud offerings such as SAP Sovereign Cloud. South America and the Middle East and Africa remain smaller but promising. Brazil and Saudi Arabia lead government digitization, and Mexico's USMCA membership accelerates cross-border supply-chain integrations that need real-time ERP connectors. Together, geographic diversification cushions the global ERP integration services market against localized shocks.

- Accenture plc

- IBM Corporation

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infosys Limited

- Capgemini SE

- Tata Consultancy Services Limited

- Deloitte Touche Tohmatsu Limited

- Cognizant Technology Solutions Corporation

- Wipro Limited

- HCL Technologies Limited

- MuleSoft LLC

- Boomi LP

- Celigo Inc.

- Jitterbit Inc.

- SnapLogic Inc.

- Workato Inc.

- Software AG

- Seeburger AG

- Infor Inc.

- Epicor Software Corporation

- IFS AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Cloud-Based ERP Systems

- 4.2.2 Need for Real-Time Data Synchronization Across Heterogeneous Systems

- 4.2.3 Increasing API-First Digital Transformation Strategies

- 4.2.4 Growing Popularity of iPaaS Platforms Among SMEs

- 4.2.5 Emergence of Low-Code/No-Code Integration Tools

- 4.2.6 Compliance Mandates Driving Data Integration in Regulated Industries

- 4.3 Market Restraints

- 4.3.1 Complexity of Legacy ERP Customizations

- 4.3.2 High Total Cost of Ownership for Large Integration Projects

- 4.3.3 Data Security and Governance Concerns in Hybrid Environments

- 4.3.4 Shortage of Skilled Integration Specialists

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Application Integration

- 5.1.2 Data Integration

- 5.1.3 Process Integration

- 5.1.4 API Management

- 5.1.5 B2B/EDI Integration

- 5.1.6 Cloud Integration Brokerage

- 5.1.7 Other Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 Manufacturing

- 5.4.2 BFSI

- 5.4.3 Retail and Ecommerce

- 5.4.4 Healthcare

- 5.4.5 IT and Telecom

- 5.4.6 Government and Public Sector

- 5.4.7 Energy and Utilities

- 5.4.8 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 IBM Corporation

- 6.4.3 SAP SE

- 6.4.4 Oracle Corporation

- 6.4.5 Microsoft Corporation

- 6.4.6 Infosys Limited

- 6.4.7 Capgemini SE

- 6.4.8 Tata Consultancy Services Limited

- 6.4.9 Deloitte Touche Tohmatsu Limited

- 6.4.10 Cognizant Technology Solutions Corporation

- 6.4.11 Wipro Limited

- 6.4.12 HCL Technologies Limited

- 6.4.13 MuleSoft LLC

- 6.4.14 Boomi LP

- 6.4.15 Celigo Inc.

- 6.4.16 Jitterbit Inc.

- 6.4.17 SnapLogic Inc.

- 6.4.18 Workato Inc.

- 6.4.19 Software AG

- 6.4.20 Seeburger AG

- 6.4.21 Infor Inc.

- 6.4.22 Epicor Software Corporation

- 6.4.23 IFS AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP管理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)企劃為基礎的企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP管理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)企劃為基礎的企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)