|

市場調查報告書

商品編碼

2065548

企劃為基礎的企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Project-Based Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

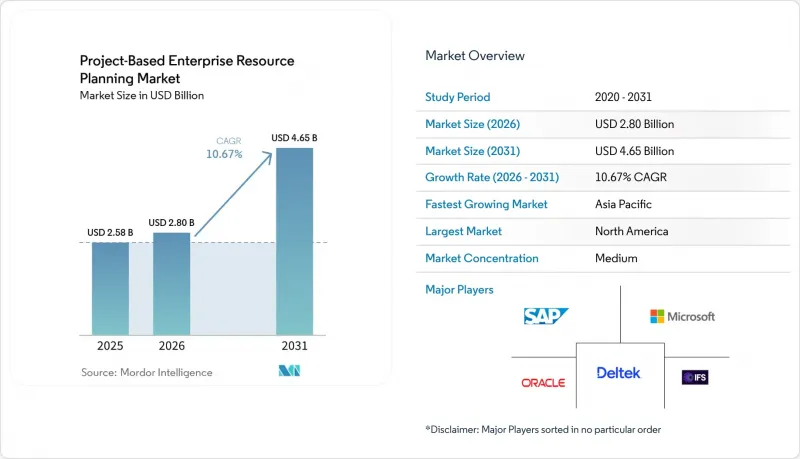

根據 Mordor Intelligence 預測,企劃為基礎的企業資源規劃 (ERP) 市場規模預計將從 2025 年的 25.8 億美元和 2026 年的 28 億美元成長到 2031 年的 46.5 億美元,2026 年至 2031 年的複合年成長率為 10.67%。

本報告按部署方式(本地部署、雲端/SaaS、混合部署)、組織規模(大型企業、中小企業)、組件(軟體、服務)、最終用戶產業(建築與工程、專業服務、航太與國防、政府與公用事業、其他)以及地區進行細分。市場預測以美元計價。

全球企劃為基礎的企業資源規劃 (ERP) 市場趨勢與分析

引入遠距工作和分散式企劃團隊

到2025年,隨著遠端辦公和混合辦公模式的普及,企業被迫逐步淘汰依賴VPN存取和桌面用戶端的本地部署系統。如今,雲端原生、企劃為基礎的ERP市場平台標配行動介面,使現場工程師能夠透過任何裝置打卡並核准變更請求。在航太和專業服務業的試點部署中,核准週期縮短了40%。工時記錄可在數小時內完成,從而提高了計費運轉率,並保護了因人工延遲而損失的利潤率。買家越來越傾向於選擇將聊天、文件管理和工作流程核准功能直接整合到其ERP系統中的供應商,而不是依賴第三方工具。這種整合簡化了使用者培訓並降低了整合成本,使遠端協作成為關鍵的採購競標。因此,針對分散式團隊體驗進行最佳化的解決方案供應商擁有競爭優勢。

向SaaS和訂閱定價模式轉型

隨著供應商陸續宣布本地部署版本的支援終止日期,企劃為基礎的ERP市場正明確地向訂閱合約模式轉型。 Epicor的藍圖顯示,到2026年1月,客戶將有四年的過渡期,這縮短了決策週期,加速了雲端採用。 SaaS模式雖然省去了伺服器硬體成本,但同時也把資本投資轉化為持續的營運支出,從長遠來看,這些支出可能超過永久授權的攤銷成本。這種權衡對那些重視持續功能更新和靈活用戶擴展的公司來說很有吸引力,但對於員工隊伍穩定的企業來說,則需要仔細評估訂閱的總生命週期成本。緊迫的過渡期迫使即使是風險規避型產業也加快資料轉型專案的步伐,從而推動了整個企劃為基礎的ERP市場雲端收入的兩位數成長。

從傳統ERP平台遷移成本高昂

遷移歷史資料、重建自訂整合以及使用者培訓可能需要 18 到 24 個月的時間,而複雜的系統重構工作可能會超出預算 30% 以上。一家中型工程公司在替換使用了 15 年的 Deltek 系統時,需要在遷移期間映射舊的成本代碼並維護有效合約的審計追蹤。 NetSuite 的「SuiteSuccess」和 Unit4 的低程式碼配置有助於縮短工期,但高昂的投資門檻令規避風險的財務長們望而卻步。在快速實施框架的可靠性在大規模部署中得到驗證之前,高昂的切換成本將減緩部分企劃為基礎的ERP 市場的採用速度。

細分市場分析

隨著企業將私有雲端資料庫與公共雲端協作模組結合,混合雲配置預計到2031年將以17.80%的複合年成長率成長。到2025年,雲端採用將佔企劃為基礎ERP市場佔有率的52.12%,這主要得益於買家對供應商管理的安全性和自動化升級的信心。例如,建築集團可能會將高度敏感的財務資料儲存在私人基礎設施上,同時將行動現場服務和分析工作負載部署到公有SaaS平台,以支援現場工程師的工作。儘管由於供應商將創新限制在雲端版本上,本地部署的企劃為基礎ERP市場正在萎縮,但國防和關鍵基礎設施產業的客戶對空氣間隙網路的需求仍然強勁。

企業在選擇實施模式時,會權衡總成本(包括訂閱費、資料傳輸和整合費)與可擴充性的柔軟性。微軟的 Dynamics 365 分階段部署方案和 SAP 的 RISE 計畫都支援分階段遷移,進而降低營運風險。對於那些苦於應對高度客製化傳統系統架構的企業而言,允許分階段模組遷移的混合解決方案極具吸引力。因此,隨著企業既需要合規性又需要快速創新,混合解決方案仍然是企劃為基礎的ERP 市場中成長最快的細分領域。

截至2025年,大型企業在以企劃為基礎的ERP市場中佔據60.29%的佔有率,而中小企業預計到2031年將以15.60%的複合年成長率成長。訂閱式定價模式消除了資金壁壘。例如,一家擁有200名員工的建築公司第一年只需花費5萬至10萬美元即可部署核心模組,這僅為傳統本地部署成本的五分之一。 Net at Work於2026年1月收購BHE Consulting,顯示整合商對中型企業市場成長的濃厚興趣。模組化授權模式允許中小企業根據自身收入情況添加採購和分析功能,從而將軟體成本與合約收入掛鉤。

專業服務、建築和IT諮詢行業正在推動ERP的普及,因為它們的利潤率依賴於即時數據收集和快速計費。儘管外匯波動和宏觀經濟不穩定仍然限制著南美和非洲地區的ERP普及,但供應商提供的靈活付款方式和本地資料中心正在降低這些障礙。隨著曾經僅限於全球企業的功能逐漸開放,中小企業將在基於企劃為基礎的ERP市場的功能藍圖方面發揮越來越重要的作用。

區域分析

北美擁有成熟的生態系統、雄厚的IT預算以及國防和專業服務服務業的集中度,預計到2025年將佔據企劃為基礎的ERP市場收入的34.26%。美國聯邦機構正在部署企業專案管理軟體來追蹤資本項目,而加拿大和墨西哥的製造商正在整合ERP系統來協調近岸供應鏈。大量認證顧問和人工智慧的早期應用也為該地區持續保持領先地位做出了貢獻。

亞太地區正經歷最快成長,預計到2031年複合年成長率將達到13.70%。中國的「一帶一路」計劃、印度的強制性電子帳單以及東南亞國協製造業的擴張,都推動了強勁的需求。澳洲和紐西蘭的採礦業電子化應用率很高,而日本正在升級其ERP系統以支援智慧工廠計畫。勞動力短缺以及有關資料儲存地點多樣化的法規正在加速區域雲區的形成和混合模式的採用。

在歐洲,企業正努力平衡商業機會與監管阻力。由於GDPR、永續發展報告和醫療設備法規的實施,合規要求日益嚴格,買家正轉向具備內建審計功能的平台。德國、英國、法國和義大利正在推動汽車、航太和工程領域的支出成長。在中東,與經濟多元化策略相關的大型企劃投資正在推進,能夠滿足合資企業和伊斯蘭金融需求的ERP系統需求旺盛。由於貨幣波動,南美洲的成長僅限於巴西和阿根廷;儘管基礎設施不足,南非和奈及利亞在非洲的採礦和電信業仍主導ERP系統的應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 引入遠距工作和分散式企劃團隊

- 向SaaS和訂閱定價模式轉型

- 人工智慧驅動的專案分析的整合

- 項目會計合規性的日益複雜化。

- 從競標到現金轉化,各個項目都需要視覺化。

- 加大對公共基礎設施大型企劃的投資

- 市場限制因素

- 從傳統ERP平台遷移成本高昂

- 缺乏熟練的專案和ERP實施專家

- 多租戶雲端環境中的資料安全問題

- 宏觀經濟不確定性下中小企業面臨的預算限制

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 透過部署方法

- 現場

- 雲/SaaS

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按組件

- 軟體

- 服務

- 按最終用戶行業分類

- 建築與工程

- 專業服務

- 航太/國防

- 政府和公用事業

- 醫療保健

- IT/通訊

- 製造業

- 石油和天然氣

- 其他工業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deltek, Inc.

- IFS AB

- Unit4 NV

- Oracle Corporation

- SAP SE

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- Workday, Inc.

- Acumatica, Inc.

- Ramco Systems Limited

- SYSPRO(Proprietary)Limited

- Priority Software Ltd.

- QAD Inc.

- Sage Group plc

- Totvs SA

- NetSuite Inc.

- FinancialForce.com, Inc.

- Aptean, Inc.

- Plex Systems, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the project-Based enterprise resource planning (ERP) market size is projected to expand from USD 2.58 billion in 2025 and USD 2.80 billion in 2026 to USD 4.65 billion by 2031, registering a CAGR of 10.67% during 2026-2031.

This report is Segmented by Deployment Mode (On-Premise, Cloud/SaaS, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Component (Software, and Services), End-User Industry (Construction and Engineering, Professional Services, Aerospace and Defense, Government and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Project-Based Enterprise Resource Planning Market Trends and Insights

Adoption Of Remote Work And Distributed Project Teams

Remote and hybrid work models became permanent in 2025, forcing companies to retire on-premises systems that rely on VPN access and desktop clients. Cloud-native Project-Based ERP market platforms now ship with mobile interfaces that let field engineers submit timecards and approve change orders from any device, cutting approval cycles by 40% in aerospace and professional-services pilots. Billable utilization climbs when time entries are captured within hours, protecting margins that would otherwise be eroded by manual delays. Buyers increasingly prefer vendors that embed chat, document management, and workflow approvals directly inside the ERP rather than through third-party tools. This consolidation simplifies user training and reduces integration overhead, making remote collaboration a key purchase criterion. As a result, solution providers that optimize experiences for distributed teams are winning competitive bids.

Transition To SaaS And Subscription-Based Pricing Models

The Project-Based ERP market is shifting decisively toward subscription contracts as vendors announce sunset dates for on-premises releases. Epicor's January 2026 roadmap gives customers four years to migrate, a deadline that compresses decision cycles and accelerates cloud adoption. SaaS eliminates server hardware costs, yet it converts capital expenditure into recurring operating expense that can exceed perpetual-license amortization over long horizons. Firms that value continuous feature updates and elastic user scaling find the trade-off attractive, whereas organizations with stable headcounts must carefully evaluate lifetime subscription totals. Migration windows are pushing even risk-averse industries to accelerate data-conversion projects, reinforcing double-digit growth in cloud revenue across the Project-Based ERP market.

High Switching Costs From Legacy ERP Platforms

Migrating historical data, rebuilding custom integrations, and training users can consume 18-24 months and overrun budgets by 30% in complex carve-outs. A mid-sized engineering firm replacing a 15-year-old Deltek instance must map legacy cost codes and maintain audit trails for active contracts during cutover. NetSuite's SuiteSuccess and Unit4's low-code configuration help compress timelines, yet the investment hurdle deters risk-averse CFOs. Until accelerated implementation frameworks prove reliable at scale, high switching costs will temper adoption velocity in parts of the Project-Based ERP market.

Other drivers and restraints analyzed in the detailed report include:

- Integration Of AI-Driven Project Analytics

- Growing Complexity Of Compliance In Project Accounting

- Shortage Of Skilled Project-ERP Implementation Specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid configurations are expanding at 17.80% CAGR through 2031 as enterprises pair private-cloud databases with public-cloud collaboration modules. Cloud installations captured 52.12% of the Project-Based ERP market share in 2025, confirming buyer confidence in vendor-managed security and automatic upgrades. A construction conglomerate might hold sensitive financials on private infrastructure but place mobile field-service and analytics workloads in public SaaS to support site engineers. The Project-Based ERP market size for on-premises deployments is shrinking as vendors limit innovation to cloud editions, yet it persists in defense and critical infrastructure accounts that require air-gapped networks.

Organizations choosing deployment models assess total cost across subscription, data egress, and integration charges versus the flexibility to scale. Microsoft's tiered Dynamics 365 options and SAP's RISE program encourage phased migrations that reduce operational risk. Hybrid offerings that allow incremental module shifts appeal to firms burdened by heavily customized legacy stacks. Consequently, hybrid remains the fastest-growing slice of the Project-Based ERP market as businesses seek both compliance and rapid innovation.

Large enterprises held a 60.29% share of the Project-Based ERP market in 2025, yet small and medium enterprises are growing at a 15.60% CAGR through 2031. Subscription pricing removes capital barriers: a 200-person architectural firm can deploy core modules for USD 50,000-100,000 in year one, a fifth of historical on-premises costs. Net at Work's January 2026 purchase of BHE Consulting underscores integrator interest in mid-market growth. Modular licensing lets SMEs add procurement or analytics when revenue allows, aligning software expense with contract inflows.

Professional services, construction, and IT consultancies lead adoption because margins depend on real-time capture and prompt billing. Currency fluctuations and macroeconomic volatility still curb adoption in South America and Africa, but vendors that offer flexible payment terms and regionally hosted data centers are reducing barriers. As capabilities once reserved for global enterprises become accessible, SMEs will exert growing influence on functional roadmaps within the Project-Based ERP market.

Geography Analysis

North America accounted for 34.26% of the Project-Based ERP market revenue in 2025, owing to mature ecosystems, high IT budgets, and a concentration of defense and professional services. U.S. federal agencies adopted enterprise project management software to track capital programs, while Canadian and Mexican manufacturers integrated ERP systems to coordinate nearshore supply chains. A deep bench of certified consultants and early AI experimentation helps the region maintain leadership.

Asia-Pacific is growing fastest, with a 13.70% CAGR through 2031. China's Belt and Road projects, India's electronic invoicing mandates, and ASEAN manufacturing expansion are fueling robust demand. Australia and New Zealand have high deployment rates in mining, and Japan is upgrading its ERP systems to support smart-factory initiatives. Talent shortages and diverse data-residency laws are driving regional cloud zones and accelerating hybrid models.

Europe balances opportunity with regulatory headwinds. GDPR, sustainability reporting, and the Medical Device Regulation elevate compliance requirements, steering buyers toward platforms with built-in audit capabilities. Germany, the United Kingdom, France, and Italy dominate spend across automotive, aerospace, and engineering. The Middle East invests in megaprojects tied to diversification agendas, seeking ERP that supports joint ventures and Islamic finance. South American growth is localized to Brazil and Argentina due to currency volatility, and Africa's uptake is led by South Africa and Nigeria in mining and telecom despite infrastructure gaps.

- Deltek, Inc.

- IFS AB

- Unit4 N.V.

- Oracle Corporation

- SAP SE

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- Workday, Inc.

- Acumatica, Inc.

- Ramco Systems Limited

- SYSPRO (Proprietary) Limited

- Priority Software Ltd.

- QAD Inc.

- Sage Group plc

- Totvs S.A.

- NetSuite Inc.

- FinancialForce.com, Inc.

- Aptean, Inc.

- Plex Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of Remote Work and Distributed Project Teams

- 4.2.2 Transition to SaaS and Subscription-Based Pricing Models

- 4.2.3 Integration of AI-Driven Project Analytics

- 4.2.4 Growing Complexity of Compliance in Project Accounting

- 4.2.5 Demand for Unified Bid-to-Cash Visibility Across Projects

- 4.2.6 Rising Investment in Public Infrastructure Megaprojects

- 4.3 Market Restraints

- 4.3.1 High Switching Costs from Legacy ERP Platforms

- 4.3.2 Shortage of Skilled Project-ERP Implementation Specialists

- 4.3.3 Data Security Concerns in Multi-Tenant Cloud Environments

- 4.3.4 Budget Constraints in SMEs Amid Macroeconomic Uncertainty

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premise

- 5.1.2 Cloud/SaaS

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Component

- 5.3.1 Software

- 5.3.2 Services

- 5.4 By End-User Industry

- 5.4.1 Construction and Engineering

- 5.4.2 Professional Services

- 5.4.3 Aerospace and Defense

- 5.4.4 Government and Utilities

- 5.4.5 Healthcare

- 5.4.6 IT and Telecom

- 5.4.7 Manufacturing

- 5.4.8 Oil and Gas

- 5.4.9 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Deltek, Inc.

- 6.4.2 IFS AB

- 6.4.3 Unit4 N.V.

- 6.4.4 Oracle Corporation

- 6.4.5 SAP SE

- 6.4.6 Microsoft Corporation

- 6.4.7 Infor, Inc.

- 6.4.8 Epicor Software Corporation

- 6.4.9 Workday, Inc.

- 6.4.10 Acumatica, Inc.

- 6.4.11 Ramco Systems Limited

- 6.4.12 SYSPRO (Proprietary) Limited

- 6.4.13 Priority Software Ltd.

- 6.4.14 QAD Inc.

- 6.4.15 Sage Group plc

- 6.4.16 Totvs S.A.

- 6.4.17 NetSuite Inc.

- 6.4.18 FinancialForce.com, Inc.

- 6.4.19 Aptean, Inc.

- 6.4.20 Plex Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP管理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP管理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)