|

市場調查報告書

商品編碼

2065550

SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

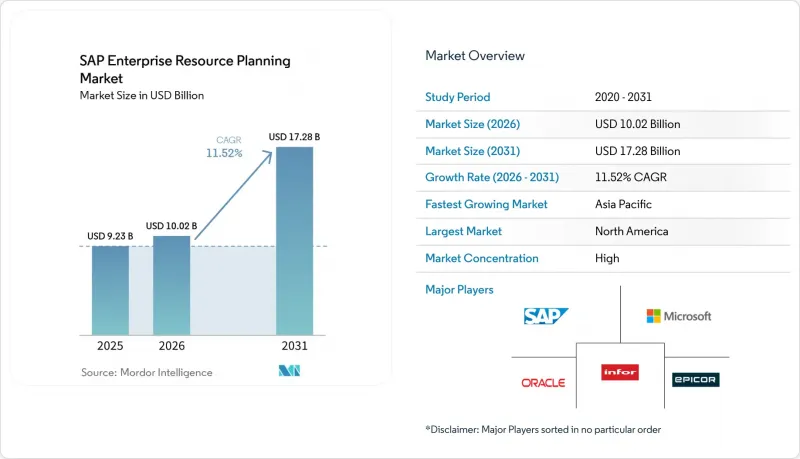

據 Mordor Intelligence 稱,2025 年 SAP 企業資源規劃 (ERP) 市場價值為 92.3 億美元,預計到 2031 年將從 2026 年的 100.2 億美元成長至 172.8 億美元,預測期(2026-2031 年)的複合年成長率為 11.52%。

本報告按部署模式(本地部署、雲端部署、混合部署)、組織規模(大型企業和中小企業)、產業(製造業、零售業、銀行、金融服務業、醫療保健業、能源和公共產業、電信業等)、模組(財務管理、供應鏈管理、人力資本管理、客戶關係管理等)和地區進行細分。市場預測以美元計價。

全球SAP企業資源規劃(ERP)市場趨勢與洞察

對即時商業分析的需求日益成長

企業正以記憶體內儀表板取代夜間批次報告,從而即時掌握利潤流出和庫存異常情況。 SAP S/4HANA 私有版中的全新 SAP Joule 功能讓財務團隊只需一次操作即可刷新即將到期的價格表,將以往需要幾分鐘才能完成的任務縮短至幾秒鐘。預先配置的零售和資產管理資料產品進一步縮短了從原始交易資料到 AI 模型的路徑。 Oracle的競爭對手正在將 ERP 資料與人力資源政策和供應商合約整合,向客戶表明自主預測不再是新鮮事物,而是必需品。因此,對預測性和指導性洞察的競爭正在加速升級週期,並推動 SAP 企業資源計劃 (ERP) 市場持續實現兩位數成長。

加速推動「雲端優先」數位轉型策略

資料中心租賃到期、超大規模資料中心業者服務商的獎勵以及董事會層面的指令,正迫使企業比原藍圖提前很多時間採用雲端運算。 Aalstrom 為期四週的工廠部署案例研究表明,採用純淨核心的 S/4HANA公共雲端部署不僅可以將舊有系統的升級時間縮短數月,還能從一開始就使用 Joule 驅動的 AI。 RAK Ceramics 決定將 55 個實體遷移到 S/4HANA私有雲端,這表明多元化製造商也同樣感受到了這種緊迫感。微軟 Azure 提供的 99.95% SLA 選項徹底消除了企業對關鍵業務工作運作的最後一個擔憂。這些因素共同推動了整個 SAP 企業資源規劃市場雲端訂閱量維持強勁的 15% 左右的成長率。

對於傳統使用者而言,從 ECC 遷移到 S/4HANA 的成本很高。

像 Al Huttime 這樣的遷移案例(資料量高達 16 Terabyte)凸顯了遷移數十年累積的自訂程式碼和聚合資料所需的數百萬美元成本和漫長的周末時間。即使部署了自動化工具,系統停機 30 小時的情況仍然屢見不鮮。目前,大量資金正湧入系統核心重建、資料清洗和變更管理項目,擠佔了原本用於創新營運的資金。只要改裝成本居高不下,部分中型企業就會延後升級,減緩 SAP ERP 市場的短期成長。

細分市場分析

預計到 2025 年,雲端運算將佔據 SAP 企業資源規劃 (ERP) 市場 48.20% 的佔有率,並將在 2031 年前保持 14.20% 的複合年成長率 (CAGR)。諸如「GROW with SAP」之類的多租戶 SaaS 服務憑藉其固定價格的套餐計劃吸引著中型企業,而大型製造商則採用與超大規模資料中心業者私有雲端版本。對於資料居住要求嚴格的國防和公共部門客戶而言,本地部署解決方案仍然佔據主導地位,而混合環境則作為過渡措施繼續存在。由於能夠快速存取 Joule 代理程式和預先配置的資料產品,雲端原生部署相比傳統架構具有更顯著的優勢。

客戶回饋,將基礎架構管理遷移到 Azure、AWS 或阿里雲端後,整體擁有成本顯著降低。 「核心淨流」策略減少了季度發布週期中的斷點,從而提高了運作和可審計性。相較之下,混合環境通常存在雙重整合層和使用者體驗不一致的問題。隨著超大規模資料中心業者不斷增加自主雲端區域,監管障礙進一步放寬,加速了雲端佔有率的成長,並持續推動 SAP 企業資源規劃 (ERP) 市場的擴張。

到2025年,大型企業將佔SAP ERP市場收入的63.40%,這主要得益於跨國部署、複雜的公司間結算流程以及已實施模組數量的不斷增加。儘管大型企業仍是SAP ERP市場收入的支柱,但預計到2031年,中小企業(SME)的年複合成長率(CAGR)將達到15.90%,超過大型企業。 「GROW with SAP」提供預先定義的產業特定流程和低程式碼擴充性,使中型企業的財務長(CFO)無需編寫自訂ABAP程式碼即可獲得預測性現金流量洞察。

印尼和越南的早期用戶表示,遷移到公共雲端版本後,交易流程更加快捷,盈利也提升了。由於全球範本需要與合併會計、貿易合規引擎和製造執行系統緊密整合,大型企業在絕對支出方面仍佔據主導地位。然而,中型企業市場的成長動能正在擴大整體潛在市場規模,進而支撐SAP企業資源規劃市場的長期健康發展。

區域分析

北美在2025年仍維持35.90%的市場佔有率,主要得益於ERP現代化以及財富500強企業早期採用雲端技術。 Azure全新的99.95%服務等級協定(SLA)透過消除對關鍵系統運作的擔憂,進一步加速了雲端遷移。在歐洲,GDPR和永續發展法規正在推動私有雲端和純淨核心策略的發展,而對數位主權的擔憂則減緩了多租戶環境的採用。法國和德國政府主導的主權雲正在透過平衡合規性和創新性來緩解這些擔憂。

亞太地區預計將以13.80%的複合年成長率實現最高成長,這主要得益於印度崛起為SAP的人工智慧中心以及技能人才供應的快速成長。日本和澳洲的自主雲端政策正在促進當地超大規模資料中心業者與SAP之間的合作,從而刺激公共部門的需求。中國市場的情況仍然複雜,合資企業採用S/4HANA私有雲端既要滿足本地化法規要求,也要與全球母公司保持一致。

中東和非洲的市場成熟度各不相同。沙烏地阿拉伯「2030願景」的投資以及阿拉伯聯合大公國的大規模私營部門項目,正使基於公共雲端的ERP成為主流的預算選擇。南非的國有企業正在證明,即使在營運週期緊張的情況下,選擇性資料遷移也能取得成功。儘管基礎設施和諮詢人才短缺阻礙了小規模經濟體的發展,但礦業和電信巨頭的關鍵項目正在為SAP企業資源規劃(ERP)市場的未來擴張奠定基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對即時商業分析的需求日益成長

- 加速推動「雲端優先」數位轉型策略

- SAP S/4HANA 中 AI 和機器學習附加元件的整合

- 大型企業中可組合式ERP架構的興起

- 永續發展合規模組是此次升級的驅動力。

- 面向中階市場的產業雲端捆綁包,專注於細分領域。

- 市場限制因素

- 對於傳統使用者而言,從 ECC 遷移到 S/4HANA 的成本相對較高。

- 新興地區認證SAP顧問短缺

- 多租用戶部署中的網路彈性問題

- 對與超大規模資料中心業者。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 現場

- 雲

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按行業分類

- 製造業

- 零售和消費品

- BFSI

- 衛生保健

- 能源公用事業

- 電訊

- 其他工業部門

- 模組特定

- 財務管理

- 供應鏈管理

- 人力資本管理

- 客戶關係管理

- 生產計畫與執行

- 分析和商業智慧

- 其他模組

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Epicor Software Corporation

- Unit4 NV

- IFS AB

- The Sage Group plc

- Workday Inc.

- QAD Inc.

- Acumatica Inc.

- SYSPRO(Pty)Ltd.

- Deltek Inc.

- Ramco Systems Limited

- TOTVS SA

- Kingdee International Software Group Company Limited

- Yonyou Network Technology Co., Ltd.

- Priority Software Ltd.

- Plex Systems Inc.

- Cegid Group SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the sAP enterprise resource planning market size was valued at USD 9.23 billion in 2025 and estimated to grow from USD 10.02 billion in 2026 to reach USD 17.28 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031).

This report is Segmented by Deployment Model (On-Premise, Cloud, and Hybrid), Organization Size (Large Enterprises and SMEs), Industry Vertical (Manufacturing, Retail, BFSI, Healthcare, Energy and Utilities, Telecommunications, and More), Module (Financial Management, SCM, HCM, Customer Relationship Management, and More), and Geography. The Market Forecasts are in Value (USD).

Global SAP Enterprise Resource Planning Market Trends and Insights

Growing Demand for Real-Time Business Analytics

Enterprises are replacing nightly batch reports with in-memory dashboards that surface profit leaks and inventory anomalies in seconds. New SAP Joule skills inside S/4HANA Private Edition let finance teams extend expiring price lists with a single prompt, cutting multi-minute tasks to seconds. Pre-configured retail and asset-management data products further shorten the path from raw transactions to AI-ready models. Oracle's rival data agents now bind ERP data to HR policies and supplier contracts, showing customers that autonomous forecasting is table stakes rather than a novelty. The race for predictive and prescriptive insights is therefore compressing upgrade horizons and sustaining double-digit expansion in the SAP Enterprise Resource Planning market.

Acceleration of Cloud-First Digital Transformation Strategies

Expiring data-center leases, hyperscaler incentives, and board-level mandates are pushing firms to cloud deployments well ahead of earlier roadmaps. A four-week factory deployment by Ahlstrom demonstrated that a clean-core S/4HANA Public Cloud roll-out can beat legacy upgrade timelines by months while unlocking Joule-powered AI from day one. RAK Ceramics' decision to move 55 legal entities to S/4HANA Private Cloud echoes the same urgency among diversified manufacturers. Microsoft's 99.95% SLA option in Azure removes the final objection to uptime for mission-critical workloads. Together, these factors sustain a robust mid-teens growth clip for cloud subscriptions inside the broader SAP Enterprise Resource Planning market.

High Migration Costs From ECC to S/4HANA For Legacy Users

Sixteen-terabyte conversions like Al-Futtaim's spotlight the millions of dollars and long weekends needed to migrate decades of custom code and data aggregates. Even with automated tooling, 30-hour outages remain common. Capital now flows into clean-core redesigns, data scrubbing, and change-management programs, diverting funds from innovation workstreams. As long as retrofit costs stay elevated, some mid-market firms defer upgrades, tempering near-term expansion of the SAP Enterprise Resource Planning market.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI and Machine Learning Add-Ons Within SAP

- Rise of Composable ERP Architecture Among Large Enterprises

- Skill Shortage of Certified SAP Consultants In Emerging Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud captured 48.20% SAP Enterprise Resource Planning market share in 2025 and is forecast to post a 14.20% CAGR to 2031. Multitenant SaaS offerings such as GROW with SAP lure mid-market firms with fixed-price bundles, while large manufacturers embrace Private Cloud editions tied to hyperscaler SLAs. On-premises persists in defense and public-sector accounts with strict data-residency rules, keeping hybrid footprints alive as a stepping stone. Cloud-native deployments enjoy quicker access to Joule agents and pre-configured data products, reinforcing their advantage over legacy stacks.

Customers report lower total ownership once infrastructure management shifts to Azure, AWS, or Alibaba Cloud. Clean-core policies mean fewer breakpoints during quarterly release cycles, improving uptime and auditability. Hybrid estates, by contrast, often juggle double integration layers and inconsistent user experiences. As hyperscalers add sovereign-cloud regions, regulatory barriers ease further, driving incremental share gains for cloud and sustaining the expansion of the SAP Enterprise Resource Planning market.

Large enterprises accounted for 63.40% of revenue in 2025 thanks to multi-country rollouts, complex intercompany eliminations, and broader module counts. They remain the revenue anchor of the SAP Enterprise Resource Planning market size, but small and medium enterprises will outpace them at a 15.90% CAGR through 2031. GROW with SAP provides predefined industry processes and low-code extensibility, enabling mid-market CFOs to obtain predictive cash flow insights without bespoke ABAP code.

Early adopters in Indonesia and Vietnam cite faster closings and improved profitability after moving to public-cloud editions. Large enterprises still dominate absolute spend because global templates require consolidation, trade-compliance engines, and deep manufacturing execution tie-ins. Yet mid-market momentum expands the total addressable base, underpinning the long-term health of the SAP Enterprise Resource Planning market.

Geography Analysis

North America retained a 35.90% share in 2025, driven by Fortune 500 ERP refreshes and early cloud adoption. Azure's new 99.95% SLA removes objections to uptime for life-and-mission-critical installations, spurring further cloud migrations. Europe's GDPR and sustainability mandates are driving private-cloud and clean-core strategies, even as digital sovereignty concerns slow multitenant adoption. Government-backed sovereign clouds in France and Germany soften that stance, aligning compliance with innovation.

Asia-Pacific is forecast to record the fastest 13.80% CAGR, buoyed by India's emergence as SAP's AI hub and rapid skills-pipeline expansion. Sovereign-cloud policies in Japan and Australia encourage local hyperscaler-SAP zones, unlocking public-sector demand. China remains a nuanced play, with joint ventures adopting S/4HANA Private Cloud to stay aligned with global parents while satisfying localization rules.

Middle East and Africa exhibit mixed maturity. Vision 2030 investments in Saudi Arabia and large private-sector projects in the United Arab Emirates move public-cloud ERP into mainstream budgets. South Africa's state-owned enterprises prove that selective data transitions can succeed even under tight operational windows. Infrastructure gaps and consultant shortages restrain smaller economies, but anchor projects by mining and telecom majors seed future expansion of the SAP Enterprise Resource Planning market.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Epicor Software Corporation

- Unit4 N.V.

- IFS AB

- The Sage Group plc

- Workday Inc.

- QAD Inc.

- Acumatica Inc.

- SYSPRO (Pty) Ltd.

- Deltek Inc.

- Ramco Systems Limited

- TOTVS S.A.

- Kingdee International Software Group Company Limited

- Yonyou Network Technology Co., Ltd.

- Priority Software Ltd.

- Plex Systems Inc.

- Cegid Group SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for real-time business analytics

- 4.2.2 Acceleration of cloud-first digital transformation strategies

- 4.2.3 Integration of AI and machine learning add-ons within SAP S/4HANA

- 4.2.4 Rise of composable ERP architecture among large enterprises

- 4.2.5 Sustainability compliance modules driving upgrades

- 4.2.6 Industry-cloud bundles tailored for mid-market niches

- 4.3 Market Restraints

- 4.3.1 High migration costs from ECC to S/4HANA for legacy users

- 4.3.2 Skill shortage of certified SAP consultants in emerging regions

- 4.3.3 Cyber-resilience concerns around multi-tenant deployments

- 4.3.4 Vendor lock-in anxiety amid hyperscaler partnerships

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Industry Vertical

- 5.3.1 Manufacturing

- 5.3.2 Retail and Consumer Goods

- 5.3.3 BFSI

- 5.3.4 Healthcare

- 5.3.5 Energy and Utilities

- 5.3.6 Telecommunications

- 5.3.7 Rest of Industry Verticals

- 5.4 By Module

- 5.4.1 Financial Management

- 5.4.2 Supply Chain Management

- 5.4.3 Human Capital Management

- 5.4.4 Customer Relationship Management

- 5.4.5 Production Planning and Execution

- 5.4.6 Analytics and Business Intelligence

- 5.4.7 Other Modules

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 Unit4 N.V.

- 6.4.7 IFS AB

- 6.4.8 The Sage Group plc

- 6.4.9 Workday Inc.

- 6.4.10 QAD Inc.

- 6.4.11 Acumatica Inc.

- 6.4.12 SYSPRO (Pty) Ltd.

- 6.4.13 Deltek Inc.

- 6.4.14 Ramco Systems Limited

- 6.4.15 TOTVS S.A.

- 6.4.16 Kingdee International Software Group Company Limited

- 6.4.17 Yonyou Network Technology Co., Ltd.

- 6.4.18 Priority Software Ltd.

- 6.4.19 Plex Systems Inc.

- 6.4.20 Cegid Group SA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年 供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)

供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031) 企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)