|

市場調查報告書

商品編碼

2065565

ERP管理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Enterprise Resource Planning Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

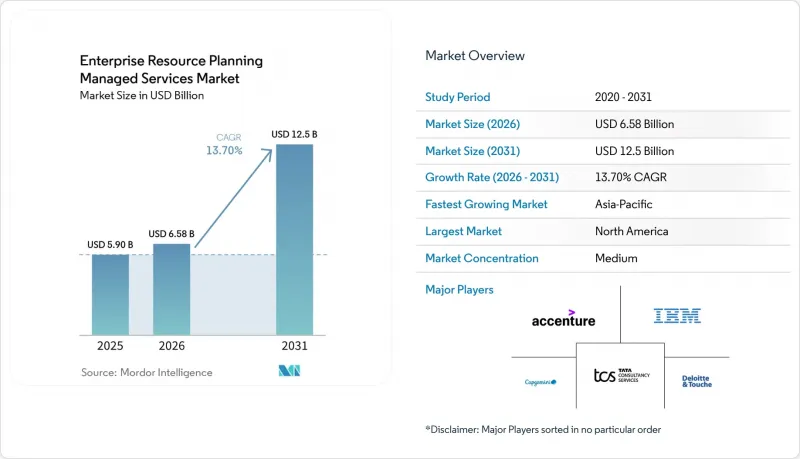

根據 Mordor Intelligence 預測,ERP 管理服務市場規模預計將在 2025 年達到 59 億美元,2026 年達到 65.8 億美元,到 2031 年達到 125 億美元,2026 年至 2031 年的複合年成長率為 13.7%。

本報告按部署模式(本地部署、雲端部署、混合部署)、公司規模(中小企業、大型企業)、產業(製造業、零售和消費品、醫療保健、銀行、金融服務和保險 (BFSI)、IT 和電信、政府和公共部門等)以及地區進行細分。市場預測以美元 (USD) 為單位。

全球ERP管理服務市場趨勢與洞察

擴大雲端ERP解決方案的採用

目前,超過70%的企業至少在一個核心ERP模組上運行,75%的新買家更傾向於雲端原生架構而非本地部署。與超大規模資料中心業者雲端服務商的夥伴關係將基礎設施額度和人工智慧服務與ERP訂閱捆綁在一起,例如SAP在IBM Power Virtual Server上推出的「RISE」服務。受ERP遷移的推動,Oracle雲端基礎設施在2025會計年度的營收也成長了52%。儘管中國和歐盟強制推行的「主權雲」政策推動了法律上隔離的多區域ERP實例的出現,但透過聯合資料模型進行跨境分析仍然可行。按需付費使用制的「Success4U」)正在幫助企業進入中端市場,迫使那些與超大規模資料中心業者服務商缺乏牢固合作關係或缺乏合規性交付模式的服務供應商放棄市場佔有率。

降低IT基礎設施成本的需求日益成長

基於訂閱的託管服務正在取代固定基礎設施支出,並將資料中心折舊免稅額成本轉化為營運費用。 IBM 將 15 萬用戶內部遷移到 SAP S/4HANA 雲端平台就是一個成功的例子,此舉使 IT 總支出減少了高達 30%。政府採購負責人也紛紛效法。美國國防後勤局 (DLA) 簽署了一份價值 9.03 億美元、為期七年的契約,將預算不確定性的風險轉移給了服務供應商,同時強制要求 99.9% 的可用性和符合 FedRAMP IL4 標準。預計到 2026 年,僅中小企業在託管 IT 服務上的支出就將超過 900 億美元,這主要得益於其固定費率模式,該模式無需組建內部 ERP 團隊。然而,多重雲端認證 ERP 專家的人事費用不斷上漲,迫使服務提供者投資於技能再培訓和人工智慧平台,以維持利潤率。

外包環境中的資料安全與隱私問題

2024年7月,Smart ERP Solutions公司發生資料外洩事件,導致79,000名用戶的個人資訊外洩。該公司因此被處以48萬歐元(約54萬美元)的GDPR罰款,並遭受約84萬歐元(約94.5萬美元)的業務損失。這凸顯了單一事件如何足以抹去託管服務多年的收入。這次針對SAP NetWeaver的零時差攻擊促使客戶實施全天候資安管理服務,並採用持續滲透測試和零信任架構。公共部門的採購要求如今強制要求採用主權雲端部署、政府所有的加密金鑰以及聘用美國公民,這提高了供應商的合規門檻。在這個監管嚴格的行業中,沒有ISO 27001認證或網路保險的供應商將難以通過採購審計。

細分市場分析

至2025年,雲端解決方案將佔ERP管理服務市場的54.8%,預計到2031年將以12.9%的複合年成長率成長。 Oracle雲端基礎設施在2025會計年度的收入激增、SAP向RISE的遷移以及阿里雲在中國的自主雲部署,都顯示訂閱定價、自動續訂和超大規模資料中心業者AI服務如今已成為決定性的採購標準。在國防和關鍵基礎設施領域,由於需要空氣間隙安全,本地部署仍然存在,但即使是這些領域的買家也在核心財務系統之上疊加基於雲端的分析功能。公共雲端用於創新工作負載,私有雲端或自主雲用於受監管資料的混合配置正在穩步成長,這需要只有少數供應商具備的編配能力。

隨著供應商將研發資源集中在雲端原生功能,傳統本地部署合約的利潤空間受到擠壓,迫使客戶遷移。同時,結合合規工具、模組化升級和利潤分成模式的託管服務正在蠶食傳統應用管理合約的市場佔有率。因此,ERP託管服務市場正朝著以雲端為中心的框架急劇轉變,而未獲得超大規模資料中心業者認證的供應商則面臨被淘汰的風險。

區域分析

到2025年,北美將佔全球整體收入的34.1%,這得益於聯邦現代化計畫和已建立的基於結果的採購框架。國防後勤局(DLA)價值9.03億美元的合約以及雅詩蘭黛與埃森哲Accenture5億美元的合作項目,都是多年期合約整合人工智慧驅動的自動化和自主雲合規性的典型例子。雖然充裕的資金和成熟的供應商生態系統為成長提供了支持,但勞動力短缺正在推高認證ERP人才的成本。

亞太地區是成長最快的地區,複合年成長率高達13.6%,這主要得益於中國的「創新」政策、印度大規模採用微軟Copilot許可證以及日本從傳統ECC系統向S/4HANA的遷移。光是中國一地,ERP管理服務市場預計到2025年就將達到34億美元。國內供應商用友和金蝶佔據了國有企業支出的大部分佔有率,而跨國公司則依賴阿里雲上的SAP主權實例。印度的頂級整合商正在向全球出口低成本、人工智慧賦能的支援工具,將印度半島打造成為全球交付人才中心。

儘管歐洲的銷售成長放緩,但人才短缺問題日益嚴重,目前S/4HANA專家的等候名單已長達90天。由於法國將於2026年9月強制推行電子帳單,以及能源公共產業要求使用數位產品護照,因此遵守性驅動的需求正在激增。南美洲、中東和非洲仍處於發展中地區,但這些地區蘊藏著豐富的商機,尤其是在缺乏稅務、薪資核算和海關本地化範本的地區。能夠順利完成多國部署並持續更新合規性的供應商,將能夠在這些新興地區建立先發優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大雲端ERP解決方案的採用

- 降低IT基礎設施成本的需求日益成長

- 即時數據分析的需求日益成長

- 由於多供應商生態系統,ERP環境日益複雜

- 人工智慧驅動的自主ERP運作的興起

- 供應商推廣基於結果的管理服務合約

- 市場限制因素

- 外包環境中的資料安全與隱私問題

- 高昂的轉換成本和供應商鎖定

- 服務供應商中缺乏產業專用的ERP人才

- 加強外包IT營運產生的範圍3排放的監控。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按部署模式

- 現場

- 雲

- 混合

- 按公司規模

- 小型企業

- 大公司

- 按行業

- 製造業

- 零售和消費品

- 衛生保健

- 銀行、金融服務和保險(BFSI)

- IT/通訊

- 政府/公共部門

- 能源公用事業

- 運輸/物流

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- International Business Machines Corporation

- Deloitte Touche Tohmatsu Limited

- Capgemini SE

- Infosys Limited

- Cognizant Technology Solutions Corporation

- Tata Consultancy Services Limited

- Wipro Limited

- HCL Technologies Limited

- NTT DATA Corporation

- DXC Technology Company

- Atos SE

- Fujitsu Limited

- Tech Mahindra Limited

- CGI Inc.

- SAP SE

- Oracle Corporation

- Syntax Systems GmbH and Co. KG

- Rimini Street, Inc.

- Navisite LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the eRP managed services market size is projected to be USD 5.90 billion in 2025, USD 6.58 billion in 2026, and reach USD 12.50 billion by 2031, growing at a CAGR of 13.7% from 2026 to 2031.

This report is Segmented by Deployment Model (On-Premises, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Industry Vertical (Manufacturing, Retail and Consumer Goods, Healthcare, Banking, Financial Services and Insurance (BFSI), IT and Telecom, Government and Public Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Resource Planning Managed Services Market Trends and Insights

Growing Adoption of Cloud-Based ERP Solutions

More than 70% of enterprises now operate at least one core ERP module in the cloud, and 75% of new buyers favor cloud-native architectures over on-premises deployments. Hyperscaler partnerships bundle ERP subscriptions with infrastructure credits and AI services, as demonstrated by SAP's RISE offering on IBM Power Virtual Server, while Oracle Cloud Infrastructure revenue surged 52% in fiscal 2025 on the back of ERP migrations. Sovereign-cloud mandates in China and the European Union drive multi-region, legally isolated ERP instances that still enable cross-border analytics through federated data models. Consumption-based pricing and 90-day deployment frameworks, such as Unit4's Success4U, are unlocking the mid-market, forcing service providers without deep hyperscaler alliances or compliance-ready delivery models to cede share.

Increasing Need to Reduce IT Infrastructure Costs

Subscription-driven managed services are replacing fixed infrastructure outlays, converting data-center depreciation into operating expense and trimming total IT spend by up to 30% in documented cases such as IBM's 150,000-user internal migration to SAP S/4HANA Cloud. Government buyers are following suit: the U.S. Defense Logistics Agency issued a USD 903 million, seven-year contract that shifts budget-predictability risk to service providers while mandating 99.9% availability and FedRAMP IL4 compliance. Small and medium enterprises alone will direct more than USD 90 billion to managed IT services through 2026, lured by fixed-fee models that eliminate the need for in-house ERP teams. The countertrend is a rising unit cost for multi-cloud-certified ERP specialists, compelling providers to invest in reskilling and AI delivery platforms to protect margins.

Data Security and Privacy Concerns in Outsourced Environments

The July 2024 Smart ERP Solutions breach exposed 79,000 personal records and triggered EUR 480,000 (USD 540,000) in GDPR fines, plus nearly EUR 840,000 (USD 945,000) in lost business, illustrating how a single incident can erase multiple years of managed-service fees. Zero-day exploits in SAP NetWeaver prompted clients to adopt 24x7 managed security services with continuous penetration testing and zero-trust architectures. Public-sector solicitations now stipulate sovereign-cloud deployment, government-owned encryption keys, and U.S.-citizen staffing, raising the compliance bar for providers. Vendors lacking ISO 27001 certification or cyber-insurance will struggle to pass procurement gates in regulated verticals.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Real-Time Data Analytics

- Growing Complexity of ERP Landscapes Due to Multi-Vendor Ecosystems

- High Switching Costs and Vendor Lock-In

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud solutions accounted for 54.8% of the ERP managed services market in 2025 and are on track to expand at a 12.9% CAGR through 2031. Oracle Cloud Infrastructure's FY 2025 revenue surge, SAP's RISE migrations, and Alibaba Cloud sovereign deployments in China confirm that subscription pricing, automatic updates, and hyperscaler AI services are now decisive purchase criteria. While on-premises deployments linger in defense and critical-infrastructure sectors that require air-gapped security, even those buyers are layering cloud-based analytics on top of core financial systems. Hybrid configurations blending public cloud for innovation workloads with private or sovereign cloud for regulated data are steadily growing, demanding orchestration skills that only a subset of providers possess.

Margins in legacy on-premises arrangements are pinched as vendors funnel Research and Development to cloud-native functionality, pushing customers toward migration. Meanwhile, managed service practices that combine compliance tooling, modular upgrades, and gain-share economics are capturing wallet share from traditional application management contracts. As a result, the ERP managed services market is tilting decisively toward cloud-centric frameworks, and providers without hyperscaler certifications risk obsolescence.

Geography Analysis

North America generated 34.1% of global revenue in 2025, anchored by federal modernization programs and well-established outcome-based procurement frameworks. The Defense Logistics Agency's USD 903 million contract and Estee Lauder's USD 500 million partnership with Accenture typify multi-year deals that integrate AI automation and sovereign-cloud compliance. Strong capital pools and mature vendor ecosystems sustain growth, even as labor shortages drive up the cost of certified ERP talent.

Asia-Pacific is the fastest-growing region, with a 13.6% CAGR, driven by China's Xinchuang mandates, India's mass deployment of Microsoft Copilot licenses, and Japan's shift from legacy ECC systems to S/4HANA. The ERP managed services market in China alone reached USD 3.40 billion in 2025, with domestic vendors Yonyou and Kingdee capturing the bulk of state-owned enterprise spend, while multinational corporations rely on SAP via Alibaba Cloud sovereign instances. India's tier-1 integrators are exporting low-cost, AI-enabled support tooling worldwide, turning the subcontinent into the labor fulcrum of global delivery.

Europe shows slower topline growth but acute talent scarcity, with S/4HANA specialists now taking 90 days to recruit. Mandatory e-invoicing in France by September 2026 and Digital Product Passport requirements in energy utilities create compliance-driven demand spikes. South America, the Middle East, and Africa remain nascent but opportunity-rich, particularly where localization templates for tax, payroll, and customs are scarce. Providers that can orchestrate multi-country rollouts with continuous compliance updates will unlock first-mover advantages across these emerging regions.

- Accenture plc

- International Business Machines Corporation

- Deloitte Touche Tohmatsu Limited

- Capgemini SE

- Infosys Limited

- Cognizant Technology Solutions Corporation

- Tata Consultancy Services Limited

- Wipro Limited

- HCL Technologies Limited

- NTT DATA Corporation

- DXC Technology Company

- Atos SE

- Fujitsu Limited

- Tech Mahindra Limited

- CGI Inc.

- SAP SE

- Oracle Corporation

- Syntax Systems GmbH and Co. KG

- Rimini Street, Inc.

- Navisite LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Cloud-Based ERP Solutions

- 4.2.2 Increasing Need to Reduce IT Infrastructure Costs

- 4.2.3 Rising Demand for Real-Time Data Analytics

- 4.2.4 Growing Complexity of ERP Landscapes Due to Multi-Vendor Ecosystems

- 4.2.5 Emergence of AI-Driven Autonomous ERP Operations

- 4.2.6 Vendor Push for Outcome-Based Managed Service Contracts

- 4.3 Market Restraints

- 4.3.1 Data Security and Privacy Concerns in Outsourced Environments

- 4.3.2 High Switching Costs and Vendor Lock-In

- 4.3.3 Shortage of Domain-Specific ERP Talent in Service Providers

- 4.3.4 Rising Scrutiny of Scope 3 Emissions from Outsourced IT Operations

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premises

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By Industry Vertical

- 5.3.1 Manufacturing

- 5.3.2 Retail and Consumer Goods

- 5.3.3 Healthcare

- 5.3.4 Banking, Financial Services and Insurance (BFSI)

- 5.3.5 Information Technology and Telecom

- 5.3.6 Government and Public Sector

- 5.3.7 Energy and Utilities

- 5.3.8 Transportation and Logistics

- 5.3.9 Other Industry Verticals

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Turkey

- 5.4.5.5 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Nigeria

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 International Business Machines Corporation

- 6.4.3 Deloitte Touche Tohmatsu Limited

- 6.4.4 Capgemini SE

- 6.4.5 Infosys Limited

- 6.4.6 Cognizant Technology Solutions Corporation

- 6.4.7 Tata Consultancy Services Limited

- 6.4.8 Wipro Limited

- 6.4.9 HCL Technologies Limited

- 6.4.10 NTT DATA Corporation

- 6.4.11 DXC Technology Company

- 6.4.12 Atos SE

- 6.4.13 Fujitsu Limited

- 6.4.14 Tech Mahindra Limited

- 6.4.15 CGI Inc.

- 6.4.16 SAP SE

- 6.4.17 Oracle Corporation

- 6.4.18 Syntax Systems GmbH and Co. KG

- 6.4.19 Rimini Street, Inc.

- 6.4.20 Navisite LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)企劃為基礎的企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)企劃為基礎的企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)