|

市場調查報告書

商品編碼

2065541

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP Vendor Ecosystem And Marketplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

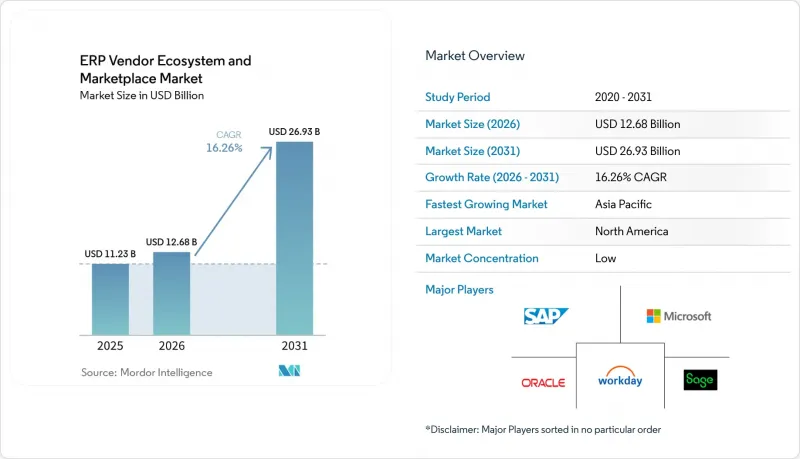

根據 Mordor Intelligence 預測,ERP 供應商生態系統市場規模預計將在 2025 年達到 112.3 億美元,2026 年達到 126.8 億美元,到 2031 年達到 269.3 億美元,2026 年至 2031 年的複合年成長率為 16.26%。

全球ERP供應商生態系市場趨勢及洞察。

SAP ECC 將於 2027 年停止支持,這將加速系統更換週期。

隨著 SAP 將於 2027 年 12 月停止對 ECC 6.0 的支持,一項長達十年的遷移工作將集中到未來 24 個月內完成,導致許可證更換率激增。這種情況對 SAP S/4HANA Cloud 和競爭對手套件均有利。儘管實施合作夥伴在 2025 年的認證人員數量實現了兩位數的成長,但超過 20% 的空缺率推高了經驗豐富的顧問的日薪,促使企業採用供應商市場提供的低程式碼遷移工具包。 Oracle 和 WorkdayOracle利用了這種市場疲勞,提供限時折扣和費用減免,吸引了那些更傾向於待開發區部署而非棕地改造的客戶。

實施嵌入式人工智慧的ERP套件

生成式人工智慧正在將ERP系統從被動的記錄系統轉變為自主決策駕駛座。 Oracle的「AI代理市場」提供能夠核對發票和預測需求的機器人,在早期試點部署中,它將結算週期從10天縮短至3天。 Microsoft Copilot for Dynamics 365利用自然語言提示自動發布日記帳分錄,將月末工作時間縮短了30%。 SAP的Joule Assistant允許採購負責人透過聊天而非電子郵件重新協商合約條款,催生了一個專注於快速工程的顧問公司新生態系統。 ERP核心和資料湖之間日益成長的API流量給傳統中間件帶來了沉重負擔,加速了事件驅動型整合平台的普及。

實施成本高且預算超支

一家擁有 500 名員工的製造企業遷移到 SAP S/4HANA Cloud 的五年平均總擁有成本 (TCO) 為 280 萬美元,但如果低估資料清理和變更管理所需的工作量,實施成本仍可能超出預算高達 50%。為此,供應商紛紛推出價格固定的快速啟動套餐,並限制客製化請求的數量,降低了准入門檻,但也壓縮了合作夥伴公司的利潤空間。小規模的顧問公司透過合併來擴張,市場上湧現大量旨在減少人工成本的自助式遷移工具。

細分市場分析

混合架構預計在2025年佔總支出的9%,但其複合年成長率高達19.90%,是所有部署模式中最快的。企業透過將事務資料庫保留在本地以降低延遲和規避監管要求,同時將分析和協作模組遷移到超大規模資料中心業者資料中心,與純本地部署環境相比,成本節省了近40%。供應商也在轉變策略。 SAP的「RISE」服務目前為35%的S/4HANA客戶提供混合拓撲的統一管理;Oracle Cloud at Customer將公共雲端軟體打包到本地設備中;Azure Stack則將Dynamics 365擴展到邊緣運算。這些舉措正在加深ERP供應商生態系統在受監管產業的市場滲透。

從ERP供應商生態系統市場的佔有率來看,雲端仍將保持其主導地位,到2025年將佔據70.40%的市場佔有率,但發展動能顯然正在轉移到混合環境。市場銷售也主要集中在混合環境,由於需要整合加速器來連接本地部署和雲端服務,客戶在混合環境中平均部署的附加元件數量為4.1個,而純雲端環境中的平均部署數量為3.2個。

到2025年,大型企業將佔總營收的62%,但中小企業(SME)的複合年成長率(CAGR)高達21.20%,幾乎是整體平均水準的兩倍。目前,按需付費使用制模式的引入降低了傳統的進入門檻,使得年收入5,000萬美元的製造商在第一年只需不到10萬美元即可部署核心財務系統。一項分兩階段實施的策略正在加速這項轉型。企業集團透過在總部維護SAP或Oracle系統,同時在其東南亞工廠部署Odoo或Acumatica系統,從而將每個工廠的成本降低了60%,並提升了其在ERP供應商生態系統專業中間商市場的佔有率。

模組化正在推動中小企業 (SMB) 的 ERP 供應商生態系統市場的成長。 Odoo 提供 40 個行業專屬軟體包,可在四週內完成部署;Rootstock 利用 Salesforce 原生物件整合 CRM 和 ERP,無需自訂連接器。儘管與大型企業的合約續約速度有所放緩,但它們仍然是利潤的核心來源。平均合約價值仍超過 500 萬美元,在現有供應商專注於獲取中小企業客戶之際,這支撐了其收入基礎。

區域分析

北美地區憑藉著密集的合作夥伴網路和快速的雲端技術應用,預計到2025年將佔總收入的37%。美國建設產業的人手不足推動了行動ERP模組的普及,這些模組可以追蹤現場工時和材料,從而減少了30%的後勤部門人員。加拿大擁有796家SAP認證公司,其中許多公司在魁北克省提供雙語支持,從而能夠實現符合兩地稅法的本地化實施方案。墨西哥的近岸外包浪潮推動了加工出口國子公司與其美國母公司之間對多幣種財務合併的需求。

亞太地區成長最快,複合年成長率達14.00%。印度的「數位印度」政策正迫使12萬家供應商在2027年前遷移到雲端ERP系統。儘管在中國,隨著金蝶和用友等替代方案的興起,供應商格局正在重組,但跨國公司仍堅持使用SAP的全球模板。日本中型製造商目前正在將其ECC系統遷移到雲端,以降低40%的維護人事費用。印尼、越南和泰國三國合計複合年成長率達18%,主要得益於大型電商公司對即時庫存管理的需求。

歐洲佔總銷售額的28%。隨著歐洲單一電子格式(ESEF)要求於2026年9月生效,12,000家上市公司將被要求嵌入XBRL標籤,報告模組的升級工作正在進行中。德國的中型企業(Mittelstands)正在分兩個階段實施,而在法國,隨著ECC支援期限的臨近,從AS/400舊有系統遷移的工作也在進行中。在南美洲,TOTVS憑藉其在地化的稅務引擎在中型企業市場中佔據主導地位;在中東,「2030願景」公共計畫正在刺激市場需求。非洲市場仍在發展中,但由於公共部門競標以行動優先為導向,市場需求正在成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速企業採用雲端運算

- 實施人工智慧驅動的ERP套件

- 對整合供應鏈可視性的需求

- 關於即時財務報告的監管義務

- SAP ECC 2027 停止支援將加快更新週期。

- 採用雙層ERP策略來支持利基供應商的發展。

- 市場限制因素

- 實施成本高且預算超支

- 關於雲端ERP系統資料安全和隱私的擔憂

- ERP實施所需合格人員短缺

- 可組合架構中的互通性挑戰

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 生態系類型分析

- 廠商專屬市場(SAP Store、Oracle Cloud Marketplace)

- 合作夥伴生態系統(系統整合商、獨立軟體開發商)

- 開放式生態系統(基於API,可與多個ERP系統整合)

第5章:預測市場規模與成長率

- 透過部署方法

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按組件

- 軟體模組

- 服務

- 按行業

- 製造業

- 零售與電子商務

- 醫學與生命科學

- 銀行、金融服務和保險業 (BFSI)

- 專業服務

- 公部門

- 其他行業

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- IFS AB

- Unit4 NV

- Acumatica, Inc.

- Sage Group plc

- Syspro(Pty)Ltd.

- QAD Inc.

- Deltek, Inc.

- Aptean, Inc.

- Plex Systems, Inc.

- Rootstock Software, Inc.

- Priority Software Ltd.

- Workday, Inc.

- Odoo SA

- Ramco Systems Limited

- TOTVS SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the eRP vendor ecosystem and marketplace market size is projected to be USD 11.23 billion in 2025, USD 12.68 billion in 2026, and reach USD 26.93 billion by 2031, growing at a CAGR of 16.26% from 2026 to 2031.

This report is Segmented by Deployment Model (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises and SMEs), Component (Software and Services), Industry Vertical (Manufacturing, Retail and E-Commerce, and Other Industry Verticals), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global ERP Vendor Ecosystem And Marketplace Market Trends and Insights

SAP ECC 2027 End-of-Support Driving Replacement Cycles

SAP's December 2027 support cutoff for ECC 6.0 is compressing a decade of migration activity into the next 24 months, creating a surge of license churn that benefits both SAP S/4HANA Cloud and rival suites. Implementation partners grew their certified headcount by double digits in 2025, yet vacancy rates above 20% are inflating day-rates for experienced consultants, pushing enterprises toward low-code migration kits distributed through vendor marketplaces. Oracle and Workday exploited the fatigue by offering time-limited discounts and fee waivers, luring defectors that prefer greenfield deployments over brownfield conversions.

Adoption of AI-Embedded ERP Suites

Generative AI is recasting ERP from a passive system of record into an autonomous decision cockpit. Oracle's AI Agent Marketplace ships bots that reconcile invoices and predict demand, trimming finance closings from 10 days to 3 days in early pilots. Microsoft Copilot for Dynamics 365 uses natural-language prompts to automatically post journals, reducing month-end labor hours by 30%. SAP's Joule assistant lets buyers renegotiate contract terms in chat rather than e-mail threads, catalyzing a new ecosystem of prompt-engineering consultancies. Growing API traffic between ERP cores and data lakes is stressing legacy middleware, accelerating uptake of event-driven integration platforms.

High Implementation Costs and Budget Overruns

Total cost of ownership for a 500-employee manufacturer moving to SAP S/4HANA Cloud averages USD 2.8 million over five years, and deployments still overshoot budgets by up to 50% when data cleansing and change management are underestimated. In response, vendors rolled out fixed-price quick-start bundles that cap customization requests, lowering the barrier to entry yet compressing partner margins. Smaller consultancies are merging to achieve scale, and self-service migration tools are proliferating inside marketplaces to limit human billable hours.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Cloud Adoption Among Enterprises

- Demand for Integrated Supply-Chain Visibility

- Data Security and Privacy Concerns in Cloud ERP

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid architectures held 9% of 2025 spending but are expanding at a 19.90% CAGR, the fastest among deployment models. Enterprises anchor transaction databases on-premises for latency or regulatory reasons and shuttle analytics and collaboration modules to hyperscalers, achieving a near 40% cost relief compared with pure on-premises landscapes. Vendors are pivoting: SAP's RISE service now orchestrates mixed topologies for 35% of S/4HANA clients, Oracle Cloud at Customer packages public-cloud software in an on-site appliance, and Azure Stack extends Dynamics 365 to edge factories, responses that deepen the ERP vendor ecosystem market penetration in regulated industries.

The ERP vendor ecosystem and marketplace market size advantage remains with cloud at 70.40% in 2025, yet momentum is firmly with hybrid. Marketplace sales skew heavier in hybrid estates; customers average 4.1 add-ons compared with 3.2 for pure cloud, because integration accelerators are required to bridge on-prem and cloud services.

Large organizations accounted for 62% of 2025 revenue, but the small and medium cohort is expanding at a 21.20% CAGR, nearly double the headline rate. Consumption-based pricing now lets a USD 50 million manufacturer roll out a financial core for under USD 100,000 in year one, eroding the historical barrier. Two-tier strategies intensify the shift: conglomerates keep SAP or Oracle at headquarters but provision Odoo or Acumatica at plants in Southeast Asia, reducing per-site fees by 60% and lifting ERP vendor ecosystem and marketplace market share for mid-market specialists.

The ERP vendor ecosystem and marketplace market-size tailwind for small and medium enterprises stems from modularity. Odoo ships 40 vertical packs that deploy in four weeks, and Rootstock leverages Salesforce-native objects to unite CRM and ERP without custom connectors. Large-enterprise renewals are slowing, but they remain the profit core: average contract value still tops USD 5 million, cushioning incumbents while they court smaller logos.

Geography Analysis

North America accounted for 37% of 2025 revenue, thanks to its dense partner network and rapid cloud adoption. The United States construction labor crunch is spurring adoption of mobile ERP modules that clock worker hours and materials on site, cutting back-office headcount 30%. Canada's 796 SAP-certified firms, many of which are bilingual in Quebec, support localized rollouts that comply with dual-jurisdiction tax codes. Mexico's nearshoring wave is driving demand for multi-currency consolidation between maquiladora subsidiaries and their U.S. parents.

Asia-Pacific is the fastest climber at 14.00% CAGR. Digital India forces 120,000 suppliers onto cloud ERP by 2027, and China's substitution drive toward Kingdee and Yonyou re-shapes the vendor mix even while multinationals cling to SAP global templates. Japanese mid-market manufacturers are now migrating ECC to the cloud to cut maintenance payroll by 40%. Indonesia, Vietnam, and Thailand together account for 18% CAGR as e-commerce giants spur demand for real-time inventory.

Europe contributes 28% of revenue. The European Single Electronic Format requirement, effective September 2026, obliges 12,000 listed firms to embed XBRL tags, prompting upgrades to reporting modules. Germany's Mittelstand runs two-tier deployments, and France is migrating from AS/400 legacies under ECC support deadlines. In South America, TOTVS dominates the mid-market through localized tax engines, while Vision 2030 public projects galvanize demand in the Middle East. Africa remains nascent, yet records lift from mobile-first public-sector tenders.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- IFS AB

- Unit4 N.V.

- Acumatica, Inc.

- Sage Group plc

- Syspro (Pty) Ltd.

- QAD Inc.

- Deltek, Inc.

- Aptean, Inc.

- Plex Systems, Inc.

- Rootstock Software, Inc.

- Priority Software Ltd.

- Workday, Inc.

- Odoo SA

- Ramco Systems Limited

- TOTVS S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Cloud Adoption Among Enterprises

- 4.2.2 Adoption of AI-Embedded ERP Suites

- 4.2.3 Demand for Integrated Supply-Chain Visibility

- 4.2.4 Regulatory Mandates for Real-Time Financial Reporting

- 4.2.5 SAP ECC 2027 End-of-Support Driving Replacement Cycles

- 4.2.6 Two-Tier ERP Strategies Fueling Niche Vendor Growth

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs and Budget Overruns

- 4.3.2 Data Security and Privacy Concerns in Cloud ERP

- 4.3.3 Shortage of ERP-Qualified Implementation Talent

- 4.3.4 Interoperability Challenges in Composable Architectures

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

- 4.9 Analysis on Ecosystem Type

- 4.9.1 Vendor-native marketplaces (SAP Store, Oracle Cloud Marketplace)

- 4.9.2 Partner ecosystems (system integrators, ISVs)

- 4.9.3 Open ecosystems (API-based, multi-ERP integrations)

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Component

- 5.3.1 Software Modules

- 5.3.2 Services

- 5.4 By Industry Vertical

- 5.4.1 Manufacturing

- 5.4.2 Retail and E-commerce

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Banking, Financial Services and Insurance

- 5.4.5 Professional Services

- 5.4.6 Public Sector

- 5.4.7 Other Industry Verticals

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 IFS AB

- 6.4.7 Unit4 N.V.

- 6.4.8 Acumatica, Inc.

- 6.4.9 Sage Group plc

- 6.4.10 Syspro (Pty) Ltd.

- 6.4.11 QAD Inc.

- 6.4.12 Deltek, Inc.

- 6.4.13 Aptean, Inc.

- 6.4.14 Plex Systems, Inc.

- 6.4.15 Rootstock Software, Inc.

- 6.4.16 Priority Software Ltd.

- 6.4.17 Workday, Inc.

- 6.4.18 Odoo SA

- 6.4.19 Ramco Systems Limited

- 6.4.20 TOTVS S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP管理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)企劃為基礎的企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP管理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)企劃為基礎的企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)