|

市場調查報告書

商品編碼

2065557

ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Enterprise Resource Planning Customization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

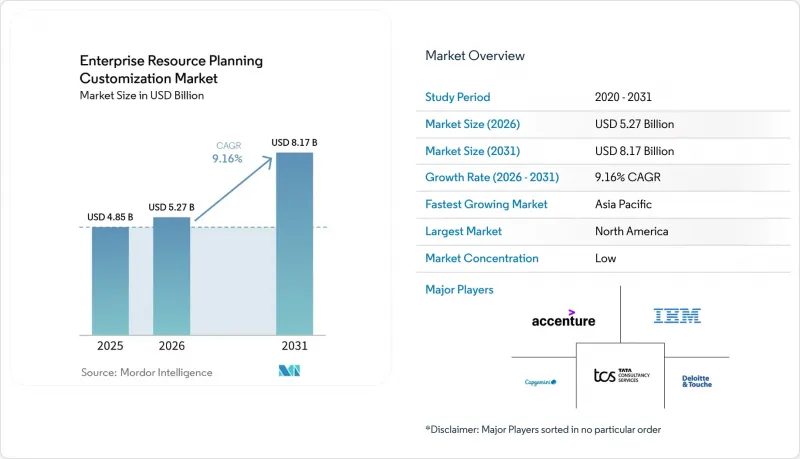

根據 Mordor Intelligence 預測,ERP 客製化服務市場規模預計將在 2025 年達到 48.5 億美元,2026 年達到 52.7 億美元,到 2031 年達到 81.7 億美元,2026 年至 2031 年的複合年成長率為 9.16%。

本報告按部署模式(本地部署、雲端部署、混合部署)、企業規模(大型企業、中小企業)、最終用戶行業(製造業、零售及電子商務、銀行、金融服務及保險業 (BFSI)、醫療保健業、資訊科技及電信業、其他)和地區進行細分。市場預測以美元 (USD) 為單位。

全球ERP客製化服務市場趨勢與洞察

對產業專用的ERP模組的需求日益成長

企業正從通用套件轉向垂直整合的功能,這些功能涵蓋現場遙測、監管報告引擎和病患資料工作流程。製造業實施者需要預測性維護和供應鏈可視性,而醫療保健提供者需要與電子健康記錄互通性。金融機構需要即時風險儀表板和自動化合規性。這種專業化趨勢正在加速模組化、API優先設計的普及,這種設計能夠保持ERP核心的簡潔性,並將大規模客製化轉移到鬆散耦合的擴充模組中。

加速推動「雲端優先」數位轉型策略

「雲端優先」策略將資本投資轉移到營運成本,從而實現持續升級並縮短引進週期。政府機構和大型企業越來越要求99.95%的服務等級協定 (SLA)、捆綁式安全工具和統一身分管理,這推動了超大規模資料中心業者和企業資源規劃 (ERP) 供應商之間的合作。隨著企業將基礎設施管理外包,客製化需求正轉向整合管治、財務營運 (FinOps) 視覺性以及針對每半年一次的雲端版本發布的主動回歸測試。

高昂的轉換成本阻礙了供應商遷移。

擁有高度客製化本地環境的組織面臨著資料傳輸成本、重新實施費用以及業務中斷的風險。主要ERP版本將於2027年12月停止支持,這加劇了問題的緊迫性,而人才短缺和諮詢費用飆升也使得大規模遷移變得困難。因此,企業選擇簡化舊版擴展,量化評估其帶來的收益,然後僅棄用、維修或重建最有價值的自訂物件。

細分市場分析

到2025年,雲端採用將佔ERP客製化服務市場59%的佔有率,預計到2031年將以14.10%的複合年成長率成長。這一轉變反映了市場對始終保持最新狀態的功能、嵌入式人工智慧以及付費使用制能夠降低整體擁有成本(TCO)。透過將低程式碼平台整合到雲端生態系中,企業可以將開發週期縮短高達70%,並釋放有限的開發資源。然而,混合環境仍然存在,某些對延遲敏感的操作和資料主權要求仍然需要本地部署,這增加了整合相關的開銷。

各行各業採用雲端ERP的組織都將自訂程式碼視為一種負擔,並推動向平台即服務 (PaaS) 層擴展,以保持升級路徑。雖然這種方法減少了技術債務,但也使多供應商授權管理變得更加複雜,從而催生了負責預測、監控和最佳化支出的財務營運中心 (FinOps)。因此,雲端相關服務中ERP客製化服務的市場規模成長速度超過了本地部署服務。同時,客戶要求在半年一次的版本發布之前,提供更嚴格的服務等級保證和自動化回歸測試。

區域分析

到2025年,北美將佔據ERP客製化服務市場35.70%的佔有率。這得歸功於雲端運算的成熟應用、聯邦政府嚴格的現代化要求以及遍布全球的系統整合商生態系統。聯邦機構正在評估商業案例的經濟效益,推動基於責任的安全模型,並強制要求對雲端託管的ERP系統進行持續監控。獲得國家醫療記錄和國防後勤現代化改造的契約,凸顯了該地區對大規模、人工智慧驅動的客製化服務的巨大需求。

預計到2031年,亞太地區將以14.80%的複合年成長率成長,主要得益於澳洲、印度和新加坡等國的自主雲端政策加速了本地託管、加密和合規工具的普及。公共雲端收入的快速成長、製造業境外外包以及數位銀行的普及,正在推動對客製化工作流程和整合加速器的支出。然而,由於與舊有系統的糾纏以及專業人才的短缺,混合部署模式(即核心系統遷移分階段進行,跨越多個預算週期)仍然十分常見。

在歐洲,受GDPR合規性、工業自動化以及現有ERP版本即將停止支援等因素的推動,市場呈現穩定但緩慢的成長態勢。尤其德國、法國和英國,由於諮詢顧問嚴重短缺,正面臨人事費用飆升和專案週期延長的雙重困境。北歐國家正著力推動雲原生擴展和分析,而南歐國家則在預算限制下分階段進行轉型。在南美、中東和非洲等新興地區,需求正逐漸成長,但基礎建設差異和外匯波動限制短期擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對產業特定ERP模組的需求日益成長

- 加速推動「雲端優先」數位轉型策略

- 中小企業對訂閱式ERP套件的採用率不斷提高。

- 實施後對超護理服務的需求(一個研究不足的領域)

- 向可組合 ERP 架構的過渡(這一趨勢尚未引起太多關注)。

- 低程式碼平台在客製化工作流程中的應用日益廣泛(一個被忽視的趨勢)

- 市場限制因素

- 高昂的轉換成本阻礙了供應商轉換。

- 認證ERP功能顧問短缺

- 人們越來越關注資料居住要求的合規性問題(未公開的問題)。

- 遺留客製化導致的技術債(常常被忽視)

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 現場

- 雲

- 混合

- 按公司規模

- 大公司

- 小型企業

- 按最終用途行業分類

- 製造業

- 零售與電子商務

- 銀行、金融服務和保險(BFSI)

- 衛生保健

- IT/通訊

- 政府/公共部門

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- Deloitte Touche Tohmatsu Limited

- Capgemini SE

- Tata Consultancy Services Limited

- Infosys Limited

- International Business Machines Corporation

- Cognizant Technology Solutions Corporation

- Wipro Limited

- HCL Technologies Limited

- Atos SE

- DXC Technology Company

- Tech Mahindra Limited

- NTT DATA Corporation

- CGI Inc.

- Larsen and Toubro Infotech Ltd(LTI Mindtree)

- EPAM Systems Inc.

- Rackspace Technology Inc.

- Hitachi Consulting Co., Ltd.

- Syntax Systems Ltd.

- Vision33 Inc.

第7章 市場機會與未來展望

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對產業特定ERP模組的需求日益成長

- 加速推動「雲端優先」數位轉型策略

- 中小企業對訂閱式ERP套件的採用率不斷提高。

- 實施後對超護理服務的需求(一個研究不足的領域)

- 向可組合 ERP 架構的過渡(這一趨勢尚未引起太多關注)。

- 低程式碼平台在客製化工作流程中的應用日益廣泛(一個被忽視的趨勢)

- 市場限制因素

- 高昂的轉換成本阻礙了供應商轉換。

- 認證ERP功能顧問短缺

- 人們越來越擔心資料居住要求的合規性問題(未公開的問題)

- 遺留客製化導致的技術債(常常被忽視)

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 現場

- 雲

- 混合

- 按公司規模

- 大公司

- 小型企業

- 按最終用途行業分類

- 製造業

- 零售與電子商務

- 銀行、金融服務和保險(BFSI)

- 衛生保健

- IT/通訊

- 政府/公共部門

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- Deloitte Touche Tohmatsu Limited

- Capgemini SE

- Tata Consultancy Services Limited

- Infosys Limited

- International Business Machines Corporation

- Cognizant Technology Solutions Corporation

- Wipro Limited

- HCL Technologies Limited

- Atos SE

- DXC Technology Company

- Tech Mahindra Limited

- NTT DATA Corporation

- CGI Inc.

- Larsen and Toubro Infotech Ltd(LTI Mindtree)

- EPAM Systems Inc.

- Rackspace Technology Inc.

- Hitachi Consulting Co., Ltd.

- Syntax Systems Ltd.

- Vision33 Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the enterprise resource planning customization services market size is projected to be USD 4.85 billion in 2025, USD 5.27 billion in 2026, and reach USD 8.17 billion by 2031, growing at a CAGR of 9.16% from 2026 to 2031.

This report is Segmented by Deployment Mode (On-Premise, Cloud, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium Enterprises), End-Use Industry (Manufacturing, Retail and E-Commerce, Banking, Financial Services and Insurance (BFSI), Healthcare, Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Resource Planning Customization Market Trends and Insights

Rising Demand for Industry-Specific ERP Modules

Enterprises are moving away from generic suites toward vertical capabilities that embed shop-floor telemetry, regulatory reporting engines, and patient data workflows. Manufacturing adopters seek predictive maintenance and supply-chain visibility, while healthcare providers require seamless interoperability with electronic health records. Financial institutions demand real-time risk dashboards and compliance automation. This push toward specialization accelerates the adoption of modular, API-first designs that keep the ERP core clean and shift heavy customization to loosely coupled extensions.

Acceleration of Cloud-First Digital Transformation Strategies

Cloud-first mandates convert capital expenditure into operating expenditure, enable evergreen upgrades, and shorten deployment cycles. Government agencies and large enterprises increasingly stipulate 99.95% service-level agreements, bundled security tooling, and unified identity management, prompting partnerships between hyperscalers and ERP vendors. As enterprises offload infrastructure management, customization requirements pivot toward integration governance, FinOps visibility, and proactive regression testing for biannual cloud releases.

High Switching Costs Limiting Vendor Migration

Organizations with heavily customized on-premises landscapes face data-egress fees, reimplementation costs, and potential business disruption. The December 2027 end-of-support for a major ERP release magnifies urgency, but talent scarcity and consulting rate inflation complicate large-scale moves. Enterprises are therefore cataloging legacy extensions, quantifying realized benefits, and choosing to retire, retrofit, or rebuild only the highest-value custom objects.

Other drivers and restraints analyzed in the detailed report include:

- Growing SME Adoption of Subscription-Based ERP Suites

- Demand for Post-Implementation Hyper-Care Services

- Shortage of Certified ERP Functional Consultants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 59% of the Enterprise Resource Planning Customization Services market share in 2025 and are on track for a 14.10% CAGR through 2031. The shift reflects demand for evergreen functionality, built-in AI, and consumption-based pricing that lowers total cost of ownership. Enterprises integrate low-code platforms within cloud ecosystems, trimming development cycles by up to 70% and freeing scarce developer capacity. However, hybrid estates persist where latency-sensitive operations or data-sovereignty mandates require local hosting, adding integration overhead.

Across industries, organizations adopting cloud ERP treat custom code as a liability, pushing extensions to platform-as-a-service layers that preserve upgrade paths. This approach reduces technical debt but introduces multi-vendor licensing complexity, prompting the rise of FinOps centers that forecast, monitor, and optimize spend. The Enterprise Resource Planning Customization Services market size for cloud-related services is therefore expanding faster than for on-premise work, even as clients demand stricter service-level guarantees and automated regression testing ahead of each biannual release.

Geography Analysis

North America accounted for 35.70% of the Enterprise Resource Planning Customization Services market in 2025, supported by mature cloud adoption, stringent federal modernization mandates, and a dense ecosystem of global systems integrators. Federal agencies evaluate business-case economics, enforce shared-responsibility security models, and require continuous monitoring of cloud-hosted ERP systems. Contract wins surrounding national health-record modernization and defense logistics confirm the region's appetite for large-scale, AI-enabled customizations.

Asia-Pacific is projected to expand at a 14.80% CAGR to 2031 as sovereign-cloud policies in Australia, India, and Singapore spur localized hosting, encryption, and compliance tooling. Rapid growth in public-cloud revenue, manufacturing offshoring, and digital banking adoption fuels spending on tailored workflows and integration accelerators. Nevertheless, legacy entanglement and specialist talent shortages often trigger hybrid rollouts that phase core-system migrations across multiple budget cycles.

Europe shows steady, if moderated, growth driven by GDPR alignment, industrial automation, and impending end-of-support deadlines for incumbent ERP releases. A significant consultant shortfall inflates labor rates and lengthens project timelines, especially in Germany, France, and the United Kingdom. Northern markets emphasize cloud-native extensions and analytics, while Southern Europe leans on phased, budget-constrained transformations. Emerging regions such as South America, the Middle East, and Africa generate incremental demand, though infrastructure gaps and currency volatility temper near-term scale.

- Accenture plc

- Deloitte Touche Tohmatsu Limited

- Capgemini SE

- Tata Consultancy Services Limited

- Infosys Limited

- International Business Machines Corporation

- Cognizant Technology Solutions Corporation

- Wipro Limited

- HCL Technologies Limited

- Atos SE

- DXC Technology Company

- Tech Mahindra Limited

- NTT DATA Corporation

- CGI Inc.

- Larsen and Toubro Infotech Ltd (LTI Mindtree)

- EPAM Systems Inc.

- Rackspace Technology Inc.

- Hitachi Consulting Co., Ltd.

- Syntax Systems Ltd.

- Vision33 Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Industry-Specific ERP Modules

- 4.2.2 Acceleration of Cloud-First Digital Transformation Strategies

- 4.2.3 Growing SME Adoption of Subscription-Based ERP Suites

- 4.2.4 Demand for Post-Implementation Hyper-Care Services (Under-the-Radar)

- 4.2.5 Shift Toward Composable ERP Architecture (Under-the-Radar)

- 4.2.6 Increasing Use of Low-Code Platforms for Tailored Workflows (Under-the-Radar)

- 4.3 Market Restraints

- 4.3.1 High Switching Costs Limiting Vendor Migration

- 4.3.2 Shortage of Certified ERP Functional Consultants

- 4.3.3 Rising Concerns Around Data Residency Compliance (Under-the-Radar)

- 4.3.4 Technical Debt From Legacy Customizations (Under-the-Radar)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By End-Use Industry

- 5.3.1 Manufacturing

- 5.3.2 Retail and E-Commerce

- 5.3.3 Banking, Financial Services and Insurance (BFSI)

- 5.3.4 Healthcare

- 5.3.5 Information Technology and Telecom

- 5.3.6 Government and Public Sector

- 5.3.7 Other End-Use Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Kenya

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Deloitte Touche Tohmatsu Limited

- 6.4.3 Capgemini SE

- 6.4.4 Tata Consultancy Services Limited

- 6.4.5 Infosys Limited

- 6.4.6 International Business Machines Corporation

- 6.4.7 Cognizant Technology Solutions Corporation

- 6.4.8 Wipro Limited

- 6.4.9 HCL Technologies Limited

- 6.4.10 Atos SE

- 6.4.11 DXC Technology Company

- 6.4.12 Tech Mahindra Limited

- 6.4.13 NTT DATA Corporation

- 6.4.14 CGI Inc.

- 6.4.15 Larsen and Toubro Infotech Ltd (LTI Mindtree)

- 6.4.16 EPAM Systems Inc.

- 6.4.17 Rackspace Technology Inc.

- 6.4.18 Hitachi Consulting Co., Ltd.

- 6.4.19 Syntax Systems Ltd.

- 6.4.20 Vision33 Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP管理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)企劃為基礎的企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP管理服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)企劃為基礎的企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)