|

市場調查報告書

商品編碼

2063423

人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)AI-Integrated Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

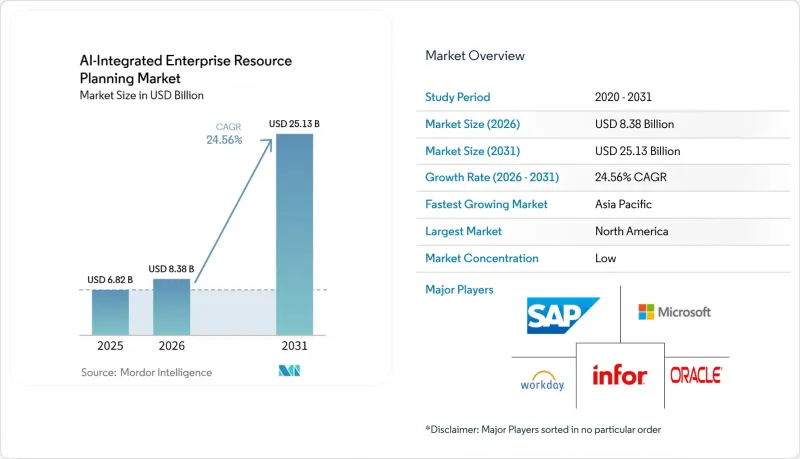

根據 Mordor Intelligence 預測,人工智慧整合 ERP(企業資源計畫)市場規模將從 2026 年的 83.8 億美元成長到 2031 年的 251.3 億美元,2026 年至 2031 年的複合年成長率為 24.56%。

本報告按部署模式(雲端、本地部署、混合部署)、組件(軟體和服務)、企業規模(大型企業和中小企業)、行業(製造業、銀行、金融和保險業、其他)、業務職能(財務和會計、其他)以及地區進行細分。市場預測以美元計價。

全球人工智慧整合ERP(企業資源計畫)市場趨勢與洞察

向融合人工智慧的雲端原生ERP系統轉型正在加速。

全球性公司通常在總部維護一個 SAP S/4HANA 或 Oracle Fusion 實例,而在其子公司部署更輕量級、更靈活的雲端套件,例如 NetSuite 或 Microsoft Dynamics 365 Business Central。這種中心輻射型架構兼顧了全球財務整合和區域營運柔軟性。預先配置的範本整合了製造、分銷或服務工作流程,簡化了部署流程,使區域實體運作。這相比傳統的全面部署(通常需要一年以上)有了顯著改善。此外,夜間同步確保了符合轉讓定價法規,同時本地團隊保留了更改採購規則的權限,而無需觸發總部層級的變更管理流程。這種方法使組織能夠在保持集中監管的同時,提高區域層面的適應性。

供應鏈中斷背景下對即時預測分析的需求

為了提高營運效率,製造商和零售商正擴大將港口擁塞、極端天氣預警和地緣政治指標等外部訊號直接整合到其計畫引擎中。這些預測模型使企業能夠主動調整生產計劃、重新安排運輸路線並重新調整安全庫存,從而防止缺貨演變成更大的混亂。例如,一些汽車和消費性電子產品製造商已經實施了與人工智慧驅動的企業資源計畫 (ERP) 系統整合的即時視覺化平台,並成功地將計畫週期縮短了三分之一。此外,這些公司也大幅降低了緊急交付成本,充分展現了這種整合帶來的實質效益。這種新方法正在將傳統的儀錶板從單純的狀態指示工具轉變為能夠自主執行糾正措施的複雜指令引擎,從而簡化決策流程並提高整個供應鏈的韌性。

受監管行業對高級資料安全和合規性的擔憂

醫療保健和銀行業營運商需要證明訓練資料始終保留在獲準的司法管轄區內,且審計追蹤符合 GDPR、HIPAA 和 SOX 等法規的要求。這確保了敏感資料得到安全透明的處理。然而,為了回應監管方面的擔憂,許多機構在進行 AI 產生的日誌條目的同時,也會進行人工審核。雖然這些審核旨在建立與監管機構的信任,但它們往往會削弱 AI 自動化所帶來的效率提升。為了克服這些挑戰,新興的聯邦學習技術提供了一種潛在的解決方案,它允許在本地進行模型訓練,而無需跨司法管轄區傳輸敏感資料。儘管聯邦學習具有巨大的潛力,但其大規模應用仍然有限,只有少數企業套件成功實現了該技術。

細分市場分析

由於受監管企業需要將敏感記錄保存在內部防火牆內,並且要求現場設備具備毫秒級的回應速度,因此,到2025年,本地部署仍佔市場收入的72.13%。然而,預計到2031年,雲端部署中整合人工智慧的企業資源規劃(ERP)市場將以25.16%的複合年成長率成長。由於供應商將尖端的協同駕駛功能限制在SaaS版本中,財務經理通常會推動模組的分階段遷移,即使核心帳簿仍保留在本地。

混合模式將本地資料湖與基於雲端的分析沙箱結合。在資料居住法律嚴格的亞洲國家,企業擴大將個人資料儲存在國內雲端,同時將匿名資料集發送到全球其他地區用於人工智慧訓練。隨著更多成功的概念驗證(PoC) 專案湧現,經營團隊越來越傾向於在非工作時間將敏感工作負載部署到外部外部部署,加速了整個人工智慧整合 ERP 市場的轉型。

大型製造商使用可程式邏輯控制器 (PLC) 和監控與資料擷取 (SCADA) 系統,這些系統會產生各自專有格式的資料。雖然這些系統對於自動化和監控工業流程至關重要,但它們產生的資料通常需要一個轉換層來確保與企業資源計劃 (ERP) 系統的兼容性。通常,這些客製化編碼的轉換層對於預測性維護代理與 ERP 工單模組的無縫整合至關重要。然而,開發和維護這些轉換層成本高昂,會顯著增加整合預算,有時甚至超過核心軟體本身的成本。此外,每次向系統引入新介面時,都可能因連接安全性差或協定過時而出現漏洞,從而構成潛在的網路安全風險。

為了因應這些挑戰,低程式碼整合中心應運而生,成為簡化異質系統間連結的解決方案。這些中心減少了對大規模自訂編碼的需求,使企業能夠簡化整合工作並降低相關成本。然而,在緩解部分挑戰的同時,它們也帶來了自身的問題,例如額外的授權費用以及需要健全的管治框架來確保合規性和安全性。因此,製造商必須仔細評估傳統自訂編碼解決方案和低程式碼平台之間的利弊,以在最佳化營運的同時降低風險。

區域分析

預計到2025年,北美將佔全球收入的37.89%,這主要得益於公共部門現代化以及零售和醫療保健行業積極的雲端遷移。光是美國聯邦政府的項目就涉及數十億美元的契約,合約期限長達十年。加拿大「雲端優先」的採購規則進一步擴大了人工智慧整合企業資源規劃(ERP)市場的潛力,並加速了資料居住管理在地化的諮詢專案。墨西哥的近岸外包熱潮正促使汽車零件製造商採用雙層架構,將當地工廠與其美國總部連接起來。

預計亞太地區2026年至2031年的複合年成長率將達25.56%,為全球最快成長速度。日本的補貼制度正在減輕中小型製造商的許可費負擔;印尼的資料在地化法鼓勵全球供應商在國內設立分支機構;印度的強制性稅務數位化正在加速中型企業的系統升級。中國的法規強制要求建立國內資料中心,這推動了全球軟體供應商與國內超大規模資料中心業者資料中心營運商之間的合資企業。在澳洲和韓國,網路安全和災害復原認證日益受到重視,促使相關區域預算進一步增加。

在歐洲,由於合規法規碎片化導致決策週期延長,成長速度較為緩慢。英國多部門SAP遷移計畫清楚展現了跨部門專案的複雜性。德國製造商正在部署人工智慧代理,以根據新的邊境調節機制追蹤碳足跡;法國醫療保健系統則在本地託管服務可用後首次採用雲端ERP系統。西班牙和義大利正在加速推進電子帳單升級,北歐國家則致力於尋找綠色資料中心。在南美、中東和非洲,整體規模較小,但差距正在迅速縮小,尤其是在政府強制推行即時電子帳單(需要整合稅務邏輯)的地區。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 向融合人工智慧的雲端原生ERP系統轉型正在加速。

- 供應鏈中斷背景下對即時預測分析的需求

- 在跨國公司的子公司實施雙層ERP系統

- 人工智慧可以減少實施時間和成本。

- 中型企業對可嵌入式低程式碼ERP模組的需求

- 政府對數位轉型的強制性要求和獎勵

- 市場限制因素

- 受監管行業對資料安全和合規性的強烈擔憂

- 與舊有系統和邊緣系統整合的複雜性。

- 具備人工智慧技能的ERP實施人員短缺

- 供應商鎖定和訂閱成本飆升

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 雲

- 現場

- 混合

- 按組件

- 軟體

- 服務

- 按公司規模

- 大公司

- 小型企業

- 按行業分類

- 製造業

- BFSI

- 衛生保健

- 零售和分銷

- 資訊科技/通訊

- 政府/公共產業

- 其他工業部門

- 業務職能

- 財會

- 人力資源管理

- 供應鍊和物流

- 客戶關係管理

- 庫存和工單管理

- 其他業務職能

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Sage Group Plc

- Infor Inc.

- Epicor Software Corporation

- Acumatica, Inc.

- Workday, Inc.

- Priority Software Ltd.

- Odoo SA

- QAD Inc.

- Ramco Systems Limited

- Plex Systems, Inc.

- SYSPRO(Pty)Ltd.

- Rootstok Software

- Deltek, Inc.

- Zoho Corporation Pvt. Ltd.

- IFS AB

- Unit4 NV

第7章 市場機會與未來展望

According to Mordor Intelligence, the aI-integrated enterprise resource planning market size is expected to increase from USD 8.38 billion in 2026 to reach USD 25.13 billion by 2031, growing at a CAGR of 24.56% over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Component (Software and Services), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (Manufacturing, BFSI, and More), Business Function (Finance and Accounting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Integrated Enterprise Resource Planning Market Trends and Insights

Accelerated Migration to Cloud-Native ERP With Embedded AI

Global corporations typically maintain a single instance of SAP S/4HANA or Oracle Fusion at their headquarters while equipping subsidiaries with lighter, more agile cloud suites such as NetSuite or Microsoft Dynamics 365 Business Central. This hub-and-spoke architecture balances global financial consolidation with localized operational flexibility. Pre-configured templates streamline deployment by packaging manufacturing, distribution, or service workflows, enabling regional entities to achieve go-live in less than 4 months. This is a significant improvement over the year or more typically required for a full-scale rollout. Additionally, nightly synchronization ensures compliance with transfer pricing regulations, while local teams retain the ability to modify procurement rules without triggering corporate-level change control processes. This approach allows organizations to maintain centralized oversight while fostering adaptability at the regional level.

Demand for Real-Time Predictive Analytics in Supply Chain Disruptions

Manufacturers and retailers are increasingly integrating external signals such as port-congestion updates, extreme-weather alerts, and geopolitical indices directly into their planning engines to enhance operational efficiency. These predictive models enable businesses to proactively reschedule production, reroute freight, and rebalance safety stock, preventing shortages from escalating into larger disruptions. For instance, automotive and consumer-electronics companies that have implemented real-time visibility platforms connected to AI-integrated enterprise resource planning market deployments have successfully reduced planning cycles by one-third. Additionally, these companies have significantly reduced expedited shipping costs, demonstrating the tangible benefits of such integrations. This emerging practice is transforming traditional dashboards from merely providing descriptive views into advanced prescriptive engines capable of autonomously executing corrective actions, thereby streamlining decision-making processes and improving overall supply chain resilience.

High Data-Security and Compliance Concerns in Regulated Industries

Healthcare and banking entities are required to demonstrate that training data remains confined within approved jurisdictions and that audit trails comply with regulations such as GDPR, HIPAA, or SOX. This ensures that sensitive data is handled securely and transparently. However, to address regulatory concerns, many organizations implement parallel manual reviews alongside AI-generated journal entries. These reviews are intended to build trust with regulators but often undermine the efficiency gains promised by AI automation. To overcome these challenges, emerging federated-learning techniques offer a potential solution by enabling local model training without transferring sensitive data across jurisdictions. Despite its promise, the adoption of federated learning at scale remains limited, as few enterprise suites have successfully operationalized it.

Other drivers and restraints analyzed in the detailed report include:

- Two-Tier ERP Adoption Among Multinational Subsidiaries

- AI-Driven Reduction in Implementation Time and Cost

- Integration Complexity With Legacy and Edge Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises installations retained 72.13% of 2025 revenue because regulated enterprises keep sensitive records within corporate firewalls and require millisecond-level response times for shop-floor equipment. The AI-integrated enterprise resource planning market size for cloud deployments, however, is projected to climb at a 25.16% CAGR to 2031. Vendors reserve the most advanced copilots for SaaS editions, so financial controllers often champion gradual module migrations even when core ledgers stay on-site.

Hybrid approaches combine local data lakes with cloud analytics sandboxes. Asian organizations in countries with stringent data-residency laws increasingly store personal data on sovereign clouds while pushing anonymized datasets to global regions for AI training. As more proofs of concept succeed, boardrooms become more comfortable staging sensitive workloads off-premises during non-business hours, accelerating broader migration waves across the AI-integrated enterprise resource planning market.

Large manufacturers use programmable logic controllers (PLCs) and supervisory control and data acquisition (SCADA) systems that generate data in proprietary formats. These systems are critical for automating and monitoring industrial processes, but the data they produce often requires translation layers to be compatible with enterprise resource planning (ERP) systems. These translation layers, frequently custom-coded, are essential for enabling predictive maintenance agents to seamlessly integrate with ERP work-order modules. However, the development and maintenance of these layers can significantly increase integration budgets, often surpassing the costs of the core software itself. Additionally, each new interface introduced into the system poses a potential cybersecurity risk, as vulnerabilities can arise from poorly secured connections or outdated protocols.

To address these challenges, low-code integration hubs have emerged as a solution to simplify connecting disparate systems. These hubs reduce the need for extensive custom coding, allowing businesses to streamline integration efforts and lower associated costs. However, while they alleviate some of the pain points, they also come with their own set of challenges, including additional licensing fees and the need for robust governance frameworks to ensure compliance and security. As a result, manufacturers must carefully evaluate the trade-offs between traditional custom-coded solutions and low-code platforms to optimize their operations while mitigating risks.

Geography Analysis

North America accounted for 37.89% of 2025 revenue, driven by public-sector modernizations and aggressive cloud migrations across retail and healthcare. United States federal programs alone represent multi-billion-dollar deals that span a decade. Canadian cloud-first procurement rules further expand the addressable AI-integrated enterprise resource planning market and fuel consulting engagements that localize data-residency controls. Mexico's nearshoring boom entices automotive suppliers to adopt two-tier architectures linking local plants with U.S. headquarters.

Asia-Pacific is set to record a 25.56% CAGR from 2026-2031, the fastest pace worldwide. Japanese subsidies help small manufacturers offset license fees, Indonesian data-localization laws push global vendors to open domestic regions, and Indian tax-digitization mandates accelerate mid-market upgrades. Chinese regulations require in-country data centers, steering deals to joint ventures between global publishers and domestic hyperscalers. Australia and South Korea emphasize cybersecurity and disaster recovery certifications, further expanding regional budgets.

Europe grows more slowly because fragmented compliance rules prolong decision cycles. The United Kingdom's multi-department SAP migration illustrates the complexity of cross-agency programs. German manufacturers add AI agents to track carbon footprints in line with new border-adjustment mechanisms, while French health systems adopt cloud ERP only after local hosting becomes available. Spain and Italy accelerate e-invoicing upgrades, and the Nordics emphasize green-data-center sourcing. South America, the Middle East, and Africa collectively represent a smaller but fast-closing gap, especially where governments introduce real-time e-invoice mandates that require embedded tax logic.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Sage Group Plc

- Infor Inc.

- Epicor Software Corporation

- Acumatica, Inc.

- Workday, Inc.

- Priority Software Ltd.

- Odoo SA

- QAD Inc.

- Ramco Systems Limited

- Plex Systems, Inc.

- SYSPRO (Pty) Ltd.

- Rootstok Software

- Deltek, Inc.

- Zoho Corporation Pvt. Ltd.

- IFS AB

- Unit4 N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Migration to Cloud-Native ERP with Embedded AI

- 4.2.2 Demand for Real-Time Predictive Analytics in Supply Chain Disruptions

- 4.2.3 Two-Tier ERP Adoption among Multinational Subsidiaries

- 4.2.4 AI-Driven Reduction in Implementation Time and Cost

- 4.2.5 Mid-Market Appetite for Composable Low-Code ERP Modules

- 4.2.6 Government Digital Transformation Mandates and Incentives

- 4.3 Market Restraints

- 4.3.1 High Data-Security and Compliance Concerns in Regulated Industries

- 4.3.2 Integration Complexity with Legacy and Edge Systems

- 4.3.3 Shortage of AI-Skilled ERP Implementation Talent

- 4.3.4 Vendor Lock-In and Escalating Subscription Costs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Industry Vertical

- 5.4.1 Manufacturing

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Retail and Distribution

- 5.4.5 IT and Telecom

- 5.4.6 Government and Utilities

- 5.4.7 Other Industry Verticals

- 5.5 By Business Function

- 5.5.1 Finance and Accounting

- 5.5.2 Human Resource Management

- 5.5.3 Supply Chain and Logistics

- 5.5.4 Customer Relationship Management

- 5.5.5 Inventory and Work Order Management

- 5.5.6 Other Business Functions

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.2.4 Saudi Arabia

- 5.6.5.2.5 Rest of Middle East

- 5.6.5.3 Africa

- 5.6.5.3.1 South Africa

- 5.6.5.3.2 Egypt

- 5.6.5.3.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Sage Group Plc

- 6.4.5 Infor Inc.

- 6.4.6 Epicor Software Corporation

- 6.4.7 Acumatica, Inc.

- 6.4.8 Workday, Inc.

- 6.4.9 Priority Software Ltd.

- 6.4.10 Odoo SA

- 6.4.11 QAD Inc.

- 6.4.12 Ramco Systems Limited

- 6.4.13 Plex Systems, Inc.

- 6.4.14 SYSPRO (Pty) Ltd.

- 6.4.15 Rootstok Software

- 6.4.16 Deltek, Inc.

- 6.4.17 Zoho Corporation Pvt. Ltd.

- 6.4.18 IFS AB

- 6.4.19 Unit4 N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年 供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)

供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031) 企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測東協企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測東協企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)