|

市場調查報告書

商品編碼

2063405

供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Supply Chain Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

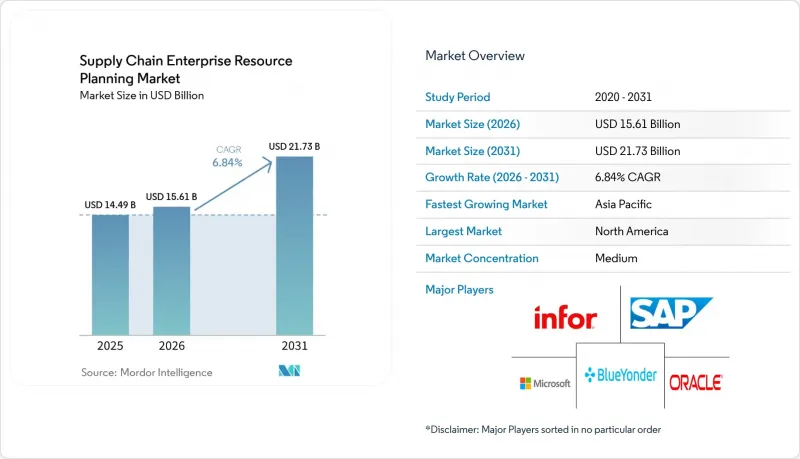

據 Mordor Intelligence 稱,2025 年供應鏈 ERP(企業資源計畫)市值為 144.9 億美元,預計到 2031 年將達到 217.3 億美元,而 2026 年為 156.1 億美元,預測期(2026-2031 年)的複合年成長率為 6.84%。

本報告按元件(軟體和服務)、部署類型(雲端、本地部署、混合部署)、最終用戶產業(製造業、消費品、醫療保健/製藥、食品飲料等)、組織規模(大型企業、中小企業)和地區進行細分。市場預測以美元計價。

全球供應鏈ERP(企業資源計畫)市場趨勢與洞察

一級ERP套件的雲端優先遷移

一級供應商正在設定雄心勃勃的雲端採用里程碑,承諾提供持續的功能、強大的模擬能力以及與第三方物流的輕鬆整合。雖然遷移通常會在五年內適度降低總體擁有成本 (TCO),但隱藏的資料清理和流程重組工作往往會延長專案工期。供應商會捆綁自動化遷移工具包和固定價格套餐以減少摩擦,但客戶越來越要求簽訂與運作里程碑掛鉤的、基於結果的合約。此外,向雲端解決方案的遷移正在推動服務交付模式的創新。供應鏈 ERP 市場供應商正在利用人工智慧 (AI) 和機器學習來增強預測分析能力,使企業能夠做出更有效的數據驅動決策。這一趨勢在製造業和零售業等行業尤為明顯,因為即時洞察對於最佳化營運至關重要。因此,企業越來越將雲端採用視為策略性投資,而不僅僅是節約成本的措施,以獲得競爭優勢。

人工智慧驅動的預測性供應鏈規劃

目前,機器學習演算法正在整合非結構化天氣資料、供應商郵件以及社群媒體的情緒分析,以最佳化需求預測並主動調整運輸路線。內建的輔助功能可適度減少人工資料輸入,使企業能夠在不影響服務水準的前提下維持更低的安全庫存。可靠性仍然依賴一致的歷史數據,這進一步推動了向統一的雲端原生環境的轉變。因此,企業越來越重視高階分析的投資,以提高營運效率和決策能力。

網路安全和資料主權合規成本

在歐盟、中國和印度等地區,資料儲存必須在本國境內,違規者將受到嚴厲處罰。因此,跨國公司需要在每個地區維護獨立的ERP系統,這導致基礎設施成本增加,主資料同步也變得複雜。零信任安全、多因素身份驗證和異常檢測等功能會使年度訂閱費用增加10-15%,對中型企業來說尤其沉重。此外,為了符合這些法規,企業通常需要投入大量資金升級IT基礎設施,以滿足當地標準。供應鏈ERP市場的趨勢正在推動對專業諮詢服務的需求,以幫助企業應對複雜的區域合規要求。

細分市場分析

供應鏈ERP(企業資源計畫)市場的服務板塊正以7.24%的複合年成長率快速擴張,成長超過軟體板塊,主要得益於專案中對資料清洗、整合和變更管理的密集需求。實施和管理服務的合約越來越依賴訂單到收款週期等績效指標。即使到了2025年,軟體仍將佔據63.71%的市場佔有率,這主要得益於一級套件和支撐現代供應鏈網路的演算法規劃附加元件的訂閱收入。隨著旨在持續改進的長期服務合約的實施,顧問將在系統運作後長期駐場,從而將服務轉化為持續的收入來源。同時,軟體供應商透過將基礎支援和託管服務捆綁銷售,模糊了產品類別的界限,促使買家評估這兩項服務的真實成本。開放原始碼挑戰者則透過提供包含所有服務的定價方案來降低整體擁有成本,從而吸引中小企業的目光。

隨著市場不斷演變,企業越來越重視ERP解決方案的敏捷性和擴充性,以適應動態供應鏈的需求。供應商也積極回應,整合高階分析和人工智慧驅動的洞察功能,以增強決策能力。此外,模組化ERP系統的普及使企業能夠分階段部署功能,從而降低前期成本和實施風險。這一趨勢對預算有限但又需要強大解決方案以保持競爭力的中型企業尤其具有吸引力。對永續性和合規性的日益關注也在推動創新,ERP供應商正在整合相關功能,以追蹤碳足跡並確保符合監管要求。

到2025年,雲端運算將佔總營收的58.83%,預計到2031年將以每年7.44%的速度成長,這主要得益於超大規模資料中心業者提供的折扣以及模擬工作負載所需的彈性容量。在國防、公共產業和公共部門等領域,混合架構正在逐漸形成,敏感帳本保留在本地,而協作模組則部署在雲端。本地部署的使用率正在下降,但在那些空氣間隙安全性置於可擴展性之上的領域,本地部署仍然普遍存在。邊緣快取設備和區域資料中心正在緩解延遲和資料儲存方面的挑戰,從而提升了雲端運算在頻寬受限地區的吸引力。訂閱模式也使得初始成本的分攤更加均衡,這對於面臨資本預算限制的製造商來說尤其有利。因此,雲端運算的採用率預計將比預期更早超過新增採用量的70%,這將進一步改變供應商的收入結構。

此外,將人工智慧 (AI) 和機器學習 (ML) 等先進技術整合到基於雲端的 ERP 系統中,正在提升各行業的營運效率。這些技術能夠實現即時數據分析、預測性洞察和自動化決策,對於希望在瞬息萬變的市場中保持競爭力的企業至關重要。此外,對永續發展的日益關注也促使企業採用能夠最佳化能耗並減少碳足跡的雲端解決方案。供應商正在擴展其綠色雲端服務產品,以契合企業的環境、社會和管治(ESG) 目標,預計這將進一步加速預測期內雲端技術的普及應用。

區域分析

北美在人工智慧驅動的規劃和美國近岸製造方面處於領先地位,預計到2025年將佔據36.18%的市場佔有率,繼續保持最大區域貢獻者的地位。加拿大生產商正在實施ERP系統以滿足出口原產地文件要求,而墨西哥的加工廠(出口加工廠)正在升級其系統,以管理涵蓋國內和美國供應商的雙重採購模式。 5G連接的普及和超大規模資料中心業者資料中心密度的不斷提高,使得即時控制塔儀錶板成為可能,從而縮短了對供應鏈中斷的響應時間。

亞太地區正處於最具活力的成長軌道上,預計在預測期內將實現7.84%的複合年成長率。在印度,商品和服務稅(GST)申報正透過合規模板自動化,甚至中型企業也開始拋棄電子表格。日本的大型企業集團正在逐步淘汰本地部署系統,因為國內雲端供應商能夠確保低延遲的可用區域。在中國,一項由政府主導的系統替換宣傳活動正在幫助企業遷移到本地管理的ERP系統,這些系統都已通過嚴格的網路安全審計,且不會影響與全球供應鏈網路的整合。

在歐洲,監管合規與永續發展領導力之間取得了平衡。 ViDA電子帳單的引入實現了全部區域資料交換,而「數位產品護照」則要求製造商追蹤其從原料提取到廢棄產品回收的整個碳足跡。一家德國汽車零件供應商正在試點將基於區塊鏈的原產地證書直接整合到ERP系統中。一家北歐零售商正在實施一項翻新和轉售計劃,該計劃基於循環經濟理念,整合了退貨數據。東歐的工廠正在利用歐盟團結基金實現營運數位化,進一步提升了對模組化套件的需求。南美、中東和非洲的市場規模較小,但隨著各國政府投資數位基礎設施以及當地企業努力與跨國公司子公司競爭,這些市場正在穩步成長。預計到2025年,巴西的ERP採用率將超過33%,並且隨著政府推進稅務合規流程的數位化,預計這一比例還將進一步成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 一級ERP套件的雲端優先遷移

- 人工智慧驅動的預測性供應鏈規劃

- 可組合和模組化ERP架構的興起

- 近岸外包和供應鏈彈性計劃

- 永續性和範圍 3 碳排放追蹤義務

- 生成式人工智慧代理可自動完成從採購到付款的流程

- 市場限制因素

- 生成式人工智慧代理可自動完成從採購到付款的流程

- 網路安全和資料主權合規成本

- 缺乏具備ERP專業知識的供應鏈人員。

- 對供應商鎖定和長期總擁有成本的擔憂

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按最終用戶行業分類

- 製造業

- 零售與電子商務

- 醫療和藥品

- 食品/飲料

- 消費品

- 按組織規模

- 大公司

- 小型企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- IFS AB

- QAD, Inc.

- Plex Systms, Inc.

- The Sage Group Plc

- SYSPRO(Proprietary)Ltd

- Acumatica, Inc.

- Unit4 NV

- Workday, Inc.

- Blue Yonder Group, Inc.

- Kinaxis Inc.

- E2open Parent Holdings, Inc.

- Manhattan Associates, Inc.

- Ramco Systems Ltd

- Odoo SA

- Aptean, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the supply chain enterprise resource planning market size was valued at USD 14.49 billion in 2025 and estimated to grow from USD 15.61 billion in 2026 to reach USD 21.73 billion by 2031, at a CAGR of 6.84% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), End-User Industry (Manufacturing, Consumer Goods, Healthcare and Pharmaceuticals, Food and Beverage, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Supply Chain Enterprise Resource Planning Market Trends and Insights

Cloud-First Migration of Tier-1 ERP Suites

Tier-1 vendors target aggressive cloud-adoption milestones, promising continuous feature delivery, elastic simulation capacity, and easier integration with third-party logistics. Migrations typically lower the five-year total cost of ownership by a moderate share, yet hidden data cleansing and process re-engineering work often extends project timelines. Vendors bundle automated migration toolkits and fixed-price packages to reduce friction, while customers increasingly insist on outcome-based contracts tied to go-live milestones. Additionally, the shift to cloud-based solutions is driving innovation in service delivery models. The supply chain ERP market vendors are leveraging artificial intelligence and machine learning to enhance predictive analytics, enabling businesses to make data-driven decisions more effectively. This trend is particularly evident in industries like manufacturing and retail, where real-time insights are critical for optimizing operations. As a result, companies are increasingly viewing cloud adoption not just as a cost-saving measure but as a strategic investment to gain a competitive edge.

AI-Enabled Predictive Supply Chain Planning

Machine-learning algorithms now ingest unstructured weather feeds, supplier emails, and social sentiment to fine-tune demand forecasts and proactively reroute shipments. Embedded copilots reduce manual data entry by up to a moderate share and enable enterprises to maintain leaner safety stock without eroding service levels. Reliability still hinges on harmonized historical data, giving an additional push toward unified, cloud-native environments. As a result, businesses are increasingly prioritizing investments in advanced analytics to enhance operational efficiency and decision-making.

Cyber-Security and Data-Sovereignty Compliance Costs

Jurisdictions such as the EU, China, and India demand in-country data storage and impose stiff penalties for violations. Multinationals, therefore, maintain region-specific ERP instances, thereby increasing infrastructure costs and complicating master data synchronization. Zero-trust security, multi-factor authentication, and anomaly detection add 10-15% to annual subscription fees, a burden felt most acutely by mid-market firms. Additionally, compliance with these regulations often requires significant investment in IT infrastructure upgrades to meet local standards. This trend, in the supply chain ERP market, is driving demand for specialized consulting services to navigate the complexities of regional compliance requirements.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Composable and Modular Architectures

- Near-Shoring and Resilience Programs

- Shortage of ERP-Skilled Supply-Chain Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The services slice of the supply chain enterprise resource planning market is expanding at a 7.24% CAGR, eclipsing software growth as projects require intensive data cleansing, integration, and change management. Implementation and managed-service contracts increasingly hinge on performance outcomes such as order-to-cash cycle days. Software still generated 63.71% of value in 2025, buoyed by subscription revenue from tier-1 suites and algorithmic planning add-ons that underpin modern supply networks. Continuous-improvement retainers now keep consultants embedded long after go-live, turning services into an annuity stream. Meanwhile, software providers blur category lines by bundling basic support and hosting, prompting buyers to evaluate true cost across both line items. Open-source challengers leverage all-inclusive pricing to cut total ownership costs and woo small and medium enterprises.

As the market evolves, enterprises increasingly prioritize agility and scalability in their ERP solutions to adapt to dynamic supply chain demands. Vendors are responding by integrating advanced analytics and AI-driven insights to enhance decision-making capabilities. Additionally, the shift toward modular ERP systems allows businesses to adopt functionalities incrementally, reducing upfront costs and implementation risks. This trend is particularly appealing to mid-market firms, which often face budget constraints but require robust solutions to remain competitive. The growing emphasis on sustainability and compliance further drives innovation, with ERP providers embedding features to track carbon footprints and ensure regulatory adherence.

Cloud installations accounted for 58.83% of 2025 revenue and are accelerating by 7.44% through 2031, propelled by hyperscaler discounts and elastic capacity for simulation workloads. Hybrid structures persist in defense, utilities, and public-sector contexts where sensitive ledgers remain on-premise while collaboration modules live in the cloud. On-premise adoption is declining, but endures where air-gapped security trumps scalability. Edge-caching appliances and regional data centers mitigate latency and residency hurdles, broadening cloud appeal in bandwidth-constrained territories. Subscription models also distribute cash outlays more evenly, an advantage for manufacturers juggling capital budgets. As a result, cloud footprints are expected to exceed 70% of new deployments well before the forecast horizon, further reshaping vendor economics.

Additionally, the integration of advanced technologies such as artificial intelligence (AI) and machine learning (ML) into cloud-based ERP systems is driving operational efficiencies across industries. These technologies enable real-time data analysis, predictive insights, and automated decision-making, which are critical for businesses aiming to stay competitive in dynamic markets. Furthermore, the growing emphasis on sustainability is pushing organizations to adopt cloud solutions that optimize energy consumption and reduce carbon footprints. Vendors are increasingly offering green cloud services, aligning with corporate environmental, social, and governance (ESG) goals, which is expected to further accelerate cloud adoption during the forecast period.

Geography Analysis

North America remains the single largest regional contributor, with a 36.18% share in 2025, anchored by the United States' drive toward AI-augmented planning and nearshore manufacturing. Canadian producers adopt ERP systems to meet export rules-of-origin documentation requirements, while Mexican maquiladoras upgrade systems to manage dual-sourcing models spanning domestic and U.S. suppliers. Widespread 5G connectivity and hyperscaler data-center density enable real-time control-tower dashboards, shrinking response times to supply disruptions.

Asia-Pacific posts the most dynamic growth trajectory with a CAGR of 7.84% over the forecast period. India's compliance-ready templates automate goods and services tax reporting, encouraging even mid-market firms to migrate away from spreadsheets. Japanese conglomerates are phasing out on-premises systems as domestic cloud vendors guarantee low-latency availability zones. In China, state-led substitution campaigns steer enterprises toward locally maintained ERP copies that pass stringent cybersecurity reviews, without sacrificing integration with global supply networks.

Europe balances regulatory compliance with sustainability leadership. The ViDA e-invoicing roll-out enables borderless data exchange across the region, while the Digital Product Passport requires manufacturers to trace their carbon footprint from raw extraction through end-of-life recycling. German automotive suppliers pilot blockchain-backed certificates of origin built directly into ERP line items. Nordic retailers incorporate circular-economy returns data, enabling refurbish and resale programs. Eastern European plants leverage EU cohesion funds to digitalize factories, adding incremental demand for modular suites. South America, the Middle East, and Africa are smaller markets but are steadily growing as governments invest in digital infrastructure and local enterprises aim to compete with multinational subsidiaries. Brazil's ERP adoption surpassed 33% in 2025, with further growth expected as the government digitizes tax compliance processes.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- IFS AB

- QAD, Inc.

- Plex Systms, Inc.

- The Sage Group Plc

- SYSPRO (Proprietary) Ltd

- Acumatica, Inc.

- Unit4 N.V.

- Workday, Inc.

- Blue Yonder Group, Inc.

- Kinaxis Inc.

- E2open Parent Holdings, Inc.

- Manhattan Associates, Inc.

- Ramco Systems Ltd

- Odoo SA

- Aptean, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-First Migration of Tier-1 ERP Suites

- 4.2.2 AI-Enabled Predictive Supply Chain Planning

- 4.2.3 Rise of Composable and Modular ERP Architectures

- 4.2.4 Near-shoring and Supply Chain Resilience Programs

- 4.2.5 Sustainability and Scope-3 Carbon-Tracking Mandates

- 4.2.6 Generative-AI Agents Automating Procure-to-Pay

- 4.3 Market Restraints

- 4.3.1 Generative-AI Agents Automating Procure-to-Pay

- 4.3.2 Cyber-Security and Data-Sovereignty Compliance Costs

- 4.3.3 Shortage of ERP-Skilled Supply-Chain Talent

- 4.3.4 Vendor Lock-In and Long-Term Total-Cost Concerns

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By End-User Industry

- 5.3.1 Manufacturing

- 5.3.2 Retail and E-commerce

- 5.3.3 Healthcare and Pharmaceuticals

- 5.3.4 Food and Beverage

- 5.3.5 Consumer Goods

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 IFS AB

- 6.4.7 QAD, Inc.

- 6.4.8 Plex Systms, Inc.

- 6.4.9 The Sage Group Plc

- 6.4.10 SYSPRO (Proprietary) Ltd

- 6.4.11 Acumatica, Inc.

- 6.4.12 Unit4 N.V.

- 6.4.13 Workday, Inc.

- 6.4.14 Blue Yonder Group, Inc.

- 6.4.15 Kinaxis Inc.

- 6.4.16 E2open Parent Holdings, Inc.

- 6.4.17 Manhattan Associates, Inc.

- 6.4.18 Ramco Systems Ltd

- 6.4.19 Odoo SA

- 6.4.20 Aptean, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年 醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)

醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031) 企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測東協企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測東協企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)