|

市場調查報告書

商品編碼

2063404

醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)Medical Device And MedTech Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

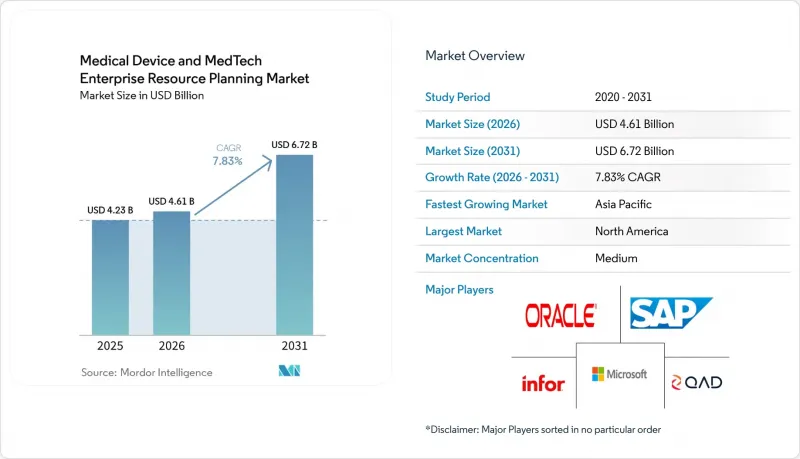

根據 Mordor Intelligence 預測,醫療設備和醫療技術 ERP(企業資源計畫)市場規模將從 2025 年的 42.3 億美元和 2026 年的 46.1 億美元成長到 2031 年的 67.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)率為 7.3%。

本報告按部署類型(雲端、本地部署、混合部署)、元件(軟體、服務)、組織規模(大型企業、中小企業)、最終用戶(醫療設備製造商、醫療技術服務供應商等)和地區進行細分。市場預測以美元計價。

全球醫療設備與醫療技術ERP(企業資源規劃)市場趨勢及洞察

對UDI和品質合規性的監管壓力日益加大

2026年5月28日是強制提交歐盟醫療器材資料庫(EUDAMED)醫療設備主資料、企業註冊資料和監測報告的截止日期。為此,ERP供應商正在發布原生連接器,可直接從產品生命週期模組傳輸序號和憑證。在美國,品質管理系統法規於2026年2月2日生效,要求電腦系統驗證必須符合ISO 13485:2016標準,並加強了對整合到ERP品質工作流程中的人工智慧模組的審查。為此, Oracle推出了醫療器材驗證程序,該程序提供預先驗證腳本,可將III類醫療設備製造商的安裝資格確認週期縮短一半。日本藥品和醫療器材管理局(PMDA)與ISO 13485標準的協調也增加了對多區域相容模板的需求,這些模板能夠在單一主資料層級結構中區分FDA、歐盟和日本的企業識別碼。總而言之,這些監管要求正在推動企業選擇能夠確保按季度進行監管合規性升級的平台。

一家中型醫療設備製造商遷移

訂閱定價模式起價為每位使用者每月 150 美元,大幅降低了先前本地部署所需的超過 200 萬美元的初始投資,使年收入在 5,000 萬美元至 5 億美元之間的公司能夠進入醫療設備和醫療技術 ERP(企業資源計畫)市場。 2025 年部署的 Microsoft Dynamics 365 整合了電子批次記錄和偏差工作流程,無需自訂程式碼即可符合 21 CFR Part 11 的要求。一家歐洲中型製造商利用預先配置的批次追蹤模板,僅用了九個月就實現了運作。同時,亞太地區的公司選擇混合雲端解決方案,將智慧財產權資料儲存在本地資料中心,以符合中國的資料安全法規。快速合規是另一個吸引人的特點。雖然 SaaS 供應商可以按季度提供新的 UDI 格式和 ISO 修訂版,但本地部署客戶通常每三年才進行一次升級。儘管如此,資料在地化法規仍在持續推動混合雲的需求,迫使供應商實現本地品管系統和雲端財務帳簿之間的低延遲同步。

高驗證成本與FDA電腦系統驗證成本

儘管FDA計劃在2024年過渡到基於風險的電腦軟體保證(CSA),但III類醫療設備製造商仍為每個ERP模組的部署、運作和效能合格測試累計約120萬美元。每次季度雲端更新都需要執行回歸測試腳本、進行影響評估並存檔已執行的測試證據,這導致發布週期延長和諮詢成本增加。歐盟也提出了類似的要求,要求審計追蹤記錄保留長達15年,這也推高了驗證成本。雲端供應商現在銷售驗證即服務(Validation-as-a-Service)套餐,Acumatica的承包文檔包售價15萬美元,但特定站點的工作流程以及與第三方系統的整合仍需要產生客製化的證據。對於一家年銷售額為5,000萬美元的製造商來說,這筆費用佔年銷售額的2.4%,這也凸顯了許多中小企業延後採用全套產品的原因。

細分市場分析

2025年,雲端採用率將佔醫療設備和醫療技術ERP(企業資源計畫)市場佔有率的54.98%,預計到2031年將以8.43%的複合年成長率成長,這主要得益於中型企業希望避免超過200萬美元的資料中心投資。供應商正利用「停止支援」來引導客戶轉向SaaS訂閱,例如SAP的ECC將於2027年停止支持, Oracle的E-Business Suite將於2030年停止支援。儘管如此,對於那些希望完全掌控軟體版本控制和檢驗腳本的跨國公司而言,本地部署環境的市場規模仍將保持。混合架構為受中國《資料安全法》和歐盟《一般資料保護規範》(GDPR)約束的組織提供了一種折衷方案,使它們能夠在本地維護高品質記錄,同時在全球雲端運作其規劃引擎。

Oracle的流程製造連接器每隔幾分鐘即可同步工廠車間的批次數據,從而消除了以往阻礙混合部署的延遲問題。微軟和第三方品質顧問提供基於風險的檢驗模板,可將運作時間縮短 40%,從而緩解 SaaS 發布週期帶來的負面影響。季度功能更新仍然要求製造商維護一支與時俱進的檢驗團隊,而本地部署客戶則可以整合變更並將其作為一項多年期的單一維修項目來實施。在所有部署模式下,買家現在都優先考慮網路安全狀況和法規遵循審計追蹤,而不是通用功能清單,評估標準也轉向自動化合規性。

到2025年,軟體授權和訂閱將佔市場收入的69.77%,但由於檢驗的日益複雜,服務業正以8.23%的複合年成長率成長。部署專案耗時12至18個月,檢驗工作佔計費工時的40%之多,迫使製造商將電腦軟體品質保證(CSA)文件外包給生命科學領域的專家。隨著客戶採用包含季度驗證、修補程式管理和法規監控服務的持續合規契約,託管服務市場正在不斷擴張。

Infosys 和 Tricentis 目前正將回歸測試自動化應用於 SAP S/4HANA 遷移過程中,從而減少了 40% 的測試案例產生量,並壓縮了整體專案預算。同樣,隨著製造商在遷移到多租戶雲端平台之前整合數十年的批次追蹤記錄,資料遷移諮詢業務也蓬勃發展。培訓是另一個亮點。品質工程師和供應鏈規劃人員需要不斷更新知識,才能在不違反驗證協議的前提下解讀 AI 產生的預測結果。隨著 AI 模組的整合日益完善且無需額外軟體成本,收入正轉向下游的諮詢、培訓和應用管理附加元件,以確保系統隨時準備接受審計。

區域分析

到2025年,北美將佔據38.39%的市場。這主要得益於美國食品藥物管理局(FDA)的嚴格監管以及眾多跨國醫療設備製造商的高度集中。新的品管系統法規要求企業重新檢驗其ERP系統,由此催生了「驗證即服務」(Validation-as-a-Service)檢驗的浪潮。併購後的重組,例如波士頓科學公司對Axonics的整合,凸顯了收購如何促進全套S/4HANA遷移,將超過16個製造地整合到一個全球統一的帳本之下。加拿大和墨西哥正在崛起為近岸契約製造中心,部署雲端ERP系統以滿足美國贊助商對即時可追溯性的要求。

亞太地區是成長最快的地區,預計到2031年將以8.83%的複合年成長率成長。中國對III類醫療設備(2024年)和II類醫療器材(2025年)實施的UDI (生產連結獎勵計畫(PLI)計畫向實施物聯網ERP系統的工廠提供高達其新增銷售額5%的補貼,從而加速新計畫中物聯網ERP系統的應用。韓國正在津貼感測器驅動的智慧工廠,而日本的「社會5.0」計畫則鼓勵二級供應商將物聯網和ERP系統整合,以實現ISO 13485合規性。

在醫療設備法規 (MDR) 和歐盟醫療器材指令 (EUDAMED) 2026 年 5 月實施期限的推動下,歐洲仍保持著較大的市場佔有率。這實際上迫使出口商對其 ERP 系統進行現代化改造。製造商們正爭分奪秒地回應 48 小時不利事件報告要求,他們越來越將即時可追溯性視為必需品,從而推動了對能夠將出貨狀態與缺陷機率關聯起來的 AI 模組的需求。南美和中東及非洲地區仍處於發展階段,但隨著當地工廠效仿其母公司的品質系統並努力成為全球品牌的首選供應商,相關實施工作正在穩步推進。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- UDI和品質合規性面臨的監管壓力日益增大

- 中型醫療技術公司遷移至雲端原生SaaS ERP

- 全球化供應鏈對即時可追溯性的需求日益成長。

- 將支援物聯網的現場數據與ERP平台整合

- 醫療設備業併購後系統整合激增

- 擴大人工智慧驅動的需求預測模組的應用

- 市場限制因素

- 高昂的驗證成本和FDA電腦系統驗證成本

- 網路安全問題正在減緩雲端ERP系統的普及。

- 醫療科技領域中小企業在ERP資料管治的技能差距

- 將傳統MES和ERP系統整合到現有工廠的複雜性

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按組件

- 軟體

- 服務

- 按組織規模

- 大公司

- 小型企業

- 最終用戶

- 醫療設備製造商

- 醫療技術服務供應商

- 契約製造組織

- 臨床研究機構

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- QAD Inc.

- Epicor Software Corporation

- Sage Group Plc

- IFS AB

- SYSPRO(Pty)Ltd.

- Plex Systems, Inc.

- Rootstock Software, Inc.

- Dassault Systemes SE

- Siemens Industry Software Inc.

- Korber Pharma Software GmbH

- Exact Holding BV

- Acumatica, Inc.

- Workday, Inc.

- Priority Software Ltd.

- Abas Software GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the medical device and MedTech enterprise resource planning market size is projected to expand from USD 4.23 billion in 2025 and USD 4.61 billion in 2026 to USD 6.72 billion by 2031, registering a CAGR of 7.83% between 2026 and 2031.

This report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Component (Software, and Services), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User (Medical Device Manufacturers, Medtech Service Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Medical Device And MedTech Enterprise Resource Planning Market Trends and Insights

Accelerating Regulatory Pressure for UDI and Quality Compliance

The May 28, 2026, deadline for mandatory EUDAMED submissions obliges manufacturers to load device master data, operator registrations, and vigilance reports into a central European database, prompting ERP vendors to release native connectors that populate serial numbers and certificates directly from product lifecycle modules. In the United States, the Quality Management System Regulation, which took effect on February 2, 2026, aligns computer system validation with ISO 13485:2016 and intensifies scrutiny of AI modules embedded in ERP quality workflows. Oracle responded with a Health Device Validation Program that ships pre-validated scripts, cutting in half the installation qualification cycles for Class III device makers. Japan's PMDA harmonization with ISO 13485 likewise boosts demand for multi-region templates capable of segregating FDA, EU, and Japanese establishment identifiers within a single master-data hierarchy. Collectively, these mandates nudge procurement decisions toward platforms that guarantee regulator-ready upgrades on a quarterly cadence.

Shift Toward Cloud-Native SaaS ERP Among Mid-Sized MedTech Firms

Subscription pricing that begins at USD 150 per user per month slashes the USD 2 million-plus capital outlay historically required for on-premise rollouts, bringing the Medical Device and MedTech enterprise resource planning market within reach of firms with USD 50 million to USD 500 million in annual sales. Microsoft's Dynamics 365 deployments during 2025 embedded electronic batch records and deviation workflows, enabling 21 CFR Part 11 compliance without custom code. European mid-sized manufacturers closed go-lives in as little as 9 months by leveraging pre-configured lot-traceability templates, while Asia-Pacific firms favored hybrid clouds that keep intellectual property data in local data centers in deference to China's Data Security Law. Rapid regulatory patching is an added lure: SaaS vendors can push new UDI formats or ISO revisions every quarter, whereas on-premises customers often defer upgrades to 3-year intervals. Even so, data-localization statutes continue to sustain hybrid demand, compelling providers to perfect low-latency synchronization between local quality systems and cloud financial ledgers.

High Validation and FDA Computer System Validation Costs

Despite the FDA's 2024 shift to risk-based Computer Software Assurance, Class III device makers still budget around USD 1.2 million per ERP module for installation, operational, and performance qualification testing. Each quarterly cloud update triggers regression scripts, impact assessments, and archival of executed test evidence, prolonging release timelines and inflating consulting fees. The European Union mirrors these demands by requiring audit trails to remain accessible for up to 15 years, driving parallel validation costs. Cloud vendors now market validation-as-a-service bundles, and Acumatica's turnkey documentation package costs USD 150,000; yet site-specific workflows and third-party integrations still mandate bespoke evidence generation. For a USD 50 million manufacturer, the expense equals 2.4% of annual revenue, underscoring why many SMEs postpone full-suite adoption.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Real-Time Traceability in Globalized Supply Chains

- Integration of IoT-Enabled Shop-Floor Data With ERP Platforms

- Cybersecurity Concerns Slowing Cloud ERP Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 54.98% of the Medical Device and MedTech enterprise resource planning market share in 2025 and are forecast to grow at an 8.43% CAGR through 2031, bolstered by mid-sized firms avoiding data-center investments of USD 2 million or more. Vendors are pulling end-of-support levers, SAP's 2027 sunset for ECC and Oracle's 2030 retirement of E-Business Suite, to prod customers toward SaaS subscriptions. The market size for on-premises instances will nonetheless persist among multinationals that prefer full control over software versioning and bespoke validation scripts. Hybrid architectures serve as a compromise for organizations subject to China's Data Security Law or the European Union's GDPR, allowing quality records to reside locally while planning engines run in global clouds.

Oracle's process-manufacturing connectors synchronize shop-floor batch data every few minutes, addressing latency anxieties that once hampered hybrid rollouts. Microsoft and third-party quality consultants package risk-based validation templates that reduce go-live by 40%, shrinking perceived disadvantages of SaaS release cadences. Even so, quarterly feature pushes force manufacturers to maintain evergreen validation teams, while on-premise customers can bundle changes into a single multi-year retrofit. Across all deployment types, buyers now elevate cybersecurity posture and regulator-ready audit trails above generic functionality checklists, shifting evaluation scorecards toward compliance automation.

Software licenses and subscriptions accounted for 69.77% of market revenue in 2025, yet the services category is growing at an 8.23% CAGR as validation complexity increases. Implementation projects consume 12-18 months, with validation tasks accounting for up to 40% of billable hours, pressuring manufacturers to outsource Computer Software Assurance documentation to life-sciences specialists. The market for managed services is expanding as clients adopt continuous-compliance contracts that bundle quarterly validation, patch management, and regulatory monitoring services.

Infosys and Tricentis now automate regression testing during SAP S/4HANA migrations, reducing test-case generation by 40% and trimming overall project budgets. Data-migration consultancies likewise flourish as manufacturers cleanse decades of lot-traceability records before moving to multi-tenant clouds. Training engagements are another bright spot; quality engineers and supply-chain planners require upskilling to interpret AI-generated forecasts without violating validation protocols. With AI modules increasingly embedded at no extra software charge, revenue shifts downstream to advisory, training, and application-management add-ons that keep systems audit-ready.

Geography Analysis

North America accounted for 38.39% of the market in 2025, propelled by stringent FDA oversight and a dense population of multinational device makers. The new Quality Management System Regulation obliges firms to re-validate ERP controls, spurring a wave of validation-as-a-service contracts. Post-merger consolidations, such as Boston Scientific's Axonics integration, underscore how acquisitions catalyze full-suite S/4HANA migrations that unify 16 or more manufacturing sites under a single global ledger. Canada and Mexico are emerging as nearshore contract-manufacturing hubs that install cloud ERP systems to meet the real-time traceability requirements of U.S. sponsors.

Asia-Pacific is the fastest-growing region, expanding at an 8.83% CAGR through 2031. China's phased UDI rollout for Class III devices in 2024 and Class II in 2025 obliges domestic factories to deploy serial-number and EUDAMED-style connectors, steering investment toward platforms that can align with both European and U.S. identifiers. India's Production Linked Incentive scheme reimburses up to 5% of incremental sales for plants equipped with IoT-enabled ERP, accelerating adoption among greenfield projects. South Korea subsidizes sensor-driven smart factories, while Japan's Society 5.0 agenda incentivizes IoT-ERP convergence among Tier 2 suppliers seeking ISO 13485 harmonization.

Europe maintains substantial share, anchored by the Medical Device Regulation and the May 2026 EUDAMED deadline that effectively forces ERP modernization for any exporter. Manufacturers racing to meet the 48-hour adverse-event reporting proposal now view real-time traceability as a must-have, sparking demand for AI modules that correlate shipment conditions with defect probabilities. South America and the Middle East and Africa remain nascent but show steady uptake as local plants aim to mirror parent-company quality systems and gain preferred-supplier status with global brands.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- QAD Inc.

- Epicor Software Corporation

- Sage Group Plc

- IFS AB

- SYSPRO (Pty) Ltd.

- Plex Systems, Inc.

- Rootstock Software, Inc.

- Dassault Systemes SE

- Siemens Industry Software Inc.

- Korber Pharma Software GmbH

- Exact Holding B.V.

- Acumatica, Inc.

- Workday, Inc.

- Priority Software Ltd.

- Abas Software GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Regulatory Pressure for UDI and Quality Compliance

- 4.2.2 Shift Toward Cloud-native SaaS ERP Among Mid-sized MedTech Firms

- 4.2.3 Rising Demand for Real-time Traceability in Globalized Supply Chains

- 4.2.4 Integration of IoT-enabled Shop-floor Data with ERP Platforms

- 4.2.5 Surge in Post-merger System Consolidations in Medical Device Sector

- 4.2.6 Increasing Adoption of AI-driven Demand Forecasting Modules

- 4.3 Market Restraints

- 4.3.1 High Validation and FDA Computer System Validation Costs

- 4.3.2 Cybersecurity Concerns Slowing Cloud ERP Adoption

- 4.3.3 Skills Gap in ERP Data Governance within MedTech SMEs

- 4.3.4 Legacy MES-ERP Integration Complexities in Brownfield Plants

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user

- 5.4.1 Medical Device Manufacturers

- 5.4.2 MedTech Service Providers

- 5.4.3 Contract Manufacturing Organizations

- 5.4.4 Clinical Research Organizations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 QAD Inc.

- 6.4.6 Epicor Software Corporation

- 6.4.7 Sage Group Plc

- 6.4.8 IFS AB

- 6.4.9 SYSPRO (Pty) Ltd.

- 6.4.10 Plex Systems, Inc.

- 6.4.11 Rootstock Software, Inc.

- 6.4.12 Dassault Systemes SE

- 6.4.13 Siemens Industry Software Inc.

- 6.4.14 Korber Pharma Software GmbH

- 6.4.15 Exact Holding B.V.

- 6.4.16 Acumatica, Inc.

- 6.4.17 Workday, Inc.

- 6.4.18 Priority Software Ltd.

- 6.4.19 Abas Software GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年 供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測東協企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測東協企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)