|

市場調查報告書

商品編碼

2063430

德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Germany Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

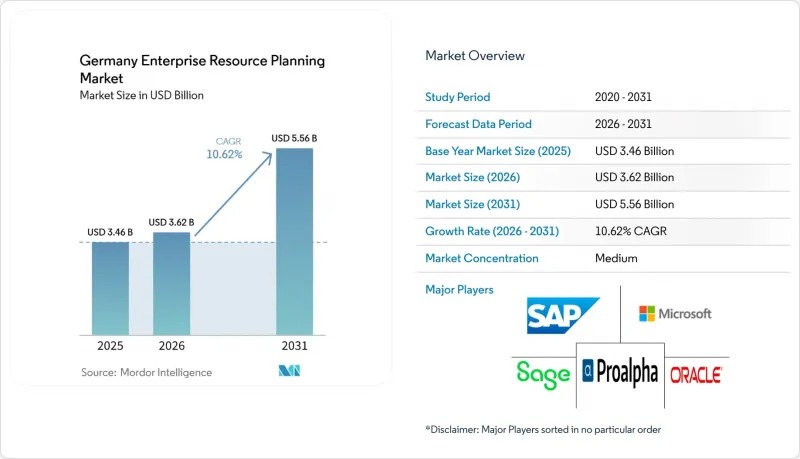

根據Mordor Intelligence預測,德國企業資源規劃(ERP)市場規模預計將從2025年的34.6億美元成長到2026年的36.2億美元,到2031年達到55.6億美元。 2026年至2031年,預計其複合年成長率將達到6.58%。

本報告按架構(雲端原生套件、行動優先ERP等)、業務功能(財務、會計等)、部署模式(本地部署、雲端部署)、組織規模(大型企業、中小企業)和產業(製造業等)進行細分。市場預測以美元計價。

德國企業資源規劃 (ERP) 市場的趨勢與洞察

加速德國中型企業採用雲端運算

過去兩年,中型企業已對其三分之二的核心系統進行了現代化改造,他們遵循廠商藍圖,並傾向於支援遠距辦公的雲端原生和混合模式。根據BITMi 2025年的一項調查,82%的企業計劃在2026年增加IT預算,其中53%將用於雲端基礎設施。 SAP-微軟在Azure上提供的私有雲ERP服務,其99.95%的服務等級協定(SLA)就是一個典型的例子,該服務能夠降低運作風險,並與Copilot和Teams整合。然而,為了規避域外資料存取法律的約束,許多買家仍然傾向於私有雲端雲或主權雲,而像proALPHA這樣的廠商現在正在推出混合解決方案,將CRM遷移到SaaS,同時保留本地部署的MES。

嚴格的資料保護條例正在推動對合規型ERP系統的需求。

《一般資料保護規則》(GDPR)、德國聯邦資料保護法和歐盟資料法要求在2027年前實現開放介面、標準化匯出格式並取消轉換費用。 42%的公司認為資料保護是採用公共雲端的一大障礙。為此,SAP和微軟與Delos Cloud GmbH合作,後者在德國監管的資料中心託管工作負載,以緩解人們對《雲端法案》的擔憂。在銀行業,《數位營運彈性法案》擴大了合規範圍,將第三方風險管理納入其中,並強制要求對ERP供應商進行嚴格的審計。

舊有系統的複雜性和高昂的遷移成本。

目前,儘管2026年5月的遷移截止日期臨近,仍有71%的SAP客戶在使用ECC HCM系統。這一趨勢凸顯了薪資核算客製化帶來的挑戰,而這些挑戰往往使得快速重新實施變得困難。例如,一家中型製造商面臨超過1,000萬歐元(1,130萬美元)的遷移成本,專案週期長達36個月。第三方維護服務可以透過延遲升級提供臨時解決方案,但這也會阻礙創新。這種做法通常會導致企業依賴過時的系統,從而使寶貴的技術人才被束縛在處理遺留技術債上,而不是專注於面向未來的專案。

細分市場分析

預計到2031年,雙層部署將以每年15.12%的速度成長,其中雲端原生套件細分市場將佔據最大佔有率,達到48.21%。跨國中型企業(Mittelstands)正在核心S/4HANA或Oracle帳簿之上部署輕量級區域實例。在德國企業資源規劃(ERP)市場,雙層架構市場預計將比其他任何細分市場成長更快,這反映了法定報告要求和更嚴格的成本控制。借助支援混合部署的ProALPHA 9.5版本,製造商可以在本地維護對延遲敏感的MES系統,同時將CRM與雲端同步,從而在不犧牲全球可視性的前提下滿足工會要求。能夠實現跨層資料複製和身分管理自動化的供應商將擁有競爭優勢。

次要影響包括介面複雜性增加以及整合管理主機的需求日益成長。像 proALPHA 這樣的供應商現在將單一登入 (SSO) 和多因素身份驗證 (MFA) 捆綁在一起,以解決碎片化問題並改善用戶體驗。隨著歐盟資料法強制使用開放式 API,客戶越來越期望邊緣實例和核心系統之間能夠無縫遷移。這種轉變正在加速採用高階整合模式,例如訊息佇列系統和事件流架構,這些模式能夠實現即時資料交換並提高營運效率。

預計人力資本管理 (HCM) 市場在預測期內將以 13.28% 的複合年成長率成長,而財務和會計行業預計將以 34.97% 的複合年成長率成長。這主要是由於各組織加快了對 SAP H4S4 遷移截止日期的回應。由於集體談判規則的複雜性,雲端薪資核算的採用率仍然較低,因此預計德國 HCM ERP 市場佔有率將顯著成長。財務仍然是核心職能,但嵌入式分析的整合和電子帳單法規的實施正在推動企業進行功能升級。為了在競爭激烈的市場中脫穎而出,供應商正在將人工智慧驅動的候選人評估、預測性離職分析和情緒分析等高級功能整合到其產品中。

歐洲約有10萬名SAP專家長期短缺,這進一步推動了對低程式碼工作流程建構器的需求。如今,企業越來越重視無需ABAP編碼專業知識、且允許人力資源和財務團隊獨立修改規則的解決方案。這種轉變不僅縮短了發布週期,還減少了對少數專家顧問的依賴,使企業能夠更快地適應不斷變化的業務需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速德國中型企業採用雲端運算

- 嚴格的資料保護條例推動了對合規型 ERP 系統的需求。

- 在德國製造業推廣工業4.0

- 對即時供應鏈可視性的需求日益成長。

- 脫碳報告要求正在推動 ERP 系統中的永續發展模組的發展。

- 熟練的 SAP ABAP 開發人員短缺,推動了低程式碼 ERP 系統的普及。

- 市場限制因素

- 舊有系統的複雜性和高昂的遷移成本。

- 對嚴格的資料居住要求的擔憂阻礙了公共雲端。

- 經濟不確定性正在抑制中小企業的IT預算。

- 能源價格飆升推高了本地系統的總擁有成本 (TCO),阻礙了升級。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 以建築學為例

- Cloud-Native Suite

- 行動優先的ERP

- 社交/協作型企業資源規劃

- 雙層/邊緣ERP

- 業務職能

- 財會

- 供應鍊和營運

- 人力資本管理

- 客戶關係與商務

- 生產執行和品質

- 按部署模式

- 現場

- 雲

- 按組織規模

- 大公司

- 小型企業

- 按行業分類

- 製造業

- 零售與電子商務

- BFSI

- 政府/公共部門

- 資訊科技/通訊

- 醫療保健和生命科學

- 其他工業部門

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Sage Group plc

- proALPHA Business Solutions GmbH

- Abas Software GmbH

- IFS AB

- Unit4 NV

- Epicor Software Corporation

- Workday Inc.

- Deltek Inc.

- DATEV eG

- Haufe-Lexware GmbH & Co. KG

- Exact Holding BV

- SYSPRO(Pty)Ltd

- Priority Software Ltd

- Acumatica Inc.

- Forterro Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany enterprise resource planning market size is expected to increase from USD 3.46 billion in 2025 to USD 3.62 billion in 2026 and reach USD 5.56 billion by 2031, growing at a CAGR of 6.58% over 2026-2031.

This report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Industry Vertical (Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Enterprise Resource Planning Market Trends and Insights

Accelerated Cloud Adoption Among German Mid-Market Firms

Mittelstand companies have replaced two-thirds of their core systems within two years, favoring cloud-native and hybrid models that align with vendor roadmaps and support remote work. A 2025 BITMi survey showed 82% of firms planning higher IT budgets for 2026, with 53% earmarked for cloud infrastructure. The SAP-Microsoft 99.95% SLA for Cloud ERP Private on Azure exemplifies offerings that de-risk uptime and integrate with Copilot and Teams. Yet many buyers still prefer private or sovereign clouds to avoid extraterritorial data-access laws, prompting vendors such as proALPHA to release hybrid options that keep MES on-premise while moving CRM to SaaS.

Stringent Data Protection Regulations Driving Demand for Compliant ERP

The General Data Protection Regulation, the German Federal Data Protection Act, and the EU Data Act mandate open interfaces, standardized export formats, and the abolition of switching fees by 2027. 42% of enterprises cite data protection as a barrier to public cloud adoption. SAP and Microsoft responded by partnering with Delos Cloud GmbH, which hosts workloads in German-controlled data centers to mitigate CLOUD Act concerns. For banks, the Digital Operational Resilience Act extends compliance to third-party risk management, forcing rigorous audits of ERP providers.

Legacy System Complexity and High Migration Costs

Currently, 71% of SAP customers continue to operate on ECC HCM, even as the May 2026 migration deadline approaches. This trend highlights the challenges posed by payroll customizations, which often make rapid re-implementation difficult. For instance, a mid-sized manufacturer is facing migration costs exceeding EUR 10 million (USD 11.3 million) and project timelines extending up to 36 months. While third-party maintenance services can provide a temporary solution by deferring upgrades, they also hinder innovation. This approach often results in organizations becoming reliant on outdated systems, which in turn locks valuable technical talent into managing legacy technical debt rather than focusing on forward-looking initiatives.

Other drivers and restraints analyzed in the detailed report include:

- Industry 4.0 Push Within German Manufacturing

- Rising Need for Real-Time Supply Chain Visibility

- Stringent Data Residency Concerns Limiting Public Cloud Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Two-tier deployments are forecast to grow at 15.12% annually through 2031, while the Cloud-Native Suite segment captured the largest share of 48.21%. As multinational Mittelstand firms overlay lightweight regional instances atop core S/4HANA or Oracle ledgers. The Germany enterprise resource planning market size for two-tier architecture is projected to expand faster than any other segment, reflecting statutory reporting demands and cost discipline. ProALPHA's hybrid-ready 9.5 release lets manufacturers keep latency-sensitive MES on-premises while syncing CRM to the cloud, preserving works council requirements without forfeiting global visibility. Vendors able to automate data replication and identity management across tiers will outpace competitors.

Second-order impacts include growing interface complexity and rising demand for unified admin consoles. Vendors such as proALPHA now bundle single sign-on (SSO) and multi-factor authentication (MFA) to address fragmentation and improve the user experience. As the EU Data Act enforces the use of open APIs, customers are increasingly expecting a seamless transition between edge instances and the core systems. This shift is driving the accelerated adoption of advanced integration patterns, such as message-queue systems and event-streaming architectures, which enable real-time data exchange and improved operational efficiency.

Human capital management is projected to log a 13.28% CAGR; however, finance and accounting generated 34.97% over the forecast period. As organizations accelerate efforts to meet SAP's H4S4 deadline. The Germany enterprise resource planning market share for HCM is expected to grow significantly, as cloud payroll adoption remains low due to the complexities of collective-bargaining rules. While finance remains the core function, the growing integration of embedded analytics and the enforcement of e-invoicing legislation are driving functional upgrades across enterprises. To stand out in the competitive landscape, vendors are incorporating advanced features such as AI-driven candidate scoring, predictive attrition analysis, and sentiment analysis into their offerings.

The persistent shortage of approximately 100,000 SAP specialists across Europe further amplifies the demand for low-code workflow builders. Enterprises are now placing greater emphasis on solutions that empower HR and finance teams to modify rules independently, without requiring ABAP coding expertise. This shift not only shortens release cycles but also reduces dependency on the limited pool of specialized consultants, enabling organizations to adapt more quickly to evolving business needs.

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Sage Group plc

- proALPHA Business Solutions GmbH

- Abas Software GmbH

- IFS AB

- Unit4 NV

- Epicor Software Corporation

- Workday Inc.

- Deltek Inc.

- DATEV eG

- Haufe-Lexware GmbH & Co. KG

- Exact Holding B.V.

- SYSPRO (Pty) Ltd

- Priority Software Ltd

- Acumatica Inc.

- Forterro Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Cloud Adoption Among German Mid-Market Firms

- 4.2.2 Stringent Data Protection Regulations Driving Demand for Compliant ERP

- 4.2.3 Industry 4.0 Push Within German Manufacturing

- 4.2.4 Rising Need for Real-Time Supply Chain Visibility

- 4.2.5 De-carbonization Reporting Mandates Fueling ERP Sustainability Modules

- 4.2.6 Shortage of Skilled SAP ABAP Developers Pushing Low-Code ERP Adoption

- 4.3 Market Restraints

- 4.3.1 Legacy System Complexity and High Migration Costs

- 4.3.2 Stringent Data Residency Concerns Limiting Public Cloud Uptake

- 4.3.3 Economic Uncertainty Curbing IT Budgets Among SMEs

- 4.3.4 Rising Energy Prices Increasing On-Premise TCO and Hindering Upgrades

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Architecture

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Others Industry Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 Sage Group plc

- 6.4.6 proALPHA Business Solutions GmbH

- 6.4.7 Abas Software GmbH

- 6.4.8 IFS AB

- 6.4.9 Unit4 NV

- 6.4.10 Epicor Software Corporation

- 6.4.11 Workday Inc.

- 6.4.12 Deltek Inc.

- 6.4.13 DATEV eG

- 6.4.14 Haufe-Lexware GmbH & Co. KG

- 6.4.15 Exact Holding B.V.

- 6.4.16 SYSPRO (Pty) Ltd

- 6.4.17 Priority Software Ltd

- 6.4.18 Acumatica Inc.

- 6.4.19 Forterro Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年 供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)

供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031) 企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測東協企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測東協企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)