|

市場調查報告書

商品編碼

2063402

歐洲企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

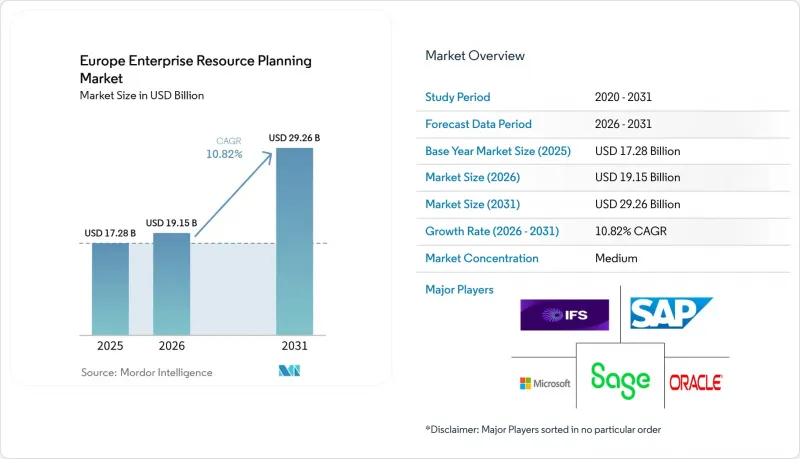

根據 Mordor Intelligence 預測,歐洲企業資源計畫 (ERP) 市場規模將從 2025 年的 172.8 億美元成長到 2026 年的 191.5 億美元,到 2031 年將達到 292.6 億美元,2026 年至 2031 年的複合年成長率為 10.82%。

本報告按架構(雲端原生套件、行動優先ERP、其他)、產業(金融和會計、其他)、部署模式(本地部署、雲端部署)、組織規模(大型企業、中小企業)、產業(製造業、銀行、金融服務和保險業、其他)和地區進行細分。市場預測以美元計價。

歐洲企業資源規劃市場的趨勢與洞察

遷移到雲端ERP解決方案

雲端遷移正在重塑歐洲企業付費使用制規劃 (ERP) 市場的成本結構,將依賴硬體的部署模式轉變為按需付費的訂閱模式,從而使支出與需求週期更加契合。 SAP RISE 專案和 Microsoft Dynamics 365 雲端套件的創紀錄成長凸顯了向「消費經濟」的全面轉型,這對尋求可預測營運成本的財務長 (CFO) 來說極具吸引力。歐洲主權雲端區域的可用性緩解了資料居住的擔憂,並有助於企業進入公共管理和醫療保健等受監管行業。使用者小組調查證實,2023 年至 2025 年間,S/4HANA 雲端部署量將加倍,中型製造商正在加速採用雲端遷移方案。在歐洲 ERP 市場,供應商提供固定價格的遷移套餐,縮短專案週期,降低預算超支的風險,即使是風險規避型的產業集團也能擺脫舊有系統。

人工智慧與進階分析的融合

生成式人工智慧正從試點階段走向生產階段,對話式輔助系統已應用於採購、財務和人力資源模組。早期採用者已將獲取洞察和人工核對的時間縮短了近一半,從而提升了下一代ERP套件的價值提案。歐洲製造商正在利用預測模型模擬供應鏈衝擊,並實現主動庫存配置,以應對關稅和物流中斷。供應商正在整合高度透明的審計追蹤,以符合歐洲人工智慧法規,並確保招聘評分等高風險功能保持可解釋性並處於人工控制之下。人工智慧的快速普及正在提高用戶生產力,加速許可證升級,並鞏固歐洲企業資源規劃市場作為數位營運模式中心樞紐的地位。

高昂的遷移和整合成本

複雜且高度客製化的現有系統環境會增加企業遷移到現代平台的預算,如果將資料清理、介面重寫和並行運作週期等費用考慮在內,預算往往會翻倍。 SAP 和 Oracle 等稀缺技能的諮詢費用超過每小時 500 美元,這給中型製造商的資金配置帶來了壓力。固定價格的遷移套餐和帶有信用額度的雲端服務可以降低財務風險,但並不能完全消除風險。因此,受監管行業正在推遲項目,直到商業案例更加明朗,這在短期內對歐洲 ERP 市場造成了拖累。

細分市場分析

預計到2025年,雲端原生套件將佔總支出的41.78%,成為即時分析和自動修補的中心。供應商每月發布更新,在不中斷營運的情況下添加人工智慧功能,使用戶始終保持最新狀態。行動優先平台正以9.65%的複合年成長率快速成長,為現場技術人員和倉庫負責人提供離線應用,這些應用可在網路連線恢復後立即同步,這對於公共產業和物流行業的分散式工作團隊而言至關重要。 IFS Cloud Mobile和類似解決方案正在推動其市場佔有率的逐步成長,因為邊緣快取技術已證明其能夠減少意外停機時間並加快存貨周轉。

雙層架構在跨國公司中日益普及,這種架構在子公司部署輕量級雲端系統,而核心財務系統則保留在嚴格控制的底層架構中。這種方法兼顧了本地的靈活性和總部的監管。工廠車間的邊緣ERP單元能夠在毫秒級的時間內協調機器人和偵測攝影機的運行,並將匯總指標發送到雲端的父系統。這種混合模式強化了品管流程,符合工業4.0的要求,但也鞏固了歐洲ERP市場的供應商鎖定。

至2025年,財務與會計模組將佔總收入的28.67%,凸顯其作為維護法定記錄系統和確保27個稅務系統審計一致性的安全隔離網閘角色。持續結算、自動對帳和嵌入式分析功能將縮短週期,使財務團隊能夠專注於更高價值的分析工作。隨著零售商將電子商務、訂單調整和服務互動整合到單一資料模型中,客戶關係管理和商務模組正以8.85%的複合年成長率快速成長。即時庫存分配和動態定價將在地緣政治因素造成的供應衝擊下保護利潤率,同時提升客戶體驗。

供應鏈套件仍然至關重要,它模擬貨運路線和替代供應商組合,以解決紅海和鐵路運輸瓶頸問題。人力資本管理解決方案憑藉著人工智慧驅動的技能本體脫穎而出,該本體能夠將內部人才與專案需求相匹配,從而緩解區域勞動力短缺問題。製造執行和品管模組整合了電子批次記錄,滿足GMP審核要求,並提供詳細數據,從而實現上游永續性揭露,鞏固了多模組在歐洲企業資源規劃市場的應用。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 遷移到雲端ERP解決方案

- 人工智慧與進階分析的融合

- 關於資料隱私的監理要求(GDPR、NIS2)

- 透過歐盟復甦與韌性基金為中小企業實施

- 涵蓋碳計量要求的供應鏈

- 即時製造管理的邊緣ERP

- 市場限制因素

- 高昂的遷移和整合成本

- 數據主權和居住地相關問題

- 歐洲ERP專業人才短缺

- 能源價格波動給IT預算帶來了壓力。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 以建築學為例

- 雲端原生套件

- 行動優先的ERP

- 社交/協作型企業資源規劃

- 雙層/邊緣ERP

- 按部門

- 財會

- 供應鍊和營運

- 人力資本管理

- 客戶關係與商務

- 生產執行和品質

- 按部署模式

- 現場

- 雲

- 按組織規模

- 大公司

- 小型企業

- 按行業

- 製造業

- 零售與電子商務

- BFSI

- 政府/公共部門

- 資訊科技/通訊

- 醫療保健和生命科學

- 其他

- 按地區

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Unit4 NV

- IFS AB

- Infor Inc.

- Sage Group Plc

- Workday Inc.

- SYSPRO(Pty)Ltd.

- Acumatica Inc.

- Ramco Systems Ltd.

- Visma AS

- Epicor Software Corporation

- QAD Inc.

- Cetek ERP LLC

- Abas Software GmbH

- Deltek Inc.

- Priority Software Ltd.

- Exact Holding BV

- Odoo SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe enterprise resource planning market size is expected to grow from USD 17.28 billion in 2025 to USD 19.15 billion in 2026 and is forecast to reach USD 29.26 billion by 2031 at a 10.82% CAGR over 2026-2031.

This report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Enterprise Resource Planning Market Trends and Insights

Shift to Cloud ERP Solutions

Cloud migration is redefining the cost profile of the European enterprise resource planning market by converting hardware-heavy installations into pay-as-you-go subscriptions that match expenditure with demand cycles. Record growth in SAP's RISE program and Microsoft Dynamics 365 cloud suites underscores a wholesale pivot toward consumption economics that appeal to finance chiefs seeking predictable operating costs. The availability of European sovereign cloud regions calms residency concerns and unlocks regulated sectors such as public administration and healthcare. Mid-market manufacturers are accelerating adoption after user-group surveys confirmed a doubling of S/4HANA cloud footprints between 2023 and 2025. In the Europe ERP market, vendors package fixed-price migration bundles that compress project timelines and de-risk budget overruns, encouraging even risk-averse industrial groups to retire legacy estates.

Integration of AI and Advanced Analytics

Generative AI is moving from pilot to production, placing conversational copilots within procurement, finance, and human resources modules. Early adopters reduce time-to-insight and manual reconciliations by roughly half, strengthening the value proposition of next-generation ERP suites. European manufacturers use predictive models to simulate supply-chain shocks, enabling proactive stock positioning in response to tariff or logistics disruptions. Vendors embed transparent audit trails to comply with the European AI Act, ensuring high-risk functions, such as recruitment scoring, remain explainable and human-governed. This rapid infusion of AI raises user productivity, drives licence upgrades, and cements the Europe enterprise resource planning market as a centerpiece of digital operating models.

High Migration and Integration Costs

Complex, customization-rich estates inflate budgets when enterprises shift to modern platforms, often doubling initial estimates once data cleansing, interface rewrites, and dual-running periods are included. Consulting fees for scarce SAP and Oracle skills have climbed above USD 500 per hour, squeezing capital allocation at mid-market manufacturers. Fixed-price migration bundles and credit-backed cloud offers temper, but do not eliminate, financial risk, prompting regulated industries to defer projects until business-case certainty firms up and feeding a near-term drag on the Europe ERP market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates on Data Privacy (GDPR, NIS2)

- SME Uptake Through EU Recovery and Resilience Facility

- Data-Sovereignty and Residency Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-native suites captured 41.78% of 2025 spending, establishing themselves as the control tower for real-time analytics and automated patching. Vendors release monthly updates that add AI features without disrupting operations, raising user expectations for evergreen functionality. Mobile-first platforms, expanding at a 9.65% CAGR, equip field technicians and warehouse pickers with offline-capable apps that sync the moment connectivity returns, a capability now central to distributed workforces across utilities and logistics. IFS Cloud Mobile and similar offerings demonstrate how edge caching cuts unplanned downtime and accelerates inventory turns, contributing incremental share gains.

Two-tier architectures gain traction as multinationals deploy lightweight cloud systems at subsidiaries while core financials remain on high-control stacks, an approach that balances local agility with headquarters oversight. Edge-enabled ERP units on factory floors orchestrate millisecond-level operations for robots and inspection cameras, then feed aggregated metrics to the cloud parent. This hybrid pattern tightens quality loops and conforms to Industrie 4.0 mandates, strengthening vendor lock-in within the Europe enterprise resource planning market.

Finance and accounting modules accounted for 28.67% of 2025 revenue, underscoring their role as statutory systems of record and gatekeepers of audit integrity across 27 tax regimes. Continuous close, automated reconciliation, and embedded analytics reduce cycle times and free finance teams for value-add analysis. Customer relationship and commerce modules are advancing at an 8.85% CAGR as retailers stitch together e-commerce, order orchestration, and service engagement in a single data model. Real-time inventory allocations and dynamic pricing drive margin protection during geopolitical supply shocks while enhancing customer experience.

Supply-chain suites remain mission-critical, simulating freight corridors and alternative supplier mixes in response to Red Sea or rail bottlenecks. Human capital management solutions differentiate via AI-driven skills ontologies that match internal talent with project demand, alleviating regional labor shortages. Manufacturing execution and quality modules embed electronic batch records, satisfying GMP audits and delivering granularity that flows upstream into sustainability disclosures, anchoring multi-module adoption inside the European enterprise resource planning market.

List of Companies Covered in this Report:

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Unit4 N.V.

- IFS AB

- Infor Inc.

- Sage Group Plc

- Workday Inc.

- SYSPRO (Pty) Ltd.

- Acumatica Inc.

- Ramco Systems Ltd.

- Visma AS

- Epicor Software Corporation

- QAD Inc.

- Cetek ERP LLC

- Abas Software GmbH

- Deltek Inc.

- Priority Software Ltd.

- Exact Holding B.V.

- Odoo S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to Cloud ERP Solutions

- 4.2.2 Integration of AI and Advanced Analytics

- 4.2.3 Regulatory Mandates on Data Privacy (GDPR, NIS2)

- 4.2.4 SME Uptake Through EU Recovery and Resilience Facility

- 4.2.5 Across Carbon-Accounting Requirements Supply Chains

- 4.2.6 Edge-Based ERP for Real-Time Manufacturing Control

- 4.3 Market Restraints

- 4.3.1 High Migration and Integration Costs

- 4.3.2 Data-Sovereignty and Residency Concerns

- 4.3.3 Shortage of ERP-Specialised Talent in Europe

- 4.3.4 Energy-Price Volatility Pressuring IT Budgets

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Architecture

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Other Industry Verticals

- 5.6 By Geography

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 Unit4 N.V.

- 6.4.5 IFS AB

- 6.4.6 Infor Inc.

- 6.4.7 Sage Group Plc

- 6.4.8 Workday Inc.

- 6.4.9 SYSPRO (Pty) Ltd.

- 6.4.10 Acumatica Inc.

- 6.4.11 Ramco Systems Ltd.

- 6.4.12 Visma AS

- 6.4.13 Epicor Software Corporation

- 6.4.14 QAD Inc.

- 6.4.15 Cetek ERP LLC

- 6.4.16 Abas Software GmbH

- 6.4.17 Deltek Inc.

- 6.4.18 Priority Software Ltd.

- 6.4.19 Exact Holding B.V.

- 6.4.20 Odoo S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

SAP企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031) 企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)