|

市場調查報告書

商品編碼

2065451

歐洲員工入職:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Employee Onboarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

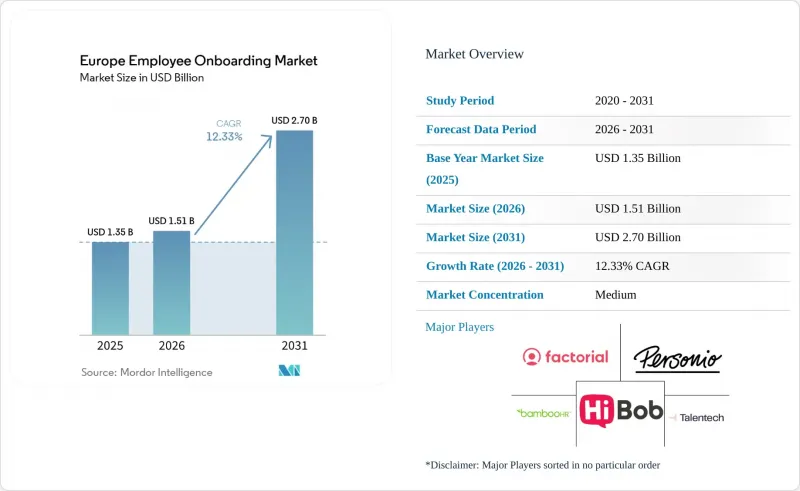

根據 Mordor Intelligence 預測,歐洲員工入職市場規模預計在 2025 年達到 13.5 億美元,在 2026 年達到 15.1 億美元,在 2031 年達到 27 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 12.33%。

本報告按部署類型(雲端等)、公司規模(大型企業、中小企業)、最終用戶行業(銀行、金融服務和保險、醫療保健/生命科學等)、功能(工作流程自動化/任務編配、文件管理/電子簽章等)和地區進行細分。市場預測以美元計價。

歐洲員工入職市場的趨勢與洞察

對GDPR合規性和多語言入職培訓的需求日益成長。

歐洲雇主越來越需要能夠創建可驗證的同意記錄、資料最小化和刪除流程的入職系統,而不僅僅是能夠自動填寫表格和發送提醒的工具。這項要求在歐洲員工入職市場尤其重要,因為在正式入職之前,一次招聘流程可能涉及多項勞動法、多種語言以及內部負責人。那些將字段級加密、租戶隔離和記錄保存功能整合到核心架構中的供應商,正在從那些將隱私合規性視為次要考慮因素的通用人力資源產品手中奪取市場佔有率。多語言需求進一步加劇了買家的緊迫性,因為在德國、法國、西班牙和荷蘭運營的雇主需要本地語言的合約、政策和培訓內容,而無需手動管理這些文件。歐洲各地的數位化進程仍然不均衡,這為符合GDPR的平台逐步取代手動工作流程留下了空間。根據歐盟統計局的數據,到2025年,52.7%的歐盟公司將使用付費雲端運算服務,但不同公司類型和國家的採用率仍有顯著差異。強大的隱私保護措施和語言在地化相結合,使專業供應商在歐洲員工入職市場中,在採購團隊評估長期合規風險時,能夠獲得持續的優勢。

從人力資源管理過渡到自動化工作流程編配

在歐洲,一系列任務流程的營運中斷正在推動自動化。這是因為新進員工入職培訓需要人力資源、IT、薪資核算、法務和業務經理協同合作,而非按部就班。歐洲員工入職市場越來越期望,簽署合約後即可自動觸發後續操作,例如發放筆記型電腦、設定薪資核算、合規註冊和通知經理,而無需人工追蹤。這種模式與目前歐洲普遍存在的企業技術基礎設施相契合。到2025年,52.7%的歐盟企業將使用付費雲端服務,85%的大型企業將部署雲端服務。因此,入職培訓的投資報酬率不再僅由人力資源部門來評估,因為IT環境搭建和身分配置的延遲在實施時會累計實際的業務成本。與其要求買家替換現有系統,不如選擇位於ATS、HRIS、薪資核算和IT堆疊頂端的供應商,因為他們能夠降低現有企業架構中的實施風險,從而越來越受歡迎。因此,在歐洲員工入職市場,能夠簡化系統間任務路由的編配層比依賴完全替換策略的平台更有價值。

ATS、HRIS、薪資核算和IT系統整合的複雜性。

實施過程中最大的營運障礙並非軟體選擇本身,而是將入職層與分散的企業系統連接起來的難度,這些系統並非設計用於以通用格式共用資料。在歐洲員工入職市場,跨國公司可能使用單一的招聘管理系統 (ATS)、單一的核心人力資源系統、每個國家/地區不同的薪資核算提供者以及獨立的 IT 配置堆疊,這使得實施成為多流程整合專案。當需要將候選人資料從 ATS 轉換為新員工記錄,然後再轉換回薪資核算和 IT 系統時,其成本和延誤可能與平台許可費本身不成比例。在德國,DATEV 已深深嵌入中型企業的薪資核算環境中,這通常需要經過認證的介面合作夥伴,而不是通用的 API 鏈接,從而造成了獨特的障礙。資料模型不匹配,例如員工 ID 結構和分類規則的差異,需要手動核對,這使得原本應該由軟體簡化的管理任務重新回到流程中。在歐洲員工入職市場,提供Workday、SAP SuccessFactors、DATEV和AFAS等系統認證連接器的供應商越來越受歡迎。這是因為買家希望加快部署速度,並減少對專業服務的依賴。

細分市場分析

預計到2025年,基於雲端的部署將佔歐洲員工入職市場68.41%的佔有率,而混合部署預計到2031年將以13.82%的複合年成長率成長。這一主導地位反映了歐洲雇主對SaaS平台的長期投資,這些平台將符合GDPR的資料居住要求、安全認證和工作流程工具作為標準功能而非可選附加元件。歐洲員工入職市場持續受益於強大的基礎設施基礎。到2025年,52.7%的歐盟公司將使用付費雲端服務,比2023年成長7.4個百分點。根據同一資料集,大型企業的雲端採用率已達到85%,這也是高價值買家仍偏好託管交付模式的原因之一。因此,對於那些尋求更快部署、降低內部維護成本以及在單一平台上輕鬆進行跨國部署的組織而言,雲端仍然是首選。

然而,混合解決方案的成長速度正在進一步加快。這是因為許多雇主並未放棄雲端策略,而是根據受監管的營運環境和舊有系統的實際情況進行調整。在歐洲員工入職產業,混合架構使雇主能夠在嚴格控制的環境中維護高度敏感的身份驗證、文件管理和薪資核算流程,同時利用 SaaS 工作流程進行協作和進度管理。這種方法適用於那些因國內託管義務、內部安全策略或關鍵基礎設施相關法規而難以獲得全面雲端遷移批准的行業。它也適用於那些已經在本地人力資源和 IT 架構上投入巨資,現在希望分階段過渡而不是進行顛覆性替換的公司。因此,在歐洲員工入職市場,能夠支援雲端、混合和本地部署路徑,且不會強迫買家採用忽視採購和合規性限制的單一架構的供應商備受青睞。

預計到2025年,大型企業(BME)將佔據歐洲員工入職市場61.29%的佔有率,而中小企業(SME)預計到2031年將以15.47%的複合年成長率成長。大型企業之所以佔據主導地位,是因為它們面臨著最具挑戰性的協調負擔,包括跨境招聘、多語種合約起草、員工代表義務以及人力資源、薪資、身分管理和合規系統之間的深度整合。從實際角度來看,對於這些雇主而言,系統化的入職流程不僅僅是一項可有可無的軟體購買,它更像是一個管理層,可以減少整個複雜招聘流程中的錯誤。此外,大型企業持續主導歐洲員工入職市場的原因在於其雄厚的預算實力,除了軟體授權費用外,它們還能承擔實施服務、政策重新設計和管理員培訓的成本。這種規模經濟確保了大型企業對軟體的強勁需求,即使供應商不斷簡化實施流程並擴展自助服務功能,這種需求仍然存在。

中小企業 (SME) 的快速擴張反映了一種不同的格局,其核心在於較低的進入門檻以及入職品質與可避免的離職率之間更清晰的關聯性。 2025 年的一項調查顯示,20.5% 的人力資源經理表示,高達 50% 的新員工會在入職後的前 90 天內離職,這使得即使是小規模軟體投資在早期高離職率的環境下也更具合理性。此外,2026 年的一份報告顯示,中小企業的雲端採用率仍然顯著落後於大型企業,這表明小規模企業在首次數位轉型方面仍有相當大的空間。憑藉更低的價格以及透過模板和引導式設定實現的便利部署,歐洲員工入職產業正在將中小企業從邊緣市場轉變為核心成長領域。這種轉變意義重大,因為那些在中小企業雇主中早期獲得市場佔有率的供應商可以在這些企業面臨更複雜的人才管理和合規需求之前,建立長期的客戶生命週期。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對符合 GDPR 標準且支援多語言的入職解決方案的需求日益成長。

- 從人力資源管理過渡到自動化工作流程編配

- 在早期階段提高員工留任率和員工體驗

- 需要將人力資源、IT和合規營運整合到單一的工作流程中。

- 為回應歐盟工資透明度指令,我們正在重組招募和入職流程中的資料流。

- 引入 EUDI 錢包和檢驗的數位憑證,以加快身份驗證速度。

- 市場限制因素

- 人力資源與資訊科技系統整合的複雜性

- 中小企業的預算與變更管理限制

- 因員工代表委員會和勞動法規造成的延誤

- 透過數據主權縮小供應商候選範圍

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按最終用戶行業分類

- BFSI

- 醫療保健和生命科學

- 資訊科技/通訊

- 零售與電子商務

- 工業製造

- 政府/公共部門

- 其他終端用戶產業

- 功能性別

- 工作流程自動化與任務編配

- 文件管理和電子簽章

- 學習與培訓管理

- 合規與政策通知

- 分析和進展追蹤

- 員工自助服務和溝通

- 按地區

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- BambooHR LLC

- Hi Bob Limited

- Personio SE and Co. KG

- Deel, Inc.

- Enboarder Pty Ltd.

- Click Boarding, LLC

- Jobvite, Inc.

- Greenhouse Software, Inc.

- ClearCompany, LLC

- Leapsome GmbH

- Zavvy GmbH

- Appical BV

- Talentech Group AS

- HR-ON ApS

- Valamis Group Oy

- WorkMotion Software GmbH

- Employment Hero Pty Ltd.

- Factorial HR, SL

- Teamtailor AB

- Abacus Umantis AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe employee onboarding market size is projected to be USD 1.35 billion in 2025, USD 1.51 billion in 2026, and reach USD 2.70 billion by 2031, growing at a CAGR of 12.33% from 2026 to 2031.

This report is Segmented by Deployment Mode (Cloud-Based, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), Functionality (Workflow Automation and Task Orchestration, Document Management and E-Signature, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Employee Onboarding Market Trends and Insights

Rising Demand for GDPR-Compliant and Multilingual Onboarding

European employers increasingly want onboarding systems that create a defensible record of consent, data minimization, and deletion handling, rather than tools that only automate forms and reminders. That requirement matters more in the Europe employee onboarding market because a single hiring process may involve several labor regimes, languages, and internal reviewers before a new hire is active. Vendors that built field-level encryption, tenant separation, and records support into their core architecture are taking share from generic HR products that treated privacy compliance as an afterthought. The multilingual requirement adds another layer of buyer urgency because employers operating across Germany, France, Spain, and the Netherlands need contracts, policies, and training content in local languages without maintaining manual versions of these documents. Digital adoption is still uneven across Europe, leaving room for GDPR-native platforms to replace manual workflows over time. 52.7% of EU enterprises used paid cloud computing services in 2025, and adoption still varied widely by enterprise type and country, according to EUROSTAT. That combination of privacy depth and language localization is giving specialized vendors a durable edge in the Europe employee onboarding market when procurement teams evaluate long-term compliance risk.

Shift From Manual HR Administration to Automated Workflow Orchestration

Operational breakdowns in sequential task handling are driving the automation case in Europe, because new-hire readiness depends on HR, IT, payroll, legal, and line managers acting simultaneously rather than in sequence. In the Europe employee onboarding market, a contract signature is increasingly expected to trigger downstream actions such as laptop provisioning, payroll setup, compliance enrollment, and manager notifications without manual chasing. That model aligns with the wider enterprise technology base now in place across Europe, where 52.7% of EU enterprises used paid cloud services in 2025, and 85% of large enterprises had already adopted cloud services. The practical effect is that onboarding ROI is no longer judged solely within HR, because delays in IT provisioning and identity setup are counted as real business costs at the point of deployment. Vendors that can sit above the ATS, HRIS, payroll, and IT stack, rather than asking buyers to replace them, are gaining traction because this lowers implementation risk within existing enterprise architectures. The Europe employee onboarding market is therefore rewarding orchestration layers that simplify task routing across systems rather than platforms that depend on a full replacement strategy.

Integration Complexity Across ATS, HRIS, Payroll, and IT Systems

The biggest operational drag on adoption is not software selection, but the difficulty of connecting the onboarding layer to fragmented enterprise systems that were never designed to share data in a common format. In the Europe employee onboarding market, a multinational employer may use a single ATS, a single core HR system, different payroll providers by country, and a separate IT provisioning stack, which makes implementation a multi-stream integration project. When candidate data must be translated from the ATS into a new hire record, then again into payroll and IT systems, the cost and delay can become disproportionate to the platform license itself. Germany adds a specific friction point because DATEV remains deeply embedded in the Mittelstand payroll environment and often requires certified interface partners rather than generic API links. Data-model mismatches, such as different employee ID structures or classification rules, then force manual reconciliation, which puts administrative work back into a process the software was meant to simplify. The Europe employee onboarding market is favoring vendors that bring certified connectors to systems such as Workday, SAP SuccessFactors, DATEV, and AFAS because buyers want faster deployment and lower professional services exposure.

Other drivers and restraints analyzed in the detailed report include:

- Stronger Focus on Early Retention and Employee Experience

- Need To Coordinate HR, IT, and Compliance Tasks in One Workflow

- Budget and Change-Management Friction Among Small and Medium-Sized Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment held 68.41% of the Europe employee onboarding market size in 2025, while hybrid is projected to expand at a 13.82% CAGR through 2031. That lead reflected years of investment by European employers in SaaS platforms that package GDPR data residency, security certifications, and workflow tools as standard capabilities rather than optional add-ons. The Europe employee onboarding market still benefits from a favorable infrastructure base, as 52.7% of EU enterprises used paid cloud services in 2025, up 7.4 percentage points from 2023. The same dataset showed that cloud adoption among large enterprises had already reached 85%, which helps explain why higher-value buyers remain comfortable with hosted delivery models. Cloud, therefore, remained the default choice for organizations seeking faster deployment, lower internal maintenance costs, and easier multi-country rollouts within a single platform.

Hybrid, however, is growing faster because many employers are not abandoning cloud strategy; they are adapting it to regulated operating conditions and legacy system realities. In the Europe employee onboarding industry, hybrid design lets employers keep sensitive identity, document, or payroll steps in tightly controlled environments while still using SaaS workflows for collaboration and progress management. That approach fits sectors where sovereign hosting obligations, internal security policies, or critical infrastructure rules make a full cloud migration difficult to approve. It also suits enterprises that already invested heavily in on-premises HR or IT stacks and now want a layered transition rather than a disruptive replacement. The Europe employee onboarding market is therefore rewarding vendors that can support cloud, hybrid, and on-premises paths without forcing buyers into a single architecture that ignores procurement and compliance constraints.

Large enterprises accounted for 61.29% of the Europe employee onboarding market size in 2025, while SMEs are projected to grow at a 15.47% CAGR through 2031. Large organizations held the lead because they face the hardest coordination burden, including cross-border hiring, multi-language contract generation, works council obligations, and deep integration across HR, payroll, identity, and compliance systems. In practical terms, structured onboarding for these employers is less a discretionary software purchase and more a control layer that reduces errors across complex hiring operations. The Europe employee onboarding market also remains enterprise-led because large buyers have budget capacity to absorb implementation services, policy redesign, and manager training alongside the software license. That scale advantage keeps enterprise demand strong even as vendors simplify implementation and broaden self-service features.

The faster expansion in SMEs reflects a different set of conditions, centered on lower entry barriers and a clearer link between onboarding quality and avoidable turnover. A 2025 survey showed that 20.5% of HR leaders said up to 50% of new hires left within the first 90 days, which makes even a smaller software investment easier to justify when early exits are frequent. A 2026 publication also showed that SME cloud adoption still trailed that of large enterprises by a wide margin, indicating substantial room for first-time digitalization across the smaller employer base. As pricing falls and setup becomes easier through templates and guided configuration, the Europe employee onboarding industry is turning SMEs from a peripheral segment into a core expansion field. That shift matters because vendors that win early among smaller employers can create long customer lifecycles before those organizations move into more complex workforce and compliance needs.

List of Companies Covered in this Report:

- BambooHR LLC

- Hi Bob Limited

- Personio SE and Co. KG

- Deel, Inc.

- Enboarder Pty Ltd.

- Click Boarding, LLC

- Jobvite, Inc.

- Greenhouse Software, Inc.

- ClearCompany, LLC

- Leapsome GmbH

- Zavvy GmbH

- Appical B.V.

- Talentech Group AS

- HR-ON ApS

- Valamis Group Oy

- WorkMotion Software GmbH

- Employment Hero Pty Ltd.

- Factorial HR, S.L.

- Teamtailor AB

- Abacus Umantis AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand For GDPR-Compliant and Multilingual Onboarding

- 4.2.2 Shift From Manual HR Administration To Automated Workflow Orchestration

- 4.2.3 Stronger Focus On Early Retention and Employee Experience

- 4.2.4 Need To Coordinate HR, IT, and Compliance Tasks In One Workflow

- 4.2.5 EU Pay Transparency Directive Readiness Reshaping Hiring and Onboarding Data Flows

- 4.2.6 EUDI Wallet and Verified Digital Credential Adoption For Faster Identity Checks

- 4.3 Market Restraints

- 4.3.1 Integration Complexity Across HR/IT Systems

- 4.3.2 SME Budget and Change-Management Limits

- 4.3.3 Works Council and Labor Rule Delays

- 4.3.4 Data Sovereignty Narrowing Vendor Pools

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-based

- 5.1.2 On-premises

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-sized Enterprises

- 5.3 By End User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Information Technology and Telecom

- 5.3.4 Retail and E-commerce

- 5.3.5 Industrial Manufacturing

- 5.3.6 Government and Public Sector

- 5.3.7 Other End-user Industries

- 5.4 By Functionality

- 5.4.1 Workflow Automation and Task Orchestration

- 5.4.2 Document Management and E-signature

- 5.4.3 Learning and Training Management

- 5.4.4 Compliance and Policy Acknowledgment

- 5.4.5 Analytics and Progress Tracking

- 5.4.6 Employee Self-service and Communication

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Russia

- 5.5.7 Netherlands

- 5.5.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 BambooHR LLC

- 6.4.2 Hi Bob Limited

- 6.4.3 Personio SE and Co. KG

- 6.4.4 Deel, Inc.

- 6.4.5 Enboarder Pty Ltd.

- 6.4.6 Click Boarding, LLC

- 6.4.7 Jobvite, Inc.

- 6.4.8 Greenhouse Software, Inc.

- 6.4.9 ClearCompany, LLC

- 6.4.10 Leapsome GmbH

- 6.4.11 Zavvy GmbH

- 6.4.12 Appical B.V.

- 6.4.13 Talentech Group AS

- 6.4.14 HR-ON ApS

- 6.4.15 Valamis Group Oy

- 6.4.16 WorkMotion Software GmbH

- 6.4.17 Employment Hero Pty Ltd.

- 6.4.18 Factorial HR, S.L.

- 6.4.19 Teamtailor AB

- 6.4.20 Abacus Umantis AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

北美人力資源合規軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)核心人力資源軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

北美人力資源合規軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)核心人力資源軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 人力資源管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署類型、組織規模、類型、最終用戶、地區和競爭對手分類,2021-2031 年

人力資源管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署類型、組織規模、類型、最終用戶、地區和競爭對手分類,2021-2031 年 核心人力資源軟體市場:依模組、部署模式、企業規模及產業分類-2026-2032年全球市場預測

核心人力資源軟體市場:依模組、部署模式、企業規模及產業分類-2026-2032年全球市場預測 員工績效管理軟體市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

員工績效管理軟體市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 2026年全球人力資源軟體市場報告績效管理系統市場:按組件、組織規模、部署類型和行業分類 - 2026-2032 年全球預測2026年全球核心人力資源軟體市場報告

2026年全球人力資源軟體市場報告績效管理系統市場:按組件、組織規模、部署類型和行業分類 - 2026-2032 年全球預測2026年全球核心人力資源軟體市場報告 人力資源管理軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類

人力資源管理軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類 核心人力資源軟體市場規模、佔有率和成長分析(按組件、部署類型、垂直產業和地區分類)-2026-2033年產業預測

核心人力資源軟體市場規模、佔有率和成長分析(按組件、部署類型、垂直產業和地區分類)-2026-2033年產業預測