|

市場調查報告書

商品編碼

2065445

員工入職前跟進和新員工入職自動化平台:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Preboarding And Onboarding Automation Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

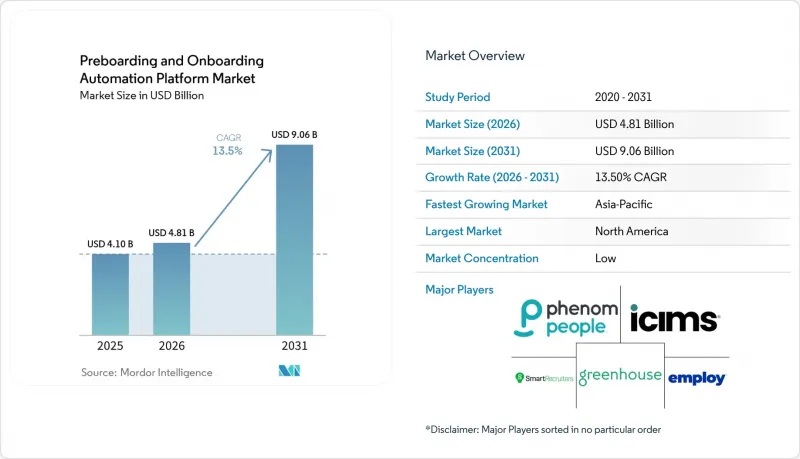

預計用於潛在員工跟進和新員工入職的自動化平台市場規模將從 2025 年的 41 億美元和 2026 年的 48.1 億美元成長到 2031 年的 90.6 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 13.50%。

本報告按部署模式(雲端、本地部署、混合部署)、企業規模(大型企業等)、最終用戶行業(銀行、金融服務和保險、醫療保健和生命科學等)、功能(從招聘到入職前準備、文件創建和檢驗等自動化流程)以及地區進行細分。市場預測以美元計價。

全球市場趨勢及對潛在員工跟進和新員工入職的自動化平台的洞察。

從人力資源工作流程過渡到數位化員工發展歷程

從人工調整到結構化數位化工作流程的轉變,仍然是自動化入職和新員工跟進平台市場最顯著的成長要素。傳統的入職流程依賴於電子郵件跟進、零散的清單以及人力資源、IT、法務和設施管理部門的單獨回复,隨著招聘人數的增加,不可避免地導致流程延誤。如今,雇主需要一個單一、一致的工作流程,該流程應在員工接受錄用通知後立即啟動,並貫穿所有文書工作、存取權限設定和入職首日準備。整合這些步驟能夠幫助採購者更清楚地了解完成情況的差距和初始體驗徵兆,從而將入職流程從單純的官僚程序轉變為更有價值的人才保留管理工具。能夠將工作流程完成情況與更快的入職準備和可衡量的成本節約聯繫起來的供應商,正在吸引自動化入職和新員工跟進平台市場採購方的廣泛關注。

混合式和分散式招募的擴展增加了對入職前自動化的需求。

混合辦公和遠距辦公的興起改變了新員工入職前必須完成的入職前準備工作的性質,進而影響了入職前準備和入職自動化平台市場。由於新員工、經理和負責人通常不在同一地點,文件收集、設備採購、溝通和準備等任務必須非同步完成。與傳統的招募模式相比,這顯著降低了基於固定辦公地點的常規入職流程的效率。預計到2026年底,超過70%的員工每月至少遠距辦公五天,因此對基於位置的入職流程的需求持續成長。那些能夠幫助雇主根據國家/地區、實體和經理調整任務,而無需每次都重新建構工作流程的供應商,在入職自動化平台市場中佔據更有利的地位。

分散的傳統人力資源系統阻礙了端到端的工作流程協調。

在入職前和入職自動化平台市場中,人力資源環境的分散化仍然是最持久的營運瓶頸。許多雇主使用多個系統,這些系統部署時間各不相同,且並非設計為統一架構來處理招募、人力資源、薪資、福利、培訓和身分管理等任務。在這樣的環境中,主要瓶頸往往並非工作流程設計本身,而是系統之間的連結點。 SAP 的「2026 年整合訊息」強調了在招募和入職作業之間建立共用資料流之前需要進行大量手動重複輸入工作,這也解釋了為什麼系統脫節會持續延緩價值實現。因此,入職前和新員工入職自動化平台市場的買家正面臨更長的引進週期、更高的服務需求以及價值實現時間的延遲。

細分市場分析

到2025年,基於雲端的部署將佔總收入的68.41%,成為自動化入職和崗前培訓平台市場的主導模式。買家更青睞雲端平台,因為它們無需新建本地基礎設施,即可輕鬆整合招募管理系統(ATS)、人力資源資訊系統(HRIS)和薪資核算系統。在法規環境下,本地部署仍然佔據重要地位,因為在這些環境下,資料管理和內部託管仍然比柔軟性更為重要。混合部署預計到2031年將以16.47%的複合年成長率成長,成為自動化入職和崗前培訓平台市場中成長最快的模式。

這一趨勢反映出許多全球企業希望在不取代現有核心人力資源管理系統的情況下,實現入職流程的現代化。混合配置方案允許企業在保留其核心記錄系統的同時,在其基礎上添加基於雲端的使用者體驗和合規性功能。 SAP 於 2026 年 3 月與 SmartRecruiters 和 SuccessFactors 的整合工作表明,將招聘和入職流程關聯起來可以減輕這種轉型模式下手動重新輸入的負擔。在入職自動化平台產業,能夠同時支援穩定的記錄系統運作和靈活的工作流程編配的供應商佔據著最有利的地位。

到2025年,大型企業將佔銷售額的62.37%,成為自動化入職和招募平台解決方案市場最大的買家群體。它們的規模、多營業單位招募需求以及高合規風險,使得採用端到端工作流程自動化更具合理性。一家財富500強製造企業報告稱,透過在各部門實施自動化,每年節省成本超過40萬美元,投資報酬率超過5倍。預計到2031年,中小企業的複合年成長率將達到17.83%,這表明自動化技術的應用範圍正在從大型企業擴展到更廣泛的群體。

中小企業的成長得益於按用戶月度定價 (PEPM)、無程式碼工作流程建構器和捆綁式合規庫,這些都降低了准入門檻。然而,這些採購企業通常缺乏專門的人力資源技術團隊,因此他們仍然需要更快的部署速度和更全面的供應商支援。 Intuit 透過 GoCo 進軍整合式人力資源自動化領域,也印證了小規模雇主需要整合式薪資核算、人力資源和入職解決方案,而不是一系列獨立工具的觀點。因此,在入職前和入職自動化平台產業,大型企業和中小企業在「從第一天起即可運作」的需求差距正在縮小,但大型企業在實施便利性方面仍然具有優勢。

區域分析

到2025年,北美將佔全球整體收入的39.61%,成為自動化入職和職前(I-9)工作流程的最大區域市場。該地區受益於成熟的人力資源軟體普及、遠端和混合招聘的高比例,以及引導雇主建立符合審計要求的工作流程的合規環境。在美國,即將於2026年3月修訂的美國移民及海關執法局(ICE)關於I-9表格重大違規行為的標準將產生重大影響。遠端檢驗中的錯誤,例如未勾選替代程序複選框或在使用遠端文件審核時未滿足E-Verify要求,現在可能導致每份表格最高2,861美元的直接罰款。這項變更正在推動自動化入職和崗前(I-9)工作流程市場對包含遠端I-9和E-Verify合規工作流程作為標準功能的產品的需求。

在歐洲,GDPR 的處理要求以及歐盟人工智慧法律帶來的廣泛管治負擔正在產生重大影響。德國仍然是監管最嚴格的地區,因為有關僱用數據和與員工代表委員會協商的規定可能會影響人工智慧驅動的入職系統的實施方式。根據第 26(7) 條,員工通知義務將在 2026 年 8 月之後繼續有效,要求平台在其員工流程中支援資訊揭露程序。英國已採用自身的工作資格驗證流程,而南美洲仍處於起步階段,其部署主要由跨國公司而非國內企業推動。

預計到2031年,亞太地區將以14.71%的複合年成長率成長,成為入職前和入職自動化平台市場成長最快的地區。這一成長主要得益於印度、澳洲、韓國和新加坡人力資源部門的數位轉型。新加坡的「就業準證」流程和菲律賓的多機構法定註冊要求,都催生了對在地化工作流程範本的明確需求。日本和中國仍蘊藏著巨大的未開發潛力,但這兩個國家在語言、資料管理和溝通模式方面都需要更深入的在地化。在中東和非洲地區,需求較為集中,主要由沙烏地阿拉伯、阿拉伯聯合大公國(阿拉伯聯合大公國)、南非和奈及利亞推動,這些國家的跨國公司子公司和區域科技公司正採用雲端優先的入職系統。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 從人力資源工作流程過渡到數位化員工旅程

- 混合和分散式架構的採用,推動了「第一天」實施之前自動化需求的增加。

- 對勞動法規、隱私法規和招聘法規的合規自動化需求。

- 跨 ATS、HRIS、薪資核算和體驗層的平台整合。

- 在應對「零運作」危機時,從人力資源部門到IT部門的身份配置是首要任務。

- 跨境招募增加了對在地化入職前程序和工作資格驗證流程的需求。

- 市場限制因素

- 分散的傳統人力資源系統正在減緩端到端工作流程的編配。

- 中小企業預算審查面臨的挑戰以及人力資源技術投資的較長投資回收期。

- 歐盟人工智慧法律和員工通知要求增加了人工智慧驅動的資料流的管治負擔。

- 由於遠距 I-9 程序和身分驗證涉及法律責任,受監管的雇主們都保持著謹慎的態度。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 基於雲端的

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按最終用戶行業分類

- BFSI

- 醫療保健和生命科學

- IT/通訊

- 零售與電子商務

- 工業製造

- 政府/公共部門

- 其他終端用戶產業

- 功能性別

- 從招募到入職前流程的自動化。

- 文件編制與檢驗

- 合規與身分管治

- IT資源配置與工作區搭建

- 提高學習效率和生產力

- 員工體驗與旅程管理

- 勞動力分析與情報

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Phenom People, Inc.

- iCIMS, Inc.

- Greenhouse Software, Inc.

- SmartRecruiters, Inc.

- Employ, Inc.

- Lever, Inc.

- ClearCompany, LLC

- Bamboo HR LLC

- GoCo.io, Inc.

- Namely, Inc.

- Talentech Group AS

- Tribepad Ltd

- EMP Trust Solutions, LLC

- Click Boarding, LLC

- Enboard.Me Pty Ltd.

- WorkBright

- NEO Global Pty Ltd.

- Affirm Software Group Pty Ltd.

- HROnboard Pty Ltd.

- Onboarded Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the preboarding and onboarding automation platform market size is projected to expand from USD 4.10 billion in 2025 and USD 4.81 billion in 2026 to USD 9.06 billion by 2031, registering a CAGR of 13.50% between 2026 and 2031.

This report is Segmented by Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and More), End-User Industry (BFSI, Healthcare and Life Sciences, and More), Functionality (Recruitment-To-Preboarding Automation, Documentation and Verification, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Preboarding And Onboarding Automation Platform Market Trends and Insights

Shift from Manual HR Workflows to Digital Employee Journeys

The move from manual coordination to structured digital workflows remains the clearest growth driver in the preboarding and onboarding automation platform market. Older onboarding routines relied on email follow-ups, disconnected checklists, and separate actions from HR, IT, legal, and facilities, which made delays hard to avoid as hiring volumes rose. Employers now want one workflow that starts as soon as the offer is accepted and continues through documentation, access setup, and first-day readiness. As these steps are brought together, buyers gain clearer visibility into completion gaps and early experience signals, making onboarding more useful for retention management, not just administration. Vendors that can tie workflow completion to faster readiness and measurable cost savings are gaining stronger buyer attention in the preboarding and onboarding automation platform market.

Hybrid and Distributed Hiring Expands Pre-Day-One Automation Needs

Hybrid and remote work changed what preboarding must complete before day one in the preboarding and onboarding automation platform market. New hires, managers, and verification contacts are often not in the same place, so document collection, equipment coordination, communication, and readiness tasks need to run asynchronously. That makes fixed office-based onboarding routines much less effective than they were in earlier hiring models. More than 70% of the workforce is expected to work remotely at least 5 days per month by the end of 2026, which keeps demand high for geography-aware onboarding flows. Vendors that let employers adapt tasks by country, legal entity, and manager without rebuilding the workflow each time are in a stronger position in the market for preboarding and onboarding automation platforms.

Fragmented Legacy HR Stacks Slow End-To-End Workflow Orchestration

Fragmented HR environments remain the most persistent operational restraint in the preboarding and onboarding automation platform market. Many employers still run recruiting, HR, payroll, benefits, learning, and identity tasks across systems acquired at different times and not built to work as a single architecture. In that setting, the main bottleneck is often the system connection point and not the workflow design itself. SAP's 2026 integration messaging highlighted the significant manual re-entry that existed before shared data flow was established across hiring and onboarding tasks, underscoring why disconnected stacks continue to delay value realization. The result is longer implementation cycles, heavier service requirements, and slower time-to-value for buyers in the preboarding and onboarding automation platform market.

Other drivers and restraints analyzed in the detailed report include:

- Compliance Automation Demand Across Labor, Privacy, and Hiring Rules

- Platform Consolidation Across ATS, HRIS, Payroll, and Experience Layers

- Budget Scrutiny And Longer HR Tech Payback Hurdles In SMBs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment accounted for 68.41% of revenue in 2025, making it the leading model in the preboarding and onboarding automation platform market. Buyers favored cloud platforms because they can connect more easily across ATS, HRIS, and payroll without requiring new on-premises infrastructure. On-premises deployment remained relevant in a narrower set of regulated environments where data control and internal hosting still carry more weight than flexibility. Hybrid deployment is projected to expand at a 16.47% CAGR through 2031, which makes it the fastest-growing model in this preboarding and onboarding automation platform market.

This pattern reflects the fact that many global employers want to modernize onboarding workflows without replacing the full HR backbone they already run. A hybrid setup lets them keep the core system of record in place while adding cloud-based experience and compliance layers on top. SAP's March 2026 integration work with SmartRecruiters and SuccessFactors demonstrated how a connected flow between recruiting and onboarding can reduce manual re-entry during this transition model. Within the preboarding and onboarding automation platform industry, vendors that support both stable system-of-record operations and flexible workflow orchestration are in the strongest position.

Large enterprises accounted for 62.37% of revenue in 2025, making them the largest buyer group in the preboarding and onboarding automation platform market. Their scale, multi-entity hiring needs, and greater compliance exposure make end-to-end workflow automation easier to justify. A Fortune 500 manufacturing case documented annual savings of more than USD 400,000 and more than 5x ROI after automation was applied across divisions. Small and medium-sized businesses are projected to grow at a 17.83% CAGR through 2031, which shows that adoption is broadening beyond the largest employers.

SMB growth is being helped by PEPM-priced offerings, no-code workflow builders, and bundled compliance libraries that reduce the entry barrier. At the same time, these buyers still expect faster activation and greater vendor support because they often lack dedicated HR technology teams. Intuit's move into connected HR automation through GoCo also supports the view that smaller employers want unified payroll, HR, and onboarding coverage rather than a collection of separate tools. The preboarding and onboarding automation platform industry is therefore seeing the gap narrow between what large enterprises and SMBs expect from day-zero readiness, even if the buying path remains easier for larger accounts.

Geography Analysis

North America accounted for 39.61% of global revenue in 2025, making it the largest regional market for preboarding and onboarding automation platforms. The region benefits from mature HR software adoption, a high level of remote and hybrid hiring, and a compliance environment that pushes employers toward audit-ready workflows. The United States is now being shaped by the March 2026 ICE revision to the substantive violation standards for Form I-9. Remote-verification errors, including failure to mark the alternative procedure checkbox and failure to meet E-Verify requirements while using remote document examination, can now trigger direct penalty exposure of up to USD 2,861 per form. That shift is increasing demand for remote I-9 and E-Verify-enabled workflows as standard product features in the preboarding and onboarding automation platform market.

Europe is shaped by GDPR handling requirements and the wider governance burden created by the EU AI Act. Germany remains the most regulation-heavy environment because employment data rules and works council consultation can affect how AI-enabled onboarding systems are deployed. Article 26(7) worker notification obligations remain relevant from August 2026, which adds disclosure steps that platforms must support in employee-facing flows. The UK follows its own right-to-work verification path, while South America remains earlier stage and is still led mainly by multinational rollouts rather than domestic-first deployments.

Asia-Pacific is projected to expand at a 14.71% CAGR through 2031, which makes it the fastest-growing region in the preboarding and onboarding automation platform market. Growth is being supported by HR digitization in India, Australia, South Korea, and Singapore. Singapore's Employment Pass process and the Philippines' multi-agency statutory enrollment needs create clear demand for localized workflow templates. Japan and China remain large untapped opportunities, but both require stronger localization around language, data control, and communication patterns. The Middle East and Africa add concentrated demand, driven by Saudi Arabia, the UAE, South Africa, and Nigeria, where multinational subsidiaries and regional technology employers are adopting cloud-first onboarding systems.

- Phenom People, Inc.

- iCIMS, Inc.

- Greenhouse Software, Inc.

- SmartRecruiters, Inc.

- Employ, Inc.

- Lever, Inc.

- ClearCompany, LLC

- Bamboo HR LLC

- GoCo.io, Inc.

- Namely, Inc.

- Talentech Group AS

- Tribepad Ltd

- EMP Trust Solutions, LLC

- Click Boarding, LLC

- Enboard.Me Pty Ltd.

- WorkBright

- NEO Global Pty Ltd.

- Affirm Software Group Pty Ltd.

- HROnboard Pty Ltd.

- Onboarded Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift From Manual HR Workflows to Digital Employee Journeys

- 4.2.2 Hybrid and Distributed Hiring Expands Pre-Day-One Automation Needs

- 4.2.3 Compliance Automation Demand Across Labor, Privacy, and Hiring Rules

- 4.2.4 Platform Consolidation Across ATS, HRIS, Payroll, and Experience Layers

- 4.2.5 HR-To-IT Identity Provisioning Becomes a Day-Zero Readiness Priority

- 4.2.6 Cross-Border Hiring Raises Need for Localized Preboarding and Right-To-Work Flows

- 4.3 Market Restraints

- 4.3.1 Fragmented Legacy HR Stacks Slow End-To-End Workflow Orchestration

- 4.3.2 Budget Scrutiny and Longer HR Tech Payback Hurdles in SMBs

- 4.3.3 EU AI Act and Worker-Notice Duties Raise Governance Burden for AI-Enabled Flows

- 4.3.4 Remote I-9 and Identity Verification Liability Keeps Regulated Employers Cautious

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-Sized Businesses

- 5.3 By End User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Information Technology and Telecom

- 5.3.4 Retail and E-commerce

- 5.3.5 Industrial Manufacturing

- 5.3.6 Government and Public Sector

- 5.3.7 Other End-user Industries

- 5.4 By Functionality

- 5.4.1 Recruitment-to-Preboarding Automation

- 5.4.2 Documentation and Verification

- 5.4.3 Compliance and Identity Governance

- 5.4.4 IT Provisioning and Workspace Enablement

- 5.4.5 Learning and Productivity Enablement

- 5.4.6 Employee Experience and Journey Management

- 5.4.7 Workforce Analytics and Intelligence

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Netherlands

- 5.5.2.8 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Phenom People, Inc.

- 6.4.2 iCIMS, Inc.

- 6.4.3 Greenhouse Software, Inc.

- 6.4.4 SmartRecruiters, Inc.

- 6.4.5 Employ, Inc.

- 6.4.6 Lever, Inc.

- 6.4.7 ClearCompany, LLC

- 6.4.8 Bamboo HR LLC

- 6.4.9 GoCo.io, Inc.

- 6.4.10 Namely, Inc.

- 6.4.11 Talentech Group AS

- 6.4.12 Tribepad Ltd

- 6.4.13 EMP Trust Solutions, LLC

- 6.4.14 Click Boarding, LLC

- 6.4.15 Enboard.Me Pty Ltd.

- 6.4.16 WorkBright

- 6.4.17 NEO Global Pty Ltd.

- 6.4.18 Affirm Software Group Pty Ltd.

- 6.4.19 HROnboard Pty Ltd.

- 6.4.20 Onboarded Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

OKR和目標管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)缺勤管理軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)北美人力資源合規軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲員工入職:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)核心人力資源軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

OKR和目標管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)缺勤管理軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)北美人力資源合規軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲員工入職:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)核心人力資源軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 人力資源管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署類型、組織規模、類型、最終用戶、地區和競爭對手分類,2021-2031 年

人力資源管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署類型、組織規模、類型、最終用戶、地區和競爭對手分類,2021-2031 年 員工績效管理軟體市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

員工績效管理軟體市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 2026年全球人力資源軟體市場報告

2026年全球人力資源軟體市場報告 績效管理系統市場:按組件、組織規模、部署類型和行業分類 - 2026-2032 年全球預測2026年全球核心人力資源軟體市場報告

績效管理系統市場:按組件、組織規模、部署類型和行業分類 - 2026-2032 年全球預測2026年全球核心人力資源軟體市場報告