|

市場調查報告書

商品編碼

2063965

核心人力資源軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Core HR Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

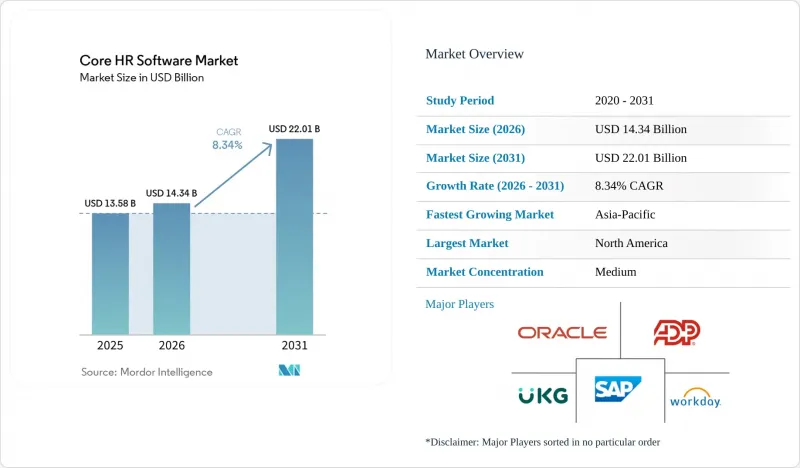

根據 Mordor Intelligence 預測,核心人力資源軟體市場預計到 2025 年將達到 135.8 億美元,到 2026 年將達到 147.4 億美元。

此外,預計從 2026 年到 2031 年,該產業將以 8.34% 的複合年成長率成長,到 2031 年達到 220.1 億美元。

本報告按組件(軟體和服務)、部署方式(雲端、本地部署、混合部署)、組織規模(中小企業和大型企業)、行業(IT和電信、銀行、金融服務和保險、醫療保健和生命科學、零售和電子商務、製造業、政府和公共部門等)以及地區(北美等)進行細分。市場預測以價值(美元)表示。

全球核心人力資源軟體市場趨勢及洞察

人力資源套件的雲端優先實施

隨著季度SaaS版本不斷推出防火牆後無法複製的創新功能,企業正逐步淘汰本地部署系統。供應商的產品藍圖日益將雲端交付與基於代理的人工智慧相結合,使客戶能夠以極低的額外成本體驗預測性員工流動分析、自動化合規性檢查和互動式自助服務。跨國公司也依賴超大規模資料中心業者資料中心來處理跨越數十個司法管轄區的複雜稅務系統。然而,在遷移之前提取和清理數十年的薪資歷史記錄仍然是一項繁瑣的工作,這推動了對實施服務的需求。

整合人工智慧驅動的人才分析

預計大型企業將在2025年大規模試點部署人工智慧驅動的人才管理工具,到2026年,企業在人力資源人工智慧方面的預算中位數將達到160萬美元。近期發布的Workday「人才最佳化」和SAP「SuccessFactors」智慧工作流程等產品,已超越了簡單的描述性儀表板,能夠提供晉升建議、繼任風險視覺化以及績效評估文件的自動生成。雖然在需要審計追蹤的高度監管行業中,人工智慧的應用正在加速推進,但許多中型企業仍然缺乏正式的管治政策,阻礙了其全面實施。

對資料居住和主權的擔憂

歐盟的《一般資料保護規範》(GDPR)、中國的《個人資料保護法》和印度的《數位個人資料保護法》等法規要求某些員工屬性必須保留在所在國家/地區。這迫使供應商為每個地區維護獨立的實例,導致美國以外地區的功能標準化進程緩慢,基礎設施成本增加。國防、銀行和醫療保健產業的買家要求提供本地託管證明,因此資料居住已成為一項關鍵的評估標準。

細分市場分析

至2025年,軟體領域將佔據核心人力資源軟體市場的79.18%。這主要得益於薪資核算、福利和勞動力分析模組的大規模定期訂閱合約。目前,成長勢頭正轉向服務領域,因為資料遷移、跨國稅務配置和人工智慧管治都需要專業技術。因此,薪資核算管理外包、一級技術支援和持續最佳化合約正在擴大系統整合商和供應商的專業服務團隊的收入來源。

隨著人工智慧代理商自動執行低價值任務,顧問可以專注於提供技能框架和變革管理方面的建議,而由服務驅動的核心人力資源軟體市場預計將從 2026 年到 2031 年以 8.87% 的複合年成長率成長。 SAP 的 SmartRecruiters 整合可以將傳統的招募工作流程自動對應到 SuccessFactors,這已經減少了約 30% 的專業服務工作量,表明自動化可以將計費工作從配置轉移到策略制定。

到2025年,雲端採用率佔總支出的72.46%。這反映出買家對供應商管理的安全保障、快速的功能交付以及相比傳統本地部署更低的預付成本充滿信心。由於雲端核心人力資源系統具有可擴展性、自動更新、支援分散式辦公室以及減輕內部IT團隊在基礎設施維護和系統升級方面的負擔等優勢,企業越來越傾向於選擇雲端核心人力資源系統。然而,混合模式(允許敏感的薪資資料保留在本地,同時以SaaS形式運行新的人才管理模組)預計將成為所有部署類型中成長最快的,到2031年複合年成長率將達到9.28%。

在兩個環境之間保持即時資料同步在技術上極具挑戰性,通常需要中間件編配。 UKG 於 2026 年初收購 Inova Payroll,將提供一個可在空氣間隙網路內運作的混合引擎,這對於必須在主權和現代化之間取得平衡的受監管實體而言至關重要。成功的關鍵在於健全的 API管治、延遲管理以及供應商和客戶之間明確的安全責任分類。

區域分析

預計到2025年,北美將佔全球整體收入的38.96%,這得益於其成熟的諮詢生態系統、大型企業買家的集中以及相對寬鬆的資料傳輸法規。公共部門現代化仍然是一個值得關注的機遇,聯邦政府的HR 2.0舉措將從2026會計年度開始,為農業部等機構引入混合核心HCM(OPM.GOV)。然而,由於大多數財富1000強企業已經在使用雲端或混合套件,並將預算轉向技能市場、員工體驗層和分析附加元件,因此成長速度正在放緩。

預計到2031年,亞太地區的複合年成長率將達到10.11%,高於其他任何地區。在政府推動勞動合約規範化和提高稅務合規性的舉措的推動下,印度、中國和東南亞的中型企業在首次實現薪資核算數位化方面最為積極。 Darwinbox於2025年3月籌集了1.4億美元,用於拓展印度以外的市場,顯示投資者對該地區永續成長潛力充滿信心。中國和印度的本地資料保護法有利於在國內或區域內託管的平台,這使得擁有本地化基礎設施的供應商具有競爭優勢。

儘管歐洲、南美、中東和非洲的整體需求保持穩定,但各地區的模式卻不盡相同。基於GDPR的資料儲存要求促使跨國買家選擇混合雲或歐盟專屬雲端實例。由於巴西擁有複雜的電子社會勞動報告系統,因此在南美地區引領此一趨勢。同時,波灣合作理事會(GCC)成員國正在強制要求根據其工資保障系統提交工資單,這推動了區域性供應商的崛起。非洲市場仍在發展中,但行動裝置的高使用率正在推動人們對雲端薪資核算的興趣,從而繞過本地部署。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 優先採用基於雲端的人力資源套件。

- 遠距和混合辦公室模式的擴展

- 監管報告日益複雜

- 整合人工智慧驅動的人才分析

- 向基於技能的人才規劃轉型

- 新興國家中型企業市場需求不斷成長

- 市場限制因素

- 對資料居住和主權的擔憂

- 從舊版套件遷移成本高昂

- 人力資源技術實施人員短缺

- 持續的網路安全和隱私洩露

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 不同的發展

- 雲

- 現場

- 混合

- 按組織規模

- 小型企業

- 大公司

- 按行業

- 資訊科技/通訊

- BFSI

- 醫療保健和生命科學

- 零售與電子商務

- 製造業

- 政府/公共部門

- 其他工業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday Inc.

- Oracle Corporation

- SAP SE

- Automatic Data Processing Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- Paycom Software Inc.

- Cornerstone OnDemand Inc.

- BambooHR LLC

- Paylocity Holding Corporation

- Gusto Inc.

- Sage Group plc

- Rippling Inc.

- Zoho Corporation Pvt. Ltd.

- OrangeHRM Inc.

- SumTotal Systems LLC

- ClearCompany Inc.

- Ceipal Corp.

- Freshworks Inc.

- Darwinbox Digital Solutions Pvt. Ltd.

- Infor Inc.

- Paycor HCM Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the core HR software market size reached USD 13.58 billion in 2025 and is expected to reach USD 14.74 billion in 2026, growing to USD 22.01 billion by 2031, at a CAGR of 8.34% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment (Cloud, On-Premises, and Hybrid), Organization Size (SMEs, and Large Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare and Lifesciences, Retail and E-Commerce, Manufacturing, Government and Public Sector, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Core HR Software Market Trends and Insights

Cloud-First Adoption of HR Suites

Organizations continue to retire on-premises systems as quarterly SaaS releases deliver innovations that cannot be replicated behind the firewall. Vendor roadmaps increasingly couple cloud delivery with agentic AI, letting customers experiment with predictive attrition, automated compliance checks, and conversational self-service at minimal incremental cost. Multinational firms also lean on hyperscaler data centers to handle complex tax engines across dozens of jurisdictions. However, extracting and cleansing decades of payroll history before migration remains labor-intensive, reinforcing demand for implementation services.

AI-Driven Talent Analytics Integration

Large enterprises piloted AI-infused talent tools at scale in 2025, and corporate budgets for HR-focused AI climbed to a median of USD 1.6 million in 2026. Recent releases such as Workday's Talent Optimization and SAP's SuccessFactors agentic workflows move beyond descriptive dashboards, recommending promotions, surfacing succession risks, and drafting performance narratives automatically. Adoption is rapid in highly regulated sectors looking for audit trails, yet many mid-market firms still lack formal governance policies, slowing full deployment.

Data Residency and Sovereignty Concerns

Rules such as the GDPR in the European Union, the Personal Information Protection Law in China, and India's Digital Personal Data Protection Act mandate that certain employee attributes remain inside national borders. Vendors are therefore forced to maintain region-specific instances, which delays feature parity outside the United States and raises infrastructure costs. Buyers in defense, banking, and healthcare demand proof of local hosting, turning data residency into a primary evaluation criterion.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Remote and Hybrid Work Models

- Shift to Skills-Based Workforce Planning

- High Switching Costs From Legacy Suites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The software segment captured 79.18% of the core HR software market share in 2025, thanks to large recurring subscriptions for payroll, benefits, and workforce analytics modules. Growth momentum is now tilting toward services because data migration, multi-country tax configuration, and AI governance demand specialized expertise. Managed payroll outsourcing, tier-1 help-desk support, and continuous optimization contracts are therefore widening the revenue base for systems integrators and vendor professional services teams.

The core HR software market size attributed to services is forecast to climb at an 8.87% CAGR between 2026 and 2031 as AI agents automate low-value tasks, freeing consultants to advise on skills frameworks and change management. SAP's SmartRecruiters integration, which auto-maps legacy recruiting workflows into SuccessFactors, already trims professional services hours by about 30%, demonstrating how automation can shift billable effort from configuration to strategy.

Cloud installations represented 72.46% of spending in 2025, reflecting strong buyer confidence in vendor-managed security, rapid feature delivery, and lower upfront capital expenditure compared to traditional on-premises deployments. Organizations are increasingly favoring cloud-based core HR systems due to their scalability, automatic updates, and ability to support distributed workforces, while also reducing the burden on internal IT teams for infrastructure maintenance and system upgrades. Yet the hybrid model is on track for a 9.28% CAGR through 2031, the fastest within deployment types, because it allows sensitive payroll data to stay on-premises while newer talent modules run in SaaS.

Maintaining real-time data synchronization across two environments is technically demanding and often requires middleware orchestration. UKG's early-2026 acquisition of Inova Payroll provides a hybrid-ready engine capable of operating inside air-gapped networks, a move aimed at regulated agencies that must balance sovereignty with modernization. Success will hinge on robust API governance, latency management, and clear division of security responsibilities between vendor and customer.

Geography Analysis

North America retained 38.96% of global revenue in 2025, benefiting from established consulting ecosystems, a concentration of large enterprise buyers, and relatively permissive data-transfer rules. Public-sector modernization remains a notable opportunity as the federal HR 2.0 initiative rolls out a hybrid core HCM to agencies such as the Department of Agriculture beginning in fiscal 2026, OPM.GOV. Growth is easing, however, because most Fortune 1000 organizations already run cloud or hybrid suites and are redirecting budgets toward skills marketplaces, employee experience layers, and analytics add-ons.

Asia-Pacific is forecast to register a 10.11% CAGR through 2031, outstripping every other region. Demand is strongest among mid-market firms in India, China, and Southeast Asia that are digitizing payroll for the first time, encouraged by government efforts to formalize employment contracts and improve tax compliance. Darwinbox raised USD 140 million in March 2025 to fund expansion beyond India, signaling investor belief in a sustained regional growth runway. Local data-protection laws in China and India favor domestic or regionally hosted platforms, giving vendors that maintain localized infrastructure a competitive edge.

Europe, South America, the Middle East and Africa collectively offer steady but fragmented demand patterns. GDPR-driven residency rules nudge multinational buyers toward hybrid or EU-specific cloud instances. Brazil leads South America on adoption because of its intricate e-social labor reporting, while Gulf Cooperation Council states mandate Wage Protection System payroll files, spurring specialized regional vendors. African markets are still nascent but exhibit high mobile use and interest in cloud payroll that leapfrogs on-premises deployments.

- Workday Inc.

- Oracle Corporation

- SAP SE

- Automatic Data Processing Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- Paycom Software Inc.

- Cornerstone OnDemand Inc.

- BambooHR LLC

- Paylocity Holding Corporation

- Gusto Inc.

- Sage Group plc

- Rippling Inc.

- Zoho Corporation Pvt. Ltd.

- OrangeHRM Inc.

- SumTotal Systems LLC

- ClearCompany Inc.

- Ceipal Corp.

- Freshworks Inc.

- Darwinbox Digital Solutions Pvt. Ltd.

- Infor Inc.

- Paycor HCM Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first Adoption of HR Suites

- 4.2.2 Expansion of Remote and Hybrid Work Models

- 4.2.3 Increasing Regulatory Reporting Complexity

- 4.2.4 AI-Driven Talent Analytics Integration

- 4.2.5 Shift to Skills-Based Workforce Planning

- 4.2.6 Rising Mid-Market Demand in Emerging Economies

- 4.3 Market Restraints

- 4.3.1 Data Residency and Sovereignty Concerns

- 4.3.2 High Switching Costs From Legacy Suites

- 4.3.3 Shortage of HR Tech Implementation Talent

- 4.3.4 Persistent Cyber-security and Privacy Breaches

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 SMEs

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Lifesciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 Oracle Corporation

- 6.4.3 SAP SE

- 6.4.4 Automatic Data Processing Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Ceridian HCM Holding Inc.

- 6.4.7 Paycom Software Inc.

- 6.4.8 Cornerstone OnDemand Inc.

- 6.4.9 BambooHR LLC

- 6.4.10 Paylocity Holding Corporation

- 6.4.11 Gusto Inc.

- 6.4.12 Sage Group plc

- 6.4.13 Rippling Inc.

- 6.4.14 Zoho Corporation Pvt. Ltd.

- 6.4.15 OrangeHRM Inc.

- 6.4.16 SumTotal Systems LLC

- 6.4.17 ClearCompany Inc.

- 6.4.18 Ceipal Corp.

- 6.4.19 Freshworks Inc.

- 6.4.20 Darwinbox Digital Solutions Pvt. Ltd.

- 6.4.21 Infor Inc.

- 6.4.22 Paycor HCM Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

北美人力資源合規軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲員工入職:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美人力資源合規軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲員工入職:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 人力資源管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署類型、組織規模、類型、最終用戶、地區和競爭對手分類,2021-2031 年

人力資源管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署類型、組織規模、類型、最終用戶、地區和競爭對手分類,2021-2031 年 核心人力資源軟體市場:依模組、部署模式、企業規模及產業分類-2026-2032年全球市場預測

核心人力資源軟體市場:依模組、部署模式、企業規模及產業分類-2026-2032年全球市場預測 員工績效管理軟體市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

員工績效管理軟體市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 2026年全球人力資源軟體市場報告績效管理系統市場:按組件、組織規模、部署類型和行業分類 - 2026-2032 年全球預測2026年全球核心人力資源軟體市場報告

2026年全球人力資源軟體市場報告績效管理系統市場:按組件、組織規模、部署類型和行業分類 - 2026-2032 年全球預測2026年全球核心人力資源軟體市場報告 人力資源管理軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類

人力資源管理軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類 核心人力資源軟體市場規模、佔有率和成長分析(按組件、部署類型、垂直產業和地區分類)-2026-2033年產業預測

核心人力資源軟體市場規模、佔有率和成長分析(按組件、部署類型、垂直產業和地區分類)-2026-2033年產業預測