|

市場調查報告書

商品編碼

2073313

缺勤管理軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)Absence Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

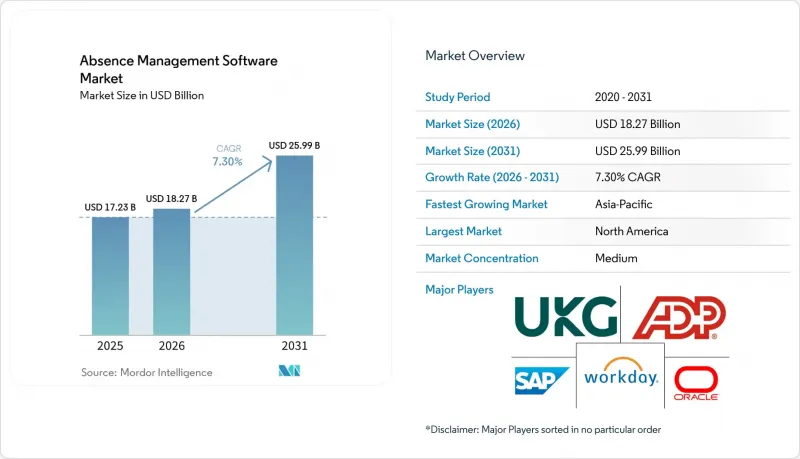

據 Mordor Intelligence 稱,2025 年缺勤管理軟體市場價值 172.3 億美元,預計 2026 年將成長至 182.7 億美元,到 2031 年將達到 259.9 億美元,2026 年至 2031 年的複合年成長率為 7.30%。

本報告按部署模式(軟體和服務)、部署方式(雲端、混合等)、最終用戶企業規模(大型企業和中小企業)、應用領域(假期管理、合規管理等)、最終用戶行業(資訊科技和電信等)以及地區進行細分。市場預測以美元計價。

全球缺勤管理軟體市場趨勢及洞察

多個司法管轄區對假日和勞動法規的要求更加嚴格

如果沒有管理軟體,跨轄區的休假規則正從人力資源部門面臨的簡單障礙轉變為雇主的核心營運挑戰。 2026年,德拉瓦、緬因州、明尼蘇達州、科羅拉多和紐約市要么推出了大規模帶薪休假計劃,要么擴大了現有福利。這使得包括華盛頓特區總合的15個轄區擁有強制性的帶薪家庭和醫療休假(PFML)框架。適用的規則通常取決於員工的實際工作地點,而不是雇主註冊成立的州。這意味著,每當在新的州僱用遠距員工時,都可能出現新的合規要求。此外,雇主必須同時管理《美國殘障人士法案》(ADA)、《帶薪家庭休假法案》(PWFA)和各州特定的PFML義務,這種組合產生了繁瑣的文檔、認證和通知程序,而這些程序無法透過電子表格工作流程進行統一處理。在管理軟體市場尚不成熟的情況下,能夠自動更新每個工作地點請假規則的供應商具有明顯的產品優勢,因為買家越來越重視準確性和速度,而不是通用工作流程的全面性。

實施雲端的人力資源管理軟體

雲端採用正從純粹的成本考量轉向功能性決策,這一轉變正在推動缺勤管理軟體市場的擴張。根據ISG發布的《2025年人力資源技術調查》,69%的組織已經實施了混合雲端的人力資源模式,83%的組織預計在2027年底前完成部署。調查也顯示,到2026年,人力資源人工智慧的平均預算將增加至160萬美元,顯示雲端平台如今已成為分析、自動化和人工智慧驅動的工作流程工具的標準基礎。領先的HCM供應商也在將原生缺勤管理功能整合到更廣泛的套件中,這提高了企業對整合、報告和工作流程連續性的期望。這一趨勢迫使缺勤管理軟體市場的獨立供應商深化夥伴關係關係,提高互通性,並展現出比以往採購週期中更清晰的業務價值。

與原有薪資和人力資源系統整合的複雜性。

與傳統薪資核算和人力資源系統的整合仍然是缺勤管理軟體廣泛應用的最大障礙之一。在ISG發布的2025年人力資源調查中,與核心平台的整合被列為繼資料安全之後的第二個重要採用因素。根據NFP的一項調查,過去兩年實施新人力資源技術的組織中,只有31%表示實施後效率顯著提高,而整合問題是許多其他組織收益有限的主要原因。許多大型企業仍然使用具有專有資料結構的系統進行薪資核算,導致新舊環境之間缺乏無縫資料流,例如缺勤餘額、薪資核算和休假事件。這正在減緩缺勤管理軟體市場的成長,因為採購公司通常需要中間件、IT支援和漫長的測試週期,才能在實際的合規工作流程中信任該系統。

細分市場分析

到2025年,軟體銷售額將佔總銷售額的65.12%,成為缺勤管理軟體市場中最大的組成部分。這一市場地位反映了企業對可配置平台的需求,這些平台能夠適應複雜的聯邦、州、地方政府和雇主特定的休假規則。大型企業往往更傾向於許可系統,因為每項合規例外情況通常都需要其自身的工作流程邏輯、核准途徑和文件集。即使沒有缺勤管理軟體,那些允許在現有的人力資源管理 (HCM) 和薪資核算環境中進行詳細配置的產品仍然很受歡迎。因此,軟體仍然是一項重要的支出構成比,因為許多買家希望直接控制政策制定和流程執行。

預計2026年至2031年間,服務業將以10.11%的複合年成長率成長,這顯示在整個缺勤管理軟體市場中,實施和營運支援的重要性日益凸顯。買家越來越意識到,擁有一個平台並不能消除配置更新、監管監控、員工溝通和案例管理支援的需求。對於小規模企業的人力資源團隊而言,託管服務和諮詢支援變得越來越重要,因為每次各州頒布新的帶薪家庭和醫療假 (PFML) 法規時,都需要進行額外的配置工作。 Oracle 於2026年2月發布的 Absence Management 26A 更新增加了一個人工智慧代理,該代理在處理員工請假申請時會參考已上傳的政策文件。這表明,曾經遊離於軟體層之外的任務正開始被納入產品設計。儘管如此,隨著雇主要求更快的實施速度、更少的違規以及將政策轉化為可重複的日常工作流程的更多支持,缺勤管理軟體市場仍有持續成長的空間。

到2025年,基於雲端的部署將佔總收入的55.24%,在缺勤管理軟體市場中佔據最大的市場佔有率(按部署類型分類)。這種主導地位源自於SaaS供應商能夠快速反映法規更新,尤其是在州或市級法規變更影響資格、福利設計或文件要求時。在簡化行政流程方面,這種更新速度比許多其他人力資源任務更為關鍵,因為錯誤可能同時影響薪資、資格和法律合規性。本地部署系統在政府機構、國防機構以及部分金融服務業仍然擁有穩固的部署基礎,因為這些機構對資料儲存位置和內部託管的監管仍然十分嚴格。這解釋了為什麼部署需求呈現多樣化,以及為什麼買家越來越要求供應商同時支援可管理性和速度。

基於雲端的部署也是成長最快的選擇,預計到2031年,該細分市場的缺勤管理軟體規模將以9.53%的複合年成長率成長。根據ISG的報告,預計到2027年底,83%的組織將採用基於雲端或混合的人力資源模式,這支持了向託管式缺勤管理平台持續轉型的趨勢。混合模式在中型企業和歐洲雇主中越來越受歡迎,他們既需要員工入口網站和基於雲端的分析功能,也希望對某些敏感的健康相關數據保持更嚴格的內部控制。這種架構符合那些高度重視稽核準備、安全認證和資料處理透明度的國家的採購需求。因此,在整個缺勤管理軟體市場中,擁有成熟混合藍圖的供應商更有優勢贏得那些既需要快速合規又需要更保守的資料管治的企業的合約。

區域分析

2025年,北美佔據了缺勤管理軟體市場35.12%的佔有率,成為最大的區域收入來源。美國仍然是主要驅動力,因為雇主通常需要同時應對聯邦《家庭醫療休假法案》(FMLA)、各州《帶薪家庭醫療休假法案》(PFML)、地方政府的帶薪病假條例以及《殘障人士法案》(ADA)規定的合理便利要求。 2026年,一些州和地方政府推出或擴大了帶薪休假計劃,進一步加劇了本已複雜的營運環境。 「地點規則」也是一個關鍵因素,因為休假義務通常根據員工的實際工作地點來確定,這使得分散式招募成為一個直接的合規問題。雖然加拿大和墨西哥由於各州不同的規章制度而增加了區域需求,但美國仍佔據北美缺勤管理軟體市場的大部分佔有率。

預計亞太地區將成為缺勤管理軟體市場規模成長最快的地區,2026年至2031年的複合年成長率將達到11.11%。該地區的情況與北美有所不同,因為印度和東南亞的許多雇主正在首次建立數位人力資源系統,而不是替換原有的休假管理平台。這推動了待開發區需求,並減輕了成熟市場中系統整合帶來的部分負擔。澳洲、日本、韓國和中國也透過不斷提高的勞動合規要求、數位化人力資源系統的廣泛應用以及對休假和工時義務更加正式的監管,推動了缺勤管理軟體市場的發展。

2025年,歐洲仍將是第三大區域叢集,由德國、英國和法國領軍。 2025年,歐洲員工的缺勤率佔其工作總工時的15%,相當於每年37個工作天。法國和義大利的健康相關缺勤率尤其高。 GDPR仍然是關鍵的選擇因素,因為它要求對員工健康記錄提供更強力的法律依據、更嚴格的管治以及更清晰的處理控制。該地區也受到新的報告義務和政策轉變的影響,這使得可配置系統比統一的單一功能工具更有價值。儘管規模仍然較小,但南美洲、中東和非洲的需求正在成長,這些地區的勞動法規正在製定中,雇主也正在努力改善其勞動管理系統中的資料管治標準。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 多個司法管轄區對假日和勞動法規的要求更加嚴格

- 實施雲端的人力資源管理軟體

- 遠距和混合辦公人員的政策管理要求

- 對自動化、分析和員工自助服務的需求

- 重返辦公室後,對支援服務的需求增加。

- 跨越五代的勞動力複雜性

- 市場限制因素

- 整合傳統薪資和人力資源系統的複雜性

- 敏感員工健康資料的隱私風險

- 在度假決策中不受控制地使用生成式人工智慧

- 捆綁式人才管理套件給獨立供應商帶來價格壓力

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 透過使用

- 假期管理

- 合規管理

- 殘疾和重返職場管理

- 分析與報告

- 按最終用戶行業分類

- 資訊科技(IT)和通訊

- 銀行、金融服務和保險(BFSI)

- 醫療保健和生命科學

- 工業製造

- 零售與電子商務

- 政府/公共部門

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 東南亞

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- WorkForce Software, LLC

- TimeClock Plus, LLC

- AbsenceSoft

- Qcera Inc.

- Optis

- Stiira Corporation

- Vacation Tracker Technologies Inc.

- Appogee HR Limited

- Calamari sp. z oo sp.k.

- absence.io GmbH

- Personio SE and Co. KG

- Timetastic Ltd.

- Venforce Inc.

- DaysPlan, Inc.

- Breathe HR Limited

- Leave Dates Ltd.

- actiTIME Inc.

- FINEOS Corporation

- TeamSense Inc.

- tamigo ApS

- Ironflow Technologies Inc.

- Bright HR Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the absence management software market was valued at USD 17.23 billion in 2025, grew to USD 18.27 billion in 2026, and is forecast to reach USD 25.99 billion by 2031, expanding at a CAGR of 7.30% during 2026-2031.

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud-Based, Hybrid, and More), End User Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Application (Leave Management, Compliance Management, and More), End-User Industry (Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Absence Management Software Market Trends and Insights

Stricter Multi-Jurisdiction Leave And Labor Compliance Requirements

Multi-jurisdiction leave rules have shifted from an HR inconvenience to a core operating issue for employers in the absence of management software. In 2026, Delaware, Maine, Minnesota, Colorado, and New York City either launched major paid leave programs or expanded existing entitlements, bringing the total to 15 states and Washington, D.C. that already had mandatory PFML frameworks in place. The applicable rule set usually follows the employee's physical work location, not the employer's state of incorporation, which means each remote hire in a new state can create a new compliance requirement. Employers also need to administer ADA, PWFA, and state PFML obligations in parallel, and that combination creates documentation, certification, and notice steps that spreadsheet workflows do not handle consistently. In the absence of a management software market, vendors that can automatically update leave rules by location gain a clear product advantage because buyers increasingly value accuracy and speed over generic workflow coverage.

Cloud-Based Human Resources Software Adoption

Cloud adoption has evolved into a capability decision rather than a narrow cost decision, and that shift is expanding the absence management software market. ISG's 2025 HR technology survey found that 69% of organizations already operated SaaS or hybrid cloud HR models, and 83% expected to do so by the end of 2027. The same survey showed average HR AI budgets rising to USD 1.6 million in 2026, indicating that cloud platforms are now the default base for analytics, automation, and AI-enabled workflow tools. Large HCM vendors are also embedding native absence functionality into broader suites, raising enterprise expectations for integration, reporting, and workflow continuity. That is pushing standalone vendors in the absence management software market to deepen partnerships, improve interoperability, and show clearer business value than they needed to prove in earlier buying cycles.

Legacy Payroll And Human Resources System Integration Complexity

Integration with legacy payroll and HR systems remains one of the clearest brakes on wider adoption in the absence management software market. ISG ranked core-platform integration as the second-most-important adoption factor in its 2025 HR survey, just behind data security. NFP found that only 31% of organizations that implemented new HR technology during the previous two years reported significant efficiency gains after deployment, and integration problems were a major reason many others saw limited returns. Many large employers still run payroll on systems with proprietary data structures, so absence balances, pay calculations, and leave events do not move cleanly between old and new environments. This slows the absence management software market because buyers often need middleware, IT support, and long testing cycles before they can trust the system in live compliance workflows.

Other drivers and restraints analyzed in the detailed report include:

- Remote And Hybrid Workforce Policy Administration Needs

- Demand For Automation, Analytics, And Employee Self-Service

- Sensitive Workforce Health Data Privacy Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 65.12% of revenue in 2025, making it the largest component of the absence management software market. That position reflects enterprise demand for configurable platforms that can be adapted to complex federal, state, local, and employer-specific leave rules. Large employers have often preferred licensed systems because each compliance exception can require its own workflow logic, approval path, and documentation set. In the absence of management software, this still favors products that allow deep configuration within existing HCM and payroll environments. The result is a component mix in which software remains the core spending category, as many buyers still want direct control over policy setup and process execution.

Services are forecast to expand at a 10.11% CAGR from 2026 to 2031, showing that implementation and operational support are becoming more important across the absence management software market. Buyers increasingly recognize that owning a platform does not remove the need for configuration updates, legal monitoring, employee communications, and case administration support. Each new state PFML rule creates additional setup work, making managed services and advisory support more relevant for mid-market employers with smaller HR teams. Oracle's February 2026 Absence Management 26A update added AI agents that reference uploaded policy documents during employee leave interactions, demonstrating how product design is beginning to absorb work that once sat outside the software layer. Even so, the absence management software market still offers room for continued growth, as employers seek faster deployment, fewer compliance errors, and more support for translating policy into repeatable daily workflows.

Cloud-based deployment accounted for 55.24% of revenue in 2025, giving it the largest share of the absence management software market by deployment mode. Its lead comes from the fact that SaaS vendors can quickly push statutory rule updates when a state or city change affects eligibility, benefit design, or documentation requirements. That update speed matters more in the absence of administration than in many other HR tasks because errors can affect pay, eligibility, and legal compliance simultaneously. On-premises systems still retain a real installed base in government, defense, and parts of financial services where data residency and internal hosting rules remain strict. This keeps deployment demand mixed, but it also reinforces why buyers increasingly ask vendors to support both control and speed.

Cloud-based deployment is also the fastest-growing option, with the absence management software market size for this segment projected to expand at a 9.53% CAGR through 2031. ISG reported that 83% of organizations expected to operate cloud- or hybrid-HR models by the end of 2027, supporting continued migration toward hosted absence platforms. Hybrid models are gaining ground among mid-market and European employers that want employee portals and cloud-based analytics while keeping some sensitive health-related data under tighter internal control. That structure aligns with procurement needs in countries where buyers place strong emphasis on audit readiness, security certifications, and transparency in data handling. Across the absence management software market, vendors with mature hybrid roadmaps are therefore better placed to win enterprise contracts that require both statutory agility and more conservative data governance.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By End User Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By Application

- Leave Management

- Compliance Management

- Disability and Return-to-Work Management

- Analytics and Reporting

- By End-User Industry

- Information Technology (IT) and Telecom

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- Industrial Manufacturing

- Retail and eCommerce

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 35.12% of the absence management software market share in 2025, making it the largest regional revenue pool. The United States remains the main driver because employers often have to administer federal FMLA, state PFML rules, local paid sick leave ordinances, and ADA accommodation requirements simultaneously. In 2026, several states and localities launched or expanded paid leave programs, further complicating an already dense operating environment. The work-situs rule also matters because leave obligations usually follow the employee's physical work location, making distributed hiring a direct compliance trigger. Canada and Mexico add regional demand through differing provincial rules and formalization trends, but the North American absence management software market still draws most of its weight from the United States.

Asia-Pacific is projected to record the fastest growth in the absence management software market size, at an 11.11% CAGR from 2026 to 2031. The regional story differs from North America because many employers in India and Southeast Asia are building digital HR systems for the first time rather than replacing older leave platforms. That creates more greenfield demand and reduces some of the integration drag seen in mature markets. Australia, Japan, South Korea, and China are also supporting the absence management software market through tighter labor compliance expectations, broader digital HR adoption, and more formal monitoring of leave and work-hour obligations.

Europe remained the third major regional cluster in 2025, led by Germany, the United Kingdom, and France. European employees missed 15% of assigned working time in 2025, equal to 37 working days per year, and France and Italy posted especially high health-related absence shares. GDPR remains a major selection factor because employee health records require stronger legal justification, tighter governance, and clearer processing controls. The region is also influenced by new reporting obligations and policy shifts that raise the value of configurable systems over rigid point tools. South America, the Middle East, and Africa remain smaller in scale, but demand is rising where labor regulation is formalizing, and employers are improving data governance standards for workforce systems.

- WorkForce Software, LLC

- TimeClock Plus, LLC

- AbsenceSoft

- Qcera Inc.

- Optis

- Stiira Corporation

- Vacation Tracker Technologies Inc.

- Appogee HR Limited

- Calamari sp. z o.o. sp.k.

- absence.io GmbH

- Personio SE and Co. KG

- Timetastic Ltd.

- Venforce Inc.

- DaysPlan, Inc.

- Breathe HR Limited

- Leave Dates Ltd.

- actITIME Inc.

- FINEOS Corporation

- TeamSense Inc.

- tamigo ApS

- Ironflow Technologies Inc.

- Bright HR Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Stricter Multi-Jurisdiction Leave and Labor Compliance Requirements

- 4.3.2 Cloud-Based Human Resources Software Adoption

- 4.3.3 Remote and Hybrid Workforce Policy Administration Needs

- 4.3.4 Demand for Automation, Analytics, and Employee Self-Service

- 4.3.5 Return-to-Office Accommodation Request Growth

- 4.3.6 Five-Generation Workforce Complexity

- 4.4 Market Restraints

- 4.4.1 Legacy Payroll and Human Resources System Integration Complexity

- 4.4.2 Sensitive Workforce Health Data Privacy Risks

- 4.4.3 Uncontrolled Generative Artificial Intelligence Use in Leave Decisions

- 4.4.4 Standalone Vendor Pricing Pressure from Bundled Human Capital Management Suites

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Application

- 5.4.1 Leave Management

- 5.4.2 Compliance Management

- 5.4.3 Disability and Return-to-Work Management

- 5.4.4 Analytics and Reporting

- 5.5 By End-User Industry

- 5.5.1 Information Technology (IT) and Telecom

- 5.5.2 Banking, Financial Services and Insurance (BFSI)

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Industrial Manufacturing

- 5.5.5 Retail and eCommerce

- 5.5.6 Government and Public Sector

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 Southeast Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 WorkForce Software, LLC

- 6.4.2 TimeClock Plus, LLC

- 6.4.3 AbsenceSoft

- 6.4.4 Qcera Inc.

- 6.4.5 Optis

- 6.4.6 Stiira Corporation

- 6.4.7 Vacation Tracker Technologies Inc.

- 6.4.8 Appogee HR Limited

- 6.4.9 Calamari sp. z o.o. sp.k.

- 6.4.10 absence.io GmbH

- 6.4.11 Personio SE and Co. KG

- 6.4.12 Timetastic Ltd.

- 6.4.13 Venforce Inc.

- 6.4.14 DaysPlan, Inc.

- 6.4.15 Breathe HR Limited

- 6.4.16 Leave Dates Ltd.

- 6.4.17 actiTIME Inc.

- 6.4.18 FINEOS Corporation

- 6.4.19 TeamSense Inc.

- 6.4.20 tamigo ApS

- 6.4.21 Ironflow Technologies Inc.

- 6.4.22 Bright HR Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

OKR和目標管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)北美人力資源合規軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)員工入職前跟進和新員工入職自動化平台:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲員工入職:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)核心人力資源軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

OKR和目標管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)北美人力資源合規軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)員工入職前跟進和新員工入職自動化平台:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲員工入職:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)核心人力資源軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 人力資源管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署類型、組織規模、類型、最終用戶、地區和競爭對手分類,2021-2031 年

人力資源管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署類型、組織規模、類型、最終用戶、地區和競爭對手分類,2021-2031 年 員工績效管理軟體市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

員工績效管理軟體市場規模、佔有率和趨勢分析報告:按組件、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 2026年全球人力資源軟體市場報告

2026年全球人力資源軟體市場報告 績效管理系統市場:按組件、組織規模、部署類型和行業分類 - 2026-2032 年全球預測2026年全球核心人力資源軟體市場報告

績效管理系統市場:按組件、組織規模、部署類型和行業分類 - 2026-2032 年全球預測2026年全球核心人力資源軟體市場報告