|

市場調查報告書

商品編碼

2063413

東協企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)ASEAN Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

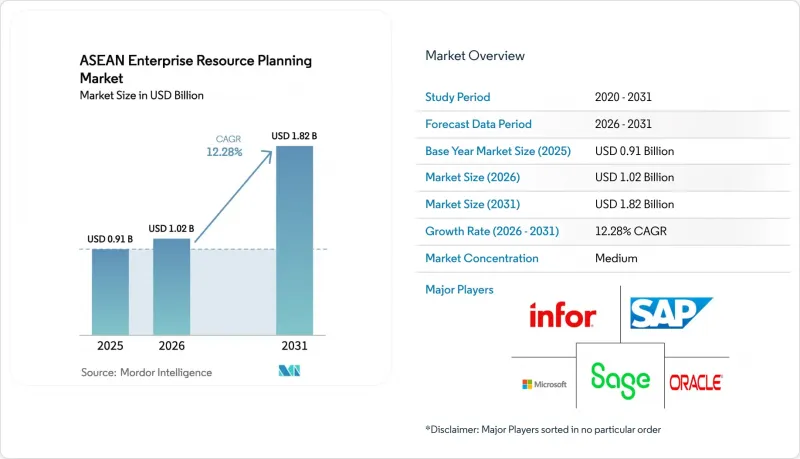

根據 Mordor Intelligence 預測,東協地區的企業資源規劃 (ERP) 市場規模將從 2025 年的 9.1 億美元成長到 2026 年的 10.2 億美元,到 2031 年將達到 18.2 億美元,2026 年至 2031 年的複合年成長率為 12.28%。

本報告按架構(雲端原生套件、行動優先ERP等)、業務功能(財務、會計等)、部署模式(本地部署、雲端部署)、組織規模(大型企業、中小企業)、產業(製造業、銀行、金融服務業等)和地區細分。市場預測以美元計價。

東協企業資源規劃(ERP)市場趨勢與洞察

加速東協中小企業雲端遷移

中小企業正在遷移到雲端原生套件,以避免伺服器方面的資本投資,實現模組的逐步擴展,並無需手動打補丁即可滿足最新的法律法規要求。 2024 年後成立的數位化原生零售商和物流公司完全拋棄了桌面會計系統,轉而選擇整合庫存管理、薪資核算和電子帳單的訂閱套餐。馬來西亞和印尼的補貼計畫定期報銷高達第一年成本一半的費用,將投資回收期縮短至 18 個月以內。提供免費試用和本地化稅務引擎的供應商正在迅速贏得客戶,而季度自動續訂則確保了企業能夠應對快速變化的監管規定,並減少因審計而導致的系統停機時間。

政府擴大數位經濟舉措

在區域政策框架中,ERP軟體如今被視為一項基礎基礎設施。政府入口網站和API整合的供應商優先採購評估,以及低利率轉型支援貸款,正在推動製造商、醫療保健機構和服務公司的系統升級。泰國的「泰國4.0」獎勵、印尼的聯合資金籌措藍圖以及新加坡的「智慧國家2.0」計畫共同保障了升級成本,並將ERP實施作為貿易融資、稅收優惠或快速核准的先決條件。即時發票和電子報稅等執行機制正在將政策從單純的目標轉化為必須立即執行的營運要求。

數據主權和本地化法規

印尼、泰國和越南的法規強制要求公民資料和敏感記錄必須在國內存儲,這迫使ERP供應商在國內雲端區域或混合配置下運作。印尼政府第71/2019號法規規定,所有處理公民數據的電子系統都必須在國內存儲和處理信息,這實際上禁止了政府承包商、醫療機構和金融機構採用純粹基於公共雲端的ERP系統,除非供應商在印尼境內建立資料中心。額外的審計、基礎設施和法律成本導致訂閱價格上漲高達四分之一,並導致與沒有居住要求的市場相比,功能標準化進程更為緩慢。無法承擔私有雲端成本的公司被迫推遲現代化改造,並維護大量本地系統,這阻礙了整體成長。

細分市場分析

雙層架構的成長率高達 13.08%,成為東協企業資源規劃 (ERP) 市場成長最快的細分領域。該架構使 SAP 和 Oracle 總部系統能夠與 NetSuite 和 Business Central 等子公司平台實現夜間同步。這種同步消除了手動外匯轉換的錯誤,簡化了財務報告流程,並將合併會計週期從數週縮短至數天。到 2025 年,雲端原生套件將佔市場採用率的 41.12%,而行動優先平台則滿足了物流和現場服務供應商的需求,他們需要透過智慧型手機無縫存取其營運系統。

區域合規要求極大地推動了這種架構的採用。由於東協五大主要市場的電子稅務入口網站、薪資核算法規和發票格式各不相同,客製化單一的全球版本在經濟上不可行。因此,子公司可以在熟悉當地法規的區域合作夥伴的支持下部署本地化平台,並在三個月內完成運作。同時,總部可以集中控制整個集團的報告和財務監督。因此,這種兩階段部署模式為混合部署奠定了基礎,鞏固了其在市場成長和發展中的作用。

隨著企業對跨越11個法律制度的薪資核算、休假管理和福利處理提出更高的要求,人力資本管理套件預計到2031年將以13.28%的年均成長率成長,超過金融業。儘管財務和會計領域佔總支出的35.16%,但其成長速度正在放緩,因為許多公司已經完成了核心帳簿的自動化。分散的社保法規意味著公司會因計算錯誤而受到處罰,這使得薪資核算準確性成為經營團隊面臨的風險。覆蓋印尼、馬來西亞、泰國、新加坡、菲律賓和越南的整合式雲端薪資核算系統可將人工報告錯誤減少三分之一以上。因此,與加班費和遣散費相關的主導複雜性正在加速東協企業資源規劃(ERP)市場對現代化人力資本管理套件的需求。

市場細分為財務、人力資源、供應鏈管理、製造、採購和客戶關係管理 (CRM)。財務模組仍然是 ERP 系統實施的基礎,因為它在財務報告、預算、稅務和合規方面發揮著至關重要的作用。然而,隨著該地區企業拓展跨境貿易並尋求更清晰地了解供應商網路、庫存管理和物流,供應鏈和採購功能的應用也日益增多。同時,隨著企業將客戶參與、銷售預測和服務管理置於優先地位,CRM 模組也越來越受歡迎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速東協中小企業雲端遷移

- 政府加大力度發展數位經濟

- 將人工智慧和分析技術整合到ERP套件中

- 為子公司實施模組化、兩層架構的ERP系統。

- 行動工作者。

- ESG報告需求的激增正在推動ERP系統升級。

- 市場限制因素

- 數據主權和本地化法規

- 東協地區ERP實施人員短缺

- 整合舊有系統的複雜性

- 中小企業總擁有成本高

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 以建築學為例

- Cloud-Native Suite

- 行動優先的ERP

- 社交/協作型企業資源規劃

- 雙層/邊緣ERP

- 業務職能

- 財會

- 供應鍊和營運

- 人力資本管理

- 客戶關係與商務

- 生產執行和品質

- 按部署模式

- 現場

- 雲

- 按組織規模

- 大公司

- 小型企業

- 按行業分類

- 製造業

- 零售與電子商務

- BFSI

- 政府/公共部門

- 資訊科技/通訊

- 醫療保健和生命科學

- 其他工業部門

- 按地區

- 新加坡

- 泰國

- 馬來西亞

- 印尼

- 菲律賓

- 其他東南亞國協

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Unit4 NV

- IFS AB

- Infor Inc.

- Sage Group Plc

- Workday Inc.

- SYSPRO(Pty)Ltd.

- Acumatica Inc.

- Ramco Systems Ltd.

- HashMicro Pte. Ltd.

- Epicor Software Corporation

- QAD Inc.

- Deskera Holdings Ltd.

- SunFish DataOn Philippins Inc.

- Zoho Corporation Pvt. Ltd.

- ECOUNT Co., Ltd.

- Highnix Pte. Ltd.

- HashMicro Pte. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the aSEAN enterprise resource planning market size is expected to grow from USD 0.91 billion in 2025 to USD 1.02 billion in 2026 and is forecast to reach USD 1.82 billion by 2031 at a 12.28% CAGR over 2026-2031.

This report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, BFSI, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

ASEAN Enterprise Resource Planning Market Trends and Insights

Cloud Migration Acceleration Among ASEAN SMEs

Small and medium enterprises are shifting to cloud-native suites to avoid capital expenditure on servers, scale modules incrementally, and keep statutory requirements up to date without manual patching. Digital-native retailers and logistics firms founded after 2024 bypassed desktop accounting entirely, choosing subscription packages that bundle inventory, payroll, and e-invoicing. Subsidy programs in Malaysia and Indonesia routinely offset up to half of first-year fees, compressing payback periods to under 18 months. Vendors that offer free trials and localized tax engines win conversions quickly, and quarterly automatic updates ensure compliance with rapid regulatory changes, reducing audit-related downtime.

Rising Government Digital Economy Initiatives

Regional policy frameworks now treat ERP software as foundational infrastructure. Preferential procurement scoring for suppliers connected via API to government portals and low-interest transformation loans pressure manufacturers, healthcare providers, and service firms to upgrade. Thailand 4.0 incentives, Indonesia's co-funding roadmap, and Singapore's Smart Nation 2.0 collectively underwrite upgrade costs, making ERP adoption a prerequisite for accessing trade-finance, tax holidays, or fast-track licensing. Enforcement mechanisms, such as real-time invoice or e-tax submission, convert policy into immediate operating requirements rather than aspirational goals.

Data Sovereignty and Localization Regulations

Mandates in Indonesia, Thailand, and Vietnam require local data storage for citizen or sensitive records, forcing ERP vendors to operate domestic cloud regions or hybrid topologies. Indonesia's Government Regulation 71/2019 mandates that all electronic systems handling citizen data must store and process information within the country, effectively prohibiting pure public-cloud ERP deployments for government contractors, healthcare providers, and financial institutions unless vendors establish in-country data centers.Additional audit, infrastructure, and legal costs inflate subscription pricing by up to one-quarter and slow feature parity relative to markets without residency restrictions. Enterprises that cannot justify the expense of private cloud defer modernization, preserving a pool of on-premises systems that drags overall growth.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI and Analytics into ERP Suites

- Adoption of Modular Two-Tier ERP for Subsidiaries

- Shortage of ERP Implementation Talent in ASEAN

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Two-tier architectures captured 13.08% growth and represent the fastest-expanding segment within the ASEAN enterprise resource planning market. These architectures enable headquarters instances of SAP or Oracle to synchronize nightly with subsidiary platforms such as NetSuite or Business Central. This synchronization eliminates manual currency translation errors, streamlines financial reporting, and reduces consolidation cycles from weeks to just a few days. Cloud-native suites accounted for 41.12% of the installed base in 2025, while mobile-first platforms cater to logistics and field-service operators who require seamless smartphone access for their operations.

Localized compliance requirements significantly drive the adoption of this architecture. The presence of separate e-tax portals, payroll statutes, and invoice formats across five key ASEAN markets makes it economically unfeasible to customize a single global instance. Instead, subsidiaries can implement localized platforms and go live within 3 months, with support from regional partners well-versed in domestic regulations. Meanwhile, headquarters retains centralized control over group reporting and financial oversight. Consequently, two-tier adoption has become a cornerstone of hybrid rollouts, solidifying its role in the growth and evolution of the market.

Human-capital suites will expand at 13.28% through 2031, eclipsing finance as enterprises seek accurate payroll, leave, and benefits processing across 11 statutory landscapes. The finance and accounting segment accounts for 35.16% of spend, but growth moderates as many firms have already automated core ledgers. Fragmented social-security rules expose firms to penalties when calculations go awry, turning payroll accuracy into a board-level risk. Unified cloud payroll covering Indonesia, Malaysia, Thailand, Singapore, the Philippines, and Vietnam reduces manual filing errors by over one-third. In turn, policy-driven complexities in overtime and severance accelerate demand for modern HCM suites in the ASEAN enterprise resource planning market.

The market is divided into finance, human resources, supply chain management, manufacturing, procurement, and customer relationship management (CRM). Finance modules continue to serve as the foundation of ERP implementations, as they play a critical role in financial reporting, budgeting, taxation, and regulatory compliance. However, supply chain and procurement functions are seeing increased adoption as businesses in the region expand cross-border trade and seek enhanced visibility into supplier networks, inventory management, and logistics. At the same time, CRM modules are gaining traction as companies prioritize customer engagement, sales forecasting, and service management.

List of Companies Covered in this Report:

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Unit4 N.V.

- IFS AB

- Infor Inc.

- Sage Group Plc

- Workday Inc.

- SYSPRO (Pty) Ltd.

- Acumatica Inc.

- Ramco Systems Ltd.

- HashMicro Pte. Ltd.

- Epicor Software Corporation

- QAD Inc.

- Deskera Holdings Ltd.

- SunFish DataOn Philippins Inc.

- Zoho Corporation Pvt. Ltd.

- ECOUNT Co., Ltd.

- Highnix Pte. Ltd.

- HashMicro Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration Acceleration among ASEAN SMEs

- 4.2.2 Rising Government Digital Economy Initiatives

- 4.2.3 Integration of AI and Analytics into ERP Suites

- 4.2.4 Adoption of Modular Two-Tier ERP for Subsidiaries

- 4.2.5 Growing Mobile Workforce Demanding Anytime Access

- 4.2.6 Surge in ESG Reporting Needs Driving ERP Upgrades

- 4.3 Market Restraints

- 4.3.1 Data Sovereignty and Localization Regulations

- 4.3.2 Shortage of ERP Implementation Talent in ASEAN

- 4.3.3 Legacy System Integration Complexities

- 4.3.4 High Total Cost of Ownership for SMEs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Architecture

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Others Industry Verticals

- 5.6 By Geography

- 5.6.1 Singapore

- 5.6.2 Thailand

- 5.6.3 Malaysia

- 5.6.4 Indonesia

- 5.6.5 Philippines

- 5.6.6 Rest of ASEAN

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 Unit4 N.V.

- 6.4.5 IFS AB

- 6.4.6 Infor Inc.

- 6.4.7 Sage Group Plc

- 6.4.8 Workday Inc.

- 6.4.9 SYSPRO (Pty) Ltd.

- 6.4.10 Acumatica Inc.

- 6.4.11 Ramco Systems Ltd.

- 6.4.12 HashMicro Pte. Ltd.

- 6.4.13 Epicor Software Corporation

- 6.4.14 QAD Inc.

- 6.4.15 Deskera Holdings Ltd.

- 6.4.16 SunFish DataOn Philippins Inc.

- 6.4.17 Zoho Corporation Pvt. Ltd.

- 6.4.18 ECOUNT Co., Ltd.

- 6.4.19 Highnix Pte. Ltd.

- 6.4.20 HashMicro Pte. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年 供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)

供應鏈ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)醫療設備和醫療技術企業資源規劃 (ERP):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031) 企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源規劃 (ERP) 市場報告:按組件、業務部門、部署類型、組織規模、產業和地區分類 (2026–2034)人工智慧整合ERP(企業資源計畫):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)