|

市場調查報告書

商品編碼

2044103

企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

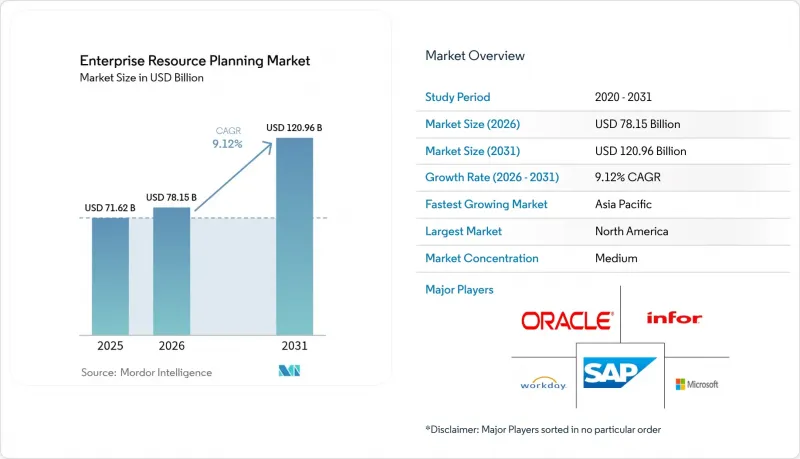

2025 年企業資源計畫 (ERP) 市場價值為 716.2 億美元,預計到 2031 年將達到 1,209.6 億美元,而 2026 年為 781.5 億美元,預測期(2026-2031 年)複合年成長率為 9.12%。

對整合流程自動化、加速雲端遷移和人工智慧驅動的分析的強勁需求正在推動製造業、服務業和公共部門組織的市場擴張。供應商正在調整藍圖,轉向可降低基礎設施成本的雲端原生套件,而企業則在加速現代化,以提高即時可見性和合規性。在強制性電子帳單和ESG會計要求的推動下,企業優先考慮嵌入式的合規功能,以降低審計風險並支援跨境業務營運。熟練顧問的短缺正在重塑競爭格局,促使供應商投資低程式碼配置工具,以縮短部署時間並降低整體擁有成本 (TCO)。

全球企業資源規劃 (ERP) 市場趨勢與洞察

雲端優先遷移的勢頭

在企業資源規劃 (ERP) 市場,各公司正加速從本地部署套件遷移到雲端部署,以實現彈性可擴展性、訂閱式定價和持續的功能更新。中型企業正在採用能夠確保成長資金的營運成本模式,而大型企業則利用「RISE with SAP」等供應商計畫來整合分散式系統環境。此外,超大規模託管選項使客戶能夠將敏感帳簿在地化,從而滿足資料主權合規性要求,同時又不犧牲統一報告功能。持續發布週期確保稅法和安全修補程式始終保持最新狀態,從而降低審計風險和升級期間的中斷。因此,與傳統的許可證續訂相比,遷移到雲端能夠更快地獲取新用戶。

將人工智慧驅動的分析功能整合到企業資源規劃系統中

人工智慧 (AI) 正在將企業資源計劃 (ERP) 市場從靜態記錄庫轉變為即時決策引擎。 Acumatica 在 2025 年高峰會上發布的「AI 優先」策略,整合了機器學習模型,用於預測付款延遲、最佳化生產批次並建議採購數量。 Oracle NetSuite 中類似的自然語言查詢功能,讓員工無需 SQL 專業知識即可建立多維報表。內部供應商基準測試表明,AI 驅動的需求預測可將安全庫存降低高達 30%,從而釋放資金用於投資。此外,低程式碼 AI 建構器支援廣泛的演算法客製化,使財務和營運團隊無需資料科學專家的協助即可建立用例原型。這些進步正在推動市場超越合規自動化,以實現收入成長。

高昂的初始成本和轉換成本

包括初始許可費、流程重組研討會和員工培訓在內,中型企業的ERP專案很容易超過100萬美元。根據Panorama Consulting的研究顯示,如果將資料遷移和變更管理服務也納入其中,總支出通常會翻倍,投資回收期超過三年。新興地區的預算限制加劇了企業對巨額資本投資的敏感度。雖然SaaS合約可以將成本分攤到一段時間內,但隱性整合工作和臨時並行營運成本仍然是沉重的負擔。因此,有些公司會推遲現代化改造,直到監管期限或客戶需求迫使其採取行動,阻礙短期市場成長。

細分市場分析

2025年,該解決方案在企業資源規劃 (ERP) 市場中保持了58.91%的主導地位。這反映了企業對財務、供應鏈和人力資本模組整合的普遍需求。然而,隨著客戶對特定產業諮詢、資料清洗和使用者實施支援的需求不斷成長,業務收益正以13.89%的複合年成長率成長。預計到2031年,專業服務市場規模將成長近一倍,超過傳統的客製化預算。 Acumatica等供應商已推出專業服務版本,將專案會計、資源調度和收入確認功能捆綁在一起,以簡化律師事務所、設計公司和諮詢公司的實施流程。對持續改善和人工智慧調優日益成長的需求正在抵消軟體毛利率的下降,並確保供應商擁有穩定的收入來源。

新的實施藍圖優先考慮業務流程重組而非功能標準化,從而提升了諮詢合作夥伴的策略角色。低程式碼工作流程建構器能夠快速建構特定產業變體的原型製作,減少編碼工作量,同時增加諮詢時間。客戶還購買了基於訂閱的成功計劃,其中包括季度健康檢查、法規合規性補丁和人工智慧模型重新訓練。這些變化使該服務從輔助收入來源轉變為核心收入來源,強化了當今市場特有的「產品+諮詢」混合價值提案。

預計到2025年,雲端架構將佔據55.73%的市場佔有率,憑藉其可預測的營運成本和自動化升級,將贏得大部分新用戶。然而,融合私有雲、公有雲和本地部署資產的混合雲配置正以16.12%的複合年成長率快速成長。跨國製造商通常將分析和協作工具託管在區域雲端中,同時將財務帳簿保存在本地資料中心,以確保符合公司本身的合規要求。因此,混合雲端解決方案的企業資源規劃(ERP)市場規模預計將超過純雲端解決方案的市場規模。

SAP 的 RISE 專案體現了這一趨勢,它允許在超大規模資料中心業者資料中心部署 S/4HANA,同時將製造執行系統保留在本地。製藥公司非常看重這種能夠共用集中式品質資料以進行全球批次放行,同時又能控制工廠現場延遲的能力。這種混合架構還支援分階段遷移,允許逐步淘汰舊版附加元件,避免一次性大規模遷移的風險。因此,市場格局正在朝著一種兼顧可控性、效能和可擴展性的共存模式發展。

區域分析

預計到2025年,北美將佔據全球市場收入的34.02%,這主要得益於幾個關鍵因素,包括高雲端採用率、強大的合作夥伴網路以及眾多財富500強企業的存在。該地區在SaaS解決方案的早期應用方面表現出色,並在成熟的創業投資系統的支持下,持續刺激對現代ERP套件的需求。這些套件正日益整合人工智慧(AI)和複雜分析等先進技術,以滿足不斷變化的業務需求。此外,政府採購政策強調數位化優先,這在加速公共部門機構採用ERP系統方面發揮著至關重要的作用,進一步鞏固了該地區的市場領導地位。

在歐洲,電子帳單的立法正在引發ERP系統的新一輪更新。為了因應這些監管變化,供應商提供的解決方案具備區域性稅務引擎、符合GDPR的資料居住功能以及根據本地需求量身定做的預配置會計表。這些功能使企業能夠從傳統的本地部署平台遷移到現代訂閱模式。因此,在合規性和營運效率需求的推動下,該地區正經歷5%左右的穩定成長。

亞太地區正以11.96%的複合年成長率(CAGR)成為市場成長最快的地區。這一成長主要得益於中國、印度和東南亞國家的快速工業擴張。政府主導的各項舉措,例如津貼和補貼,以及行動寬頻價格的下降和雲端基礎設施滲透率的提高,都顯著推動了雲端ERP的普及。中型製造和服務企業對雲端ERP的採用尤為顯著。此外,超大規模雲端服務供應商正在投資建置區域資料中心,這些資料中心不僅符合資料主權法規,還能縮短使用者回應時間。在亞太地區充滿活力的經濟環境和技術進步的推動下,這些發展正助力該地區的企業資源規劃(ERP)市場持續保持兩位數的強勁成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 雲端優先遷移的勢頭

- 將人工智慧驅動的分析功能整合到企業資源規劃系統中

- 中小企業對SaaS的採用率快速成長

- 強制電子帳單(增值稅、現金稅)

- 用於範圍 3 追蹤的 ESG 會計附加元件

- 擴大雲端ERP解決方案的採用

- 市場限制因素

- 高昂的初始設定成本和轉換成本

- 資料整合和舊有系統的複雜性

- 加強有關資料主權和資料居住的法律法規

- 微型垂直產業ERP人員短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 價格分析

- 生態系分析

第5章 市場規模與成長預測

- 報價

- 解決方案

- 服務

- 不同的發展

- 現場

- 雲

- 混合

- 按功能

- 人力資源

- 供應鏈

- 金融

- 行銷

- 其他功能

- 按公司規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 製造業

- 零售與電子商務

- BFSI

- 資訊科技和通訊

- 政府和公共部門

- 能源與公共產業

- 衛生保健

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Sage Group plc

- Epicor Software Corporation

- IFS AB

- Infor Inc.

- Unit4 NV

- Acumatica, Inc.

- Odoo SA

- QAD Inc.

- Plex Systems, Inc.

- Deltek, Inc.

- Priority Software Ltd.

- Ramco Systems

- Syspro

- TOTVS

- Yonyou

- HashMicro

第7章 市場機會與未來趨勢

- 評估未開發的領域和未滿足的需求

The Enterprise Resource Planning Market size was valued at USD 71.62 billion in 2025 and is estimated to grow from USD 78.15 billion in 2026 to reach USD 120.96 billion by 2031, at a CAGR of 9.12% during the forecast period (2026-2031).

Strong demand for integrated process automation, faster cloud migration, and AI-enabled analytics is propelling expansion across manufacturing, services, and public-sector organizations. Vendors have shifted road maps toward cloud-native suites that lower infrastructure costs, while enterprises accelerate modernization to improve real-time visibility and regulatory compliance. Spurred by mandatory e-invoicing laws and ESG accounting requirements, companies are prioritizing embedded compliance capabilities that reduce audit risk and support cross-border operations. Competitive dynamics are shaped by a shortfall of skilled consultants, prompting providers to invest in low-code configuration tools that shorten deployment timelines and lower total cost of ownership.

Global Enterprise Resource Planning Market Trends and Insights

Cloud-First Migration Momentum

Enterprises are accelerating the shift from on-premise suites to cloud deployments in the enterprise resource planning market to unlock elastic scalability, subscription pricing, and continuous functional updates. Mid-market firms embrace operating-expense models that free cash for growth, while large companies leverage vendor programs such as RISE with SAP to consolidate fragmented landscapes. In addition, hyperscale hosting options enable customers to localize sensitive ledgers for data sovereignty compliance without sacrificing unified reporting. Continuous release cycles keep tax codes and security patches up to date, reducing audit exposure and disruption during upgrades. As a result, cloud conversions help the market add new subscribers faster than traditional license refreshes.

AI-Driven Analytics Embedded in ERP

Artificial intelligence is recasting the enterprise resource planning market as a real-time decision engine rather than a static record repository. Acumatica's AI-first strategy, unveiled at its 2025 summit, embeds machine-learning models that predict late payments, optimize production runs, and recommend purchase quantities. Similar natural-language query features in Oracle NetSuite let staff build multi-dimensional reports without SQL expertise. Internal vendor benchmarks show that AI-assisted forecasting can reduce safety-stock buffers by up to 30%, freeing up cash for investment. Low-code AI builders are also democratizing algorithm customization, enabling finance and operations teams to prototype use cases without data science support. These advances expand the market beyond compliance automation, enabling revenue growth.

High Implementation and Switching Costs

Upfront license fees, process redesign workshops, and staff training can push ERP projects for a mid-size organization above USD 1 million. Panorama Consulting surveys reveal that total outlays often double when data migration and change-management services are factored in, extending payback periods beyond 3 years. Budget constraints in emerging regions amplify sensitivity to large capital commitments. Although SaaS contracts distribute expense over time, hidden integration work and temporary parallel-run costs remain significant. Consequently, some firms postpone modernization until regulatory deadlines or customer mandates force action, which caps short-term market growth.

Other drivers and restraints analyzed in the detailed report include:

- SME SaaS Adoption Surge

- Mandatory E-Invoicing Mandates

- Shortage of Micro-Vertical ERP Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions maintained a commanding 58.91% share of the enterprise resource planning market in 2025, reflecting the universal need for integrated financial, supply chain, and human capital modules. Yet service revenue is rising at a 13.89% CAGR as customers seek industry-specific consulting, data cleansing, and user adoption coaching. The market for professional services is on track to nearly double by 2031, surpassing traditional customization budgets. Vendors such as Acumatica introduced professional-services editions bundling project accounting, resource scheduling, and revenue recognition to streamline deployment for law, design, and consulting agencies. Growing demand for continuous improvement and AI tuning offsets narrowing software gross margins and secures annuity streams for providers.

Implementation roadmaps now prioritize business-process redesign over feature parity, elevating the strategic role of consulting partners. Low-code workflow builders enable rapid prototyping of industry-specific variants, reducing coding volume while increasing advisory hours. Customers also purchase subscription-based success plans that include quarterly health checks, regulatory patching, and AI model retraining. These shifts reposition services from ancillary to core revenue, reinforcing the hybrid product-plus-consulting value proposition that defines the contemporary market.

Cloud architectures accounted for 55.73% of the market in 2025, securing the majority of new installations thanks to predictable operating expenses and automatic upgrades. However, hybrid configurations that blend private, public, and on-premises assets are advancing at a 16.12% CAGR. Multinational manufacturers frequently retain financial ledgers in local data centers for sovereignty compliance while hosting analytics and collaboration tools in regional clouds. As a result, the enterprise resource planning market size for hybrid solutions is projected to outpace that of pure cloud segments.

SAP's RISE program exemplifies this trend by enabling customers to deploy S/4HANA on hyperscalers while keeping manufacturing execution systems on-site. Pharmaceutical firms value the ability to preserve plant-floor latency budgets while sharing centralized quality data for global batch release. Hybrid blueprints also support phased migrations, allowing legacy add-ons to retire gradually without the risk of a big bang. Consequently, the market's deployment landscape is evolving toward coexistence models that balance control, performance, and elasticity.

The Enterprise Resource Planning Market Report is Segmented by Offering (Solutions, and Services), Deployment (On-Premise, Cloud, Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Manufacturing, Retail and E-Commerce, BFSI, IT and Telecom, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 34.02% of the market revenue in 2025, driven by several key factors, including high cloud adoption rates, robust partner networks, and the presence of a significant number of Fortune 500 organizations. The region benefits from its early adoption of SaaS solutions, supported by a mature venture-capital ecosystem that continues to fuel demand for modern ERP suites. These suites are increasingly integrating advanced technologies like artificial intelligence (AI) and sophisticated analytics to meet evolving business needs. Additionally, digital-first government procurement policies are playing a crucial role in encouraging public-sector agencies to adopt ERP systems, further solidifying the region's leadership in the market.

Europe maintains steady market growth, with widespread adoption across key sectors such as manufacturing and public administration. However, the introduction of mandatory e-invoicing laws is triggering a new replacement cycle for ERP systems. To address these regulatory changes, vendors are offering solutions equipped with localized tax engines, GDPR-compliant data-residency features, and pre-configured charts of accounts tailored to regional requirements. These capabilities are enabling businesses to transition from outdated on-premise platforms to modern subscription-based models. As a result, the region is experiencing stable mid-single-digit growth, driven by the need for compliance and operational efficiency.

Asia-Pacific is emerging as the fastest-growing region in the market, with a CAGR of 11.96%. This growth is fueled by rapid industrial expansion in countries such as China, India, and those in Southeast Asia. Government initiatives, including grants and subsidies, combined with the increasing affordability of mobile broadband and the growing availability of cloud infrastructure, are significantly boosting cloud ERP deployments. These deployments are particularly prominent among mid-tier manufacturers and service-oriented firms. Furthermore, hyperscale cloud providers are investing in the development of regional data centers, which not only comply with data-sovereignty regulations but also enhance user response times. These advancements are ensuring that the enterprise resource planning market in Asia-Pacific continues to experience robust double-digit growth, driven by the region's dynamic economic landscape and technological advancements.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Sage Group plc

- Epicor Software Corporation

- IFS AB

- Infor Inc.

- Unit4 NV

- Acumatica, Inc.

- Odoo SA

- QAD Inc.

- Plex Systems, Inc.

- Deltek, Inc.

- Priority Software Ltd.

- Ramco Systems

- Syspro

- TOTVS

- Yonyou

- HashMicro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-First Migration Momentum

- 4.2.2 AI-Driven Analytics Embedded in ERP

- 4.2.3 SME SaaS Adoption Surge

- 4.2.4 Mandatory E-Invoicing Mandates (VAT, CTC)

- 4.2.5 ESG Accounting Add-Ons For Scope-3 Tracking

- 4.2.6 Increasing Adoption of Cloud-Based ERP Solutions

- 4.3 Market Restraints

- 4.3.1 High Implementation and Switching Costs

- 4.3.2 Data Integration and Legacy Complexity

- 4.3.3 Rising Data-Sovereignty / Residency Laws

- 4.3.4 Shortage Of Micro-Vertical ERP Talent

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Ecosystem Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Function

- 5.3.1 Human Resources

- 5.3.2 Supply Chain

- 5.3.3 Finance

- 5.3.4 Marketing

- 5.3.5 Other Functions

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-user Industry

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 IT and Telecom

- 5.5.5 Government and Public Sector

- 5.5.6 Energy and Utilities

- 5.5.7 Healthcare

- 5.5.8 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 Sage Group plc

- 6.4.6 Epicor Software Corporation

- 6.4.7 IFS AB

- 6.4.8 Infor Inc.

- 6.4.9 Unit4 NV

- 6.4.10 Acumatica, Inc.

- 6.4.11 Odoo SA

- 6.4.12 QAD Inc.

- 6.4.13 Plex Systems, Inc.

- 6.4.14 Deltek, Inc.

- 6.4.15 Priority Software Ltd.

- 6.4.16 Ramco Systems

- 6.4.17 Syspro

- 6.4.18 TOTVS

- 6.4.19 Yonyou

- 6.4.20 HashMicro

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年 企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測

企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測 2026年全球產品實施服務市場報告2026年全球開放原始碼企業資源規劃(ERP)市場報告

2026年全球產品實施服務市場報告2026年全球開放原始碼企業資源規劃(ERP)市場報告 物聯網資源最佳化解決方案市場預測至2034年-按解決方案類型、元件、部署模式、應用、最終用戶和地區分類的全球分析

物聯網資源最佳化解決方案市場預測至2034年-按解決方案類型、元件、部署模式、應用、最終用戶和地區分類的全球分析 電子商務ERP整合:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)2026年全球ERP和ECM整合市場報告2026年企業資源規劃(ERP)區塊鏈全球市場報告亞太地區企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

電子商務ERP整合:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)2026年全球ERP和ECM整合市場報告2026年企業資源規劃(ERP)區塊鏈全球市場報告亞太地區企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2030年全球企業資源規劃系統整合與諮詢市場

2026-2030年全球企業資源規劃系統整合與諮詢市場