|

市場調查報告書

商品編碼

2063344

中東第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031)Middle East Third-Party Logistics (3PL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

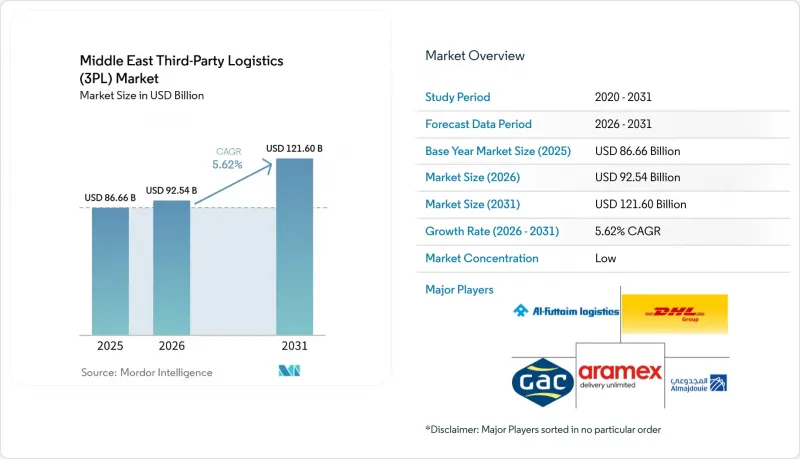

根據 Mordor Intelligence 預測,中東第三方物流(3PL) 市場規模將從 2025 年的 866.6 億美元成長到 2026 年的 925.4 億美元,到 2031 年將達到 1216 億美元,2026 年至 2031 年的複合成長率 5.62%。

石油需求放緩、製造業多元化成長以及電子商務的穩定發展支撐著這一成長趨勢,而客戶如今更重視監管合規、ESG報告和即時可視性,而非單純的貨運成本。本報告按服務(國內運輸管理、國際運輸管理及其他)、終端用戶行業(汽車、能源與公共產業、生命科學與醫療保健及其他)、物流模式(輕資產及其他)以及國家/地區(阿拉伯聯合大公國、沙烏地阿拉伯、土耳其、阿曼及其他)進行細分。市場預測以美元計價。

中東第三方物流(3PL) 市場趨勢與洞察

土耳其與海灣合作理事會之間的跨境電子商務協議將加速小包裹的流通。

雙邊便利化協議已將土耳其的海關清關時間從最長72小時縮短至2024年的12-18小時,將推動土耳其電子商務出口激增42億美元。更快的清關速度改變了空運貨物的成本結構,並實現了自動化分揀,使第三方物流公司能夠投資於土耳其自由區機場附近的保稅設施。預清關拼箱服務已將物流成本降低了高達30%,促使沿岸地區的線上零售商將土耳其視為繼中國之後的第二大採購中心。杜拜和阿布達比作為中轉樞紐,提高了該地區「最後一公里」配送網路的小包裹密度。因此,擁有跨國海關API的供應商比那些僅限於國內運輸車輛的資產密集型競爭對手更具優勢。

GreenSkuk 的資金籌措旨在支持太陽能發電和 ESG 認證倉庫的發展。

2024年,伊斯蘭綠色金融產品為物流資產籌集了25億美元,降低了致力於實現可衡量碳排放目標的開發商的資金籌措成本。沙烏地阿拉伯公共投資基金(PIF)30億美元的融資框架中,一部分資金被分配給了符合LEED認證標準的物流中心,以支持「2030願景」。每個設施都必須報告能源強度和可再生能源佔比,並將第三方審計納入日常營運。擁有內部永續發展團隊的大型第三方物流公司具有優勢,而小規模營運商則難以承擔檢驗成本。在阿拉伯聯合大公國,一個規劃中的50萬平方公尺太陽能發電園區展示了公私合營如何重新定義客戶如今期望的最低ESG標準。

海灣合作理事會沿線貨櫃設施長期失衡,推高了搬遷成本。

由於繞過紅海航線導致進口貨櫃供應減少,進口商運輸空貨櫃的成本目前高達每標準箱400至600美元。航運公司將部分負擔轉嫁給與其簽訂固定價格合約的第三方物流公司,這擠壓了它們的利潤空間。海灣國家出口量遠小於進口量,因此這種不平衡狀況持續存在。同時,對於日常消費品(FMCG)托運人而言,其他散貨運輸方案並不現實。擁有重新定位聯盟和貨櫃共用平台的供應商可以降低成本,但在船隊區域配置恢復正常之前,許多中型營運商將面臨盈利下降的困境。

細分市場分析

隨著客戶日益重視監管合規、序列化追蹤和ESG認證,增值倉儲和物流服務預計到2031年將以6.98%的複合年成長率成長。這項轉變促使競爭對手將關注點從每個托盤成本指標轉向應對力和技術整合。儘管國際運輸管理面臨貨櫃設施不平衡和地緣政治不穩定等挑戰,但具備多模態協調能力的供應商可以透過最佳化即時運輸能力和成本來脫穎而出。預計到2025年,國內運輸管理將佔中東物流(3PL)市場佔有率的49.34%,受益於電子商務的成長和快速交易需求,但司機短缺和燃油成本波動正對固定價格合約的利潤率構成壓力。

在醫藥物流領域,將GS1序列化整合到增值物流(VAWD)營運中,既提高了庫存可視性和存貨周轉,也確保了合規性。中東合作委員會(GCC)的港口作為轉運樞紐,支持海上運輸的協調,但由於貨櫃短缺和即期運費波動加劇,其運輸能力受到限制。對於時效性要求高的藥品和航太貨物而言至關重要的空運服務,也因區域機場運力不足而面臨瓶頸。 GCC市場的陸路運輸受益於公路基礎設施的改善和跨境物流的便利化,但由於強制性的司機本地化和許可製度,成本有所增加。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 土耳其與海灣合作理事會的跨境電子商務協議加快了小包裹的流通。

- GreenSkuk提供的資金籌措正在促進配備太陽能和ESG認證的倉庫的發展。

- 阿曼的氫氣出口大型企劃(NEOM)正在創造對低溫散裝氣體物流的需求。

- 沙烏地阿拉伯藥品供應鏈中強制性的 GS1 序列化正在促使符合規定的第三方物流合約數量增加。

- 將超履約配送外包給第三方物流微型配送中心,這些中心按暗店類型的即時雜貨新創公司進行分類。

- 阿拉伯聯合大公國的航太和衛星組裝叢集正在推動專案貨物第三方物流服務的成長。

- 市場限制因素

- 海灣合作理事會沿線貨櫃設施長期失衡,推高了搬遷成本。

- 海灣合作理事會增值稅框架協調工作的延遲,使保稅跨境運輸變得複雜。

- 由於疫苗和生物製藥貿易不斷擴大,導致醫藥級冷藏貨櫃船短缺。

- 勒索軟體和網路入侵風險的增加導致第三方物流保費上漲和停機時間延長。

- 價值供應鏈分析

- 科技展望(物聯網、人工智慧、機器人、氫燃料卡車)

- 監管情勢與政府應對措施

- 對電子商務業務的洞察

- 波特五力模型

- 地緣政治事件對市場的影響

第5章 市場規模與成長預測

- 按服務

- 國內運輸管理

- 路

- 航空

- 其他

- 國際運輸管理

- 路

- 航空

- 海上運輸

- 多模態/跨模態

- 加值倉儲與物流 (VAWD)

- 國內運輸管理

- 按最終用戶行業分類

- 車

- 能源與公共產業

- 製造業

- 生命科學與醫療保健

- 技術與電子

- 電子商務

- 消費品/快速消費品

- 飲食

- 其他

- 物流模型

- 輕資產(託管)

- 資產密集型(公司車輛和倉庫)

- 混合

- 國家

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 卡達

- 巴林

- 科威特

- 阿曼

- 其他中東國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Al-Futtaim Logistics

- Almajdouie Logistics

- APL Logistics Ltd.

- Aramex

- BDP International

- 達飛集團(包括CEVA物流)

- Crane Worldwide Logistics

- DHL Group

- DSV A/S

- Emirates Logistics

- Gulf Agency Company(GAC)

- GWC(Gulf Warehousing Company)

- Kanoo Logistics

- Nippon Express Holdings

- NYK航運公司(含郵船物流)

- RAK Logistics

- Saudi Post

- TLM International Freight Services LLC

- Total Freight International

- Tristar Transport LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east third-Party logistics market size is expected to increase from USD 86.66 billion in 2025 to USD 92.54 billion in 2026 and reach USD 121.60 billion by 2031, growing at a CAGR of 5.62% over 2026-2031.

Softer oil demand, diversified manufacturing growth, and steady e-commerce adoption underpin the trajectory, while clients now rank regulatory compliance, ESG reporting, and real-time visibility ahead of pure freight-rate considerations. This report is Segmented by Service (Domestic Transportation Management, International Transportation Management, and More), by End-User Industry (Automotive, Energy and Utilities, Life Sciences and Healthcare, and More), by Logistics Model (Asset-Light, and More), and by Country (United Arab Emirates, Saudi Arabia, Turkey, Oman, and More). The Market Forecasts are Provided in Terms of Value (USD).

Middle East Third-Party Logistics (3PL) Market Trends and Insights

Turkey-GCC Cross-Border E-commerce Accords Accelerating Small-Parcel Flows

Bilateral facilitation agreements slashed customs clearance from as high as 72 hours to 12-18 hours in 2024, which triggered a surge in Turkish e-commerce exports valued at USD 4.2 billion. Faster clearance reshaped the cost curve for air freight and automated sortation, letting 3PLs invest in bonded facilities near Turkish free-zone airports. Consolidated pre-cleared shipments now trim logistics costs by up to 30%, redirecting Gulf online retailers toward Turkey as a China-plus-one sourcing base. Dubai and Abu Dhabi serve as transshipment nodes, amplifying parcel densities that feed regional last-mile networks. Providers owning multi-country brokerage APIs are therefore winning contracts ahead of asset-heavy rivals limited to domestic fleets.

Green Sukuk Financing Spurring Roll-out of Solar-Powered, ESG-Certified Warehouses

Islamic green instruments mobilized USD 2.5 billion for logistics assets in 2024, cutting financing costs for developers that commit to measurable carbon metrics. The Public Investment Fund's USD 3 billion tranche earmarked a portion for LEED-rated distribution centers that underpin Vision 2030. Each facility must report energy intensity and renewable-power share, which embeds third-party audits into everyday operations. Larger 3PLs with in-house sustainability teams gain an edge, while smaller operators struggle with verification fees. In the UAE, a planned 500,000 sqm solar-powered park showcases how public-private initiatives reset the minimum ESG standard clients now expect.

Persistent Container-Equipment Imbalance Inflating Repositioning Costs on GCC Lanes

Empty-equipment transfers now cost importers USD 400-600 per TEU as Red Sea detours reduce inbound container pools. Carriers pass part of the burden to 3PLs locked in fixed-price contracts, eroding margins. Gulf import dominance versus lower export flows sustains the deficit, while alternative break-bulk solutions are unviable for FMCG shippers. Providers with repositioning alliances or container-sharing platforms can contain costs, but most mid-tier players face profitability headwinds until fleet geography normalizes.

Other drivers and restraints analyzed in the detailed report include:

- Hydrogen Export Mega-Projects Generating Demand for Cryogenic Bulk-Gas Logistics

- Mandatory GS1 Serialization in Saudi Pharma Supply Chains

- Slow GCC VAT-Framework Harmonization Complicating Bonded Cross-Border Movements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Value-added warehousing and distribution is set to grow at a 6.98% CAGR through 2031 as clients prioritize regulatory compliance, serialization tracking, and ESG certification. This shift has moved competition from cost-per-pallet metrics to audit-readiness and technology integration. International transportation management faces challenges like container equipment imbalances and geopolitical uncertainties, but providers with multimodal coordination capabilities can differentiate by optimizing real-time capacity and costs. Domestic transportation management, projected to hold a 49.34% of the Middle East third-party logistics market share in 2025, benefits from e-commerce growth and quick commerce demands, though driver shortages and fuel cost volatility are squeezing margins on fixed-price contracts.

In pharmaceutical logistics, GS1 serialization integration within VAWD operations ensures compliance while improving inventory visibility and stock rotation. GCC ports, positioned as transshipment hubs, support sea freight coordination, but container shortages limit capacity and increase spot-rate volatility. Air freight services, crucial for time-sensitive pharmaceutical and aerospace cargo, face bottlenecks due to regional airport capacity constraints. Road transportation in GCC markets benefits from better highway infrastructure and cross-border facilitation but struggles with rising costs from driver nationalization mandates and licensing restrictions.

List of Companies Covered in this Report:

- Al-Futtaim Logistics

- Almajdouie Logistics

- APL Logistics Ltd.

- Aramex

- BDP International

- CMA CGM Group (Including CEVA Logistics)

- Crane Worldwide Logistics

- DHL Group

- DSV A/S

- Emirates Logistics

- Gulf Agency Company (GAC)

- GWC (Gulf Warehousing Company)

- Kanoo Logistics

- Nippon Express Holdings

- NYK Line (Including Yusen Logistics)

- RAK Logistics

- Saudi Post

- TLM International Freight Services LLC

- Total Freight International

- Tristar Transport LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Turkey-GCC Cross-Border E-Commerce Accords Accelerating Small-Parcel Flows

- 4.2.2 Green Sukuk Financing Spurring Roll-Out of Solar-Powered, ESG-Certified Warehouses

- 4.2.3 Hydrogen Export Mega-Projects (NEOM, Oman) Generating Demand for Cryogenic Bulk-Gas Logistics

- 4.2.4 Mandatory GS1 Serialization in Saudi Pharma Supply Chain Expanding Compliance-Ready 3PL Contracts

- 4.2.5 Dark-Store Instant-Grocery Start-Ups Outsourcing Hyper-Local Fulfilment to 3PL Micro-Hubs

- 4.2.6 UAE Aerospace and Satellite-Assembly Clusters Driving Growth in Project-Cargo 3PL Services

- 4.3 Market Restraints

- 4.3.1 Persistent Container-Equipment Imbalance Inflating Repositioning Costs on GCC Lanes

- 4.3.2 Slow GCC VAT-Framework Harmonization Complicating Bonded Cross-Border Movements

- 4.3.3 Shortfall of Pharmaceutical-Grade Reefer Assets amid Rising Vaccine and Biologics Trade

- 4.3.4 Escalating Ransomware and Cyber-Intrusion Risks Increasing 3PL Insurance Premiums and Downtime

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technology Outlook (IoT, AI, Robotics, Hydrogen Trucks)

- 4.6 Regulatory Landscape and Government Initiatives

- 4.7 Insights into E-commerce Business

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service

- 5.1.1 Domestic Transportation Management

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Others

- 5.1.2 International Transportation Management

- 5.1.2.1 Road

- 5.1.2.2 Air

- 5.1.2.3 Sea

- 5.1.2.4 Multimodal / Intermodal

- 5.1.3 Value-Added Warehousing and Distribution (VAWD)

- 5.1.1 Domestic Transportation Management

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Energy and Utilities

- 5.2.3 Manufacturing

- 5.2.4 Life Sciences and Healthcare

- 5.2.5 Technology and Electronics

- 5.2.6 E-commerce

- 5.2.7 Consumer Goods and FMCG

- 5.2.8 Food and Beverages

- 5.2.9 Others

- 5.3 By Logistics Model

- 5.3.1 Asset-Light (Management-Based)

- 5.3.2 Asset-Heavy (Own Fleet and Warehouses)

- 5.3.3 Hybrid

- 5.4 By Country

- 5.4.1 United Arab Emirates

- 5.4.2 Saudi Arabia

- 5.4.3 Turkey

- 5.4.4 Egypt

- 5.4.5 Qatar

- 5.4.6 Bahrain

- 5.4.7 Kuwait

- 5.4.8 Oman

- 5.4.9 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Al-Futtaim Logistics

- 6.4.2 Almajdouie Logistics

- 6.4.3 APL Logistics Ltd.

- 6.4.4 Aramex

- 6.4.5 BDP International

- 6.4.6 CMA CGM Group (Including CEVA Logistics)

- 6.4.7 Crane Worldwide Logistics

- 6.4.8 DHL Group

- 6.4.9 DSV A/S

- 6.4.10 Emirates Logistics

- 6.4.11 Gulf Agency Company (GAC)

- 6.4.12 GWC (Gulf Warehousing Company)

- 6.4.13 Kanoo Logistics

- 6.4.14 Nippon Express Holdings

- 6.4.15 NYK Line (Including Yusen Logistics)

- 6.4.16 RAK Logistics

- 6.4.17 Saudi Post

- 6.4.18 TLM International Freight Services LLC

- 6.4.19 Total Freight International

- 6.4.20 Tristar Transport LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球履約服務市場報告2026年生物製藥冷藏物流鏈全球市場報告

2026年全球履約服務市場報告2026年生物製藥冷藏物流鏈全球市場報告 亞太地區第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031)

亞太地區第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031) 第三方化學品分銷市場:依產品類型、實體形態、服務及最終用途產業分類-2026-2032年全球市場預測第三方物流(3PL) 軟體市場:2026-2032 年全球市場預測(按應用、部署類型、服務類型、組織規模和最終用戶產業分類)

第三方化學品分銷市場:依產品類型、實體形態、服務及最終用途產業分類-2026-2032年全球市場預測第三方物流(3PL) 軟體市場:2026-2032 年全球市場預測(按應用、部署類型、服務類型、組織規模和最終用戶產業分類) 第三方化學品分銷市場:按類型、應用和地區分類(2026-2034 年)第三方物流市場:依產品/服務、服務模式、定價模式、運輸方式、應用領域及最終用戶產業分類-2026-2032年全球市場預測2026年全球第三方物流(3PL)市場報告

第三方化學品分銷市場:按類型、應用和地區分類(2026-2034 年)第三方物流市場:依產品/服務、服務模式、定價模式、運輸方式、應用領域及最終用戶產業分類-2026-2032年全球市場預測2026年全球第三方物流(3PL)市場報告 2026-2030年全球汽車第三者物流市場

2026-2030年全球汽車第三者物流市場 第三方物流軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類

第三方物流軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類