|

市場調查報告書

商品編碼

2072899

印度第三方物流倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India 3PL Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

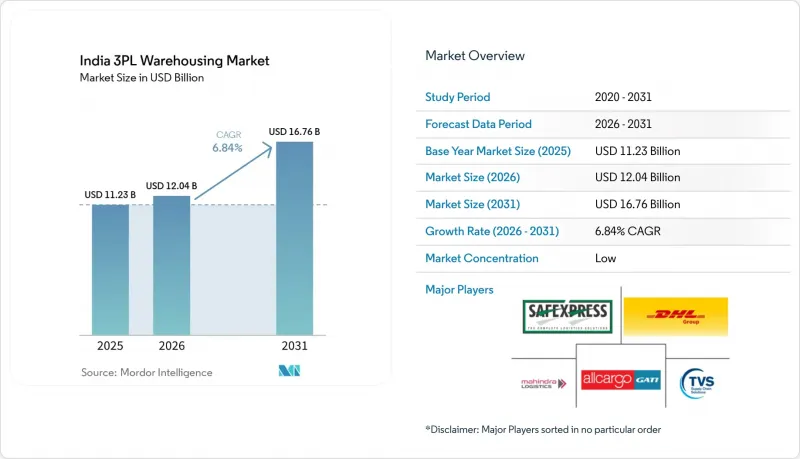

根據 Mordor Intelligence 預測,印度第三方物流倉儲市場預計將從 2025 年的 112.3 億美元成長到 2026 年的 120.4 億美元,到 2031 年達到 167.6 億美元,2026 年至 2031 年的複合年成長率為 6.84%。

受外包業務成長、電子商務發展、製造業擴張以及供應鏈向規範化轉型等因素的推動,印度第三方物流倉儲市場表現良好。本報告按服務類型(倉儲、配送和庫存管理等)、倉庫類型(普通共用/多客戶倉庫、保稅倉庫等)、溫度控制方式(非溫控、溫控)、技術應用(人工、半自動化等)、終端用戶行業(製造業、消費品等)以及地區(北部、中部等)進行細分。市場預測以美元計價。

印度第三方物流倉儲市場趨勢與洞察

電子商務履約的快速成長

在印度的第三方物流倉儲市場,從單純的倉儲空間預訂到以履約主導的需求轉變正變得日益明顯。在主要城市,速度和庫存可用性已成為至關重要的因素,這促使電商企業不斷擴展其暗店和補貨網路。 Flipkart Minutes 計劃在 2025 年底將其暗店數量從 500 多家增加到 2026 年 4 月的 1000 家,凸顯了都市區補貨網路的快速擴張。截至 2025 年 10 月,印度已有 2525 家暗店運作,預計到 2030 年將達到 7,500 家。這將持續推動對城市母中心、區域倉儲點以及能夠快速揀貨的設施的需求。這一趨勢迫使第三方物流業者重新思考其傳統的中心輻射式模式,以適應高密度城市佈局、較小的佔地面積和更快的存貨周轉。

促進基礎設施發展

印度第三方物流倉儲市場也受惠於交通基礎設施的改善,這縮短了運輸時間,並促進了規模更大、效率更高的倉儲網路的建設。到2025年3月,東西部專用貨運走廊的運作將達到96.4%,總長2,741公里,將德里和孟買之間的運輸時間縮短近40%,並將貨車週轉時間從15-16天縮短至2-3天。此外,到2025年10月,印度鐵路將在18個邦運作118個Gati Shakti多式聯運貨運站,擴大鐵路一體化倉儲的需求範圍。 PM GatiShakti入口網站向私人用戶開放也改善了選址規劃,使營運商能夠透過通用資料層評估走廊通行情況、公用設施連接和土地適宜性。走廊可視性的提高和運輸波動性的降低,正在提升整個印度第三方物流倉儲市場大規模多客戶和工廠互聯設施的可行性。

土地徵用及分區瓶頸

土地徵用仍是阻礙因素,尤其是在需求正向城市郊區和工業走廊附近轉移的地區。印度倉儲協會在2025年7月指出,建立一個倉庫仍需獲得近60項來自邦政府和中央政府的許可。這減緩了發展速度,並增加了實施風險。城市規劃法規是另一個障礙,因為許多城市限制在住宅使用倉庫和冷庫設施。同時,許多邦規定了更寬的道路和最小用地面積,這在人口稠密的地區難以實現。這些挑戰對於需要位置消費者而非遠離城市中心的快速貿易和小規模規模企業來說尤其突出。此外,這種情況有利於資金雄厚的企業,因為它們可以處理授權手續、購買位置更好的土地,並有更長的時間來完成專案。

細分市場分析

預計到2025年,倉儲服務將佔印度第三方物流(3PL)倉儲市場佔有率的59.07%,這意味著基礎倉儲空間提供和物流外包仍將佔據當前需求的最大佔有率。配送和庫存管理仍是第二大服務領域,因為電子商務、消費品和零售客戶越來越需要在單一營運網路內存貨周轉、訂單處理和退貨支援。附加價值服務是成長最快的細分領域,預計到2031年將以9.67%的複合年成長率成長,凸顯了印度3PL倉儲產業正從單純的倉儲轉變為一體化履約。這種轉變最為明顯,因為客戶希望在倉庫內而非內部管理套件組裝、貼標、二次包裝和單據支援。隨著客戶要求減少交接環節並在單一營運平台上提高透明度,服務組成也在改變。

增值服務的成長也反映了印度第三方物流倉儲市場品質標準的不斷提高。食品和製藥行業的客戶需要更嚴格的記錄保存、批次管理、更嚴格的先進先出(FIFO)或新鮮度優先(FEFO)流程以及更強的流程合規性,這提升了專業外包的效用。由於客戶更傾向於資料整合和更順暢的運營,投資於更完善的倉庫管理系統和追溯工具的營運商在贏得這些合約方面更具優勢。因此,尤其是在處理多種品類的共用設施中,所提供的服務範圍(而不僅僅是占地面積)正成為更明顯的差異化因素。

到2025年,共用/多客戶倉儲將佔印度第三方物流倉儲市場的55%,反映出托運人對靈活且資產密集型倉儲模式的持續偏好。這種模式適用於季節性需求、新興的D2C品牌以及不希望簽訂長期租賃協議或承諾專屬倉儲能力的中型製造商。專屬合約倉儲對於需要毗鄰工廠的設施、客製化佈局和有保障的處理能力的關鍵客戶仍然至關重要。保稅倉儲是成長最快的模式,到2031年複合年成長率將達到8.85%。這主要是由於出口導向製造業和跨國採購對關稅延期支付和與海關合作進行更嚴格監管的倉儲需求不斷成長。因此,保稅倉儲的戰略重要性遠超其目前的規模。

此細分市場的優勢源自於印度第三方物流倉儲市場獨特的需求邏輯。電子產品、半導體和工業供應鏈,尤其是與生產獎勵(PLI) 相關的供應鏈,需要進行生產前零件接收管理,從而推動了對港口和工業走廊附近保稅設施的需求。 TVS供應鏈解決方案公司於2026年3月在清奈附近開設了一座佔地4萬平方英尺的自由貿易區 (FTWZ) 設施,以支持Caterpillar公司從印度開展的全球供應鏈,這凸顯了保稅倉儲在工業物流中日益成長的重要性。日本通運公司也於2026年1月宣佈在多雷拉建造一個半導體物流中心,並概述了為半導體材料開發專用保稅倉庫的計畫。這些發展表明,保稅基礎設施正在成為支撐出口相關成長的長期基礎,而不僅僅是一項小眾的海關服務。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務履約的快速成長

- 促進基礎設施發展(Gati Shakti,Bharatmala)

- 透過商品及服務稅 (GST) 進行網路整合

- 大型零售公司對甲級物業的需求

- 微型倉庫在暗店與快速交易中的興起

- PLI(工廠可能檢查)系統旨在促進工廠附近物流樞紐的形成。

- 市場限制因素

- 與土地徵用和分區相關的瓶頸

- 脆弱的首末公里多模態協作

- 低溫運輸合規體系的碎片化

- 高昂的電價給自動化投資報酬率帶來了壓力。

- 法律規範

- 價值鍊和通路分析

- 技術創新前景

- 波特五力模型

- 低溫運輸倉庫需求的演變

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模及成長預測(價值,2026-2031 年)

- 按服務類型

- 貯存

- 經銷和庫存管理

- 附加價值服務及其他服務(套件組裝、貼標籤)

- 倉庫類型

- 通用共用/多客戶端倉庫

- 專用合約倉庫

- 保稅倉庫

- 透過溫度控制

- 非溫控型

- 溫控型

- 透過技術實施

- 手動的

- 半自動

- 全自動

- 按最終用戶行業分類

- 製造業

- 消費品

- 食品/飲料

- 零售與電子商務

- 醫療保健和製藥

- 其他

- 按地區

- 北方

- 中部

- 西方

- 東方

- 南

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- DHL Supply Chain

- Mahindra Logistics Ltd.

- TVS Supply Chain Solutions

- Allcargo Supply Chain Pvt. Ltd.(Gati-Allcargo ecosystem)

- Safexpress Pvt. Ltd.

- Delhivery Ltd.

- Blue Dart Express Ltd.

- Transport Corporation of India(TCI Supply Chain Solutions)

- CJ Darcl Logistics Ltd.

- DP World Logistics India

- Yusen Logistics India Pvt. Ltd.

- FedEx Supply Chain India

- Kuehne+Nagel India

- DSV(incl. Schenker integration)

- Nippon Express India

- Prozo Integrated Supply Chain Solutions

- Shiprocket Fulfillment

- Xpressbees Logistics

- Shadowfax Technologies

- Om Logistics Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the india 3PL warehousing market size is expected to increase from USD 11.23 billion in 2025 to USD 12.04 billion in 2026 and reach USD 16.76 billion by 2031, growing at a CAGR of 6.84% over 2026-2031.

India's 3PL warehousing market is performing well, driven by rising outsourcing, e-commerce growth, manufacturing expansion, and the shift toward organized supply chains. This report is Segmented by Service Type (Storage, Distribution and More), by Warehouse Type (General Shared, Bonded, and More), by Temperature Control (Non-Temperature, Temperature), by Technology Adoption (Manual, Semi-Automated, and More), by End User Industry (Manufacturing, Consumer Goods, and More), and by Region (North, Central, and More). The Market Forecasts are Provided in Terms of Value (USD).

India 3PL Warehousing Market Trends and Insights

Rapid Growth of E-Commerce Fulfillment

The India 3PL warehousing market is seeing a sharper shift toward fulfillment-led demand rather than simple capacity booking. E-commerce operators are expanding dark-store and replenishment networks because speed now matters as much as inventory depth in major cities. Flipkart Minutes targeted 1,000 dark stores by April 2026, up from more than 500 in late 2025, underscoring how quickly urban replenishment networks are scaling. India had 2,525 operational dark stores as of October 2025, and this base is projected to reach 7,500 by 2030, keeping demand high for intra-city mother hubs, local storage points, and rapid-picking formats. This pattern is forcing 3PL operators to redesign legacy hub-and-spoke models around denser urban layouts, smaller footprints, and faster inventory turns.

Infrastructure Push

The India 3PL warehousing market is also benefiting from transport upgrades that reduce movement time and support larger, more efficient warehouse networks. The Eastern and Western dedicated freight corridors were 96.4% operational by March 2025, covering 2,741 route km and cutting Delhi-Mumbai freight transit time by close to 40%, while wagon turnaround dropped from 15-16 days to 2-3 days. Indian Railways had also commissioned 118 Gati Shakti Multimodal Cargo Terminals across 18 states by October 2025, which widened the map for rail-linked warehousing demand. The opening of the PM GatiShakti portal to private users also improves site planning by enabling operators to assess corridor access, utility links, and land suitability through a common data layer. Better corridor visibility and lower transit variability are making bigger multi-client and factory-linked locations more viable across the India 3PL warehousing market.

Land Acquisition and Zoning Bottlenecks

Land access remains a direct growth constraint for the India 3PL warehousing market, especially where demand is shifting closer to city limits and industrial corridors. The Warehousing Association of India stated in July 2025 that setting up a warehouse still needed close to 60 state and central permissions, which slows development and raises execution risk. Urban zoning rules add another layer because several cities restrict warehouse and cold-storage use in residential zones. At the same time, many states require wider access roads and minimum plot sizes that are hard to secure in dense neighborhoods. These frictions are particularly difficult for quick-commerce and small-format operators because they need sites close to consumers rather than far from the urban core. They also favor well-capitalized operators that can manage approvals, buy better land parcels, and wait longer for project completion.

Other drivers and restraints analyzed in the detailed report include:

- PLI Schemes Triggering Near-Factory Logistics Hubs

- Rise of Dark Stores and Quick-Commerce Micro-Warehousing

- Fragmented Cold-Chain Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Storage accounted for 59.07% of the India 3PL warehousing market share in 2025, indicating that basic space-and-handle outsourcing still accounts for the largest share of current demand. Distribution and inventory management remained the second-largest service line because e-commerce, consumer goods, and retail clients increasingly need stock rotation, order handling, and returns support within a single operating network. Value-added services are the fastest-growing sub-segment, with a 9.67% CAGR through 2031, confirming that the India 3PL warehousing industry is moving beyond static storage toward integrated fulfillment. This shift is strongest where clients want kitting, labeling, secondary packaging, and documentation support within the warehouse, rather than managing those steps internally. The service mix is changing because clients want fewer handoffs and greater visibility across a single operating platform.

The growth of value-added work also reflects a higher quality threshold in the India 3PL warehousing market. Food and pharma customers need tighter record keeping, batch control, FIFO or FEFO discipline, and stronger process compliance, which makes specialist outsourcing more useful. Operators that invest in better warehouse management systems and traceability tools are better positioned to capture these contracts, as clients prefer connected data and cleaner execution. The result is that service depth is becoming a clearer differentiator than floor space alone, especially in shared facilities serving multiple categories.

General shared/multi-client warehousing held 55% of the India 3PL warehousing market share in 2025, reflecting the continued preference for flexible, asset-light warehousing among shippers. This format works well for seasonal demand, early-stage D2C brands, and mid-sized manufacturers that do not want to commit to long leases or dedicated capacity. Dedicated contract warehousing remains important for anchor clients that need plant-adjacent facilities, custom layouts, and protected throughput. Bonded warehousing is the fastest-growing format, with a 8.85% CAGR through 2031, because export-oriented manufacturing and multi-country sourcing require duty-deferred storage and tighter customs-linked controls. That makes bonded space more strategic than its current scale might suggest.

The strength of this segment comes from a different demand logic inside the India 3PL warehousing market. PLI-linked electronics, semiconductor, and industrial supply chains need inbound component management before production starts, and that supports bonded facilities near ports and industrial corridors. TVS Supply Chain Solutions opened a 40,000 ft2 FTWZ facility near Chennai in March 2026 to support Caterpillar's global supply chains from India, underscoring the growing prominence of bonded warehousing in industrial logistics. Nippon Express also discussed a semiconductor logistics hub in Dholera in January 2026, with plans for specialized bonded warehousing for semiconductor materials. These moves suggest that bonded infrastructure is becoming a long-term enabler of export-linked growth rather than a niche customs service.

Complete Report Scope:

- By Service Type

- Storage

- Distribution and Inventory Management

- Value-Added Services and Others (Kitting, Labelling)

- By Warehouse Type

- General Shared / Multi-client Warehousing

- Dedicated Contract Warehousing

- Bonded Warehousing

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Technology Adoption

- Manual

- Semi-automated

- Fully Automated

- By End User Industry

- Manufacturing

- Consumer Goods

- Food and Beverage

- Retail and E-commerce

- Healthcare and Pharma

- Other End-user Industries

- By Region

- North

- Central

- West

- East

- South

List of Companies Covered in this Report:

- DHL Supply Chain

- Mahindra Logistics Ltd.

- TVS Supply Chain Solutions

- Allcargo Supply Chain Pvt. Ltd. (Gati-Allcargo ecosystem)

- Safexpress Pvt. Ltd.

- Delhivery Ltd.

- Blue Dart Express Ltd.

- Transport Corporation of India (TCI Supply Chain Solutions)

- CJ Darcl Logistics Ltd.

- DP World Logistics India

- Yusen Logistics India Pvt. Ltd.

- FedEx Supply Chain India

- Kuehne+Nagel India

- DSV (incl. Schenker integration)

- Nippon Express India

- Prozo Integrated Supply Chain Solutions

- Shiprocket Fulfillment

- Xpressbees Logistics

- Shadowfax Technologies

- Om Logistics Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth of E-Commerce Fulfilment

- 4.2.2 Infrastructure Push (Gati Shakti, Bharatmala)

- 4.2.3 GST-Driven Network Consolidation

- 4.2.4 Organized Retail's Demand for Grade-A Space

- 4.2.5 Rise of Dark Stores and Quick-Commerce Micro-Warehousing

- 4.2.6 PLI Schemes Triggering Near-Factory Logistics Hubs

- 4.3 Market Restraints

- 4.3.1 Land Acquisition and Zoning Bottlenecks

- 4.3.2 Weak First/Last-Mile Multimodal Links

- 4.3.3 Fragmented Cold-Chain Compliance

- 4.3.4 High Power Tariffs Denting Automation ROI

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Evolution of Cold-Chain Warehousing Requirements

- 4.9 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution and Inventory Management

- 5.1.3 Value-Added Services and Others (Kitting, Labelling)

- 5.2 By Warehouse Type

- 5.2.1 General Shared / Multi-client Warehousing

- 5.2.2 Dedicated Contract Warehousing

- 5.2.3 Bonded Warehousing

- 5.3 By Temperature Control

- 5.3.1 Non-Temperature Controlled

- 5.3.2 Temperature Controlled

- 5.4 By Technology Adoption

- 5.4.1 Manual

- 5.4.2 Semi-automated

- 5.4.3 Fully Automated

- 5.5 By End User Industry

- 5.5.1 Manufacturing

- 5.5.2 Consumer Goods

- 5.5.3 Food and Beverage

- 5.5.4 Retail and E-commerce

- 5.5.5 Healthcare and Pharma

- 5.5.6 Other End-user Industries

- 5.6 By Region

- 5.6.1 North

- 5.6.2 Central

- 5.6.3 West

- 5.6.4 East

- 5.6.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Supply Chain

- 6.4.2 Mahindra Logistics Ltd.

- 6.4.3 TVS Supply Chain Solutions

- 6.4.4 Allcargo Supply Chain Pvt. Ltd. (Gati-Allcargo ecosystem)

- 6.4.5 Safexpress Pvt. Ltd.

- 6.4.6 Delhivery Ltd.

- 6.4.7 Blue Dart Express Ltd.

- 6.4.8 Transport Corporation of India (TCI Supply Chain Solutions)

- 6.4.9 CJ Darcl Logistics Ltd.

- 6.4.10 DP World Logistics India

- 6.4.11 Yusen Logistics India Pvt. Ltd.

- 6.4.12 FedEx Supply Chain India

- 6.4.13 Kuehne+Nagel India

- 6.4.14 DSV (incl. Schenker integration)

- 6.4.15 Nippon Express India

- 6.4.16 Prozo Integrated Supply Chain Solutions

- 6.4.17 Shiprocket Fulfillment

- 6.4.18 Xpressbees Logistics

- 6.4.19 Shadowfax Technologies

- 6.4.20 Om Logistics Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

美國第三方物流倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國第三方物流倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中東第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031)

美國第三方物流倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國第三方物流倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中東第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031) 2026年全球履約服務市場報告2026年生物製藥冷藏物流鏈全球市場報告亞太地區第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031)

2026年全球履約服務市場報告2026年生物製藥冷藏物流鏈全球市場報告亞太地區第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031) 第三方化學品分銷市場:依產品類型、實體形態、服務及最終用途產業分類-2026-2032年全球市場預測第三方物流(3PL) 軟體市場:2026-2032 年全球市場預測(按應用、部署類型、服務類型、組織規模和最終用戶產業分類)

第三方化學品分銷市場:依產品類型、實體形態、服務及最終用途產業分類-2026-2032年全球市場預測第三方物流(3PL) 軟體市場:2026-2032 年全球市場預測(按應用、部署類型、服務類型、組織規模和最終用戶產業分類) 第三方化學品分銷市場:按類型、應用和地區分類(2026-2034 年)第三方物流市場:依產品/服務、服務模式、定價模式、運輸方式、應用領域及最終用戶產業分類-2026-2032年全球市場預測

第三方化學品分銷市場:按類型、應用和地區分類(2026-2034 年)第三方物流市場:依產品/服務、服務模式、定價模式、運輸方式、應用領域及最終用戶產業分類-2026-2032年全球市場預測