|

市場調查報告書

商品編碼

2072691

德國第三方物流倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Germany 3PL Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

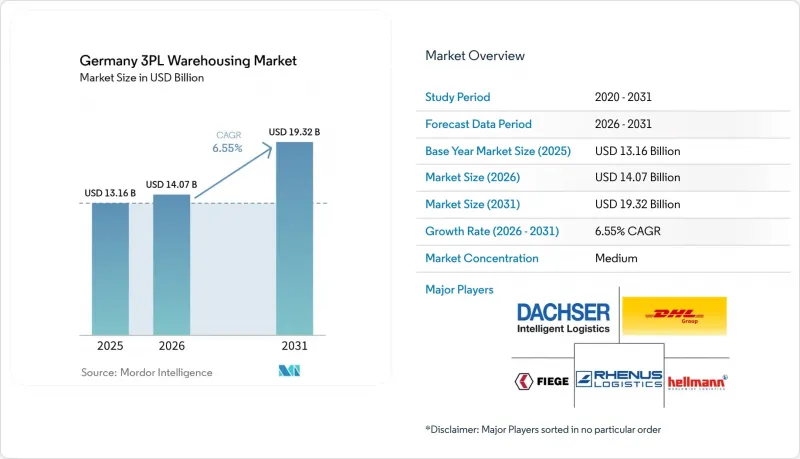

據 Mordor Intelligence 稱,2025 年德國第三方物流倉儲市場價值為 131.6 億美元,預計到 2031 年將達到 193.2 億美元,而 2026 年為 140.7 億美元,2026 年至 2031 年的複合年成長率為 6.55%。

德國第三方物流倉儲市場持續受惠於該國作為歐洲製造業和運輸樞紐的地位。德國與九個國家接壤,位於物流三角區的核心地帶,該三角區涵蓋法蘭克福、漢堡和萊茵-魯爾區。該地區的倉儲供應依然緊張,優質地段的租金在歐洲名列前茅。本報告按服務類型(倉儲、配送及庫存管理、其他)、倉庫類型(普通共用/多客戶倉庫、保稅倉庫、其他)、溫控類型(非溫控倉庫、其他)、技術類型(手動、半自動、全自動)以及最終用戶(製造業、消費品行業、其他行業)進行細分。市場預測以美元計價。

德國第三方物流倉儲市場趨勢與洞察

電子商務中當日達/隔日達的壓力

在德國的第三方物流倉儲市場,隨著線上零售需求從基礎倉儲轉向高度依賴配送速度和退貨處理,履約壓力日益增大。 2024年,德國線上零售市場銷售額達806億歐元(約870億美元),服務了6,800萬線上消費者。每位消費者的年均消費額達2,200歐元(約2,376美元)。在服裝、家電和美妝產品等類別中,隔日達正逐漸成為標準服務;而在人口密集的都市區,當日達也從一項高階服務轉變為一項競爭優勢。由於德國時尚類商品的退貨率仍然很高,退貨處理的重要性與配送速度不相上下。簡言之,逆向物流處理能力不再是可有可無的附加功能,而是倉儲的核心功能。這種情況促使營運商在主要人口密集區附近尋找合適的位置,即使租金高昂且新地稀缺。隨著都市區待開發區(新開發用地)選擇範圍縮小,維修大規模棕地(現有設施)和建立郊區正成為那些仍需擴大規模並滿足快速收款期限的企業更現實的選擇。

醫藥和生物製藥行業的低溫運輸繁榮

德國第三方物流倉儲市場正因醫藥物流的蓬勃發展而顯著成長,因為生物製藥、生物相似藥和特藥對儲存和管理的要求比傳統產品更為嚴格。 2025年5月,DHL集團啟用了位於弗洛爾施塔特4號的3萬平方公尺多溫區倉庫。該倉庫的啟用使弗洛爾施塔特醫療物流園區的總面積擴展至10萬平方公尺,托盤吞吐量超過14萬個。對溫度敏感的產品數量不斷增加,正在改變採購模式,因為符合GDP和GMP規範如今在合約授予和續約中扮演直接角色。此外,生物製藥行業的客戶希望最大限度地降低儲存、搬運和運輸過程中的風險,這提升了可數位化審計、多溫區且經過認證的設施的價值。 Vetter Pharma在拉文斯堡投資1.5億歐元(約1.635億美元)的擴建工程新增了16,000個托盤式儲存空間,目標是在2028年達到68,000個托盤式儲存空間。這也反映出市場對外包剩餘庫存、緩衝儲存以及製造商自有設施周邊支援能力的需求日益成長。因此,低溫運輸倉儲不再是德國第三方物流倉儲市場的小眾領域,而是快速成長的產業,對網路規劃的影響也越來越大。

樞紐城市高品質工業用地短缺且成本高昂

德國第三方物流倉儲市場面臨結構性土地短缺問題。這是因為物流走廊內最擁擠的區域也是需求最旺盛的區域。預計到2025年,慕尼黑主要物流中心的租金將達到每平方公尺每月11歐元(12美元),法蘭克福為8.7歐元(9.5美元),斯圖加特為8.5歐元(9.3美元),證實了主要樞紐的供應仍然緊張。德國和歐盟層面日益嚴格的土地使用政策使得解決長期空間短缺問題變得越來越困難。重新開發棕地是一種解決方案,但污染風險、所有權分散和漫長的維修週期等問題正在拖慢專案進度。對於無法主動取得土地或投資更複雜設施配置的中型業者而言,這個問題尤其嚴重。從長遠來看,土地短缺預計將繼續有利於德國第三方物流倉儲市場中那些擁有雄厚財力和與開發商建立更深厚關係的大型供應商。

細分市場分析

到2025年,倉儲服務將佔德國第三方物流(3PL)倉儲市場佔有率的48.11%,反映出汽車、零售和消費品供應鏈對庫存緩衝的持續需求。物流和庫存管理將繼續發揮關鍵作用,將倉儲能力與揀貨包裝作業、運輸規劃以及全國範圍內的庫存可視性聯繫起來。預計到2031年,附加價值服務和其他服務將以9.38%的複合年成長率成長,顯著高於整體市場成長率,顯示合約範圍已不再局限於提供倉儲空間。該領域在德國第三方物流倉儲市場的成長源自於客戶尋求最終階段的客製化服務,而無需自行承擔設施、人事費用和系統成本。與幾年前相比,套件組裝、貼標、退貨處理和聯合包裝如今已成為倉儲營運的核心環節。

這項轉變是由兩方面因素共同推動的。電子商務訂單需要逐件處理、客製化包裝和更快捷的退貨流程,而醫療保健產品則需要更嚴格的文件記錄和嚴密控制的處理程序。此外,德國的包裝和產品責任法規也提升了合規標籤和包裝服務的價值,尤其對於那些尋求單一外包流程的客戶而言。與標準倉儲作業相比,經過認證的流程密集作業更難替代,這使得可靠的供應商能夠獲得更高的利潤率。因此,德國第三方物流倉儲產業正轉向對人事費用、系統整合和合規性要求更高的合約模式。在消費性電子和醫療保健領域擁有良好業績記錄的供應商,將更有利於開拓這一高階市場。

預計到2025年,典型的共享和多客戶倉庫將佔德國第三方物流(3PL)倉儲市場規模的54.83%,凸顯了托運人仍然優先考慮資本效率和全國覆蓋範圍。多客戶倉庫仍然具有吸引力,因為它們允許3PL供應商將固定成本分攤到多個客戶以及波動的季節性需求模式上。這種模式在電子商務和日常消費品(FMCG)行業尤其有效,因為這些行業的尖峰需求波動很大,在需求高峰期柔軟性至關重要。 FIEGE公司位於哈明克恩(Hamminkern)的5.5萬平方公尺項目和位於黑森州利希特瑙(Hessisch Lichtenau)的5.2萬平方公尺項目(均計劃於2026年秋季投入運營)表明,多用戶倉儲能力在特定地點持續擴張。對許多租戶而言,共用倉庫仍然是進入德國3PL倉儲市場最現實的方式。

由於部分客戶難以適應共用環境,專用合約倉庫仍是成長最快的倉庫類型,預計到2031年複合年成長率將達到8.55%。處理藥品、汽車、定序和危險物品的使用者需要比一般多客戶倉庫更嚴格的流程控制、污染隔離或安全措施。這些要求提升了專用倉庫和長期合約的價值。此外,由於更嚴格的驗證、工程設計和客戶核准,准入門檻也更高。儘管保稅倉庫的規模仍然較小,但隨著海關文件和要求的日益嚴格,它們在歐盟以外貨物流入德國港口系統中的重要性日益凸顯。因此,德國第三方物流倉庫市場呈現兩極化,共用空間主導了業務量的成長,而專用空間主導了合規主導成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務領域對當日達/隔日達服務的壓力

- 醫藥和生物製藥行業的低溫運輸繁榮

- 汽車一級供應商的近岸外包

- 在人手不足的背景下,如何提高自動化投資報酬率

- 碳中和倉庫標準的快速推廣

- 按需空間數位市場平台

- 市場限制因素

- 樞紐城市優質工業用地的稀缺性與高成本

- 溫控設施電費上升

- 嚴格的GDP/GMP審核會延遲藥品倉庫的運作啟動。

- 中小規模第三方物流供應商基礎設施的碎片化正在減緩新技術的採用。

- 法律規範

- 價值鍊和通路分析

- 技術創新前景

- 波特五力分析

- 低溫運輸倉庫需求的演變

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模與成長預測

- 按服務類型

- 貯存

- 經銷和庫存管理

- 附加價值服務及其他服務(套件組裝、貼標籤)

- 倉庫類型

- 通用共用/多客戶端倉庫

- 專用合約倉庫

- 保稅倉庫

- 透過溫度控制

- 無溫度控制

- 具備溫度控制功能

- 透過技術實施

- 手動的

- 半自動

- 全自動

- 按最終用戶行業分類

- 製造業

- 消費品

- 食品/飲料

- 零售與電子商務

- 醫療保健和製藥

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- DACHSER

- Rhenus Logistics

- FIEGE Logistics

- Hellmann Worldwide Logistics

- Kuehne+Nagel

- DSV A/S(Including DB Schenker)

- GEODIS

- CMA CGM Group(Including CEVA Logistics)

- BLG Logistics

- Nagel-Group

- Arvato Supply Chain Solutions

- LGI Logistics Group International

- Nippon Express

- NYK Line(Including Yusen Logistics)

- AP Moller-Maersk

- FedEx

- ID Logistics

- Rudolph Logistics Group

- Honold Logistik Gruppe

- Imperial Logistics

- Schnellecke Logistics

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany 3PL warehousing market size was valued at USD 13.16 billion in 2025 and is projected to grow from USD 14.07 billion in 2026 to reach USD 19.32 billion by 2031, growing at a CAGR of 6.55% during 2026-2031.

The Germany 3PL warehousing market continues to benefit from the country's role as Europe's manufacturing and transit backbone, with borders to 9 countries and a central position across the Frankfurt, Hamburg, and Rhine-Ruhr logistics triangle, where supply remains tight and prime logistics space commands some of the continent's highest rents. This report is Segmented by Service Type (Storage, Distribution and Inventory Management, and Others), by Warehouse Type (General Shared/Multi-client, Bonded, and More), by Temperature Control (Non-Temperature Controlled, and More), by Technology (Manual, Semi-Automated, Fully Automated), and by End User (Manufacturing, Consumer Goods, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany 3PL Warehousing Market Trends and Insights

E-Commerce Same-/Next-Day Fulfillment Pressure

The Germany 3PL warehousing market is seeing stronger fulfillment pressure because online retail demand now depends as much on delivery speed and returns handling as on basic storage. Germany's online retail market generated EUR 80.6 billion (USD 87.0 billion) in 2024 and served 68 million online shoppers, with average annual spend reaching EUR 2,200 (USD 2,376) per shopper. Next-day delivery has become the normal service expectation in categories such as apparel, electronics, and beauty, and same-day service is moving from a premium option to a competitive differentiator in dense urban areas. Returns matter just as much as outbound speed because Germany continues to record very high fashion return rates, which means reverse logistics capacity is now a core warehouse function rather than an optional add-on. This is pushing operators toward sites near major population centers even when rents are high and new land is scarce. As urban greenfield options tighten, large brownfield retrofits and edge-of-city nodes are becoming a more practical route for operators that still need scale and fast cut-off windows.

Pharmaceutical Biologics Cold-Chain Boom

The Germany 3PL warehousing market is getting a strong lift from pharmaceutical logistics because biologics, biosimilars, and specialty therapies need stricter storage control than conventional products. DHL Group opened Florstadt 4 in May 2025 as a 30,000 sqm multi-temperature warehouse, which expanded the Florstadt health logistics campus to 100,000 sqm and more than 140,000 pallet positions. The rise of temperature-sensitive products is changing procurement behavior because GDP and GMP compliance now play a direct role in contract awards and renewals. This shift is also raising the value of digitally auditable, multi-temperature, and certified facilities, since biopharma clients want fewer weak points across storage, handling, and release processes. Vetter Pharma's EUR 150 million (USD 163.5 million) expansion in Ravensburg, which adds 16,000 pallet positions and targets 68,000 positions by 2028, also points to rising demand for outsourced overflow, buffer storage, and support capacity around manufacturer-owned sites. The result is that cold-chain warehousing is no longer a niche within the Germany 3PL warehousing market, but a faster-growing layer that increasingly shapes network planning.

Scarcity and Cost of Prime Industrial Land in Hub Cities

The Germany 3PL warehousing market faces a structural land problem because the tightest logistics corridors are also the ones where demand is strongest. Prime logistics rents in 2025 reached EUR 11.0 per sqm per month (USD 12.0) in Munich, EUR 8.7 (USD 9.5) in Frankfurt, and EUR 8.5 (USD 9.3) in Stuttgart, which confirms that core hubs remain supply-constrained. The long-run space gap is becoming more difficult to close because land-use policy is tightening at both German and EU levels. Brownfield redevelopment offers one route forward, but it brings contamination risk, fragmented ownership, and longer remediation periods, which slow project delivery. This issue is most severe for mid-sized operators that cannot pre-emptively acquire land or finance more complex formats. Over time, land scarcity is likely to keep the Germany 3PL warehousing market tilted toward larger providers with stronger balance sheets and deeper developer relationships.

Other drivers and restraints analyzed in the detailed report include:

- Near-Shoring of Automotive Tier-1 Suppliers

- Automation ROI Rise Amid Labor Shortages

- Rising Electricity Prices for Temperature-Controlled Sites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Storage services held 48.11% of the Germany 3PL warehousing market share in 2025, which reflects the continued need for inventory buffering across automotive, retail, and consumer goods supply chains. Distribution and inventory management remain essential because they connect warehouse capacity with pick-pack execution, transport planning, and stock visibility across national networks. Value-added services and others are projected to expand at a 9.38% CAGR through 2031, well above the overall rate and indicating that contract scope is moving beyond basic space provision. This part of the Germany 3PL warehousing market is growing because clients want late-stage customization without taking on their own site, labor, and systems costs. Kitting, labeling, returns processing, and co-packing now sit closer to the center of warehouse economics than they did a few years ago.

That shift is being driven by two pressures at once. E-commerce orders need more unit-level handling, tailored packaging, and faster returns workflows, while healthcare products need tighter documentation and more controlled handling procedures. Germany's packaging and producer responsibility rules also make compliant labeling and preparation services more valuable for customers that want a single outsourced workflow. This is where reputable operators can build better margins, since certified and process-heavy work is harder to replace than standard storage. The Germany 3PL warehousing industry is therefore moving toward contracts where labor content, systems integration, and compliance execution all matter more. Operators with proven capability in consumer electronics and healthcare are better placed to capture this premium layer of demand.

General shared and multi-client warehousing accounted for 54.83% of the German 3PL warehousing market size in 2025, underscoring how strongly shippers still value capital efficiency and national reach. Multi-client buildings remain attractive because they allow 3PL providers to spread fixed costs across multiple customers and varying seasonal demand patterns. This model is especially useful in e-commerce and FMCG, where peak patterns move quickly and overflow flexibility matters. FIEGE's 55,000 sqm Hamminkeln project and 52,000 sqm Hessisch Lichtenau project, both targeted for autumn 2026, show that multi-user capacity is still being added in carefully selected nodes. For many occupiers, shared warehousing remains the most practical route into the Germany 3PL warehousing market.

Dedicated contract warehousing remains the fastest-growing warehouse type, with a 8.55% CAGR through 2031, as some customers cannot operate in shared environments. Pharmaceutical, automotive, sequencing, and hazardous-goods users need stronger process control, contamination separation, or security arrangements than a general multi-client site can provide. That requirement increases the value of purpose-built facilities and longer contract terms. It also raises entry barriers because validation, engineering design, and customer approval become more demanding. Bonded warehousing remains smaller, but it is becoming more relevant for non-EU flows entering Germany's port system as customs documentation and clearance requirements tighten. This leaves the Germany 3PL warehousing market with a dual structure where shared space leads on volume and dedicated space leads on compliance-driven growth.

Complete Report Scope:

- By Service Type

- Storage

- Distribution and Inventory Management

- Value-Added Services and Others (Kitting, Labelling)

- By Warehouse Type

- General Shared / Multi-client Warehousing

- Dedicated Contract Warehousing

- Bonded Warehousing

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Technology Adoption

- Manual

- Semi-automated

- Fully Automated

- By End User Industry

- Manufacturing

- Consumer Goods

- Food and Beverage

- Retail and E-commerce

- Healthcare and Pharma

- Other End-user Industries

List of Companies Covered in this Report:

- DHL Group

- DACHSER

- Rhenus Logistics

- FIEGE Logistics

- Hellmann Worldwide Logistics

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- GEODIS

- CMA CGM Group (Including CEVA Logistics)

- BLG Logistics

- Nagel-Group

- Arvato Supply Chain Solutions

- LGI Logistics Group International

- Nippon Express

- NYK Line (Including Yusen Logistics)

- A.P. Moller - Maersk

- FedEx

- ID Logistics

- Rudolph Logistics Group

- Honold Logistik Gruppe

- Imperial Logistics

- Schnellecke Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Same-/Next-Day Fulfilment Pressure

- 4.2.2 Pharmaceutical Biologics Cold-Chain Boom

- 4.2.3 Near-Shoring of Automotive Tier-1 Suppliers

- 4.2.4 Automation ROI Rise Amid Labor Shortages

- 4.2.5 Rapid Adoption of Carbon-Neutral Warehouse Standards

- 4.2.6 Digital Marketplace Platforms for On-Demand Space

- 4.3 Market Restraints

- 4.3.1 Scarcity and Cost of Prime Industrial Land in Hub Cities

- 4.3.2 Rising Electricity Prices for Temperature-Controlled Sites

- 4.3.3 Strict GDP / GMP Audits Delaying Pharma Warehouse Onboarding

- 4.3.4 Fragmented SME 3PL Base Slowing Uniform Tech Adoption

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Evolution of Cold-Chain Warehousing Requirements

- 4.9 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution and Inventory Management

- 5.1.3 Value-Added Services and Others (Kitting, Labelling)

- 5.2 By Warehouse Type

- 5.2.1 General Shared / Multi-client Warehousing

- 5.2.2 Dedicated Contract Warehousing

- 5.2.3 Bonded Warehousing

- 5.3 By Temperature Control

- 5.3.1 Non-Temperature Controlled

- 5.3.2 Temperature Controlled

- 5.4 By Technology Adoption

- 5.4.1 Manual

- 5.4.2 Semi-automated

- 5.4.3 Fully Automated

- 5.5 By End User Industry

- 5.5.1 Manufacturing

- 5.5.2 Consumer Goods

- 5.5.3 Food and Beverage

- 5.5.4 Retail and E-commerce

- 5.5.5 Healthcare and Pharma

- 5.5.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 DACHSER

- 6.4.3 Rhenus Logistics

- 6.4.4 FIEGE Logistics

- 6.4.5 Hellmann Worldwide Logistics

- 6.4.6 Kuehne+Nagel

- 6.4.7 DSV A/S (Including DB Schenker)

- 6.4.8 GEODIS

- 6.4.9 CMA CGM Group (Including CEVA Logistics)

- 6.4.10 BLG Logistics

- 6.4.11 Nagel-Group

- 6.4.12 Arvato Supply Chain Solutions

- 6.4.13 LGI Logistics Group International

- 6.4.14 Nippon Express

- 6.4.15 NYK Line (Including Yusen Logistics)

- 6.4.16 A.P. Moller - Maersk

- 6.4.17 FedEx

- 6.4.18 ID Logistics

- 6.4.19 Rudolph Logistics Group

- 6.4.20 Honold Logistik Gruppe

- 6.4.21 Imperial Logistics

- 6.4.22 Schnellecke Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

印度第三方物流倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)美國第三方物流倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中東第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031)

印度第三方物流倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)美國第三方物流倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中東第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031) 2026年全球履約服務市場報告2026年生物製藥冷藏物流鏈全球市場報告亞太地區第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031)

2026年全球履約服務市場報告2026年生物製藥冷藏物流鏈全球市場報告亞太地區第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031) 第三方化學品分銷市場:依產品類型、實體形態、服務及最終用途產業分類-2026-2032年全球市場預測第三方物流(3PL) 軟體市場:2026-2032 年全球市場預測(按應用、部署類型、服務類型、組織規模和最終用戶產業分類)

第三方化學品分銷市場:依產品類型、實體形態、服務及最終用途產業分類-2026-2032年全球市場預測第三方物流(3PL) 軟體市場:2026-2032 年全球市場預測(按應用、部署類型、服務類型、組織規模和最終用戶產業分類) 第三方化學品分銷市場:按類型、應用和地區分類(2026-2034 年)第三方物流市場:依產品/服務、服務模式、定價模式、運輸方式、應用領域及最終用戶產業分類-2026-2032年全球市場預測

第三方化學品分銷市場:按類型、應用和地區分類(2026-2034 年)第三方物流市場:依產品/服務、服務模式、定價模式、運輸方式、應用領域及最終用戶產業分類-2026-2032年全球市場預測