|

市場調查報告書

商品編碼

2063343

亞太地區第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031)Asia-Pacific Third-Party Logistics (3PL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

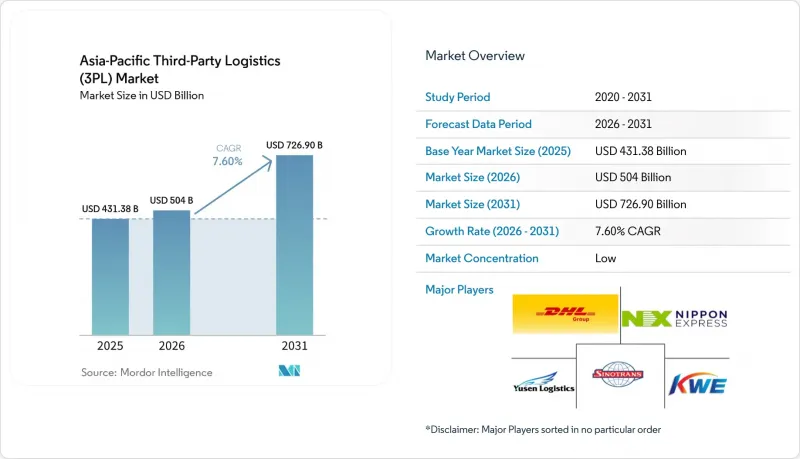

根據 Mordor Intelligence 預測,亞太地區第三方物流(3PL) 市場規模將從 2025 年的 4,313.8 億美元和 2026 年的 5,040 億美元成長到 2031 年的 7,269 億美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按服務(國內運輸管理、國際運輸管理、增值倉儲和配送)、終端用戶行業(汽車、能源和公共產業、製造業及其他)、物流模式(輕資產、重資產、混合模式)以及地區(中國、印度、日本及其他)進行分類。市場預測以美元計價。

亞太地區第三方物流(3PL) 市場趨勢與洞察

電子商務的快速發展正在推動當日達和最後一公里配送。

隨著線上訂單密度的增加,第三方物流 (3PL) 業務正從大規模出貨轉向依賴自動化樞紐的高頻次履約。物流報告稱,到 2025 年底,將在約 20 個城市運營超過 20 個朗祖科技自動化倉庫,這表明隨著貨運量的成長,大型托運人正依靠先進的設施來支援配送速度和訂單準確性。在亞太第三方物流市場,這些資產正被用於吸收傳統網路無法應對的季節性需求激增。自動化分類系統和「貨到人」系統縮短了小包裹的周轉時間,改善了客戶體驗,並擴大了對準時性要求極高的可服務商品的市場。亞太地區第三方物流市場也受到平台主導投資的影響,這些投資正在提高主要城市樞紐的履約標準。將自動化與高密度末端配送路線結合的供應商,即使在價格透明度不斷提高的情況下,也更有能力維持利潤率。

區域貿易協定的實施

RCEP持續減少其覆蓋15個經濟區的貿易網路中的摩擦,鼓勵托運人整合跨境物流,減少合作夥伴數量。截至2024年第三季度,中國與RCEP成員國之間的貨物貿易額年增,達9.63兆元。此外,自2021年下半年以來,中老鐵路已運輸跨境貨物1,158萬噸,為第三方物流(3PL)企業提供跨國多模態解決方案奠定了基礎。亞太地區第三方物流市場已開始圍繞這些走廊發展公路、鐵路和航空一體化運輸服務。透過「東協單一窗口」等措施實現單證流程標準化,減少了參與成員國的行政時間,並支持端到端的物流可視性和更可靠的運輸規劃。隨著關稅和程序的日益統一,亞太地區第三方物流市場對跨境公路和鐵路運輸替代方案的需求正在不斷成長。隨著海關清關時間表的逐步取消和原產地證書被整合到數位化工作流程中,擁有海關程序專業知識的供應商以及在原產地和目的地都擁有合規團隊的供應商正在獲得優勢。

新興市場基礎建設差距

與經合組織(OECD)基準相比,多個經濟區的交通網路仍然高度依賴公路,發展落後。這限制了路線的柔軟性,並增加了內陸地區長途運輸的服務成本。亞洲交通觀察站的數據顯示,該地區的基礎設施密度和公路鐵路轉換率落後於已開發國家標準,限制了交通中斷期間的運輸方式轉換選項。在泰國,農產品運輸仍嚴重依賴公路,鐵路使用率極低。這導致成本高於全球平均水平,擠壓了散裝和日常消費品(FMCG)托運人的利潤空間。雖然亞太地區的第三方物流(3PL)市場可以透過利用現有的鐵路和沿海支線服務來繞過瓶頸,但在交通走廊密集的地區仍然面臨尖峰時段堵塞。氣候風險進一步加劇了該地區公路和鐵路資產的風險,該地區降雨量不穩定,颱風頻繁,導致營運商的運作和恢復成本增加。在亞太地區的第三方物流市場,策略可能會出現兩極分化,一邊是正在進行計劃改進的主要走廊,另一邊是繼續依賴公路的次要路線,這將影響可達到的服務水準。

細分市場分析

到2025年,國內運輸管理將佔46.12%,這反映了區域內貿易的規模以及人口稠密的城市地區對卡車運輸在「最後一公里」運輸方面的依賴。這一佔有率凸顯了路線競標和動態運輸能力經紀在亞太第三方物流市場的核心地位,因為該市場正在實現短途和區域路線貨物類型的多元化。加值倉儲和物流服務將成為成長最快的服務,到2031年複合年成長率將達到7.84%,因為托運人將庫存轉移到更靠近消費地的位置,並擴大藥品和高階食品的冷藏倉儲規模。亞太地區第三方物流市場正在整合更靠近客戶的倉儲和微型倉配,並結合溫控處理,以提高處理能力並維持產品品質。與常溫儲存相比,提供適當環境管理和檢驗流程的供應商可以保持更高的利潤率。一些一體化營運商透過將供應商輔助裝載 (VAWD) 設施與合約物流相結合,並實施管理式補貨和供應商管理庫存 (VMI),來穩定存貨周轉並改善營運資金。此外,在亞太地區第三方物流市場,自動化儲存和檢索系統、高層貨架和機器人輔助揀貨等技術正被用於在不擴大設施面積的情況下管理多 SKU 的複雜性。

隨著成本和可靠性週期的變化,國際運輸管理正朝著以海運、空運和鐵路主導的多式聯運模式發展。紅海海域的中斷迫使承運人和托運人延長運輸路線,導致運輸週期延長,對時效性要求高的貨物附加費增加。為此,第三方物流公司(3PL)重新評估了空運配額,並為敏感產品配備了溫控緩衝設施。在某些運輸路線上,鐵路運輸與公路和空運的銜接日益緊密,以滿足海運在動盪條件下無法實現的交貨時限,從而強化了特定路線的第三方物流公司在協調多模態計劃方面的作用。 CEVA強調了工程化運輸和海關數位化在縮短跨境路線的停留時間和加快產品上市速度方面的重要作用,這在海運計劃恢復正常的同時,也拓展了多式聯運的應用場景。在亞太地區的第三方物流(3PL) 市場,服務定價正逐漸趨於多元化,不再僅基於單一路線的運費,而是綜合考慮運輸方式、風險緩衝和合規性等因素。國內和國際服務正圍繞著一個統一的控制中心進行整合,該中心負責協調跨運輸方式和區域的預訂、物流資訊和異常情況處理。

在這種服務結構中,到 2025 年,國內運輸管理佔亞太地區第三方物流市場佔有率的 46.12%。隨著對時間敏感貨物的多溫區儲存能力的擴大,預計到 2031 年,亞太地區第三方物流市場中的增值倉儲和配送服務將以每年 7.84% 的速度成長。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全部區域電子商務快速成長

- 區域貿易協定的實施

- 低溫運輸基礎設施建設

- 數位物流平台的普及

- 汽車和電子製造業的成長

- 中小企業外包趨勢

- 市場限制因素

- 新興國家的基礎建設差距

- 法規環境碎片化

- 熟練勞動力短缺

- 地緣政治緊張局勢與貿易不確定性

- 價值供應鏈分析

- 技術展望

- 監理情勢

- 對電子商務業務的洞察

- 波特五力模型

- 地緣政治事件對市場的影響

第5章 市場規模與成長預測

- 按服務

- 國內運輸管理

- 路

- 航空

- 其他

- 國際運輸管理

- 路

- 航空

- 海

- 多模態/跨模態

- 加值倉儲與物流 (VAWD)

- 國內運輸管理

- 按最終用戶行業分類

- 車

- 能源與公共產業

- 製造業

- 生命科學醫療保健

- 技術與電子

- 零售與電子商務

- 消費品/快速消費品

- 飲食

- 其他

- 物流模型

- 輕資產(託管)

- 資產密集型(公司車輛和倉庫)

- 混合

- 按地區

- 中國

- 印度

- 日本

- 韓國

- 新加坡

- 越南

- 印尼

- 澳洲

- 其他亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Supply Chain and Global Forwarding

- Sinotrans Ltd.

- Kintetsu World Express

- Nippon Express Holdings

- Yusen Logistics(NYK)

- Kuehne+Nagel International AG

- DSV A/S

- CEVA Logistics(CMA CGM)

- GEODIS

- Kerry Logistics Network

- LOGISTEED

- Toll Group

- JD Logistics

- AWOT Global Logistics Group

- CIMC Wetrans Logistics Technology

- Mainfreight

- Linfox

- CJ Logistics

- Hellmann Worldwide Logistics

- Savino Del Bene

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific third-Party logistics market size is projected to expand from USD 431.38 billion in 2025 and USD 504 billion in 2026 to USD 726.90 billion by 2031, registering a CAGR of 7.60% between 2026 to 2031.

This report is Segmented by Service (Domestic Transportation Management, International Transportation Management, Value-Added Warehousing and Distribution), End-User Industry (Automotive, Energy and Utilities, Manufacturing, and More), Logistics Model (Asset-Light, Asset-Heavy, Hybrid), and Geography (China, India, Japan, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Third-Party Logistics (3PL) Market Trends and Insights

E-commerce boom fuelling same-day and last-mile fulfilment

Rising online order density is shifting 3PL activity from bulk movements to high-frequency fulfillment that relies on automated nodes. JD Logistics reported operating more than 20 automated LangzuTech warehouses across nearly 20 cities by late 2025, which signals how large shippers are leaning on advanced facilities to support delivery speed and order accuracy as volumes increase. The Asia-Pacific third-party logistics market uses such assets to absorb seasonal spikes that would overwhelm traditional networks. Automated sorting and goods-to-person systems compress cycle times for small parcels, which improves customer experience and expands the serviceable market for time-sensitive categories. The Asia-Pacific third-party logistics market is also shaped by platform-backed investments that raise the floor for fulfillment standards across major urban hubs. Providers that align automation with dense last-mile routing are better placed to hold margins as price transparency increases.

Regional Trade Agreement Implementation

RCEP continues to lower friction across a trade zone spanning 15 economies, which encourages shippers to consolidate cross-border logistics under fewer partners. China's recorded goods trade with RCEP members reached RMB 9.63 trillion by Q3 2024, with year-over-year growth, and the China-Laos Railway has moved 11.58 million tons of cross-border cargo since late 2021, which underpins new multimodal solutions that 3PLs can package across borders. The Asia-Pacific third-party logistics market is already building combined road-rail-air offerings around these corridors. Document flow standardization through initiatives like the ASEAN Single Window has reduced paperwork time for participating members, which supports end-to-end visibility and more reliable transit planning. The Asia-Pacific third-party logistics market sees stronger appeal for cross-border trucking and rail alternatives when tariffs and procedures align. Providers with customs brokerage depth and origin-destination compliance teams gain an edge as tariff schedules phase down and certificates of origin integrate into digital workflows.

Infrastructure Gaps in Emerging Markets

Transport networks in several economies remain road-heavy and underdeveloped relative to OECD benchmarks, which limits route flexibility and raises cost-to-serve for long inland moves. Asian Transport Observatory data shows regional infrastructure density and road-to-rail mix lagging developed norms, which constrains modal shift options during disruptions. In Thailand, agricultural freight remains predominantly road-based with minor rail share, which pushes costs above global medians and compresses margins for bulk and FMCG shippers. The Asia-Pacific third-party logistics market can route around bottlenecks with selective use of rail and coastal feeder services where they exist, but dense corridors still face peak congestion. Climate risk adds exposure for roads and rail assets across the region with high precipitation volatility and typhoon frequency, which increases downtime and recovery costs for operators. The Asia-Pacific third-party logistics market will likely bifurcate strategies between premium corridors with planned upgrades and secondary routes where road dependence persists, which affects achievable service levels.

Other drivers and restraints analyzed in the detailed report include:

- Digital Logistics Platform Proliferation

- Cold Chain Infrastructure Development

- Geopolitical Tensions and Trade Uncertainties

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Domestic Transportation Management accounted for 46.12% in 2025, which reflected the scale of intra-regional trade and the reliance on trucking for the first and last mile across dense city clusters. That share underlined how route tendering and dynamic capacity brokerage are core capabilities as the Asia-Pacific third-party logistics market diversifies load profiles across short-haul and regional lanes. Value-Added Warehousing and Distribution is the fastest-growing service at a 7.84% CAGR in the period to 2031 as shippers shift inventory closer to consumption and expand cold-ready storage for pharmaceuticals and premium foods. The Asia-Pacific third-party logistics market integrates near-customer storage with micro-fulfillment and controlled-temperature handling to raise throughput and preserve product integrity. Providers that offer calibrated environments and validated processes can sustain higher yields relative to ambient storage. Select integrators are pairing VAWD sites with contract logistics for managed replenishment and vendor-managed inventory to stabilize turns and improve working capital. The Asia-Pacific third-party logistics market is also using automated storage and retrieval, high-bay racking, and robot-assisted picking to manage multi-SKU complexity without expanding footprints.

International Transport Management is diversifying across ocean, air, and rail-led intermodal as cost and reliability cycles shift. Red Sea disruptions pushed carriers and shippers to extend routings, which increased cycle times and raised premiums for time-definite freight, a trend 3PLs addressed with refined air allocation and temperature-controlled buffers for sensitive products. On select corridors, rail segments are now linked more seamlessly to trucking and air uplift to meet delivery windows that the ocean could not meet during volatility, which strengthens the role of corridor-specialist 3PLs that orchestrate multimodal schedules. CEVA highlights the role of engineered transport and customs digitization in reducing dwell time and increasing speed to market on cross-border routes, which expands the use cases for intermodal even as ocean schedules normalize. The Asia-Pacific third-party logistics market increasingly prices services on outcomes that blend mode choice, risk buffers, and compliance rather than on single-lane tariffs alone. Domestic and international services are converging around unified control towers that reconcile bookings, visibility, and exceptions across modes and zones.

In this service mix, Domestic Transportation Management accounted for 46.12% of the Asia-Pacific third-party logistics market share in 2025. Value-Added Warehousing and Distribution within the Asia-Pacific third-party logistics market size is projected to grow at 7.84% through 2031 as multi-temperature capacity scales for time-critical loads.

List of Companies Covered in this Report:

- DHL Supply Chain and Global Forwarding

- Sinotrans Ltd.

- Kintetsu World Express

- Nippon Express Holdings

- Yusen Logistics (NYK)

- Kuehne + Nagel International AG

- DSV A/S

- CEVA Logistics (CMA CGM)

- GEODIS

- Kerry Logistics Network

- LOGISTEED

- Toll Group

- JD Logistics

- AWOT Global Logistics Group

- CIMC Wetrans Logistics Technology

- Mainfreight

- Linfox

- CJ Logistics

- Hellmann Worldwide Logistics

- Savino Del Bene

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Boom Across Region

- 4.2.2 Regional Trade Agreement Implementation

- 4.2.3 Cold Chain Infrastructure Development

- 4.2.4 Digital Logistics Platform Proliferation

- 4.2.5 Automotive and Electronics Manufacturing Growth

- 4.2.6 Outsourcing Trend by SMEs

- 4.3 Market Restraints

- 4.3.1 Infrastructure Gaps in Emerging Markets

- 4.3.2 Fragmented Regulatory Environment

- 4.3.3 Shortage of Skilled Workforce

- 4.3.4 Geopolitical Tensions and Trade Uncertainties

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Insights into E-commerce Business

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts (Value USD)

- 5.1 By Service

- 5.1.1 Domestic Transportation Management

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Others

- 5.1.2 International Transportation Management

- 5.1.2.1 Road

- 5.1.2.2 Air

- 5.1.2.3 Sea

- 5.1.2.4 Multimodal / Intermodal

- 5.1.3 Value-Added Warehousing and Distribution (VAWD)

- 5.1.1 Domestic Transportation Management

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Energy and Utilities

- 5.2.3 Manufacturing

- 5.2.4 Life Sciences and Healthcare

- 5.2.5 Technology and Electronics

- 5.2.6 Retail and E-commerce

- 5.2.7 Consumer Goods and FMCG

- 5.2.8 Food and Beverages

- 5.2.9 Others

- 5.3 By Logistics Model

- 5.3.1 Asset-Light (Management-Based)

- 5.3.2 Asset-Heavy (Own Fleet and Warehouses)

- 5.3.3 Hybrid

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Singapore

- 5.4.6 Vietnam

- 5.4.7 Indonesia

- 5.4.8 Australia

- 5.4.9 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Supply Chain and Global Forwarding

- 6.4.2 Sinotrans Ltd.

- 6.4.3 Kintetsu World Express

- 6.4.4 Nippon Express Holdings

- 6.4.5 Yusen Logistics (NYK)

- 6.4.6 Kuehne + Nagel International AG

- 6.4.7 DSV A/S

- 6.4.8 CEVA Logistics (CMA CGM)

- 6.4.9 GEODIS

- 6.4.10 Kerry Logistics Network

- 6.4.11 LOGISTEED

- 6.4.12 Toll Group

- 6.4.13 JD Logistics

- 6.4.14 AWOT Global Logistics Group

- 6.4.15 CIMC Wetrans Logistics Technology

- 6.4.16 Mainfreight

- 6.4.17 Linfox

- 6.4.18 CJ Logistics

- 6.4.19 Hellmann Worldwide Logistics

- 6.4.20 Savino Del Bene

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

中東第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031)

中東第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031) 2026年全球履約服務市場報告2026年生物製藥冷藏物流鏈全球市場報告

2026年全球履約服務市場報告2026年生物製藥冷藏物流鏈全球市場報告 第三方化學品分銷市場:依產品類型、實體形態、服務及最終用途產業分類-2026-2032年全球市場預測第三方物流(3PL) 軟體市場:2026-2032 年全球市場預測(按應用、部署類型、服務類型、組織規模和最終用戶產業分類)

第三方化學品分銷市場:依產品類型、實體形態、服務及最終用途產業分類-2026-2032年全球市場預測第三方物流(3PL) 軟體市場:2026-2032 年全球市場預測(按應用、部署類型、服務類型、組織規模和最終用戶產業分類) 第三方化學品分銷市場:按類型、應用和地區分類(2026-2034 年)第三方物流市場:依產品/服務、服務模式、定價模式、運輸方式、應用領域及最終用戶產業分類-2026-2032年全球市場預測2026年全球第三方物流(3PL)市場報告

第三方化學品分銷市場:按類型、應用和地區分類(2026-2034 年)第三方物流市場:依產品/服務、服務模式、定價模式、運輸方式、應用領域及最終用戶產業分類-2026-2032年全球市場預測2026年全球第三方物流(3PL)市場報告 2026-2030年全球汽車第三者物流市場

2026-2030年全球汽車第三者物流市場 第三方物流軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類

第三方物流軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類