|

市場調查報告書

商品編碼

2072714

美國第三方物流倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States 3PL Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

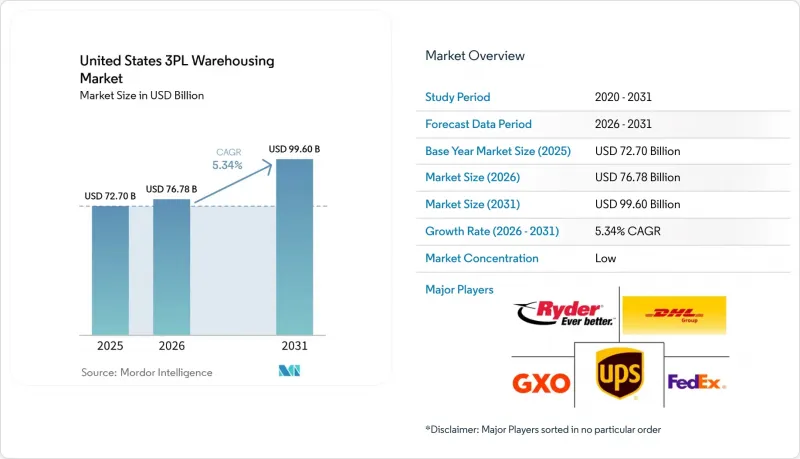

據 Mordor Intelligence 稱,2025 年美國第三方物流倉儲市場價值為 727 億美元,預計到 2031 年將達到 996 億美元,而 2026 年為 767.8 億美元,在 2026 年至 2031 年的預測期內,複合年成長率為 5.34%。

美國第三方物流倉儲市場的擴張主要受託運人從固定價格倉庫轉向可變成本合約的驅動,後者能夠應對關稅波動、採購履約變化以及更快的訂單履行需求。本報告按服務類型(倉儲、物流、附加價值服務)、倉庫類型(通用共用、專用合約倉庫、保稅倉庫)、溫度控制(非溫控倉庫、溫控倉庫)、技術應用(人工操作、半自動操作、全自動操作)以及最終用戶(製造業、消費品業等)進行細分。市場預測以以金額為準呈現。

美國第三方物流倉儲市場趨勢與洞察

疫情後電子商務物流履約的現狀

第三方履約(3PL) 已成為日常營運模式中不可或缺的一部分,84% 的品牌至少在部分訂單中使用第三方履約公司,44.0% 的品牌計劃在 2026 年前增加履約中心的數量。儘管疫情期間的倉儲需求激增有所緩解,但由於訂單日益複雜,需求依然強勁。全通路功能、品牌包裝、套件組裝和退貨處理等都增加了倉庫的工作流程。這種轉變使能夠管理多個地點而非僅管理一個大型物流中心的3PL 供應商更具優勢。此外,取消第 321 條的最低限度豁免也迫使跨境電商企業在美國境內設立更多履約中心。超過 75% 的品牌計劃在 2026 年前至少新增一個銷售管道,這意味著所有管道對庫存管理和訂單調整的需求將進一步增加。因此,美國 3PL 倉儲市場正從服務密集營運而非基礎倉儲中獲得更多收入。

美國供應鏈的近岸外包與回岸外包

近岸外包透過兩個相互關聯的階段推高了倉儲需求。首先,貨物需要在邊境進行轉運並利用保稅倉庫的容量,然後轉移到內陸的緩衝庫存和區域配送中心。德迅集團位於埃爾帕索的保稅倉庫在開業一年內便已滿負荷運轉,該公司宣布將於2025年11月利用毗鄰的新址進行60%的擴建。這個例子說明了在內陸倉儲網路全面投入運作之前,邊境地區的市場有多緊張。隨著製造商決定在北美建立生產基地,他們也需要更穩定的倉儲安排來抵禦供應中斷和運費波動的影響。這使得位於美國西南部和中西部部分走廊地帶的專用、保稅且合規性高的倉儲設施更具優勢。因此,美國第三方物流倉儲市場不僅受益於貿易路線的變化,也受益於與這些採購決策相關的長期商業週期。

人手不足和工資上漲

由於全國各地物流中心的職缺持續居高不下,勞動力仍是限制倉庫生產能力的阻礙因素。根據最新的就業和人員流動統計(JOLTS)報告,截至2026年3月,運輸、倉儲和公共產業行業的職缺超過80萬個。薪資上漲加劇了這個問題,因為運輸和倉儲業的薪資水準在2026年初持續上漲。高離職率進一步複雜化了這個問題,迫使營運商花費大量時間培訓和再培訓員工,而不是維持穩定的生產力。雖然自動化緩解了部分壓力,但也增加了對能夠操作和支援更先進技術系統的員工的需求。因此,勞動力仍然是美國第三方物流倉儲市場最明顯的短期阻礙因素之一。

細分市場分析

到2025年,倉儲服務將占美國第三方物流(3PL)倉儲市場的46.81%,這意味著托盤和庫存儲存能力仍將是該市場的基礎。這一高佔有率得以穩定維持,是因為許多托運人持有更多國內緩衝庫存,以降低關稅變化、前置作業時間波動和採購路線重組帶來的風險。對於經營多通路庫存池的零售商和製造商而言,分銷和庫存管理仍然至關重要。然而,成長趨勢正從純粹的倉儲合約轉向勞動密集型服務。附加價值服務和其他服務,包括套件組裝、貼標、重新包裝和退貨處理,預計到2031年將以8.18%的複合年成長率成長。

這種快速成長反映出客戶群不斷擴大,他們希望履約夥伴能夠在同一倉庫空間內處理更多流程。據ShipBob稱,品牌正在增加銷售管道數量並提高履約的複雜性,即使整體倉儲需求成長放緩,這也推動了每位客戶的收入成長。這也改變了定價方式,合約正從簡單的倉儲費轉向與操作次數、處理規則和服務保障掛鉤的收費系統。 Kenco和橘子之間為期五年的合作就是一個很好的例子,它展現了中型營運商如何利用編配軟體和機器人技術,在履約中心擴展這些高價值營運。在美國第三方物流倉儲產業,這種服務結構的轉變正在幫助那些能夠平衡嚴格的勞動力管理和工作流程自動化的營運商提高獲利能力。

到2025年,典型的共享或多客戶倉儲將占美國第三方物流倉儲市場的49.32%。這證實了即使在2024年庫存波動之後,柔軟性仍然具有很高的價值。許多托運人仍然傾向於共享倉儲,因為它允許他們在不受限於特定設施的情況下擴展或縮減空間。這種模式也適用於那些需要地域覆蓋的客戶以及目前不希望擁有專用於單一營運模式的租戶。同時,預計到2031年,專用合約倉儲將以每年7.35%的速度成長,高於任何其他倉儲模式。這種快速成長主要反映了客戶群的變化,他們主要是大型製造商和受監管的托運人,希望在建立更穩定的供應鏈結構後確保可靠的倉儲能力。

這兩種形式的差異表明,市場同時滿足兩種風險管理需求。共用空間幫助客戶在業務量波動時保持柔軟性,而專用空間則在需求趨於穩定時保護客戶免受產能短缺和價格上漲的影響。隨著進口商尋求延期繳納關稅和應對進口政策不確定性的方法,保稅倉儲也變得越來越重要。 DSV位於俄亥俄州哥倫布市附近、佔地120萬平方英尺的多客戶倉儲設施於2025年初投入使用,這表明,如果設計得當,單一資產可以同時滿足高規格工業用戶和電子商務租戶的需求。在美國第三方物流倉儲市場,倉庫類型的選擇越來越取決於每個托運人所需的柔軟性、合規性和成本可視性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務物流履約(後疫情時代標準)

- 美國供應鏈中的近岸外包與回岸外包

- 食品和製藥行業低溫運輸的擴展

- 倉庫自動化和機器人的成本優勢

- 機構投資者擴大對房地產投資信託基金投資的潛力

- 州級物流稅收優惠(東南部和中西部)

- 市場限制因素

- 勞動力嚴重短缺和工資上漲

- 城市地區土地短缺和分區障礙

- 利率上升導致資本投資收緊

- 溫控設施的ESG合規成本

- 法律規範

- 價值鍊和通路分析

- 技術創新的前景

- 波特五力分析

- 低溫運輸倉庫需求的演變

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模與成長預測

- 按服務類型

- 貯存

- 經銷和庫存管理

- 附加價值服務及其他服務(套件組裝、貼標籤)

- 倉庫類型

- 通用共用/多客戶端倉庫

- 專用合約倉庫

- 保稅倉庫

- 透過溫度控制

- 非溫控型

- 溫控型

- 透過技術實施

- 手動的

- 半自動

- 全自動

- 按最終用戶行業分類

- 製造業

- 消費品

- 食品/飲料

- 零售與電子商務

- 醫療保健和製藥

- 其他終端用戶產業

- 按地區

- 東北

- 東南

- 中西部

- 西南

- 西方

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- GXO Logistics

- Ryder System, Inc.

- United Parcel Service of America, Inc.(UPS)

- FedEx

- XPO, Inc.

- Kuehne+Nagel

- DSV A/S(Including DB Schenker)

- GEODIS

- CMA CGM Group(Including CEVA Logistics)

- Penske Corporation

- Lineage, Inc.

- Americold

- NFI Industries

- Kenco Group

- CJ Logistics

- Saddle Creek Logistics Services

- OHL

- Buske Logistics

- Burris Logistics

- Weber Logistics

- Radial

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states 3PL warehousing market size was valued at USD 72.70 billion in 2025 and estimated to grow from USD 76.78 billion in 2026 to reach USD 99.60 billion by 2031, at a CAGR of 5.34% during the forecast period 2026-2031.

The United States 3PL warehousing market is expanding because shippers are moving fixed warehouse assets into variable-cost contracts that can absorb tariff swings, changing sourcing routes, and faster fulfillment expectations. This report is Segmented by Service Type (Storage, Distribution, Value-Added Services), by Warehouse Type (General Shared, Dedicated Contract, Bonded), by Temperature Control (Non-Temperature Controlled, Temperature Controlled), by Technology Adoption (Manual, Semi-Automated, Fully Automated), and by End User (Manufacturing, Consumer Goods, and More). The Market Forecasts are Provided in Terms of Value.

United States 3PL Warehousing Market Trends and Insights

E-Commerce Fulfillment Boom Post-Pandemic Baseline

Third-party fulfillment is now embedded in everyday operating models, with 84% of brands using a third-party fulfillment company for at least some orders, and 44.0% planning to increase their number of fulfillment centers in 2026. The storage surge seen during the pandemic period has matured, but order complexity has kept demand firm because omnichannel compliance, branded packaging, kitting, and returns work all require more warehouse touches. That shift favors 3PL operators that can manage multiple sites rather than only a single large distribution center. The removal of the Section 321 de minimis exemption is also pushing cross-border e-commerce sellers to establish more domestic fulfillment footprints in the United States. More than 75% of brands plan to add at least 1 new sales channel in 2026, which means inventory placement and order orchestration become more demanding across every channel. As a result, the United States 3PL warehousing market is gaining more revenue from service intensity than from basic storage alone.

Nearshoring and Reshoring of the United States Supply Chains

Nearshoring is increasing warehouse demand in 2 linked steps, with freight first needing border transload and bonded capacity, and then moving into inland buffer stock and regional distribution space. Kuehne+Nagel's El Paso bonded warehouse reached full capacity within 1 year of opening, which led the company to announce a 60% expansion through a new adjacent site in November 2025. That example shows how border markets are tightening before inland warehouse networks have fully adjusted. Once manufacturers commit to North American production footprints, they also need more stable warehouse arrangements to protect against supply interruptions and rate volatility. This favors dedicated, bonded, and high-compliance facilities in the Southwest and selected Midwest corridors. The United States 3PL warehousing market is therefore benefiting not only from trade rerouting, but also from the longer operating cycles that follow those sourcing decisions.

Acute Labor Shortages and Wage Inflation

Labor remains a direct limit on warehouse output because open positions are still elevated across the national logistics base. The latest JOLTS release showed more than 800,000 job openings in transportation, warehousing, and utilities in March 2026. Wage growth is compounding the issue, since transportation and warehousing compensation continued to rise through early 2026. High turnover makes the problem harder to solve because operators spend more time training and retraining staff instead of stabilizing productivity. Automation can ease some of the pressure, but it also increases the need for workers who can operate and support more technical systems. For that reason, labor remains one of the clearest near-term limits on the United States 3PL warehousing market.

Other drivers and restraints analyzed in the detailed report include:

- Cold-Chain Expansion for Food and Pharma

- Warehouse Automation and Robotics Cost Advantages

- Urban-Core Land Scarcity and Zoning Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Storage accounted for 46.81% of the United States 3PL warehousing market in 2025, indicating that pallet and inventory capacity still form the basis of this market. That large share has remained resilient because many shippers are holding more domestic buffer stock to reduce exposure to tariff changes, lead-time volatility, and sourcing realignment. Distribution and inventory management also remain important for retailers and manufacturers running multi-channel inventory pools. Even so, the growth pattern has moved toward more labor-intensive services rather than pure storage contracts. Value-added services and others, including kitting, labeling, repackaging, and returns handling, are projected to expand at an 8.18% CAGR through 2031.

This faster growth reflects a customer mix that wants fulfillment partners to absorb more process steps inside the same warehouse footprint. ShipBob reported that brands are increasing channel counts and fulfillment complexity, which supports higher revenue per client even as total storage demand grows more slowly. That changes pricing discussions, because contracts move away from a narrow storage rate and toward charges tied to touches, handling rules, and service commitments. Kenco's 5-year partnership with GreyOrange shows how mid-tier operators are using orchestration software and robotics to scale those higher-value activities across fulfillment centers. In the United States 3PL warehousing industry, this service mix shift supports margins for operators that can pair labor discipline with workflow automation.

General shared or multi-client warehousing held 49.32% of United States 3PL warehousing market share in 2025, which confirms that flexibility still carries strong value after the inventory swings seen in 2024. Many shippers continue to prefer shared capacity because it allows them to scale space up or down without tying capital to dedicated buildings. This format also suits tenants that need regional coverage but do not yet want a site built around a single operating model. At the same time, dedicated contract warehousing is projected to grow at 7.35% through 2031, which is faster than any other warehouse format. That faster growth reflects a different customer set, mainly larger manufacturers and regulated shippers that want assured capacity once they commit to a more stable supply chain footprint.

The split between these 2 formats shows that the market is serving 2 kinds of risk management at once. Shared space helps customers stay flexible during volume swings, while dedicated space protects them against capacity shortages and price spikes once demand becomes more predictable. Bonded warehousing has also gained relevance as importers look for ways to defer duties and manage policy uncertainty around inbound goods. DSV's 1.2 million-square-foot multi-client facility near Columbus, Ohio, which opened in early 2025, shows how a single asset can serve both high-spec industrial users and e-commerce tenants when the design is right. In the United States 3PL warehousing market, warehouse type selection increasingly depends on how much flexibility, compliance, and cost visibility each shipper needs.

Complete Report Scope:

- By Service Type

- Storage

- Distribution and Inventory Management

- Value-Added Services and Others (Kitting, Labeling)

- By Warehouse Type

- General Shared / Multi-client Warehousing

- Dedicated Contract Warehousing

- Bonded Warehousing

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Technology Adoption

- Manual

- Semi-automated

- Fully Automated

- By End User Industry

- Manufacturing

- Consumer Goods

- Food and Beverage

- Retail and E-commerce

- Healthcare and Pharma

- Other End-user Industries

- By Region

- Northeast

- Southeast

- Midwest

- Southwest

- West

List of Companies Covered in this Report:

- DHL Group

- GXO Logistics

- Ryder System, Inc.

- United Parcel Service of America, Inc. (UPS)

- FedEx

- XPO, Inc.

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- GEODIS

- CMA CGM Group (Including CEVA Logistics)

- Penske Corporation

- Lineage, Inc.

- Americold

- NFI Industries

- Kenco Group

- CJ Logistics

- Saddle Creek Logistics Services

- OHL

- Buske Logistics

- Burris Logistics

- Weber Logistics

- Radial

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Fulfilment Boom (Post-Pandemic Baseline)

- 4.2.2 Nearshoring and Reshoring of the United States Supply Chains

- 4.2.3 Cold-Chain Expansion for Food and Pharma

- 4.2.4 Warehouse Automation and Robotics Cost Advantages

- 4.2.5 Institutional REIT Investment Expanding Capacity

- 4.2.6 State-Level Logistics Tax Incentives (SE and Midwest)

- 4.3 Market Restraints

- 4.3.1 Acute Labor Shortages and Wage Inflation

- 4.3.2 Urban-Core Land Scarcity and Zoning Hurdles

- 4.3.3 Rising Interest-Rate Driven Cap-Ex Squeeze

- 4.3.4 ESG Compliance Costs for Temperature-Controlled Sites

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Evolution of Cold-Chain Warehousing Requirements

- 4.9 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution and Inventory Management

- 5.1.3 Value-Added Services and Others (Kitting, Labeling)

- 5.2 By Warehouse Type

- 5.2.1 General Shared / Multi-client Warehousing

- 5.2.2 Dedicated Contract Warehousing

- 5.2.3 Bonded Warehousing

- 5.3 By Temperature Control

- 5.3.1 Non-Temperature Controlled

- 5.3.2 Temperature Controlled

- 5.4 By Technology Adoption

- 5.4.1 Manual

- 5.4.2 Semi-automated

- 5.4.3 Fully Automated

- 5.5 By End User Industry

- 5.5.1 Manufacturing

- 5.5.2 Consumer Goods

- 5.5.3 Food and Beverage

- 5.5.4 Retail and E-commerce

- 5.5.5 Healthcare and Pharma

- 5.5.6 Other End-user Industries

- 5.6 By Region

- 5.6.1 Northeast

- 5.6.2 Southeast

- 5.6.3 Midwest

- 5.6.4 Southwest

- 5.6.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 GXO Logistics

- 6.4.3 Ryder System, Inc.

- 6.4.4 United Parcel Service of America, Inc. (UPS)

- 6.4.5 FedEx

- 6.4.6 XPO, Inc.

- 6.4.7 Kuehne+Nagel

- 6.4.8 DSV A/S (Including DB Schenker)

- 6.4.9 GEODIS

- 6.4.10 CMA CGM Group (Including CEVA Logistics)

- 6.4.11 Penske Corporation

- 6.4.12 Lineage, Inc.

- 6.4.13 Americold

- 6.4.14 NFI Industries

- 6.4.15 Kenco Group

- 6.4.16 CJ Logistics

- 6.4.17 Saddle Creek Logistics Services

- 6.4.18 OHL

- 6.4.19 Buske Logistics

- 6.4.20 Burris Logistics

- 6.4.21 Weber Logistics

- 6.4.22 Radial

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

印度第三方物流倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國第三方物流倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中東第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031)

印度第三方物流倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國第三方物流倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)中東第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031) 2026年全球履約服務市場報告2026年生物製藥冷藏物流鏈全球市場報告亞太地區第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031)

2026年全球履約服務市場報告2026年生物製藥冷藏物流鏈全球市場報告亞太地區第三方物流(3PL):市場佔有率分析、產業趨勢與統計及成長預測 (2026-2031) 第三方化學品分銷市場:依產品類型、實體形態、服務及最終用途產業分類-2026-2032年全球市場預測第三方物流(3PL) 軟體市場:2026-2032 年全球市場預測(按應用、部署類型、服務類型、組織規模和最終用戶產業分類)

第三方化學品分銷市場:依產品類型、實體形態、服務及最終用途產業分類-2026-2032年全球市場預測第三方物流(3PL) 軟體市場:2026-2032 年全球市場預測(按應用、部署類型、服務類型、組織規模和最終用戶產業分類) 第三方化學品分銷市場:按類型、應用和地區分類(2026-2034 年)第三方物流市場:依產品/服務、服務模式、定價模式、運輸方式、應用領域及最終用戶產業分類-2026-2032年全球市場預測

第三方化學品分銷市場:按類型、應用和地區分類(2026-2034 年)第三方物流市場:依產品/服務、服務模式、定價模式、運輸方式、應用領域及最終用戶產業分類-2026-2032年全球市場預測