|

市場調查報告書

商品編碼

2062363

德國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Germany E-Commerce Warehouse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

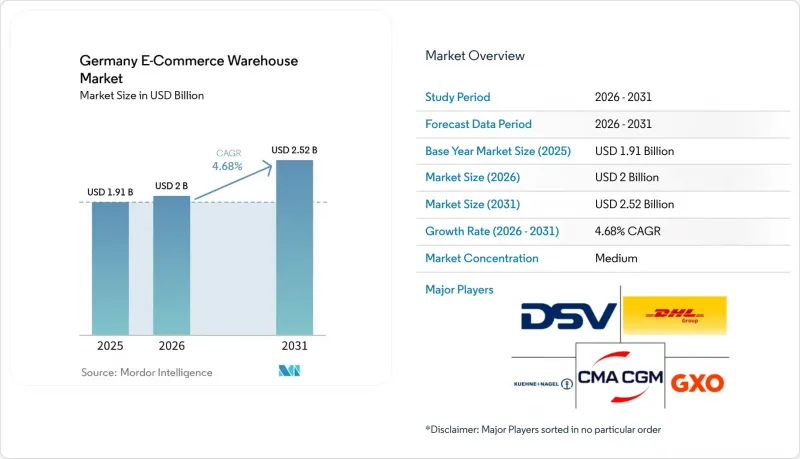

根據 Mordor Intelligence 預測,德國電子商務倉儲市場規模將從 2025 年的 19.1 億美元成長到 2026 年的 20 億美元,到 2031 年將達到 25.2 億美元,2026 年至 2031 年的複合年成長率為 4.68%。

隨著投資轉向自動化維修、多溫區儲存系統和垂直擴建,營運商優先考慮提高儲存密度而非新建倉庫,產能規劃也正在重新定義。本報告按倉庫類型(例如:履約中心、物流中心等)、服務類型(例如:倉儲、揀貨包裝等)、自動化程度(例如:人工、半自動、全自動)、終端用戶行業(例如:服裝鞋類、消費電子產品等)和地區(例如:北萊茵-威斯特法倫州等)進行細分。市場預測以美元計價。

德國電子商務倉儲市場的趨勢與洞察

歐盟境內跨境電子商務分銷快速成長

德國地理位置居中,與萊茵-阿爾卑斯走廊交通便捷,是泛歐歐盟的重要樞紐。企業利用保稅區,將關稅延至最終交付時繳納,從而減輕經銷商的營運資金負擔。 DHL位於鄰近的波茲南的樞紐,日處理包裹量達百萬件,是網路擴張的典範,將德國和東歐的設施連接成一個統一的履約網路。對附加價值服務(例如多幣種結算、本地化包裝和符合增值稅增值稅的文件)日益成長的需求正在推動市場成長。同時,多語種員工團隊和內部海關專業知識正逐漸成為企業的競爭優勢。

線上雜貨和快速電商的需求加速成長

預計到2030年,線上食品雜貨銷售額將達到180億歐元(206億美元),佔食品總支出的17%。 REWE位於馬格德堡的物流中心耗資2.5億歐元(2.86億美元),自動化程度達50%,每天處理28.6萬個包裹,充分體現了多溫區物流履約的資本密集特性。快速電商品牌正在客戶3-5公里範圍內建立微型倉配中心,將配送時間縮短至60分鐘以內。多區域儲存系統將常溫、冷藏和冷凍商品整合到單一自動化框架中,逐漸成為行業標準,從而在不犧牲產能的前提下,實現更快的商品處理速度。

高功率自動化系統中的電網容量瓶頸

機器人系統通常消耗3-5兆瓦的持續電力,這往往超過當地變電站的備用容量。如此高的能源需求常常對基礎設施的準備構成重大挑戰。由於併網等待時間長達18個月,部署被延誤,迫使營運商選擇分階段部署或採用臨時性的半自動化解決方案來維持營運的連續性。與公共產業的合作凸顯了所需升級的規模。例如,DHL和E.ON的直流電氣化計畫就表明,為了支援先進的機器人系統,迫切需要對能源基礎設施進行現代化改造。

細分市場分析

到2025年,履約中心將佔德國電商倉儲市場的52.94%,體現了其在產品類別和訂單類型方面的多功能性。同時,由於快消業者需要在收到終端用戶訂單後幾分鐘內提供庫存,預計到2031年,暗店和微型倉配中心將以9.1%的複合年成長率穩步成長。低溫運輸自動化技術的進步正推動大規模履約中心和緊湊型城市倉庫採用多溫區設計。配銷中心繼續為傳統零售商處理大宗補貨,而低溫運輸倉庫在醫藥和生鮮食品行業中越來越受歡迎。 「其他」類別包括逆向物流中心和保稅倉庫,它們提供諸如倉儲和退貨處理等特殊增值提案,允許延期繳納關稅。

技術進步正以各種形式蓬勃發展。在弗拉申波斯特(Flaschenpost)位於朗根費爾德(Langenfeld)的倉庫中,一套用於常溫和冷藏商品的整合式AutoStore網格每小時可處理1000份訂單,充分展現了自動化如何在速度和溫度控制之間取得平衡。傳統的履約中心正積極採用模組化機器人系統,這些系統能夠根據季節靈活調整產能,在最大限度地降低成本的同時,確保未來應對力變化的產品組合。隨著全通路業者對倉庫空間的需求日益成長,倉庫類型之間的界限也變得越來越模糊,這些空間只需進行最小程度的重新配置即可在托盤式散裝貨物和單件揀貨之間切換。

到2025年,倉儲營運將佔總收入的54.11%,並將繼續作為所有企業必須提供的基礎職能。然而,隨著品牌商將套件組裝、貼標和在地化等業務外包以縮短前置作業時間和降低複雜性,到2031年,附加價值服務的複合年成長率將達到7.92%。揀貨和包裝是電子商務的核心環節,也是勞動密集環節,因此佔據了自動化投資的大部分,因為該環節的準確性和速度直接影響客戶滿意度。 REWE位於馬格德堡的配送中心已實現了50%的倉儲和揀貨區域的自動化,這表明整合服務包如何減少貨物停留時間並降低對勞動力的依賴。

具備法規遵從、測試和小型客製化專業知識的業者能夠建立牢固的客戶關係並提高利潤率。人工智慧驅動的倉庫管理系統 (WMS) 解決方案可最佳化訂單批量處理和人員配置,而機器人技術則可降低錯誤率並支援全天候尖峰時段迴應。隨著商品化倉儲獲利能力的下降,多元化的服務組合成為客戶維繫和合約續約的關鍵因素。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟內部跨境電子商務交易激增。

- 線上雜貨和快速電商的需求加速成長

- 訂閱和自動續訂商業的激增

- 現有零售商整合全通路庫存

- 現有設施中垂直自動化夾層系統的維修

- 與環境、社會及公司治理(ESG)相關的綠色倉儲融資獎勵

- 市場限制因素

- 高功率自動化中的電網容量瓶頸

- 倉庫營運技術系統面臨的網路安全威脅日益加劇

- 歐盟關於包裝和廢棄物。

- 建築材料供應衝擊和成本飆升

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 倉庫類型

- 履約中心

- 物流中心(DC)

- 低溫運輸倉庫

- 暗店/微型倉配中心

- 其他(逆向物流中心、保稅倉庫、多功能空間等)

- 按服務類型

- 貯存

- 揀貨和包裝

- 附加價值服務及其他服務(套件組裝、貼標籤)

- 按自動化級別

- 手動的

- 半自動

- 自動化

- 按最終用戶行業分類

- 服裝和鞋類

- 消費性電子產品

- 食品和快速消費品

- 醫藥、美容和健康

- 家居用品/家具

- 其他

- 按州分類 - 德國

- 北萊茵-威斯特法倫州

- 巴伐利亞

- 巴登-符騰堡州

- 其他州

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- DSV(incl. Schenker)

- Otto Group

- Fiege Logistik

- Rhenus Logistics

- GXO Logistics

- CMA CGM Group(Including CEVA Logistics)

- B+S Logistics

- Kuehne+Nagel

- Arvato Supply Chain Solutions

- Zalando Logistics

- Loxxess AG

- Pfenning Logistics Group

- BLG Logistics Group

- DACHSER

- Hellmann Worldwide Logistics

- GEODIS

- Hermes Fulfilment

- Geis Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany e-commerce warehouse market size is expected to grow from USD 1.91 billion in 2025 to USD 2.00 billion in 2026 and is forecast to reach USD 2.52 billion by 2031 at 4.68% CAGR over 2026-2031.

An investment shift toward automation retrofits, multi-temperature capabilities, and vertical expansions is redefining capacity planning as operators favor density over new footprints. This report is Segmented by Warehouse Type (Fulfilment Centers, Distribution Centers, and More), by Service Type (Storage, Picking and Packing, and More), by Automation Level (Manual, Semi-Automated, Automated), by End-User Industry (Apparel and Footwear, Consumer Electronics, and More), and by Geography (North Rhine-Westphalia, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany E-Commerce Warehouse Market Trends and Insights

Booming Cross-Border EU E-Commerce Flows

Germany's central geography and Rhine-Alpine corridor connectivity make it the preferred consolidation point for pan-European e-commerce. Operators deploy customs-bonded zones that defer duties until final delivery, lowering working-capital exposure for merchants. DHL's 1 million-parcel-per-day hub in nearby Poznan exemplifies network extensions that knit German and Eastern European facilities into a single fulfillment mesh. Growth in multi-currency invoicing, localized packaging, and VAT-compliant documentation strengthens demand for value-added services, while multilingual labor pools and in-house brokerage expertise emerge as competitive moats.

Acceleration of Online Grocery & Q-Commerce Demand

Online grocery sales are on track to hit EUR 18 billion (USD 20.6 billion) by 2030 as penetration climbs to 17% of food outlays. REWE's EUR 250 million (USD 286 million) Magdeburg hub processes 286,000 packages daily with 50% automation, showing the capital intensity of multi-temperature fulfillment. Quick-commerce brands place micro-fulfillment nodes within 3-5 km of customers, compressing delivery windows below 60 minutes. Multi-zone storage grids that integrate ambient, chilled, and frozen SKUs inside the same automation framework are becoming standard, allowing high-velocity SKU handling without capacity trade-offs.

Electric-Grid Capacity Bottlenecks for High-Power Automation

Robotic systems typically consume 3-5 MW of continuous power, frequently surpassing the spare capacity of local substations. This high energy demand often creates significant challenges for infrastructure readiness. With connection queues stretching up to 18 months, rollouts face delays, nudging operators towards phased deployments or temporary semi-automated solutions to maintain operational continuity. The scale of necessary upgrades is underscored by partnerships with utilities, exemplified by DHL-E.ON's DC electrification program, which highlights the critical need for modernized energy infrastructure to support advanced robotic systems.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Subscription/Auto-Replenishment Commerce

- Omni-channel Inventory Consolidation by Legacy Retailers

- Rising Cybersecurity Threats to Warehouse OT Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fulfilment centers held 52.94% of the Germany e-commerce warehouse market size in 2025, reflecting their versatility across product categories and order profiles. Dark Stores and micro-fulfilment centers, however, post a brisk 9.1% CAGR through 2031 as quick-commerce players require inventory within minutes of end users. The rise of cold-chain automation brings multi-zone temperature designs to both large fulfilment hubs and compact urban nodes. Distribution centres continue to serve bulk replenishment for legacy retailers, while cold-chain warehouses gain traction among pharma and fresh-food operators. Reverse-logistics hubs and bonded sites populate the others category, offering specialized value propositions like duty-deferred storage and returns processing.

Technical sophistication grows in all formats. Flaschenpost's Langenfeld facility processes 1,000 orders per hour via integrated ambient and chilled AutoStore grids, showcasing how automation harmonizes speed and temperature control. Legacy fulfilment centres reply with modular robotics that flex capacity across seasons, minimizing sunk costs while future-proofing against evolving product mixes. Blurred lines between warehouse types emerge as omni-channel merchants demand spaces able to pivot from bulk pallet moves to single-unit picks with minimal reconfiguration.

Storage remains foundational at 54.11% of 2025 revenue, a function every operator must offer. Yet Value-Added Services grow 7.92% CAGR to 2031 as brands outsource kitting, labeling, and localization to reduce lead times and complexity. Picking and packing, the labor-intensive heart of e-commerce, drives most automation spend because accuracy and speed here translate directly into customer satisfaction. REWE's Magdeburg hub, automated to 50% across storage and pick zones, illustrates how integrated service bundles cut dwell times and curb workforce dependency.

Operators who master regulatory compliance, testing, and light customization create sticky relationships and margin uplifts. AI-enhanced WMS solutions optimize order batching and labor allocation, while robotics shrinks error rates and supports 24/7 peaks. As commoditized storage yields lower margins, diversified service portfolios become decisive in client retention and contract renewals.

List of Companies Covered in this Report:

- DHL Group

- DSV (incl. Schenker)

- Otto Group

- Fiege Logistik

- Rhenus Logistics

- GXO Logistics

- CMA CGM Group (Including CEVA Logistics)

- B+S Logistics

- Kuehne+Nagel

- Arvato Supply Chain Solutions

- Zalando Logistics

- Loxxess AG

- Pfenning Logistics Group

- BLG Logistics Group

- DACHSER

- Hellmann Worldwide Logistics

- GEODIS

- Hermes Fulfilment

- Geis Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming Cross-Border EU E-Commerce Flows

- 4.2.2 Acceleration of Online Grocery and Q-Commerce Demand

- 4.2.3 Surge in Subscription/Auto-Replenishment Commerce

- 4.2.4 Omni-Channel Inventory Consolidation by Legacy Retailers

- 4.2.5 Vertical Automated Mezzanine Retrofits in Existing Sites

- 4.2.6 ESG-Linked Green-Warehouse Financing Incentives

- 4.3 Market Restraints

- 4.3.1 Electric-Grid Capacity Bottlenecks for High-Power Automation

- 4.3.2 Rising Cybersecurity Threats to Warehouse OT Systems

- 4.3.3 Stricter EU Packaging and Waste-Compliance Directives

- 4.3.4 Construction-Material Supply Shocks & Cost Spikes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 Fulfilment Centres

- 5.1.2 Distribution Centres (DCs)

- 5.1.3 Cold-Chain Warehouses

- 5.1.4 Dark Stores / Micro-Fulfillment Centers

- 5.1.5 Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-Use Spaces, etc.)

- 5.2 By Service Type

- 5.2.1 Storage

- 5.2.2 Picking and Packing

- 5.2.3 Value-Added Services and Others (Kitting, Labelling)

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-Automated

- 5.3.3 Automated

- 5.4 By End-User Industry

- 5.4.1 Apparel and Footwear

- 5.4.2 Consumer Electronics

- 5.4.3 Grocery and FMCG

- 5.4.4 Pharmaceuticals, Beauty and Wellness

- 5.4.5 Home Essentials and Furnishings

- 5.4.6 Others

- 5.5 By States - Germany (Value)

- 5.5.1 North Rhine-Westphalia

- 5.5.2 Bavaria (Bayern)

- 5.5.3 Baden-Wurttemberg

- 5.5.4 Rest of States

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 DHL Group

- 6.4.2 DSV (incl. Schenker)

- 6.4.3 Otto Group

- 6.4.4 Fiege Logistik

- 6.4.5 Rhenus Logistics

- 6.4.6 GXO Logistics

- 6.4.7 CMA CGM Group (Including CEVA Logistics)

- 6.4.8 B+S Logistics

- 6.4.9 Kuehne+Nagel

- 6.4.10 Arvato Supply Chain Solutions

- 6.4.11 Zalando Logistics

- 6.4.12 Loxxess AG

- 6.4.13 Pfenning Logistics Group

- 6.4.14 BLG Logistics Group

- 6.4.15 DACHSER

- 6.4.16 Hellmann Worldwide Logistics

- 6.4.17 GEODIS

- 6.4.18 Hermes Fulfilment

- 6.4.19 Geis Group

7 Market Opportunities and Future Outlook

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告

2026年全球多深度穿梭系統市場報告 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年) 按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)亞太地區化學品倉儲市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)亞太地區化學品倉儲市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 全球按需倉儲市場:按組織、產業和地區分類-市場規模、產業動態、機會分析和預測(2026-2035 年)中東電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

全球按需倉儲市場:按組織、產業和地區分類-市場規模、產業動態、機會分析和預測(2026-2035 年)中東電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)