|

市場調查報告書

商品編碼

2062296

中東電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Middle East E-commerce Warehouse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

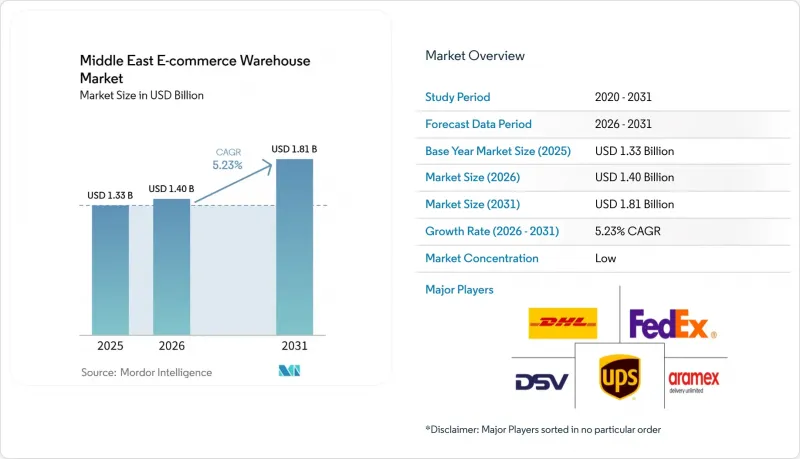

根據 Mordor Intelligence 預測,中東電子商務倉儲市場規模預計到 2025 年將達到 13.3 億美元,到 2026 年將達到 14 億美元,到 2031 年將達到 18.1 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 5.23%。

隨著線上零售交易量的快速成長、數位支付的日益普及以及新的跨境貿易協定縮短了履約週期,市場正在不斷擴張,企業也因此更傾向於建設更智慧、位置更優越的設施。 [1] 南非統計局,《月度批發零售指數》,stats.gov.sa。大量投資湧入溫控倉庫、最後一公里配送中心和人工智慧驅動的庫存管理系統,同時政府資金持續用於建造整合港口、機場和自由區的大型物流園區。本報告按倉庫類型(履約中心、配銷中心等)、服務類型(倉儲、揀貨包裝、附加價值服務)、自動化程度(人工、半自動、全自動)、終端用戶行業(服裝鞋帽、食品雜貨及快速消費品等)和地區(沙烏地阿拉伯等)進行細分。市場預測以美元計價。

中東電子商務倉儲市場趨勢與洞察

數位支付的日益普及使得預付的履約能力得以擴展。

數位錢包和「先買後付」選項的普及,已將現金處理從倉庫轉移到金融科技領域。預付訂單減少了營運資金的佔用,降低了安全庫存,並使履約團隊無需進行貨到付款流程即可承諾當日出貨。降低竊盜風險和保險費用帶來了成本效益,而銀行提供的即時驗證API則使得倉庫能夠在結帳後幾分鐘內開始波浪式揀貨。現金週轉週期的縮短在阿拉伯聯合大公國尤為顯著,該國超過70%的線上訂單已採用預付方式,這使得企業能夠在不相應增加庫存的情況下擴展業務。

區域自由貿易協定縮短了海灣合作理事會區域內的海關清關時間。

2025年1月海灣合作理事會統一關稅表的擴展,將原本各自獨立的國家網路整合為區域性平台。憑藉統一的編碼和一站式清關服務,利雅德的履約中心現在可以在72小時內向科威特和阿曼的客戶補貨,無需重新申報。沙烏地阿拉伯新建的特殊綜合物流區提供長達50年的免稅待遇,正加速向樞紐輻射型物流模式的轉型。同時,杜拜正利用保稅走廊加強港口與機場之間的協調。智慧型手機和快時尚等快速消費品的貿易摩擦正在得到最迅速的解決,這為企業提供了一種新的選擇:只需一次採購,即可在整個沿岸地區反覆銷售。

自由貿易區外甲級物流用地短缺,推高了租金溢價。

許多新建倉庫都位置自由貿易區區內,而區外的土地往往缺乏寬鬆的高度限制、消防安全設施或明確的外國所有權規定。由於供應無法滿足需求,預計到2025年,杜拜主要幹道的租金將出現兩位數的成長,迫使小型開發商轉向道路網路較弱的郊區地塊。儘管一些投機性開發商已經開始建設,但由於獲得授權可能需要數年時間,供應短缺預計將持續一段時間。客製化建造協議雖然可以確保租戶,但通常需要長期租賃,這使得小規模品牌難以進入市場,新進入者仍面臨許多挑戰。

細分市場分析

至2025年,履約中心將佔中東電商倉儲市場佔有率的43.81%。這反映了它們作為多通路庫存樞紐的作用,為幹線運輸、小包裹遞送和線上訂購線下自提網路提供庫存。這些物流中心的面積通常在1萬至5萬平方公尺之間,位置於郊區,兼顧租金和港口、高速公路的便利交通。營運商正在部署高層貨架、用於附加價值服務的夾層以及與承運商API同步的倉庫管理系統(WMS)。隨著營運商從單體倉庫轉向第三方共用設施,無需擁有資產即可實現規模化擴張,市場需求仍然強勁。

都市區暗店和微型倉配中心正經歷最快的成長,預計到2031年將達到10.68%的複合年成長率,這主要得益於承諾30分鐘內送達食品雜貨和藥品的電商應用程式。這些面積在300至2000平方公尺之間的場所專注於暢銷商品,採用高密度的周轉箱網格佈局,並受益於人工智慧技術,能夠按小時預測本地需求。儘管微型倉配在中東電商倉儲市場中的規模仍然小規模,但城市地區的土地稀缺促使人們開發出巧妙的解決方案,例如改造購物中心的地下室和屋頂。德迅集團位於杜拜EZDubai區的23,000平方公尺的設施展示了傳統第三方物流公司如何將大型履約中心與相鄰的微型配送中心相結合,從而同時滿足大容量儲存和超快速配送的需求。

到2025年,倉儲服務將佔中東電商倉儲市場規模的50.07%,因為電商仍依賴安全、溫控的庫存儲存。托盤容量、層高和消防設施仍然是大多數租戶的關鍵租賃要求。然而,服務的商品化導致利潤率較低,營運商正在尋求更永續的收入來源。附加價值服務以10.15%的複合年成長率成長,包括套件組裝、後製製造、個人化包裝和攝影棚。隨著品牌商要求本地化客製化以縮短供應鏈並遵守語言和監管標籤規則,與這些服務相關的中東電商倉儲市場規模正在成長。

Expeditors位於杜拜南部的23,200平方公尺的設施正是這種轉型的象徵,它將訂單管理、退貨檢驗和出口單據製作全部集中在一處。品牌願意為在地化服務支付額外費用,以實現針對特定地區的產品發布和季節性產品組合。雖然揀貨和包裝仍然至關重要,但自動化、語音引導耳機和揀貨指示燈貨架的運用縮短了每筆訂單的處理時間,使Expeditors能夠將競爭優勢集中於更高價值的組裝和客製化服務,而非簡單的入庫和出庫操作。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 數位支付的廣泛應用正在釋放預付履約的潛力。

- 透過區域自由貿易協定縮短海灣合作理事會內部海關週期。

- 疫情後,食品雜貨和藥品補給應轉向「線上優先」。

- 即插即用的4PL控制塔輔助中小企業拓展跨境業務

- 循環經濟再交易平台的快速崛起正在推動專門的退貨中心的建立。

- 人工智慧驅動的庫存預測引擎:論證高吞吐量自動化的合理性

- 市場限制因素

- 自由貿易區外甲級物流用地短缺,推高了租金溢價。

- 工業電費波動對低溫運輸利潤率帶來壓力。

- 環境、社會及公司治理(ESG)資訊揭露要求正在推動對太陽能發電和碳中和倉庫的投資增加。

- 貨到付款的廣泛應用使逆向物流和資金回收流程變得複雜。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 倉庫租金趨勢

第5章 市場規模與成長預測

- 倉庫類型

- 履約中心

- 物流中心(DC)

- 低溫運輸倉庫

- 暗店/微型倉配中心

- 其他(逆向物流中心、保稅倉庫、多功能空間等)

- 按服務類型

- 貯存

- 揀貨和包裝

- 附加價值服務及其他服務(套件組裝、貼標籤)

- 按自動化級別

- 手動的

- 半自動

- 自動的

- 按最終用戶行業分類

- 服裝和鞋類

- 家用電子產品

- 食品和快速消費品

- 醫藥、美容和健康

- 家居用品和家具

- 其他

- 國家

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 卡達

- 科威特

- 巴林

- 阿曼

- 埃及

- 其他中東國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Aramex

- DSV(Including DH Schenker)

- DHL Supply Chain

- UPS Supply Chain Solutions

- FedEx Logistics

- Gulf Warehousing Company

- Naqel Express

- RSA Global

- iMile

- J&T Express Middle East

- Wared Logistics

- SAL Saudi Logistics

- Bahri Logistics

- DP World Logistics

- Emirates Logistics

- Etihad Cargo Logistics

- Al-Futtaim Logistics

- AJEX

- GAC

- CMA CGM(Including CEVA Logistics)*

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east e-commerce warehousing market size is projected to be USD 1.33 billion in 2025, USD 1.40 billion in 2026, and reach USD 1.81 billion by 2031, growing at a CAGR of 5.23% from 2026 to 2031.

The market is expanding as fast-growing online retail volumes, wider digital-payment adoption, and new cross-border trade agreements shorten fulfillment cycles and push operators to build smarter, better-located facilities. [1] General Authority for Statistics, "Monthly Wholesale and Retail Indices," stats.gov.sa Investments are flowing into temperature-controlled buildings, last-mile dark stores, and AI-enabled inventory systems, while sovereign wealth funds continue to bankroll mega-logistics parks that integrate ports, airports, and free zones. This report is Segmented by Warehouse Type (Fulfilment Centers, Distribution Centers, and More), by Service Type (Storage, Picking & Packing, Value-Added Services), by Automation Level (Manual, Semi-Automated, Automated), by End-User Industry (Apparel & Footwear, Grocery & FMCG, and More), and by Geography (Saudi Arabia, and More). The Market Forecasts are Provided in Terms of Value (USD).

Middle East E-commerce Warehouse Market Trends and Insights

Expanding Digital-Payment Penetration Unlocking Prepaid Fulfillment Capacity

Digital wallets and buy-now-pay-later options have moved cash handling out of the warehouse and onto fintech rails. Prepaid orders reduce working-capital lockups, enable leaner safety stocks, and allow fulfillment teams to promise same-day dispatch without cash-on-delivery reconciliation steps. Lower theft risk and insurance premiums add a cost bonus, and banks' real-time confirmation APIs now trigger warehouse wave picking within minutes of checkout. Faster cash cycles are particularly evident in the UAE, where prepaid penetration already tops 70% of online orders, giving operators room to scale without proportional inventory buildup.

Regional Free-Trade Pacts Shrinking Intra-GCC Customs Cycle Times

The January 2025 expansion of the GCC Integrated Customs Tariff has turned formerly national networks into one regional pool. Harmonized codes and single-window clearance allow a fulfillment center in Riyadh to replenish shoppers in Kuwait or Oman in under 72 hours with no re-declaration paperwork. Saudi Arabia's 50-year tax exemptions inside new Special Integrated Logistics Zones accelerate the hub-and-spoke shift, while Dubai leverages its bonded corridors to keep ports and airports synchronized. Trade friction is falling fastest for high-velocity goods such as smartphones and fast fashion, giving operators new options to stock inventory once and sell it many times across the Gulf.

Scarcity of Grade-A Logistics Land Outside Free-Trade Zones Inflating Lease Premiums

Most modern warehouses sit inside free zones, and land beyond them often lacks height allowances, fire systems, or foreign-ownership clarity. Rents in Dubai's prime corridors rose by double digits in 2025 as supply lagged demand, pushing second-tier operators into outlying plots with weaker road links. Speculative developers are breaking ground, but permitting cycles take years, so capacity tightness will linger. Build-to-suit deals lock in tenants yet require long leases that smaller brands hesitate to sign, keeping market entry tough for new players.

Other drivers and restraints analyzed in the detailed report include:

- Post-Pandemic Shift Toward Online-First Grocery & Pharmacy Replenishment

- Plug-And-Play 4PL Control Towers Enabling SME Cross-Border Scaling

- Volatile Industrial Electricity Tariffs Eroding Cold-Chain Profit Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fulfillment centers accounted for 43.81% of the Middle East e-commerce warehousing market share in 2025, reflecting their role as multi-channel inventory pools that feed line-haul, parcel, and click-and-collect networks. Typically sized 10,000-50,000 m2, they sit on peri-urban land that balances rent with access to ports and highways. Operators outfit them with high-bay racking, mezzanines for value-added services, and WMS integrations that sync with carrier APIs. Demand is steady as merchants shift from single-store rooms to shared third-party sites where they gain scale without owning assets.

Urban dark stores and micro-fulfillment centers post the fastest growth at a 10.68% CAGR through 2031, driven by quick-commerce apps promising 30-minute grocery or pharmacy delivery. These 300-2,000 m2 nodes specialize in top-selling SKUs, use dense tote-based grids, and benefit from AI that predicts neighborhood demand by hour. The Middle East e-commerce warehousing market size for micro-fulfillment is still modest, yet land scarcity inside city limits has sparked creative solutions such as mall basements and rooftop conversions. Kuehne + Nagel's 23,000 m2 site in Dubai's EZDubai zone shows how legacy 3PLs mix large fulfillment halls with adjacent micro hubs to cover both bulk storage and ultrafast delivery.

Storage services generated 50.07% of the Middle East e-commerce warehousing market size in 2025, because e-commerce still rests on safe, climate-controlled inventory holding. Pallet positions, clear height, and fire protection remain the primary leasing criteria for most tenants. However, commoditization keeps margins thin, and operators search for stickier income streams. Value-added services, expanding at a 10.15% CAGR, include kitting, postponement manufacturing, personalized packaging, and photo studios. The Middle East e-commerce warehousing market size linked to such services rises as brands demand local customization to shorten supply chains and comply with language or regulatory labeling rules.

Expeditors' 23,200 m2 Dubai South facility illustrates the shift, offering order management, returns grading, and export documentation under one roof. Brands pay premiums for last-minute localization that enables region-specific launches or seasonal bundles. Picking and packing remain essential, yet automation here, voice-directed headsets, pick-to-light shelves, reduces labor minutes per order, focusing competitive positioning on higher-value assembly or customization tasks instead of basic cartons-in, cartons-out.

List of Companies Covered in this Report:

- Aramex

- DSV (Including DH Schenker)

- DHL Supply Chain

- UPS Supply Chain Solutions

- FedEx Logistics

- Gulf Warehousing Company

- Naqel Express

- RSA Global

- iMile

- J&T Express Middle East

- Wared Logistics

- SAL Saudi Logistics

- Bahri Logistics

- DP World Logistics

- Emirates Logistics

- Etihad Cargo Logistics

- Al-Futtaim Logistics

- AJEX

- GAC

- CMA CGM (Including CEVA Logistics)*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Digital-Payment Penetration Unlocking Prepaid Fulfillment Capacity

- 4.2.2 Regional Free-Trade Pacts Shrinking Intra-GCC Customs Cycle-Times

- 4.2.3 Post-Pandemic Shift Toward Online-First Grocery & Pharmacy Replenishment

- 4.2.4 Plug-And-Play 4PL Control-Towers Enabling SME Cross-Border Scaling

- 4.2.5 Rapid Rise of Circular-Economy Recommerce Platforms Spurring Dedicated Returns Hubs

- 4.2.6 AI-Driven Inventory-Prediction Engines Justifying High-Throughput Automation

- 4.3 Market Restraints

- 4.3.1 Scarcity of Grade-A Logistics Land Outside Free-Trade Zones Inflating Lease Premiums

- 4.3.2 Volatile Industrial Electricity Tariffs Eroding Cold-Chain Profit Margins

- 4.3.3 ESG Disclosure Mandates Escalating Capex for Solar-Powered & Carbon-Neutral Warehouses

- 4.3.4 Cash-On-Delivery Persistence Complicating Reverse-Logistics Flows & Cash Recovery

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Warehouse Rental Pricing Trends

5 Market Size & Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 Fulfilment Centres

- 5.1.2 Distribution Centres (DCs)

- 5.1.3 Cold-Chain Warehouses

- 5.1.4 Dark Stores / Micro-Fulfillment Centers

- 5.1.5 Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, etc.)

- 5.2 By Service Type

- 5.2.1 Storage

- 5.2.2 Picking & Packing

- 5.2.3 Value-Added Services and Others (Kitting, Labelling)

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-Automated

- 5.3.3 Automated

- 5.4 By End-User Industry

- 5.4.1 Apparel and Footwear

- 5.4.2 Consumer Electronics

- 5.4.3 Grocery and FMCG

- 5.4.4 Pharmaceuticals, Beauty and Wellness

- 5.4.5 Home Essentials and Furnishings

- 5.4.6 Others

- 5.5 By Country (Value)

- 5.5.1 United Arab Emirates

- 5.5.2 Saudi Arabia

- 5.5.3 Qatar

- 5.5.4 Kuwait

- 5.5.5 Bahrain

- 5.5.6 Oman

- 5.5.7 Egypt

- 5.5.8 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Aramex

- 6.4.2 DSV (Including DH Schenker)

- 6.4.3 DHL Supply Chain

- 6.4.4 UPS Supply Chain Solutions

- 6.4.5 FedEx Logistics

- 6.4.6 Gulf Warehousing Company

- 6.4.7 Naqel Express

- 6.4.8 RSA Global

- 6.4.9 iMile

- 6.4.10 J&T Express Middle East

- 6.4.11 Wared Logistics

- 6.4.12 SAL Saudi Logistics

- 6.4.13 Bahri Logistics

- 6.4.14 DP World Logistics

- 6.4.15 Emirates Logistics

- 6.4.16 Etihad Cargo Logistics

- 6.4.17 Al-Futtaim Logistics

- 6.4.18 AJEX

- 6.4.19 GAC

- 6.4.20 CMA CGM (Including CEVA Logistics)*

7 Market Opportunities and Future Outlook

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

歐洲化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

2026年全球多深度穿梭系統市場報告北美化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)義大利化學品倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)