|

市場調查報告書

商品編碼

2062053

印度倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Warehouse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

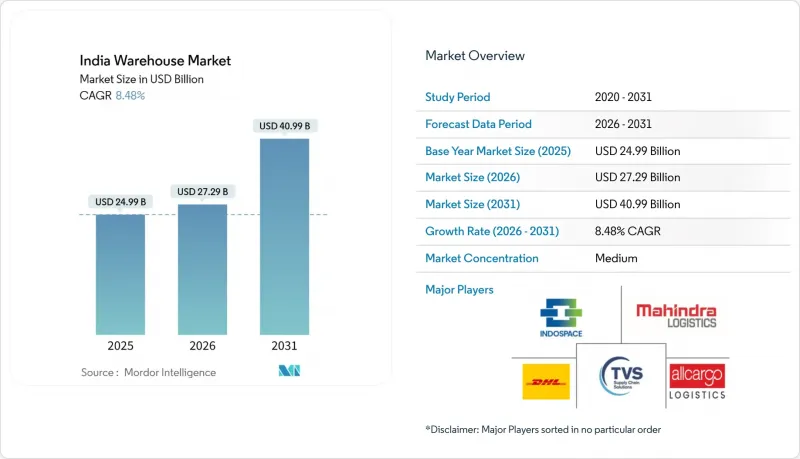

根據 Mordor Intelligence 預測,印度倉儲市場規模將從 2025 年的 249.9 億美元成長到 2026 年的 272.9 億美元,到 2031 年將達到 409.9 億美元,2026 年至 2031 年的複合年成長率為 8.48%。

本報告按倉庫類型(普通倉儲、冷藏倉儲)、等級(A級、B級、C級、非正規倉儲)、終端用戶行業(電子商務和零售、食品飲料、醫藥保健、其他)以及地區(印度北部、印度南部、印度西部、印度東部、印度中部)進行細分。市場預測以美元計價。

印度倉儲市場趨勢與洞察

國家物流政策(NLP-2022)實施

該計畫旨在2030年將物流成本降低至GDP的8%以下,從而刺激對標準化倉儲的投資。各邦的物流行動計劃(CLAP)引入了一站式清關服務,以縮短核准週期,尤其是在馬哈拉斯特拉邦拉邦、古吉拉突邦和泰米爾納德邦。 ULIP整合了36個中央和邦級系統,實現了貨物和運力的即時可見性,從而能夠為第三方物流營運商動態分配空間。在4,600億印度盧比的支持下,35個強制性多模態物流園區匯集了倉儲、海關和運輸樞紐,擴大了內陸可用位置的範圍。租戶可以受益於更快捷的鐵路和公路連接,從而減少整體停留時間並提高存貨周轉。

專用貨運走廊和多模態物流園區的運作

到2025年,西部和東部走廊的建設將完成96.4%,屆時每天將有352列貨運列車以100公里/小時的速度運行,德里至孟買以及魯迪亞納至加爾各答之間的運輸時間將縮短多達40%。租戶現在更傾向於選擇距離走廊交匯點30公里以內的位置,魯哈利和比萬迪強勁的需求吸收證明了這一點。開發商,例如IndoSpace佔地170萬平方英尺的比萬迪公園和Welspun One佔地120萬平方英尺的塔萊加翁項目,都特別強調了接近性DFC換乘站和規劃中的MMLP(多用途物流園區)的優勢。

延長環境影響評估和消防安全審核期限

面積超過2萬平方公尺的設施需要根據環境、森林和氣候變遷部(MoEFCC)的指導方針進行環境影響評估(EIA),這可能會使計畫推出期延長至多12個月。此外,高層倉庫建築必須符合基於2016年國家建築標準(NBC-2016)的嚴格噴灌和消防栓標準。為了減少延誤,開發商有時會將專案規模縮小到低於EIA要求,犧牲規模經濟效益。儘管2024年WDRA手冊旨在統一技術標準,但各邦對這些標準的採用情況卻不盡相同。

細分市場分析

截至2025年,普通倉儲將佔印度倉儲市場佔有率的60.01%,主要服務於電子商務、快速消費品和工程產品產業。受疫苗分發、快餐店擴張和生鮮食品出口的推動,冷藏倉儲預計將以12.94%的複合年成長率成長。 Snowman 物流在2026年3月將其在22個城市的托盤容量從154,330個增加到160,230個,並在普納和巴特那新增了倉儲設施。由於冷藏倉儲的合規要求更為嚴格,其租金溢價最高可達常溫倉儲的60%,入住率高達85-90%。因此,預計到2031年,印度倉儲市場中低溫運輸倉儲的規模將超過新增常溫倉儲的供應量。

製藥公司租戶要求倉儲環境符合世衛組織藥品生產品質管理規範 (WHO-GDP) 標準並接受持續監控,這有助於維持長期租賃關係,並為專業營運商帶來更高的獲利能力。普通倉儲依然重要,但商品同質化和微型市場的供應過剩抑制了租金上漲,迫使業主引入自動化和環境、社會及公司治理 (ESG) 功能。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 國家物流政策(NLP-2022)實施

- 專用貨運走廊和多模態物流園區的運作

- 生產連結獎勵計畫(PLI)計劃正在提振國內製造業的庫存需求。

- 由全通路零售驅動的分散式微型倉配中心

- 符合ESG標準的「綠色倉庫」認證數量激增,吸引了大量優質租戶。

- 電子商務退貨量的增加正在推動對逆向物流和退貨處理空間的需求。

- 市場限制因素

- 延長環境影響評估和消防安全審查

- 不穩定的電力供應會威脅自動化系統的運作,導致備用設備的投資增加。

- 倉庫自動化技術員短缺

- 倉庫火災和天氣風險正在推高保險費。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 倉庫類型細分

- 普通倉庫/存儲

- 冷藏倉庫和存儲

- 基於年級的分段

- A級

- B級

- C級和無組織

- 最終用戶行業細分

- 電子商務與零售

- 食品/飲料

- 製藥和醫療保健

- 車

- 製造工程產品

- 其他

- 區域分類

- 印度北部

- 德里首都區

- 旁遮普邦

- 哈里亞納邦

- 其他

- 南印度

- 卡納塔克邦

- 泰米爾納德邦

- 特倫甘納邦

- 其他

- 西印度群島

- 馬哈拉斯特拉邦

- 古吉拉突邦

- 其他

- 東印度

- 西孟加拉邦

- 奧里薩邦

- 其他

- 印度中部

- 中央邦

- 恰蒂斯加爾邦

- 印度北部

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mahindra Logistics

- Snowman Logistics

- IndoSpace

- DHL Group

- VRL Logistics Limited

- TVS Supply Chain Solutions

- Allcargo Logistics

- TCI Supply Chain Solutions

- Delhivery

- Safexpress

- LOGOS India

- Godamwale Logistic

- Warehouzez

- Ascendas Firstspace

- StarAgri Warehousing

- Blue Dart Express

- ColdEx Logistics

- Kintetsu World Express (India) Pvt. Ltd.

- XpressBees

- Apollo LogiSolutions*

第7章 市場機會與未來展望

According to Mordor Intelligence, the india warehouse market size is expected to grow from USD 24.99 billion in 2025 to USD 27.29 billion in 2026 and is forecast to reach USD 40.99 billion by 2031 at 8.48% CAGR over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing and Storage, Refrigerated Warehousing and Storage), by Grade (Grade-A, Grade-B, Grade-C and Unorganized), by End-User Industry (E-Commerce and Retail, Food and Beverage, Pharma and Healthcare, and More), and by Geography (North India, South India, West India, East India, Central India). The Market Forecasts are Provided in Terms of Value (USD).

India Warehouse Market Trends and Insights

Implementation of National Logistics Policy (NLP-2022)

The policy targets a logistics-cost reduction to below 8% of GDP by 2030, spurring organized warehousing investment. State-level CLAPs have introduced single-window clearances that shorten approval cycles, especially in Maharashtra, Gujarat, and Tamil Nadu. ULIP's integration of 36 central and state systems offers real-time visibility of cargo and capacity, enabling dynamic space allocation for 3PLs. The mandated 35 multi-modal logistics parks, backed by INR 46,000 crore, embed warehousing, customs, and transport nodes, widening the radius of feasible hinterland sites. Tenants gain faster access to rail-road interfaces, cutting overall dwell time and improving inventory turns.

Commissioning of Dedicated Freight Corridors & Multi-Modal Logistics Parks

By 2025, the Western and Eastern corridors reached 96.4% completion, enabling 352 daily freight trains running at 100 km/h and slicing Delhi-Mumbai and Ludhiana-Kolkata transit times by up to 40%. Occupiers now favor sites within 30 km of corridor nodes, evidenced by robust absorption in Luhari and Bhiwandi. Developer announcements, such as IndoSpace's 1.7 million sq ft Bhiwandi park and Welspun One's 1.2 million sq ft Talegaon project, specifically cite proximity to DFC interchanges and planned MMLPs.

Lengthy Environmental-Impact & Fire-Safety Clearance Timelines

Facilities exceeding 20,000 sq m require EIA approval under MoEFCC guidelines, extending project gestation by up to 12 months. High-rack structures also face strict sprinkler and hydrant compliance under NBC-2016. Developers sometimes phase projects below the EIA threshold to mitigate delays, sacrificing economies of scale. The 2024 WDRA handbook aims to harmonize technical norms, yet adoption varies across states.

Other drivers and restraints analyzed in the detailed report include:

- Production-Linked Incentive Schemes Boosting Manufacturing Inventory

- Omni-Channel Retail's Push for Decentralized Micro-Fulfilment Centers

- Intermittent Grid Power Jeopardizing Automation Uptime

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General warehousing and storage controlled 60.01% of India warehouse market share in 2025, serving e-commerce, FMCG, and engineering goods. Refrigerated warehousing is forecast to grow at 12.94% CAGR on the back of vaccine distribution, QSR expansion, and perishable exports. Snowman Logistics augmented capacity from 154,330 to 160,230 pallets across 22 cities by March 2026, adding new Pune and Patna sites. Refrigerated facilities command rent premiums of up to 60% over ambient warehouses and achieve 85-90% occupancy due to stringent compliance gaps. The India warehouse market size for the cold chain sub-segment is thus projected to outpace ambient space additions through 2031.

Pharmaceutical occupiers demand WHO-GDP-validated environments with continuous monitoring, sustaining long-duration leases and higher yields for specialized operators. General warehousing remains vital, but commoditization and micro-market oversupply temper rent growth, pushing landlords to retrofit automation and ESG features.

List of Companies Covered in this Report:

- Mahindra Logistics

- Snowman Logistics

- IndoSpace

- DHL Group

- VRL Logistics Limited

- TVS Supply Chain Solutions

- Allcargo Logistics

- TCI Supply Chain Solutions

- Delhivery

- Safexpress

- LOGOS India

- Godamwale Logistic

- Warehouzez

- Ascendas Firstspace

- StarAgri Warehousing

- Blue Dart Express

- ColdEx Logistics

- Kintetsu World Express (India) Pvt. Ltd.

- XpressBees

- Apollo LogiSolutions*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Implementation of National Logistics Policy (NLP-2022)

- 4.2.2 Commissioning of Dedicated Freight Corridors and Multi-Modal Logistics Parks

- 4.2.3 Production-Linked Incentive (PLI) Schemes Boosting Domestic Manufacturing Inventory Needs

- 4.2.4 Omni-Channel Retail's Push for Decentralized Micro-Fulfilment Centers

- 4.2.5 Surge in ESG-Compliant 'Green Warehouse' Certifications Attracting Premium Tenants

- 4.2.6 Reverse-Logistics & Returns-Processing Space Demand from Rising E-Commerce Returns

- 4.3 Market Restraints

- 4.3.1 Lengthy Environmental-Impact & Fire-Safety Clearance Timelines

- 4.3.2 Intermittent Grid Power Jeopardizing Automation Uptime, Raising Backup CAPEX

- 4.3.3 Shortage of Skilled Warehouse Automation Technicians

- 4.3.4 Insurance Premiums Escalating Due to Warehouse Fire-Load & Climate Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 Segmentation by Warehouse Type (Value)

- 5.1.1 General Warehousing and Storage

- 5.1.2 Refrigerated Warehousing and Storage

- 5.2 Segmentation by Grade (Value)

- 5.2.1 Grade-A

- 5.2.2 Grade-B

- 5.2.3 Grade-C & Unorganised

- 5.3 Segmentation by End-User Industry (Value)

- 5.3.1 E-commerce and Retail

- 5.3.2 Food and Beverage

- 5.3.3 Pharma and Healthcare

- 5.3.4 Automotive

- 5.3.5 Manufacturing and Engineering Goods

- 5.3.6 Others

- 5.4 Segmentation by Region (Value)

- 5.4.1 North India

- 5.4.1.1 Delhi-NCR

- 5.4.1.2 Punjab

- 5.4.1.3 Haryana

- 5.4.1.4 Others

- 5.4.2 South India

- 5.4.2.1 Karnataka

- 5.4.2.2 Tamil Nadu

- 5.4.2.3 Telangana

- 5.4.2.4 Others

- 5.4.3 West India

- 5.4.3.1 Maharashtra

- 5.4.3.2 Gujarat

- 5.4.3.3 Others

- 5.4.4 East India

- 5.4.4.1 West Bengal

- 5.4.4.2 Odisha

- 5.4.4.3 Others

- 5.4.5 Central India

- 5.4.5.1 Madhya Pradesh

- 5.4.5.2 Chhattisgarh

- 5.4.1 North India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Mahindra Logistics

- 6.4.2 Snowman Logistics

- 6.4.3 IndoSpace

- 6.4.4 DHL Group

- 6.4.5 VRL Logistics Limited

- 6.4.6 TVS Supply Chain Solutions

- 6.4.7 Allcargo Logistics

- 6.4.8 TCI Supply Chain Solutions

- 6.4.9 Delhivery

- 6.4.10 Safexpress

- 6.4.11 LOGOS India

- 6.4.12 Godamwale Logistic

- 6.4.13 Warehouzez

- 6.4.14 Ascendas Firstspace

- 6.4.15 StarAgri Warehousing

- 6.4.16 Blue Dart Express

- 6.4.17 ColdEx Logistics

- 6.4.18 Kintetsu World Express (India) Pvt. Ltd.

- 6.4.19 XpressBees

- 6.4.20 Apollo LogiSolutions*

7 Market Opportunities & Future Outlook

倉儲物流市場-2026-2032年全球市場預測

倉儲物流市場-2026-2032年全球市場預測 2026年全球自主移動機器人倉儲物流市場報告2026年全球座椅縫隙儲物盒市場報告2026年全球機器人分類系統市場報告

2026年全球自主移動機器人倉儲物流市場報告2026年全球座椅縫隙儲物盒市場報告2026年全球機器人分類系統市場報告 全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)2026年全球多深度穿梭系統市場報告

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)2026年全球多深度穿梭系統市場報告 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年) 按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)