|

市場調查報告書

商品編碼

2062188

北美倉儲與儲存:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Warehousing And Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

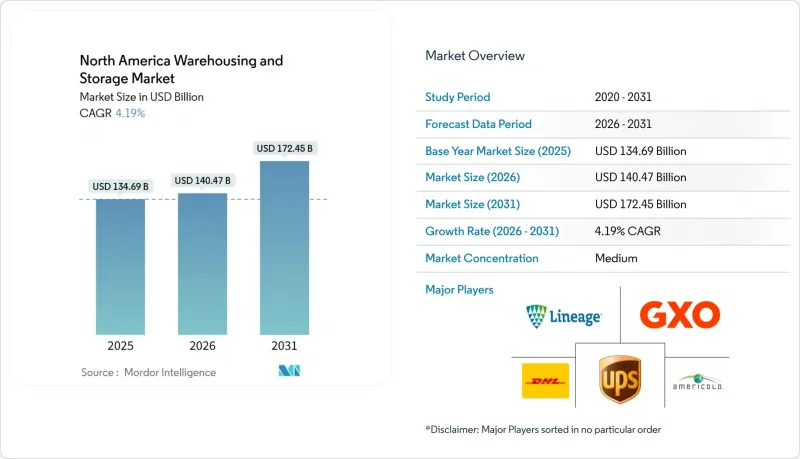

根據 Mordor Intelligence 預測,北美倉儲市場規模將從 2025 年的 1,346.9 億美元成長到 2026 年的 1,404.7 億美元,然後在 2031 年達到 1724.5 億美元,2026 年至 2031 年的複合成長率為 4.19%。

本報告按倉庫類型(普通倉儲、冷藏倉儲、農業倉儲)、終端用戶行業(電子商務和零售、食品飲料、汽車、製造和工程產品、其他)以及地區(美國、加拿大、墨西哥)進行細分。市場預測以美元(USD)為單位。

北美倉儲市場的趨勢和洞察。

全通路零售向當日送達轉型

為了因應更短的配送時間,零售商們正將庫存部署在距離市中心10英里(約16公里)的範圍內。亞馬遜位於賓州帝國市和愛達荷州南帕市的倉庫每天處理超過2萬份訂單,而沃爾瑪位於印第安納州麥科斯維爾市的220萬平方英尺(約20萬平方米)的配送中心則利用自動化倉庫系統(AS/RS)將揀貨到出貨的周期縮短至兩小時以內。面積小於5萬平方英尺(約4,600平方公尺)的末端配送設施空置率約4%,低於7.4%的全國平均。凱斯公司新近在豐塔納開設的20.97萬平方英尺(約19700萬平方米)的綜合設施,將小包裹分揀與當日送達的準備工作相結合,服務於內陸帝國地區的460萬居民。預計到2025年第一季,電子商務在美國零售總額中的滲透率將達到16%,屆時,無法獲得市中心空間的企業將面臨失去盈利的合約的風險,這些合約可能會被垂直整合的競爭對手搶走。

透過倉庫自動化和機器人化快速提高投資報酬率。

人事費用上升和設備價格下降已將機器人的投資回收期縮短至兩到三年。據物流稱,自主機器人已將處理能力提高了30%至40%,投資回收期不到36個月。盧卡斯系統公司的語音控制節流技術可將生產力提高20%至40%,同時降低10%至20%的人事費用。斯托德公司斥資4000萬美元擴建位於希伯倫的工廠,新增了52.5萬平方英尺的自動化分類設施,使中型貨運公司能夠以低於傳統成本結構的價格運作。主要限制因素是人員短缺。 64%的營運商難以招募維修技術人員,供應商被迫將服務人員納入多年合約中。

工業租金兩位數的成長給企業的利潤率帶來了壓力。

美國主要市場的租金預計將從2020年的每平方英尺8-10美元上漲到2025年的每平方英尺12-15美元,其中南加州的租金漲幅條款每年將超過8%。由此帶來的利潤率壓力正促使第三方物流(3PL)營運商遷往裡諾、鳳凰城和其他二線都會區,這些地區的土地成本比沿海主要樞紐低30-40%。然而,長途運輸導致的12-24小時配送時間增加正在威脅當日達服務。隨著租約在2026-2027年到期,25-35%的租金漲幅將迫使營運商精簡其資產組合,轉向自動化、高密度的設施。

細分市場分析

冷藏倉儲預計複合年成長率將達9.85%。這主要歸因於企業為滿足藥品低溫運輸需求以及生鮮食品線上銷售的成長而加大投入,冷藏倉儲租金已達每平方英尺12至15美元,而常溫倉儲租金僅為每平方英尺8至10美元。 NewCold位於賓州黎巴嫩的全自動化設施,其托盤密度比傳統速凍設施提高了30%;而EVERSANA位於孟菲斯的樞紐則將約20°C的儲存環境與人工智慧庫存管理系統相結合,用於生物類似藥的儲存。

儘管預計到2025年,普通倉儲仍將保持最大的市場佔有率,但隨著通用商品轉向高密度自動化設施,其在北美倉儲市場的佔有率(51.5%)正在萎縮。農產品倉儲仍然是一個小眾領域,僅限於中西部糧食走廊地區,該地區季節性波動會削弱自動化投資的回報。目前,資金正流入混合式設計,這種設計將常溫和冷藏區分隔在同一設施內,從而實現收入來源多元化並分散設施風險。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在全通路零售過渡到當日送達選項。

- 倉庫自動化和機器人技術的投資報酬率快速提升

- 美墨加協定實施後的免稅配額將促進跨境電子商務交易量的成長。

- 將閒置的購物中心改造成溫控物流中心

- 美國西岸港口電氣化津貼鼓勵利用棕地倉庫用地。

- 人工智慧驅動的動態插槽放置技術的應用,正在推動對儲存密度要求的提高。

- 市場限制因素

- 工業租金兩位數的成長給企業的利潤率帶來了壓力。

- 美國海關和邊防安全(CBP) 加強貨物檢查,導致跨境貨物吞吐量下降。

- 熟練的自動化工程師短缺,增加了停機風險。

- 市政當局禁止使用柴油場內卡車,這限制了該場地的生產力。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 倉庫類型

- 一般倉儲和存儲

- 冷藏倉庫存放與保鮮

- 農產品的倉儲儲存與保藏

- 按最終用戶行業分類

- 電子商務與零售

- 飲食

- 製藥和醫療保健

- 車

- 製造和工程產品

- 其他

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Lineage, Inc.

- Americold

- DHL Group

- GXO Logistics

- Prologis

- GEODIS

- Kenco Logistics

- FedEx

- UPS Supply Chain Solutions

- Penske Logistics

- Ryder System

- CMA CGM(Including CEVA Logistics)

- DSV

- United States Cold Storage(USCS)

- Saddle Creek Logistics Services

- NFI Industries

- CJ Logistics

- Kuehne+Nagel

- Radial Inc.(bpost group)

- Metro Supply Chain

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america warehousing and storage market size is expected to grow from USD 134.69 billion in 2025 to USD 140.47 billion in 2026 and is forecast to reach USD 172.45 billion by 2031 at 4.19% CAGR over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing and Storage, Refrigerated Warehousing and Storage, Farm Product Warehousing and Storage), by End-User Industry (E-Commerce and Retail, Food and Beverage, Automotive, Manufacturing and Engineering Goods, and More), and by Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Warehousing And Storage Market Trends and Insights

Omni-Channel Retail Shift to Same-Day Delivery Windows

Retailers now stage inventory within 10 miles of urban cores to meet shrinking delivery windows. Amazon's Imperial, Pennsylvania, and Nampa, Idaho sites each process 20,000-plus daily orders, while Walmart's 2.2 million square-foot McCordsville, Indiana hub uses automated storage and retrieval systems to cut pick-to-ship cycles below two hours. Vacancy in sub-50,000 square-foot last-mile facilities sits near 4% versus the 7.4% national average. Kase's new 209,700 square-foot Fontana complex integrates parcel sortation with same-day staging for 4.6 million Inland Empire residents. Operators unable to secure infill land risk ceding profitable contracts to vertically integrated rivals as e-commerce penetration climbed to 16% of United States retail sales in Q1 2025.

Rapid ROI Improvements in Warehouse Automation & Robotics

Payback periods for robotics have fallen to two to three years as labor costs soar and equipment prices drop. GXO Logistics reports 30-40% throughput gains from autonomous mobile robots with sub-36-month paybacks. Lucas Systems' voice-directed slotting delivers 20-40% productivity increases alongside 10-20% labor-cost reductions. Stord's USD 40 million Hebron expansion embeds 525,000 square feet of automated sortation, undercutting legacy cost structures for mid-market shippers. The primary constraint is talent: 64% of operators struggle to hire maintenance technicians, pushing vendors to embed service staff in multi-year contracts.

Double-Digit Industrial Rent Escalation Compressing Operator Margins

Asking rents in tier-one US markets reached USD 12-15 per square foot in 2025, up from USD 8-10 in 2020, while escalation clauses top 8% annually in Southern California. Resulting margin pressure pushes 3PLs toward Reno, Phoenix, and other secondary metros where land costs trail coastal gateways by 30-40%. Yet longer line-haul distances add 12-24 hours to delivery times, jeopardizing same-day offerings. Lease renewals coming due in 2026-2027 will impose 25-35% rent resets, forcing portfolio rationalization into automated, higher-density facilities.

Other drivers and restraints analyzed in the detailed report include:

- Post-USMCA Duty-Free Thresholds Boosting Cross-Border E-Commerce Flows

- Surplus Mall Conversions into Temperature-Controlled Distribution Nodes

- Enhanced CBP Cargo Screening Slowing Cross-Border Throughput

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated warehousing posted a 9.85% forecast CAGR, as operators chase pharmaceutical cold-chain mandates and fresh-food e-grocery flows, paying USD 12-15 per square foot in rent against ambient's USD 8-10. NewCold's fully automated Lebanon, Pennsylvania site delivers 30% higher pallet density compared with legacy blast-freeze layouts, while EVERSANA's Memphis hub aligns -20 °C storage with AI inventory for biosimilars.

General warehousing retains the largest 2025 footprint, yet its 51.5% North America warehousing and storage market share erodes as commodity SKUs migrate toward higher-density automated sites. Farm-product storage stays niche, limited to Midwest grain corridors where seasonal volatility undermines automation ROI. Capital now flows to hybrid designs that partition ambient and cold zones under one roof, capturing diverse revenue streams while diluting site risk.

List of Companies Covered in this Report:

- Lineage, Inc.

- Americold

- DHL Group

- GXO Logistics

- Prologis

- GEODIS

- Kenco Logistics

- FedEx

- UPS Supply Chain Solutions

- Penske Logistics

- Ryder System

- CMA CGM (Including CEVA Logistics)

- DSV

- United States Cold Storage (USCS)

- Saddle Creek Logistics Services

- NFI Industries

- CJ Logistics

- Kuehne + Nagel

- Radial Inc. (bpost group)

- Metro Supply Chain

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Omni-Channel Retail Shift to Same-Day Delivery Windows

- 4.2.2 Rapid ROI Improvements in Warehouse Automation & Robotics

- 4.2.3 Post-USMCA Duty-Free Thresholds Boosting Cross-Border E-Commerce Flows

- 4.2.4 Surplus Mall Conversions into Temperature-Controlled Distribution Nodes

- 4.2.5 US West-Coast Port Electrification Grants Opening Brownfield Warehouse Sites

- 4.2.6 AI-Driven Dynamic Slotting Increasing Storage-Density Requirements

- 4.3 Market Restraints

- 4.3.1 Double-Digit Industrial Rent Escalation Compressing Operator Margins

- 4.3.2 Enhanced CBP Cargo Screening Slowing Cross-Border Throughput

- 4.3.3 Shortage Of Skilled Automation Technicians Elevating Downtime Risk

- 4.3.4 Municipal Moratoria on Diesel Yard Trucks Limiting Site Productivity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Warehouse Type (Value)

- 5.1.1 General Warehousing and Storage

- 5.1.2 Refrigerated Warehousing and Storage

- 5.1.3 Farm Product Warehousing and Storage

- 5.2 By End-User Industry (Value)

- 5.2.1 E-commerce & Retail

- 5.2.2 Food & Beverage

- 5.2.3 Pharma & Healthcare

- 5.2.4 Automotive

- 5.2.5 Manufacturing & Engineering Goods

- 5.2.6 Others

- 5.3 By Geography (Value)

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Lineage, Inc.

- 6.4.2 Americold

- 6.4.3 DHL Group

- 6.4.4 GXO Logistics

- 6.4.5 Prologis

- 6.4.6 GEODIS

- 6.4.7 Kenco Logistics

- 6.4.8 FedEx

- 6.4.9 UPS Supply Chain Solutions

- 6.4.10 Penske Logistics

- 6.4.11 Ryder System

- 6.4.12 CMA CGM (Including CEVA Logistics)

- 6.4.13 DSV

- 6.4.14 United States Cold Storage (USCS)

- 6.4.15 Saddle Creek Logistics Services

- 6.4.16 NFI Industries

- 6.4.17 CJ Logistics

- 6.4.18 Kuehne + Nagel

- 6.4.19 Radial Inc. (bpost group)

- 6.4.20 Metro Supply Chain

7 Market Opportunities & Future Outlook

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告

2026年全球多深度穿梭系統市場報告 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年) 按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)亞太地區化學品倉儲市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)亞太地區化學品倉儲市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 全球按需倉儲市場:按組織、產業和地區分類-市場規模、產業動態、機會分析和預測(2026-2035 年)

全球按需倉儲市場:按組織、產業和地區分類-市場規模、產業動態、機會分析和預測(2026-2035 年)