|

市場調查報告書

商品編碼

2062049

美國化學品倉儲市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)United States Chemical Warehousing And Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

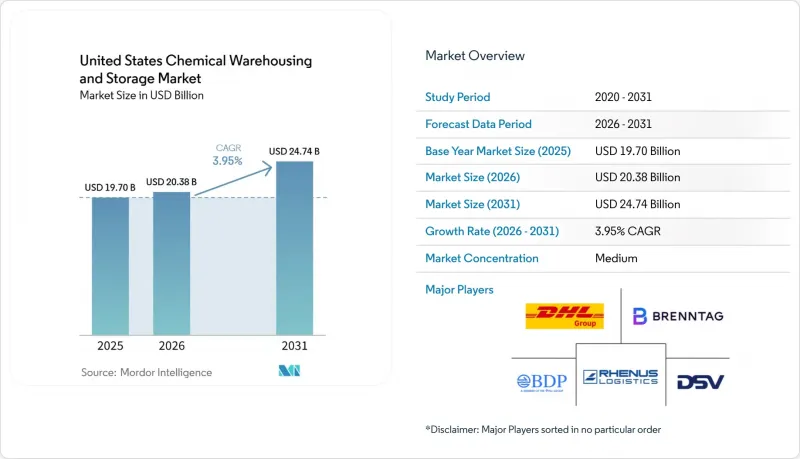

根據 Mordor Intelligence 預測,美國化學品倉儲市場規模將從 2025 年的 197 億美元成長到 2026 年的 203.8 億美元,到 2031 年達到 247.4 億美元,2026 年至 2031 年的複合年成長率為 3.95%。

本報告按倉庫類型(普通倉庫、特殊化學品倉庫等)、化學品類型(易燃液體、腐蝕性物質等)、終端用戶行業(基礎化學品製造、特種化學品製造等)和地區(東北部、中西部等)進行細分。市場預測以以金額為準呈現。

美國化學品倉儲市場趨勢與洞察

頁岩氣繁榮與石化產業的復甦

墨西哥灣沿岸新建和規劃中的裂解裝置正在滿足生產基地和出口走廊附近對危險品儲存設施的多年需求。信德能源在伊伯維爾帕里什(Iberville Parrish)投資34億美元建設的乙烯-氯-鹼聯合裝置預計將於2030年竣工,這意味著路易斯安那州的原料供應將支持產能的持續擴張。埃克森美孚正在考慮在科珀斯克里斯蒂附近建造一座乙烷裂解裝置和聚乙烯工廠,投資額高達86億美元。如果獲得批准,隨著聚合物和中間體產量的增加,對臨時儲存設施的需求推動要素需求的進一步上升。 Ventures Global已批准了卡梅倫帕里什(Cameron Parrish)投資86億美元的CP2項目,而切尼爾能源已申請在科珀斯克里斯蒂增建四條生產線,這將使尖峰時段產能每年增加2400萬噸。這些大型企劃需要將冷媒、腐蝕抑制劑和特殊製程化學品儲存在相鄰的地點,並進行嚴格的隔離和控制,同時進行即時庫存追蹤。出口物流正在推動這一周期,Energy Transfer 的 Flexport 和 Enterprise Products Partners 的擴張計劃正在塑造荷蘭和休士頓航道周圍的運轉率和即時庫存策略。

化工產品的近岸外包與回岸外包

對製藥和特種化學品的投資正在推動對靠近美國生產線的溫控倉儲設施和檢驗的品質系統的需求。大型製藥公司在其公佈的計劃中強調了活性成分(API)和注射劑產能的成長,這將需要符合GDP標準的倉儲設施和符合21 CFR Part 11標準的監控。經銷商的投資也反映了這一轉變;Cencora承諾到2030年投資10億美元用於其遍布全國的物流中心。這包括西海岸的擴張以及在阿拉巴馬州多森市加強低溫運輸,以滿足對需要在2-8攝氏度下儲存的產品日益成長的需求。網路整合也在推動生產回流,DSV將於2025年完成對DB Schenker的收購,以進一步擴展和標準化其區域間倉儲網路。區域營運商正在增加附加價值服務,例如港口拖車清潔和維護,以縮短液體散裝資產的周轉時間,隨著近岸外包的推進,這將進一步鞏固美國化學品倉儲市場。

用於處理危險物質的設施需要大量資本投資

危險物品倉庫的維修或新建需要大量資金投入,包括防火等級達120分鐘的建築結構、獨立的防漏區域、泡沫滅火系統和蒸氣控制系統。營運方也正在更新危險物品資訊與安全資料表 (SDS),以符合美國職業安全與健康管理局 (OSHA) 2024 年的最終規定,該規定要求在 2026 年 1 月前實現物質合規,在 2027 年 7 月前實現混合物合規。經濟影響評估表明,雖然一些標籤變更將減輕持續的合規負擔,但文件和標籤的修訂以及培訓將產生一次性成本。州和聯邦流程的變更,包括電子清單的使用和記錄保存,為系統和工作流程增加了新的操作流程,許多場所正在將這些流程與品管和倉庫管理系統 (WMS) 應用程式整合。儲存措施必須符合美國環保署 (EPA) 的二級防護要求,需要足夠的容量和合適的材料來抵禦洩漏和雨水。這會影響設施佈局和資本投資計劃。這些要求正在推高美國化學品倉庫和儲存市場中合規設施的溢價。在這個市場中,有據可查的安全記錄和檢查日誌對於保險承保和客戶審核至關重要。

細分市場分析

2025年,特種化學品倉庫將佔據市場主導地位,佔34.12%。這主要得益於配備防火牆、獨立防漏區和本質安全處理的專用設施,這些設施能夠在單一地點管理易燃、腐蝕性和氧化性物質,同時確保合規性。預計到2031年,溫控倉庫的複合年成長率將達到4.8%,成為成長最快的倉庫類型,因為生命科學產品的推出需要經過驗證的冷卻系統、冗餘電源以及符合21 CFR Part 11標準的記錄器。 DHL位於安維爾的100萬平方英尺的醫療保健中心採用符合GDP和GMP標準的管理模式,並擁有自由貿易區(FTZ)地位,旨在最佳化對時間要求嚴格的藥品物流的清關和關稅流程。在美國化學品倉庫和儲存市場,兼具安全性、品質和低溫運輸可靠性的設施租金高於一般工業倉庫。

整個場地內的危險物品倉庫將增強通風、洩漏預防措施和二次防護方案與相容的存放方式和定期培訓相結合。雖然共用場地的一般化學品儲存仍在處理非危險產品和成品,但成長最快的是結合自動化和符合稽核要求的文件的溫控環境。近期專案包括EVERSANA的孟菲斯物流中心,該中心利用人工智慧機器人和新的倉庫管理系統(WMS)擴大了冷藏容量,同時保持了準時交貨率。這些趨勢正在推動美國化學品倉儲產業對能夠大規模標準化危險物品管理和品質系統的多客戶場地的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 頁岩氣繁榮與石化產業的復興

- 化工製造領域的近岸外包與回岸外包

- 墨西哥灣沿岸石化出口碼頭擴建

- 特用化學品產量增加

- 化工製造商外包趨勢

- 與墨西哥和加拿大擴大化學品貿易

- 市場限制因素

- 用於處理危險物質的設施需要大量資本投資

- 訓練有素的危險物品處理人員嚴重短缺。

- 保險費和責任險飆升

- 主要港口和鐵路樞紐周邊土地短缺問題突出。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 將自動化整合到化學品庫存管理中

- 向多客戶共用化學品儲存模式過渡

第5章 市場規模與成長預測

- 倉庫類型

- 普通倉庫

- 特用化學品倉庫

- 危險品(HAZMAT)倉庫

- 溫控化學品倉庫

- 依化學類型

- 易燃液體

- 腐蝕性物質

- 危險物質

- 氧化劑

- 其他

- 按最終用戶行業分類

- 基礎化學製造

- 特種化學品製造

- 製藥和生命科學

- 農業化學品

- 油漆、塗料、黏合劑

- 食品/飼料添加劑

- 石油天然氣/石油化工

- 其他

- 按地區分類 - 美國

- 東北

- 中西部

- 東南

- 西南

- 西方

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- Brenntag North America

- Rhenus Logistics

- BDP International

- DSV

- CH Robinson

- XPO Logistics

- HOYER Group

- ADLI Logistics

- CEVA Logistics

- Quantix Supply Chain

- R&S Logistics

- Talke Logistics

- Hellmann Worldwide Logistics

- Yusen Logistics(part of NYK Line)

- Bertschi AG

- Kuehne+Nagel

- Den Hartogh Logistics

- Weber Hazmat Logistics

- Odyssey Logistics & Technology Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states chemical warehousing and storage market size is expected to increase from USD 19.70 billion in 2025 to USD 20.38 billion in 2026 and reach USD 24.74 billion by 2031, growing at a CAGR of 3.95% over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing, Speciality Chemical Warehouse, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Regions (Northeast, Midwest, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

United States Chemical Warehousing And Storage Market Trends and Insights

Shale Gas Boom and Petrochemical Renaissance

New and proposed Gulf Coast crackers anchor multi-year demand for hazmat-compliant storage near production centers and export corridors. Shintech's USD 3.4 billion ethylene and chlor-alkali complex in Iberville Parish targets 2030 completion, and signals sustained feedstock-backed capacity growth in Louisiana. ExxonMobil is evaluating an ethane cracker and polyethylene plant near Corpus Christi with a potential USD 8.6 billion capital plan, which, if approved, would expand staging needs for polymers and intermediates buildouts add further pull. Venture Global approved the USD 8.6 billion CP2 project in Cameron Parish, while Cheniere filed to add four Corpus Christi trains that would lift peak capacity by 24 mtpa. These energy megaprojects require adjacent storage of refrigerants, corrosion inhibitors, and specialty process chemicals under strict segregation with real-time inventory tracking. Export logistics reinforce the cycle, as Energy Transfer's Flexport and Enterprise Products Partners' expansions shape occupancy and just-in-time inventory strategies near Nederland and the Houston Ship Channel.

Nearshoring and Reshoring of Chemical Manufacturing

Pharmaceutical and specialty chemical investments increase demand for temperature-controlled storage and validated quality systems close to the United States manufacturing lines. Corporate plans disclosed by leading pharma manufacturers highlight expanded active pharmaceutical ingredients and injectable therapy capacity that will rely on GDP-compliant warehousing and 21 CFR Part 11-validated monitoring. Distributor investments mirror this shift, as Cencora committed USD 1 billion through 2030 across national hubs, including a West Coast expansion and a cold-chain scale-up at Dothan, Alabama, to meet the rise in products that need 2-to-8 degree Celsius storage. Network consolidation also supports reshoring, with DSV completing the DB Schenker acquisition in 2025, enhancing cross-regional warehousing reach and standardization. Regional operators add value-added services such as trailer wash and maintenance at ports to reduce cycle times for liquid-bulk assets, reinforcing the United States chemical warehousing and storage market as nearshoring advances.

High Capital Investment for Hazmat-Compliant Facilities

Upgrading or building hazmat-ready warehouses requires significant capital for 120-minute fire-rated construction, segregated bunded zones, and foam-deluge and vapor-control systems. Operators are also updating hazard communication and safety data sheets to align with OSHA's 2024 final rule, which sets substance compliance by January 2026 and mixture compliance by July 2027. Economic impact assessments indicate one-time costs for file and label revisions and training, even as certain labeling changes reduce recurring compliance burdens. State and federal process changes, including e-Manifest use and record retention, add system and workflow workstreams that many sites integrate with quality management and WMS applications. Storage practices must meet EPA secondary-containment expectations, with adequate capacity and compatible materials for spills and stormwater, which drives site layout and capex plans. These obligations reinforce premium pricing for compliant sites in the United States chemical warehousing and storage market, where documented safety and inspection logs are essential for insurability and customer audits.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Gulf Coast Petrochemical Export Terminals

- Rising Specialty Chemicals Production Volumes

- Acute Shortage of Trained Hazardous Material Handlers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty chemical warehouses led with 34.12% in 2025, reflecting purpose-built facilities with rated fire walls, segregated bunded zones, and intrinsically safe handling that allow flammables, corrosives, and oxidizers to be managed in a single site while maintaining compliance. Temperature-controlled warehouses post the fastest growth at a projected 4.8% CAGR to 2031 as life sciences launches require validated chillers, redundant power, and 21 CFR Part 11-validated data loggers. DHL's million-square-foot healthcare hub in Annville is designed with GDP and GMP controls and Foreign Trade Zone status to align customs and tariff processes with time-sensitive pharma flows. Facilities that can blend safety, quality, and cold-chain reliability sustain rent premiums that exceed general industrial levels in the United States chemical warehousing and storage market.

Across the base, hazardous material warehouses combine enhanced ventilation, spill containment, and secondary containment plans with compatibility-controlled storage and routine drills. General chemical storage in shared sites continues to serve non-hazmat products and finished goods, but the fastest growth sits in temperature-controlled settings that pair automation with audit-ready documentation. Recent projects include EVERSANA's Memphis distribution center using AI-enabled robotics and a new WMS to expand cold capacity while sustaining on-time delivery metrics. These patterns consolidate demand around multi-client nodes that can standardize hazard controls and quality systems at scale for the United States chemical warehousing and storage industry.

List of Companies Covered in this Report:

- DHL Group

- Brenntag North America

- Rhenus Logistics

- BDP International

- DSV

- C.H. Robinson

- XPO Logistics

- HOYER Group

- ADLI Logistics

- CEVA Logistics

- Quantix Supply Chain

- R&S Logistics

- Talke Logistics

- Hellmann Worldwide Logistics

- Yusen Logistics (part of NYK Line)

- Bertschi AG

- Kuehne + Nagel

- Den Hartogh Logistics

- Weber Hazmat Logistics

- Odyssey Logistics & Technology Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shale Gas Boom and Petrochemical Renaissance

- 4.2.2 Nearshoring and Reshoring of Chemical Manufacturing

- 4.2.3 Expansion of Gulf Coast Petrochemical Export Terminals

- 4.2.4 Rising Specialty Chemicals Production Volumes

- 4.2.5 Outsourcing Trend Among Chemical Manufacturers

- 4.2.6 Growing Cross-Border Chemical Trade with Mexico and Canada

- 4.3 Market Restraints

- 4.3.1 High Capital Investment for Hazmat-Compliant Facilities

- 4.3.2 Acute Shortage of Trained Hazardous Material Handlers

- 4.3.3 Escalating Insurance and Liability Premiums

- 4.3.4 Land Scarcity Near Major Port and Rail Terminals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Automation Integration in Chemical Inventory Management

- 4.9 Shift Toward Multi-Client Shared Chemical Storage Models

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Region - United States

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 Southeast

- 5.4.4 Southwest

- 5.4.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Brenntag North America

- 6.4.3 Rhenus Logistics

- 6.4.4 BDP International

- 6.4.5 DSV

- 6.4.6 C.H. Robinson

- 6.4.7 XPO Logistics

- 6.4.8 HOYER Group

- 6.4.9 ADLI Logistics

- 6.4.10 CEVA Logistics

- 6.4.11 Quantix Supply Chain

- 6.4.12 R&S Logistics

- 6.4.13 Talke Logistics

- 6.4.14 Hellmann Worldwide Logistics

- 6.4.15 Yusen Logistics (part of NYK Line)

- 6.4.16 Bertschi AG

- 6.4.17 Kuehne + Nagel

- 6.4.18 Den Hartogh Logistics

- 6.4.19 Weber Hazmat Logistics

- 6.4.20 Odyssey Logistics & Technology Corporation

7 Market Opportunities & Future Outlook

全球食品飲料倉儲市場。

全球食品飲料倉儲市場。 個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年)

個人及家庭服務機器人市場規模、佔有率及趨勢分析報告:按類型、技術、地區及細分市場分類(2026-2033 年) 2026年全球多深度穿梭系統市場報告

2026年全球多深度穿梭系統市場報告 化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年)

化學品倉儲市場報告:按類型、應用和地區分類(2026-2034年) 按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)亞太地區化學品倉儲市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

按需倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度倉儲市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國電子商務倉庫:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)亞太地區化學品倉儲市場:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 全球按需倉儲市場:按組織、產業和地區分類-市場規模、產業動態、機會分析和預測(2026-2035 年)

全球按需倉儲市場:按組織、產業和地區分類-市場規模、產業動態、機會分析和預測(2026-2035 年)