|

市場調查報告書

商品編碼

2061746

視訊串流軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Video Streaming Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

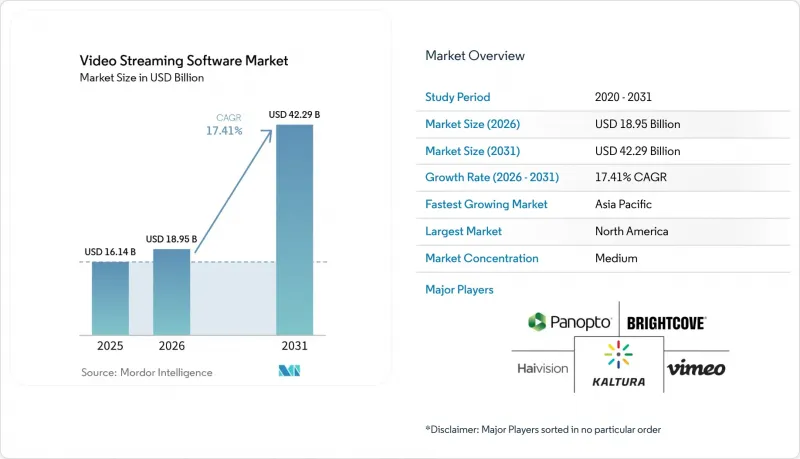

根據 Mordor Intelligence 估計,影片串流軟體市場規模從 2025 年的 161.4 億美元成長到 2026 年的 189.5 億美元,預計到 2031 年將達到 422.9 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 17.41%。

本報告按組件(解決方案、服務)、部署模式(雲端、本地部署)、串流媒體格式(直播、視訊點播)、產業(媒體娛樂、企業、其他)和地區進行細分。市場預測以美元計價。

全球視訊串流軟體市場趨勢及洞察

5G獨立組網的快速部署正在改變亞太地區的企業視訊使用方式。

在早期的製造先導計畫中,獨立組網5G的部署已將端對端延遲降低到10毫秒以下。工廠現在能夠將機器人焊接線上的多角度高清影像串流傳輸給遠端偵測人員,從而消除人工操作造成的延遲,確保生產持續進行。由於即使延遲降低不到一秒,也能轉化為每小時產量的提升,經營團隊正迅速將預算分配給視訊串流軟體市場,用於線上品質監控解決方案。這些新案例正在供應鏈聯盟中迅速傳播,並將目標需求擴展到早期智慧工廠採用者之外。

雲端原生微服務能夠加速北美OTT平台的功能迭代週期。

2024年,許多北美視訊串流服務供應商將原本的單體系統拆分成容器化的微服務,分別處理編碼、建議和伺服器端廣告插入等獨立工作負載。這使得營運商能夠僅擴展那些在高負載高峰期(例如直播名人訪談期間的建議)需要擴展的微服務,而不會對其他部分造成過大的成本。由此產生的「按需收費」模式減少了資源過度分配的需求,增加了研發投入,吸引了更多新用戶,並進一步推動了影片串流軟體市場的發展。

專利費上漲正促使獨立供應商採用開放式轉碼器。

與自我調整位元率相關的智慧財產權最低支付額的增加,迫使小眾服務提供者嘗試免版稅格式。一個學習管理平台調整了其比特率階梯,以抵消略微增大的文件大小並節省許可費用,從而保障了其毛利率。伺服器端偵測程式透過將不支援的裝置切換到較低的位元率來對沖不斷上漲的專利費率,但同時,它們也給影片串流軟體市場中那些最易受專利費影響的細分領域帶來了下行壓力。

細分市場分析

預計到2025年,解決方案收入將佔總收入的絕大部分,達到約89.3%。這是因為資產攝取、編碼和管理的核心平台在所有部署中仍然至關重要。隨著分析、AI縮圖和自動化品管(QC)等功能被添加到同一程式碼庫中,這個核心基礎設施將推動影片串流軟體市場的持續擴張。同時,業務收益預計將以20.9%的複合年成長率成長。這主要是由於不堪重負的IT部門將語音轉文字標記、事件驅動轉碼和零信任存取控制等複雜的整合任務外包出去。管理合約透過監控服務等級協定(SLA)的合規性和修復漏洞,提供了穩定且持續的收入來源。在整個預測期內,平台供應商和專業整合商之間的聯合銷售計劃將為視訊串流軟體市場帶來更多商機。

即使服務成長加速,擁有平台架構的供應商仍保持著定價權,因為一旦內容庫和業務邏輯整合完畢,客戶很少會更換平台。轉碼器的持續創新促使用戶定期升級,進而帶來合約續約。同時,分析插件為儀表板提供信息,將解約率與緩衝事件關聯起來。這些互動穩定了收入,即使服務生態系統蓬勃發展,解決方案層仍然是視訊串流軟體市場的核心。

預計到2025年,雲端部署將佔影片串流軟體市場規模的68.40%,年複合成長率達22.1%,因為越來越多的營運商需要具備強大的彈性容量來應對不可預測的流量高峰。邊緣節點現在能夠更靠近終端用戶執行即時打包和廣告決策處理,從而縮短啟動時間並減輕來源伺服器的負載。這種方法在2025年的音樂節上得到了驗證,即使在不穩定的行動電話網路條件下,多機位4K視訊串流的幀一致性也得以保持,這進一步增強了人們對影片串流軟體市場雲端邊緣架構的信心。

從資料主權或現有投資的角度來看,當需要本地處理時,本地部署解決方案仍然可行。銀行會在私有資料中心對高度敏感的董事會會議進行編碼,並將受DRM保護的視訊串流推送至外部CDN,供全球用戶播放。混合管道,例如本地採集、區域雲端轉碼和邊緣地理封鎖,使營運商能夠在合規性和擴充性之間取得平衡。儘管整合主機的普及意味著決策者越來越重視商業性考量而非架構理想,但與更廣泛的影片串流軟體市場一致的「雲端優先」策略的勢頭依然強勁。

區域分析

預計到2025年,北美將佔據視訊串流軟體市場37.60%的佔有率,主要得益於寬頻普及率、高密度超大規模容量以及向視訊優先工作流程的早期文化轉變。醫院正在為符合合規要求的檔案庫分配預算,將監管負擔轉化為搜尋的知識庫;而廣播公司正在整合預測分析功能以提高客戶維繫。一家上市供應商在2024年向美國證券交易委員會提交的文件證實,其策略已轉向自動化互動引擎,投資者對此表示歡迎,並提高了公司估值,這表明他們對差異化功能集而非同質化交付方式充滿信心。

亞太地區預計將以約19.4%的複合年成長率成長,這主要得益於行動優先的人口結構以及5G獨立組網解決方案的積極部署,旨在即使在農村地區也能提供高清、低延遲的體驗。各國政府正在津貼通訊基地台建設和本地內容製作,而特定語言的字幕和配音也成為標準的競標要求。服務供應商正在部署多租戶區域雲,這些雲共用控制平面,同時按國家/地區隔離工作負載,從而在兼顧合規性和規模經濟的同時,擴大了影片串流軟體的整體潛在市場規模。

在歐洲,消費者的高期望與嚴格的隱私權法律並存。 2024年的一項司法裁決促使各平台加快在歐盟境內建置資料中心,以確保個人識別資訊不會流出歐盟。英國一家廣播公司將超過7000小時的歷史內容遷移到雲端原生工作流程中,並行處理吞吐量因此提升了十倍。雖然初期成本激增,但處理時間的縮短使得「當日劇集交付」成為可能,而如今觀眾對此習以為常。廣告商資助的費率方案日益普及,推動了針對歐洲衡量框架最佳化的SSAI模組的需求,並擴大了影片串流軟體市場的區域商業機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 5G SA 網路的快速部署正在加速亞太地區對低延遲企業串流媒體的需求。

- 雲端原生微服務的採用正在推動北美SaaS OTT平台的發展。

- 歐洲企業在與混合辦公相關的全公司會議上的支出正在推動內部即時影片平台的成長。

- 中東地區具有購物功能的即時電商的興起,正在推動對互動串流媒體工具的需求。

- 美國醫療保險和醫療補助服務中心 (CMS) 的規定要求醫療領域必須進行安全的視訊和電視存檔。

- D2C體育賽事轉播權的轉變正在重振南美洲的多CDN編配。

- 市場限制因素

- 與自適應位元率相關的專利費飆升,給中小供應商帶來了壓力。

- GDPR/Schrems II 裁決設置了障礙,限制了歐盟內部影片資料的跨境流動。

- 非洲農村地區最後一公里網路擁塞正在破壞服務品質協定 (QoS SLA)。

- 免費增值平台上創作者的高流失率正在降低中小企業的平均每用戶收入(ARPU)。

- 監理展望

- 技術展望

- 波特五力模型

- 投資分析

- 價格分析

- 基於訂閱

- 廣告收入

- 按交易付費(按次付費)

- 混合/免費增值

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 視訊管理

- 轉碼和處理

- 影片發行和後製

- 影片分析

- 服務

- 專業服務

- 託管服務

- 解決方案

- 依部署類型

- 雲

- 現場

- 按串流媒體類型

- 居住

- 視訊點播

- 按行業

- 媒體與娛樂

- OTT平台

- 廣播電視網路

- 體育和電子競技

- 公司/企業

- 教育和數位學習

- 醫療保健和遠端醫療

- 銀行、金融服務和保險(BFSI)

- 其他行業

- 媒體與娛樂

- 按地區

- 北美洲

- 美國

- 加拿大

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 紐西蘭

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- Strategic Developments

- Vendor Positioning Analysis

- 公司簡介

- Brightcove Inc.

- Kaltura Inc.

- Amazon Web Services, Inc.(AWS Elemental)

- IBM Corporation

- Vimeo.com Inc.

- Panopto Inc.

- Haivision Systems Inc.

- Vbrick Systems Inc.

- Qumu Corporation

- Dacast

- Mux

- MediaPlatform, Inc.

- Bitmovin

- Akamai Technologies, Inc.

- Wowza Media Systems, LLC

- JW Player Inc.

- Google LLC(YouTube Live)

- Harmonic Inc.

- Telestream, LLC

- Cloudinary

- Synamedia Ltd.

- Verizon Media(Edgecast)

第7章 市場機會與未來展望

According to Mordor Intelligence, the video streaming software market size in 2026 is estimated at USD 18.95 billion, growing from 2025 value of USD 16.14 billion with 2031 projections showing USD 42.29 billion, growing at 17.41% CAGR over 2026-2031.

This report is Segmented by Component (Solutions, Services), Deployment Type (Cloud, On-Premise), Streaming Type (Live, Video On Demand), Vertical (Media and Entertainment, Corporate and Enterprise, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Video Streaming Software Market Trends and Insights

Rapid 5G stand-alone networks transforming enterprise video in Asia-Pacific

Standalone 5G roll-outs have pushed end-to-end latency below 10 milliseconds in early manufacturing pilots. Factories now stream multi-angle HD feeds from robotic welding lines to remote inspectors, eliminating manual lag and keeping production running. When every fractional second saved translates into extra units produced per hour, management quickly assigns a budget to the video streaming software market for inline quality monitoring solutions. Emerging case studies travel fast across supply-chain consortia, expanding addressable demand beyond initial smart-factory adopters.

Cloud-native microservices shortening feature cycles for North-American OTT platforms

In 2024, many North American providers decomposed monoliths into containerised microservices that handle encoding, recommendation, and server-side ad insertion as independent workloads. Operators can now dial up only the microservice that spikes, such as recommendations during a celebrity live interview, without overspending on the rest of the stack. The resulting pay-as-you-grow economics reduce over-provisioning, fuel incremental R&D allocations, and attract new subscribers, feeding additional momentum into the video streaming software market.

Patent royalty escalation motivating open codecs among independent vendors

Rising minimum payments for adaptive-bitrate IP compel niche providers to trial royalty-free formats. One learning-management platform offset marginally larger file sizes by re-balancing bitrate ladders, saving licence fees and protecting gross margin. Server-side detection routines down-switch devices that lack support, providing a hedge against royalty hikes, yet placing downward pressure on the video streaming software market in segments most exposed to patent fees.

Other drivers and restraints analyzed in the detailed report include:

- Corporate hybrid-work townhalls fuelling live-video platforms in Europe

- Interactive livestream shopping catalysing ultra-low-latency tools in the Middle East

- GDPR data-transfer rulings reshaping EU platform architectures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions contributed the larger slice of 2025 revenue, estimated at 89.3%, because every deployment still needs a platform core to ingest, encode, and manage assets. That core foundation keeps the video streaming software market expanding as feature road-maps layer analytics, AI thumbnails, and automated QC onto the same codebase. Services revenue, however, is forecast to climb at 20.9% CAGR as overstretched IT departments outsource complex integrations such as speech-to-text tagging, event-driven transcodings, and zero-trust access controls. Managed contract, then monitor SLA compliance and patch vulnerabilities, creating sticky annuity streams. Over the forecast horizon, joint go-to-market programmes between platform suppliers and specialised integrators will channel incremental opportunities back into the video streaming software market.

Even with faster services growth, vendors that own the platform architecture preserve pricing power because customers rarely re-platform once content libraries and business logic are embedded. Continuous codec innovation triggers periodic upgrades that renew contracts, while analytics plug-ins feed dashboards correlating churn to buffer events. The interplay stabilises revenue and keeps the solutions layer at the centre of the video streaming software market even as service ecosystems flourish in parallel.

Cloud deployment captured 68.40% of the video streaming software market size in 2025 and is projected to grow at a 22.1% CAGR as operators gravitate toward elastic capacity that accommodates unpredictable traffic spikes. Edge nodes now handle just-in-time packaging and ad decisioning nearer to end-users, reducing startup time and offloading origin servers. The approach shone during a 2025 music festival where multi-camera 4K streams retained frame integrity despite fluctuating cellular conditions, reinforcing trust in cloud-edge architectures within the video streaming software market.

On-premise solutions remain viable when data sovereignty or sunk investments dictate local processing. Banks encode sensitive board meetings inside private centres, then push DRM-protected ladders to external CDNs for worldwide playback. Hybrid pipelines, capture on-premise, transcode in regional clouds, enforce geo-blocking at the edge, let operators blend compliance with elasticity. As single-pane consoles converge, decision makers weigh commercial terms rather than architectural philosophy, yet the momentum still favours cloud-first strategies that align with the broader video streaming software market.

Geography Analysis

North America held 37.60% of the video streaming software market in 2025 due to widespread broadband, dense hyperscale capacity, and an early cultural shift toward video-first workflows. Hospitals budget for compliant archives that convert regulatory burdens into searchable knowledge bases, while broadcasters embed predictive analytics that improve customer retention. A publicly listed vendor's 2024 SEC filing confirmed a strategic pivot toward automated engagement engines, and investors rewarded the move with valuation gains, signalling confidence in differentiated feature sets over commoditised delivery .

Asia-Pacific is set for roughly 19.4% CAGR thanks to mobile-first demographics and aggressive 5G stand-alone coverage that brings high-resolution, low-latency experiences into rural districts. Governments subsidise tower build-outs and local content production, turning language-specific subtitles and dubbing into standard bid requirements. Providers deploy multi-tenant regional clouds that segregate workloads by country while sharing control planes, balancing compliance with economies of scale and enlarging the total addressable slice of the video streaming software market.

Europe blends advanced consumer expectations with stringent privacy laws. After 2024 judicial rulings, platforms accelerated data-centre build-outs inside the bloc to ensure personal identifiers never exit EU borders. A UK broadcaster's migration of 7,000-plus hours of heritage content into a cloud-native workflow yielded a ten-fold uptick in parallel processing throughput . Though upfront costs spiked, turnaround times shrink, enabling same-day episodic release that viewers now expect. Advertiser-funded tiers gain traction, driving demand for SSAI modules tuned to European measurement frameworks and enlarging the regional opportunity within the video streaming software market.

- Brightcove Inc.

- Kaltura Inc.

- Amazon Web Services, Inc. (AWS Elemental)

- IBM Corporation

- Vimeo.com Inc.

- Panopto Inc.

- Haivision Systems Inc.

- Vbrick Systems Inc.

- Qumu Corporation

- Dacast

- Mux

- MediaPlatform, Inc.

- Bitmovin

- Akamai Technologies, Inc.

- Wowza Media Systems, LLC

- JW Player Inc.

- Google LLC (YouTube Live)

- Harmonic Inc.

- Telestream, LLC

- Cloudinary

- Synamedia Ltd.

- Verizon Media (Edgecast)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid rollout of 5G SA networks accelerating low-latency enterprise streaming demand in Asia-Pacific

- 4.2.2 Cloud-native micro-services adoption boosting SaaS OTT platforms in North America

- 4.2.3 Corporate spend on hybrid-work townhalls fuelling internal live-video platforms in Europe

- 4.2.4 Shoppable livestream commerce uptake driving interactive streaming tools in the Middle East

- 4.2.5 US CMS rules mandating secure tele-video archiving in healthcare

- 4.2.6 D2C sports-rights migration energising multi-CDN orchestration in South America

- 4.3 Market Restraints

- 4.3.1 Escalating adaptive-bitrate patent royalties squeezing smaller vendors

- 4.3.2 GDPR / Schrems-II hurdles limiting EU cross-border video data flows

- 4.3.3 Rural last-mile congestion in Africa undermining QoS SLAs

- 4.3.4 High creator churn on freemium platforms eroding SMB ARPU

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis

- 4.8 Pricing Analysis

- 4.8.1 Subscription-based

- 4.8.2 Advertising-supported

- 4.8.3 Transaction-based (Pay-per-View)

- 4.8.4 Hybrid / Freemium

5 MARKET SIZE AND GROWTH FORECASTS (VALUE USD BILLION)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Video Management

- 5.1.1.2 Transcoding and Processing

- 5.1.1.3 Video Delivery and Post-Production

- 5.1.1.4 Video Analytics

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Type

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Streaming Type

- 5.3.1 Live

- 5.3.2 Video on Demand

- 5.4 By Vertical

- 5.4.1 Media and Entertainment

- 5.4.1.1 OTT Platforms

- 5.4.1.2 Broadcast and Cable TV Networks

- 5.4.1.3 Sports and Esports

- 5.4.2 Corporate and Enterprise

- 5.4.3 Education and eLearning

- 5.4.4 Healthcare and Telemedicine

- 5.4.5 Banking, Financial Services and Insurance (BFSI)

- 5.4.6 Other Verticals

- 5.4.1 Media and Entertainment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Latin America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Mexico

- 5.5.2.4 Rest of Latin America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Brightcove Inc.

- 6.3.2 Kaltura Inc.

- 6.3.3 Amazon Web Services, Inc. (AWS Elemental)

- 6.3.4 IBM Corporation

- 6.3.5 Vimeo.com Inc.

- 6.3.6 Panopto Inc.

- 6.3.7 Haivision Systems Inc.

- 6.3.8 Vbrick Systems Inc.

- 6.3.9 Qumu Corporation

- 6.3.10 Dacast

- 6.3.11 Mux

- 6.3.12 MediaPlatform, Inc.

- 6.3.13 Bitmovin

- 6.3.14 Akamai Technologies, Inc.

- 6.3.15 Wowza Media Systems, LLC

- 6.3.16 JW Player Inc.

- 6.3.17 Google LLC (YouTube Live)

- 6.3.18 Harmonic Inc.

- 6.3.19 Telestream, LLC

- 6.3.20 Cloudinary

- 6.3.21 Synamedia Ltd.

- 6.3.22 Verizon Media (Edgecast)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球視訊串流軟體市場:按產品/服務、串流媒體類型、觀看模式/設備、部署模式、產業和地區分類-預測至2031年

全球視訊串流軟體市場:按產品/服務、串流媒體類型、觀看模式/設備、部署模式、產業和地區分類-預測至2031年 影片串流軟體市場:2026-2032年全球市場預測(依內容類型、經營模式、平台、部署方式及最終用戶產業分類)

影片串流軟體市場:2026-2032年全球市場預測(依內容類型、經營模式、平台、部署方式及最終用戶產業分類) 影片串流軟體市場:按組件、串流媒體類型、部署方式、行業和地區分類

影片串流軟體市場:按組件、串流媒體類型、部署方式、行業和地區分類 2026年全球視訊串流軟體市場報告

2026年全球視訊串流軟體市場報告 影片串流軟體市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、設備、部署類型、最終用戶和解決方案分類

影片串流軟體市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、設備、部署類型、最終用戶和解決方案分類 影片串流軟體市場 - 全球產業規模、佔有率、趨勢、機會及預測(按解決方案、串流媒體、平台、服務類型、收入模式、部署類型、最終用戶、地區和競爭格局分類),2021-2031年

影片串流軟體市場 - 全球產業規模、佔有率、趨勢、機會及預測(按解決方案、串流媒體、平台、服務類型、收入模式、部署類型、最終用戶、地區和競爭格局分類),2021-2031年 影片串流軟體市場規模、佔有率和成長分析(按類型、解決方案、平台、服務業、收入模式、部署類型和地區分類)-2026-2033年產業預測

影片串流軟體市場規模、佔有率和成長分析(按類型、解決方案、平台、服務業、收入模式、部署類型和地區分類)-2026-2033年產業預測 影片串流軟體市場機會、成長要素、產業趨勢分析及2026年至2035年預測

影片串流軟體市場機會、成長要素、產業趨勢分析及2026年至2035年預測 視訊串流軟體市場:2025-2030 年預測

視訊串流軟體市場:2025-2030 年預測 影音串流軟體市場:各串流類型,各部署模式,不同企業規模,各業界,各地區,機會,預測,2017年~2031年

影音串流軟體市場:各串流類型,各部署模式,不同企業規模,各業界,各地區,機會,預測,2017年~2031年