|

市場調查報告書

商品編碼

2044284

英國陶瓷電容器(MLCC):市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)United Kingdom MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

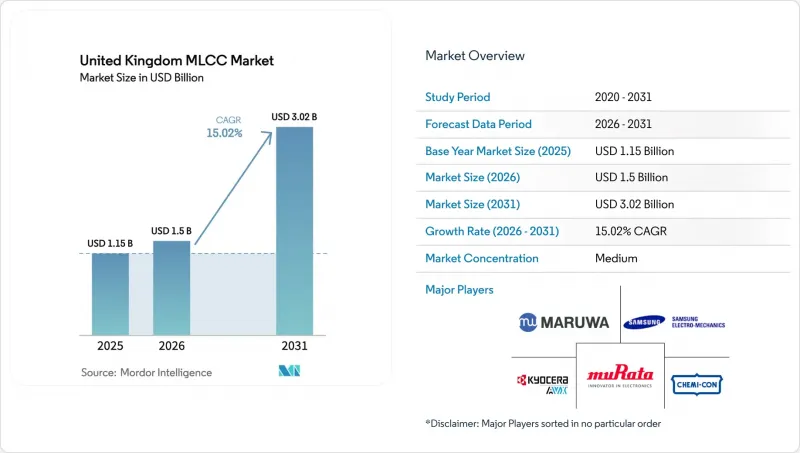

2025 年英國MLCC 市場價值為 11.5 億美元,預計到 2031 年將達到 30.2 億美元,而 2026 年為 15 億美元,預測期(2026-2031 年)複合年成長率為 15.02%。

零排放車輛的強力政策支援、自由港地區優惠的折舊免稅額規則以及AUKUS公司國防電子產品的在地採購,都促進了國內需求的成長。然而,全球供給能力緊張推高了平均售價,促使買家轉向雙重採購和緩衝庫存策略。為此,本地分銷商正在擴大靠近汽車和醫療設施的保稅庫存,以降低分配風險。同時,向800V汽車平台、小型化醫療植入和高頻5G無線技術的轉變,正推動產品結構向高壓、超高穩定性和超小型電容器傾斜。

英國MLCC市場趨勢與洞察

英國將於2030年禁止內燃機汽車(ICE),在此之前,電動車產量將激增。

英國汽車製造商正在擴大電動車 (EV) 的生產規模,為 2030 年內燃機 (ICE) 禁令做準備,每輛車的電容器數量幾乎增加了兩倍。塔塔集團在薩默塞特郡和 AESC 在桑德蘭投資建設的超級工廠,為當地的電池和電力電子生態系統奠定了基礎,並推動了英國多層陶瓷電容器 (MLCC) 市場的認證工作。總額達 25 億英鎊的「DRIVE35」計畫已撥款 26 億美元用於電力電子供應鏈的資本投資,這表明這種刺激措施將會持續下去。由於每輛電動車大約需要 1 萬個電容器,並且隨著 800V 架構的普及,其耐壓需求也進一步提高。當地分銷商目前正在西米德蘭茲郡的原始設備製造商 (OEM) 工廠附近儲備保稅庫存,以減輕來自亞洲的供不應求的影響。這些發展共同推動了英國MLCC 市場的成長前景。

5G部署的加速將提振小型基地台的需求。

通訊業者正利用數千個小型基地台提高其5G網路的密度,每個基地台都配備數十個0201和0402封裝的電容器,以實現高頻旁路功能。英國通訊管理局(Ofcom)的「互聯國家」(Connected Nations)數據顯示,倫敦、曼徹斯特和伯明罕等都市區的網路覆蓋範圍正在迅速擴大。村田製作所2025會計年度上半年的電容器銷售量年增9%,部分原因是通訊領域的訂單。隨著功率密度的提高,設計人員更傾向於使用X7R和X5R介質材料,這些材料即使在偏壓下也能提供穩定的電容值,並且他們優先選擇擁有先進材料技術的供應商。因此,通訊網路的擴張進一步推動了英國多層陶瓷電容器(MLCC)市場的發展。

MLCC 的供需失衡狀況持續存在,導致前置作業時間延長。

對人工智慧 (AI) 伺服器的需求已將村田製作所的全球運轉率推至近 95%,導致其緩衝庫存告罄。分配風險迫使英國買家接受更長的合約期限或在現貨市場支付溢價。需要可追溯批次的汽車和國防相關項目受到的衝擊最大。一些一級供應商目前正使用聚合物混合電容器或薄膜電容器作為雙電源,但高昂的重新認證成本阻礙了向替代方案的轉變。

細分市場分析

到2025年,2類MLCC將佔英國MLCC市場佔有率的45.72%,主要由高容量的X7R和X5R等級組成。它們的優勢在於體積效率高,使其適用於消費性電子和工業基板上的去耦和儲能應用。然而,由於汽車逆變器、雷達模組和嵌入式設備優先考慮劣化接近零且公差嚴格的產品,預計到2031年,1類C0G和NP0組件的複合年成長率將達到15.42%。因此,英國用於精密定時和感測電路的MLCC市場正在向1類技術轉型。

供應商正在擴展其高壓1類產品線,其中包括TDK的3225型10nF、1250V C0G電容。汽車工程師優先考慮偏壓下電容的穩定性,以確保電池管理的精確度,而醫療設備製造商則要求電容在數十年內保持溫度不變。儘管每微法成本較高,但這些特性使得1類元件在設計上廣泛應用,並鞏固了其在英國醫療設備(MLCC)市場的領先地位。

到2025年,402尺寸的MLCC將佔英國MLCC市場佔有率的37.29%,這反映了貼片良率和電容裕度之間的平衡。然而,由於5G無線電和血糖值貼片等應用中基板面積的限制,201尺寸的MLCC市佔率正以15.83%的複合年成長率成長。諸如TDK的1608封裝電容器等技術進步,使得設計人員能夠在更小的安裝面積內實現相同的電容值。 1608封裝電容器在100V電壓下電容值提高了10倍。

隨著邏輯電路向晶片封裝轉型,被動元件的面積進一步縮小,推動了對更小尺寸元件的需求。在英國多層陶瓷電容器(MLCC)市場,預計醫療穿戴式裝置和通訊小型基地台領域對201和01005尺寸元件的需求成長最為迅速。同時,汽車電力電子基板仍使用大於1210尺寸的元件來承受漣波電流。這種兩極化的需求使得供應商必須提供各種尺寸的封裝。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 英國計劃在2030年禁止銷售內燃機汽車(ICE),在此之前,電動車製造業將迎來一波激增。

- 5G基礎設施部署的加速將提升小型基地台的需求。

- 對小型穿戴式醫療設備和植入式醫療設備的需求不斷成長

- 政府對被動元件國內生產的稅收優惠政策

- 電池管理系統設計正朝著更高容量的方向發展。

- 透過AUKUS和英國國防部的舉措,實現國防電子設備的在地化

- 市場限制因素

- MLCC 的供需失衡狀況持續存在,導致前置作業時間延長。

- 鎳和銅價格的波動給利潤率帶來了壓力。

- 新製造項目面臨的監管障礙(規劃和ESG)

- HDI PCB中嵌入式電容器的更換工作正在進行中。

- 價值鏈分析

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按介電類型

- 一年級

- 二年級

- 按箱尺寸

- 0201

- 0402

- 0603

- 1005

- 1210

- 其他

- 透過電壓

- 低電壓(100V 或以下)

- 中壓(100-500V)

- 高壓(超過500伏特)

- MLCC安裝類型

- 金屬帽

- 徑向引線

- 表面黏著技術

- 透過最終用戶應用程式

- 航太/國防

- 車

- 家用電器

- 工業的

- 醫療設備

- 電力/公共產業

- 溝通

- 其他終端用戶應用程式

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Kyocera AVX Components Corporation

- MARUWA Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Samwha Capacitor Co., Ltd.

- TAIYO YUDEN Co., Ltd.

- TDK Corporation

- Vishay Intertechnology, Inc.

- Walsin Technology Corporation

- Worth Elektronik GmbH and Co. KG

- Yageo Corporation

- Panasonic Industry Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- KEMET Corporation

- Darfon Electronics Corp.

- Shenzhen Sunlord Electronics Co., Ltd.

- Exxelia Group

- Knowles Precision Devices

- NIC Components Corp.

第7章 市場機會與未來展望

The United Kingdom MLCC market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.50 billion in 2026 to reach USD 3.02 billion by 2031, at a CAGR of 15.02% during the forecast period (2026-2031).

Solid policy support for zero-emission vehicles, favorable capital-allowance rules inside Freeport zones, and defense-electronics localisation under AUKUS together energize local demand. Tight global capacity, however, continues to lift average selling prices, nudging buyers toward dual-sourcing and buffer-stock strategies. Local distributors are responding by expanding bonded inventory close to automotive and medical hubs to limit allocation risk. At the same time, the pivot to 800-volt vehicle platforms, miniaturised medical implants, and high-frequency 5G radios is tilting the product mix toward high-voltage, ultra-stable, and ultra-small capacitors.

United Kingdom MLCC Market Trends and Insights

Surge in EV Manufacturing Ahead of the 2030 UK ICE Ban

United Kingdom vehicle makers are scaling up electric-vehicle output to meet the 2030 ban on internal-combustion engines, lifting per-car capacitor content roughly threefold. Gigafactory investments by Tata in Somerset and AESC in Sunderland anchor local battery and power-electronics ecosystems, pulling qualification work into the United Kingdom MLCC market. The GBP 2.5 billion DRIVE35 program earmarks USD 2.6 billion for capital expenditure on power-electronics supply chains, signaling continued policy pull. Each electric vehicle contains about 10,000 capacitors, and design migration to 800-volt architectures further raises voltage-rating requirements. Local distributors now maintain bonded stock near West Midlands OEM sites to avoid Asian allocation shocks. These moves jointly amplify the growth outlook of the United Kingdom MLCC market.

Accelerated 5G Roll-Out Boosting Small-Cell Demand

Telecom operators are densifying 5G networks with thousands of small-cell base stations, each loaded with dozens of 0201 and 0402 capacitors for high-frequency bypass functions. Ofcom's Connected Nations data confirms rapid urban coverage expansion in London, Manchester, and Birmingham. Murata's capacitor revenue rose 9% year on year in the first half of fiscal 2025, driven partly by telecommunications orders. As power density climbs, designers prefer X7R and X5R dielectrics with stable capacitance under bias, and they favor suppliers with advanced material know-how. This telecom build-out therefore feeds an incremental tailwind into the United Kingdom MLCC market.

Persistent MLCC Supply-Demand Imbalance Inflating Lead-Times

Artificial-intelligence server demand has pushed Murata's global utilisation towards 95%, draining buffer inventory. Allocation risk forces UK buyers to accept longer contract horizons or pay premiums on the spot market. Automotive and defense programs that need traceable lots face the greatest exposure. Some tier-1s now dual-source with polymer hybrids or film capacitors, but re-qualification costs remain high, tempering substitution.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Compact Medical Wearables and Implantables

- Government Tax Incentives for On-Shore Passive-Component Production

- Nickel and Copper Price Volatility Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class 2 compositions held 45.72% of the United Kingdom MLCC market share in 2025, anchored by high-capacitance X7R and X5R grades. Their dominance comes from volumetric efficiency that suits decoupling and energy-storage tasks across consumer and industrial boards. However, Class 1 C0G and NP0 parts are projected to expand at a 15.42% CAGR through 2031 as automotive inverters, radar modules, and implantables prioritize near-zero aging and tight tolerance. The United Kingdom MLCC market for precision timing and sensing circuits is therefore tilting toward Class 1 technology.

Suppliers are widening high-voltage Class 1 offerings, such as TDK's 10 nF, 1,250 V C0G in 3225 format. Automotive engineers value stable capacitance under bias for battery-management accuracy, while medical device makers need temperature-invariant behavior over decades. These attributes let Class 1 parts capture design wins even where their cost per microfarad is higher, reinforcing their forecast outperformance in the United Kingdom MLCC market.

The 402 size accounted for 37.29% of the United Kingdom MLCC market share in 2025, reflecting its balance of pick-and-place yield and capacitance headroom. Yet board-area scarcity in 5G radios and glucose patches is driving a 15.83% CAGR for the 201 format. Designers can now achieve the same capacitance in fewer footprints due to breakthroughs such as TDK's 1608 case capacitors with tenfold capacitance gains at 100 V.

As more logic shifts to chiplet packages, the passive placement area shrinks further, raising demand for smaller formats. The United Kingdom MLCC market size allocated to 201 and even 01005 footprints will likely rise fastest in medical wearables and telecom small cells. In contrast, power-electronics boards in vehicles still rely on 1210 or larger parts for ripple-current handling. This dual-track demand keeps a broad case-size portfolio essential for suppliers.

The United Kingdom MLCC Market Report is Segmented by Dielectric Type (Class 1 and Class 2), Case Size (201, 402, 603, 1005, 1210, and Other Case Sizes), Voltage (Low Voltage, Mid Voltage, and High Voltage), MLCC Mounting Type (Metal Cap, Radial Lead, and Surface Mount), End-User Application (Aerospace and Defence, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Kyocera AVX Components Corporation

- MARUWA Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Samwha Capacitor Co., Ltd.

- TAIYO YUDEN Co., Ltd.

- TDK Corporation

- Vishay Intertechnology, Inc.

- Walsin Technology Corporation

- Worth Elektronik GmbH and Co. KG

- Yageo Corporation

- Panasonic Industry Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- KEMET Corporation

- Darfon Electronics Corp.

- Shenzhen Sunlord Electronics Co., Ltd.

- Exxelia Group

- Knowles Precision Devices

- NIC Components Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV Manufacturing Ahead of 2030 UK ICE-Ban

- 4.2.2 Accelerated 5G Infrastructure Roll-Out Boosting Small-Cell Demand

- 4.2.3 Rising Demand for Compact Medical Wearables and Implantables

- 4.2.4 Government Tax Incentives for On-Shore Passive Component Production

- 4.2.5 Battery Management-System Design Shifts to Higher Capacitance

- 4.2.6 Defence Electronics Localisation under AUKUS and UK MoD Initiatives

- 4.3 Market Restraints

- 4.3.1 Persistent MLCC Supply-Demand Imbalance Inflating Lead-Times

- 4.3.2 Nickel and Copper Price Volatility Squeezing Margins

- 4.3.3 Regulatory Hurdles for New Fab Construction (Planning and ESG)

- 4.3.4 Growing Substitution by Embedded Capacitors in HDI PCBs

- 4.4 Value-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Dielectric type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 By Case Size

- 5.2.1 0201

- 5.2.2 0402

- 5.2.3 0603

- 5.2.4 1005

- 5.2.5 1210

- 5.2.6 Other Case Sizes

- 5.3 By Voltage

- 5.3.1 Low Voltage (Less Than or Equal to 100 V)

- 5.3.2 Mid Voltage (100-500 V)

- 5.3.3 High Voltage (Greater Than500 V)

- 5.4 By MLCC Mounting Type

- 5.4.1 Metal Cap

- 5.4.2 Radial Lead

- 5.4.3 Surface Mount

- 5.5 By End-User Application

- 5.5.1 Aerospace and Defense

- 5.5.2 Automotive

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial

- 5.5.5 Medical Devices

- 5.5.6 Power and Utilities

- 5.5.7 Telecommunication

- 5.5.8 Other End-User Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Kyocera AVX Components Corporation

- 6.4.2 MARUWA Co., Ltd.

- 6.4.3 Murata Manufacturing Co., Ltd.

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics Co., Ltd.

- 6.4.6 Samwha Capacitor Co., Ltd.

- 6.4.7 TAIYO YUDEN Co., Ltd.

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology, Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Worth Elektronik GmbH and Co. KG

- 6.4.12 Yageo Corporation

- 6.4.13 Panasonic Industry Co., Ltd.

- 6.4.14 Holy Stone Enterprise Co., Ltd.

- 6.4.15 KEMET Corporation

- 6.4.16 Darfon Electronics Corp.

- 6.4.17 Shenzhen Sunlord Electronics Co., Ltd.

- 6.4.18 Exxelia Group

- 6.4.19 Knowles Precision Devices

- 6.4.20 NIC Components Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

用於MLCC內電極的鎳漿-2026年至2032年全球市佔率及排名、總收入及需求預測

用於MLCC內電極的鎳漿-2026年至2032年全球市佔率及排名、總收入及需求預測 日本積層陶瓷電容(MLCC)市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

日本積層陶瓷電容(MLCC)市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 用於MLCC電極的鎳漿(<200nm)—全球市場佔有率和排名、總收入和需求預測(2025-2031年)MLCC鎳內電極膏:全球市佔率排名、總銷售額及需求預測,2025-2031年中國MLCC市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)中壓MLCC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太地區MLCC:市場佔有率分析、產業趨勢與成長預測(2025-2030年)個人電腦和筆記型電腦用 MLCC——市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)北美MLCC:市場佔有率分析、產業趨勢與成長預測(2025-2030年)印度MLCC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

用於MLCC電極的鎳漿(<200nm)—全球市場佔有率和排名、總收入和需求預測(2025-2031年)MLCC鎳內電極膏:全球市佔率排名、總銷售額及需求預測,2025-2031年中國MLCC市場佔有率分析、產業趨勢與統計、成長預測(2025-2030年)中壓MLCC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太地區MLCC:市場佔有率分析、產業趨勢與成長預測(2025-2030年)個人電腦和筆記型電腦用 MLCC——市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)北美MLCC:市場佔有率分析、產業趨勢與成長預測(2025-2030年)印度MLCC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)